Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube.

In today’s edition of The Daily Brief:

- What does the IMF’s India report card say?

- Are loan recoveries going up?

What does the IMF’s India report card say?

Last month, the IMF just published a massive report on India’s financial system. This isn’t one of its regular, surface-level economic updates either — it’s a deep dive into the very plumbing of our financial system, and how resilient it is.

Why is the IMF doing this? See, India’s financial system, according to the IMF, is “systemically important .” That is to say: we’re big, and we’re deeply enmeshed in global finance. People from all over the world invest in India, lend to India, trade with India, and have all sorts of financial relationships with us.

That’s a fantastic thing, but for the rest of the world, it’s also a source of risk. Because of how densely interconnected the financial world is, small ruptures in one corner of the world can send dominoes tumbling everywhere. And because of our deep relationship with global finance, those ruptures can begin in India as well. When something trips up in our markets, the ripple effects could touch other parts of global finance. And so, the whole world has an interest in making sure that India’s financial markets are safe and well-run.

That’s why the IMF, under its Financial Sector Assessment Program (FSAP), takes a thorough look at financial sectors of important countries like India. The IMF is basically trying to answer one question: in a doomsday scenario, could a system-wide panic wreck our financial system? Could we be the source of the next global financial contagion? These ‘black swan’ events happen every once in a while: take the 2008 financial crisis, or the 2013 taper tantrum. How vulnerable might we be in the face of one?

Today, we look into what its latest report says.

First, the good news

The IMF’s assessment of our financial system is actually quite positive!

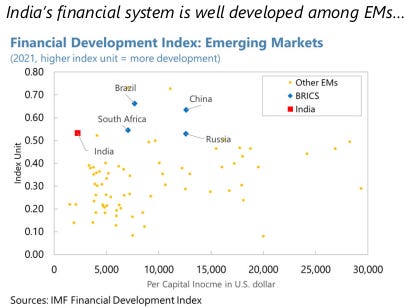

Since the last FSAP, in 2017, India has made real progress on financial stability. We’ve cleaned up our banking sector. Our NBFCs, after wobbling in 2018-19, are now bigger, more diversified, and are better regulated than ever before. And our ‘digital public infrastructure’ — UPI, Aadhaar, e-KYC, account aggregators etc. — is genuinely world-leading. In fact, for our low per capita income, Indian finance is remarkably well developed.

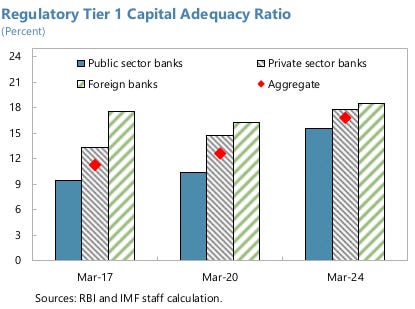

Our banks have enough capital to take a few hits. Their ‘Capital Adequacy Ratios’ — the buffers banks keep to absorb potential losses — have improved across the board. In 2018, they hovered around 14%; today, they’re comfortably over 17%.

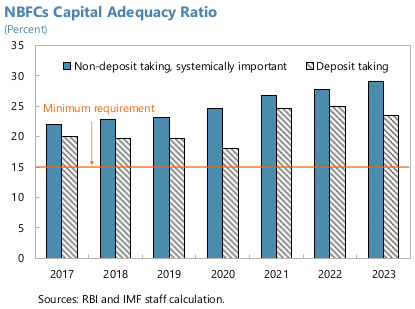

Non-bank financial companies, too, do well on this front, having gone from 23% to over 26% since the last FSAP. At least on paper, both sectors can handle serious stress.

In fact, NBFCs have grown substantially since the last FSAP. They now provide nearly half the private credit in the country. And unlike before, where even large NBFCs operated with little oversight, the RBI now regulates them through a “scale-based” framework. Larger and more complex NBFCs are subject to tighter scrutiny, capital norms, and disclosure rules — perhaps a lesson we learnt after 2018’s liquidity crunch, which brought IL&FS and DHFL to their knees.

It’s not just NBFCs, though. Financial institutions of all kinds have grown stronger — from mutual funds, to insurance, to stock markets. India has made strides in financial inclusion. 80% of all adult Indians have financial accounts. And our digital infrastructure is second to none.

In short, India’s financial system looks robust. We have the raw materials for stability, depth, and inclusion. Of course, that doesn’t mean we’re bulletproof.

Now, the bad news

Sadly, a good financial system isn’t a perfect one. We aren’t immune to risk. There are still issues that could come out of the blue and sow system-wide chaos. There are many issues that the IMF points to. While we recommend you go through them in detail, here are the three biggest ones that caught our eye.

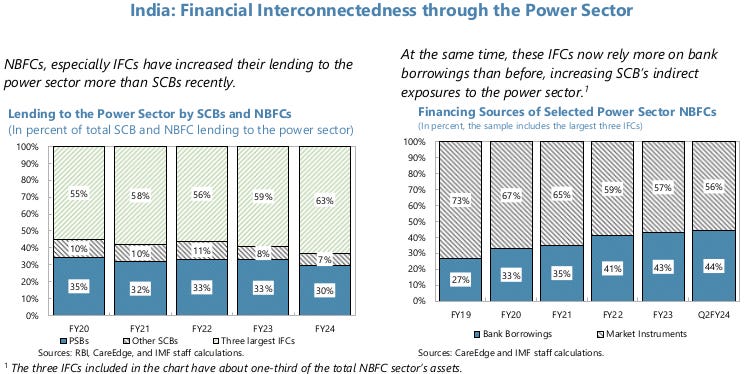

One: Our power sector could trigger a big crisis

Our power sector is run in a notoriously terrible manner, and this has caused heartburn for our financial sector before. In 2016, many infrastructure and power companies began defaulting on their loans — because of a combination of cost overruns, delayed tariffs, coal shortages, and weak demand. This blew a hole right through the books of major banks, sparking a crisis that we took years to resolve.

This problem hasn’t gone away, though. Although the government has tried reforming the sector, our structural challenges remain. And while banks have tried cutting down their exposure to the sector, the risk to our financial system remains — it has simply shifted.

Instead of banks, NBFCs — especially state-owned infrastructure financing companies (IFCs) — are now the biggest lenders to the power sector. In fact, some IFCs have lent as much as 65% of their tier 1 capital to individual power companies, and so, a single large default could push them underwater. And those NBFCs and IFCs, in turn, are financed by banks. Which means that ultimately, banks remain at risk from the power sector — just with extra steps.

So, what happens if an NBFC is hit by a bad power sector default? Unlike banks, which can at least get some emergency liquidity assistance from the RBI, NBFCs don’t have any protection. This is a wider problem that the report highlights — despite taking up half of India’s private sector lending, NBFCs remain outside the perimeter of RBI’s last-resort support.

Two: Climate change is a structural issue

The report presents a nuanced picture of the climate risk India faces. It doesn’t try to spook you. In fact, it suggests that, at least up to 2040, India’s climate transition will probably only have a moderate impact on the financial system.

But underneath that, there are fault lines that deserve attention.

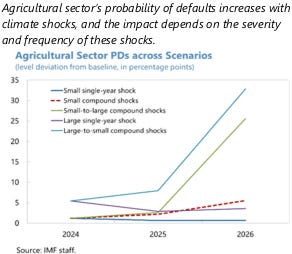

One sector that’s deeply vulnerable to ‘physical risks’ — that is, the direct damage we might face because of cyclones or shifts in monsoon patterns — is agriculture. And banks, especially regional rural banks (RRBs), are heavily exposed to that sector. Agricultural loans make up 13% of scheduled commercial bank portfolios, and over 60% for RRBs. We could survive one bad monsoon. But if a string of bad monsoons hits crop yields, the risk could spike sharply. In the IMF’s worst-case scenario, where you see a series of shocks compounding over three bad years, defaults on agricultural loans could increase by over 30%.

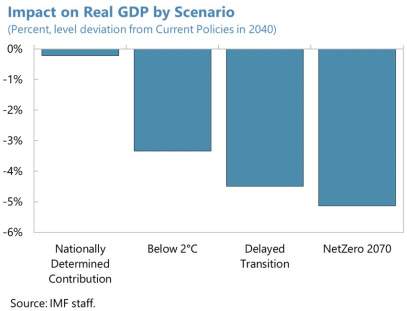

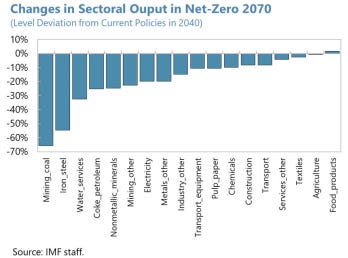

On top of that, we also face ‘transition risks’, that is, some firms might find that their business is suddenly less attractive as India transitions to more climate-friendly technology. These risks are concentrated in carbon-heavy sectors — carbon-based power, mining, metals.

Banks have sizable exposures to these sectors. NBFCs are even more exposed. If we transition aggressively — say, we actually set out to achieve our goals of being ‘Net Zero’ by 2070 — that could shave off 5% of our GDP by 2040. That sounds minor, but think about it — that drag won’t be evenly spread. While some industries will barely feel a thing, others will be decimated completely. And their lenders, in turn, might suddenly find themselves vulnerable.

The worst problem, though, is that we just don’t have enough data. We’re flying blind; our financial system doesn’t know where its climate risks are concentrated. Without that, IMF’s stress-testing can’t do much. There may be challenges which take us completely by surprise.

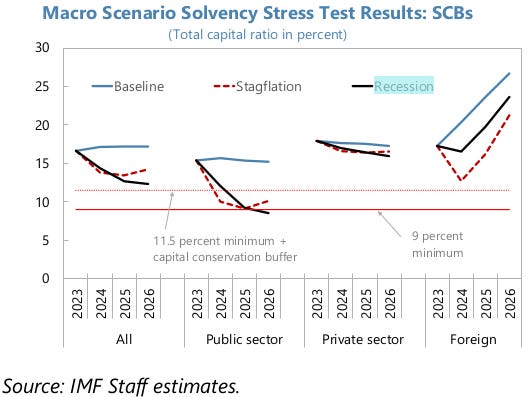

Three: Public Sector Banks remain fragile

Although India has really cleaned up its banking sector in the last decade, there are still cracks that begin to show under stress — most of which are in the public sector banks.

As per the IMF’s models, if India were ever to suffer stagflation, a number of PSBs would have to dip into their “capital conservation buffers” — their rainy day fund, of sorts — and would barely survive. If things got worse, and we saw a recession, they wouldn’t even meet their minimum capital requirements. Basically, if our economy sees serious challenges, PSBs would quickly begin to struggle. And because they still dominate India’s banking landscape, that means a few bad years for our economy could seriously damage Indian banking — making our economic problems much, much worse. It would force them to start deleveraging precisely when the economy needs credit.

Most of this risk sits in just ten banks, which hold 24-36% of the assets of all scheduled commercial banks. These banks need more capital to stave off the risk of serious problems in a crisis. One way of doing that, perhaps, would be to pay less dividend to the government, and start using that money to cushion themselves from shocks.

The bigger picture: we’re stronger, but we aren’t bulletproof

Ultimately, it’s the IMF’s job to look for risks. None of this should take away from the real progress we’ve made. The Indian financial system today is stronger, better regulated, and more sophisticated than it was the last time the IMF was doing this. We faced repeated crises — in 2016, in 2018 and in 2020, and we’ve come out of them stronger.

But that doesn’t mean we can survive anything. Financial systems are tightly interconnected. When things go wrong, problems have a bad habit of jumping from entity to entity. Any of the problems the IMF points to — a power sector default, a climate crisis, or a PSB collapse during a bad year — could send shockwaves through the entire system, infecting everything from banks to bond markets.

This isn’t a reason to panic, but to have some perspective. There’s a lot of good news here. But in a system as large and consequential as India’s, any risk, no matter how distant, warrants close attention.

Are loan recoveries going up?

We came across a headline from a CRISIL press release this week. It read, “For ARCs, redemption rate for retail SRs to improve ~600 bps. ”

Umm… what? Honestly, even if you rearranged those words randomly, they’d probably make about as much sense to us as they did this way — absolutely zilch!

So, we thought we’d dive in and figure out what exactly Crisil meant by this. And guess what? Along the way, we ended up discovering a pretty fascinating corner of the capital markets—one we haven’t explored much here on The Daily Brief.

Now, for today’s story, we’re not going to be overly ambitious. We won’t try uncovering any third-order effects hidden behind that headline, nor will we search for a quirky angle that no one’s thought of yet. Instead, we’ll keep this one simple and straightforward. We hope to give you just enough context to decode headlines like this one, if you ever come across them again.

For that, we’ll cover everything from what ARCs (Asset Reconstruction Companies, by the way) actually are, why they’re important, the quirky relationships they have with banks, why they issue these super complicated instruments called Security Receipts (or SRs for short), and — most importantly — what all this means for you.

Let’s dive in.

What are ARCs, and what exactly do they do?

Here’s a fairly foundational problem with a banking system:

Banks give out loans. Not everyone pays those loans back. If that happens, what options do banks have?

If someone misses payments for 90 days straight, their loan gets classified as an NPA — or a ‘non-performing asset’. That basically means it’s a bad loan, and if the bank doesn’t manage to recover it, it’s a loss for them. Now, banks could try chasing after these bad loans themselves, but honestly, they’d probably be better off spending their time doing what they’re good at: lending money.

That’s where ARCs step in.

ARCs “buy” bad loans from banks, allowing them to tidy up their balance sheets and focus on their core lending business. And then, ARCs leverage their expertise to restructure or liquidate those distressed assets, basically trying to claw back as much money as possible.

But what, exactly, do we mean when we say ARCs “buy” loans? After all, it’s hard to imagine people actually ‘buying’ or ‘selling’ loans. Well, those mysterious ‘SRs’, or Security Receipts from the headline? Here’s where they come into the picture. Let us explain.

How do ARCs do what they do?

Suppose a bank has given a ₹200 crore loan to a manufacturing firm named SteelCo. Unfortunately, SteelCo runs into financial trouble and stops making its repayments. This goes on for over 90 days, and the loan becomes an NPA. Now, the bank has a problem. Recovering NPAs is tricky, expensive, and uncertain — banks prefer lending rather than chasing after unpaid loans. So, the bank decides to transfer this problematic loan to an ARC.

The ARC, now, carefully looks into SteelCo’s finances and assesses the value of its assets. It studies how much land the company has, what its buildings are worth, whether they can sell its machinery, and so on. After all this, the ARC comes up with an estimate: let’s say, it thinks it can realistically recover around ₹120 crore over the next few years. Given the risks of trying to do so, the ARC strikes a deal with the bank: it’ll buy the ₹200 crore loan from the Bank for just ₹100 crore. That ₹20 crore discount reflects the complexity and uncertainty involved.

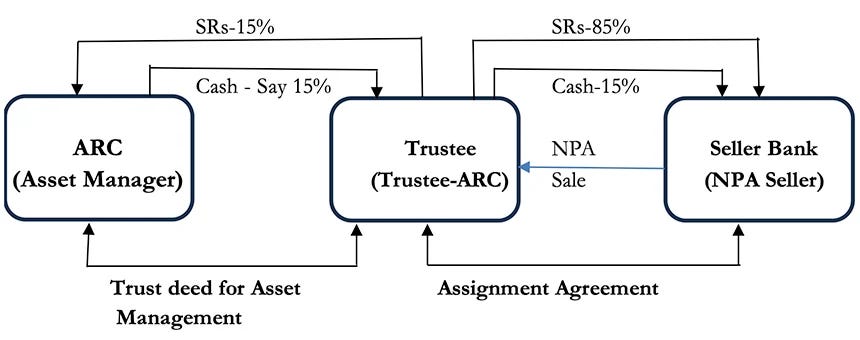

Now, the ARC sets up a special-purpose trust to hold this specific loan. Following RBI guidelines, the ARC funds this trust using a “15:85” model: they pay ₹15 crore in cash upfront to the bank, and for the remaining ₹85 crore, the trust issues ‘Security Receipts’ (SRs) to the Bank. These receipts, in essence, represent the bank’s ongoing stake in any future recoveries the trust makes. The ARC also gets ₹15 crore worth of SRs for its upfront payment, ensuring they’re invested alongside the bank.

Now, here’s where it gets interesting: the ₹85 crore worth of SRs issued to the bank don’t have to stay with the original bank . They can actually sell these SRs to other banks, Housing Finance Companies (HFCs), or Non-Banking Financial Companies (NBFCs). In short, they become an asset that you can buy and sell — a little like bonds. This forms the foundation of India’s distressed asset management industry, but that’s a topic for another day.

Once the transaction is complete, the ARC actively works to recover the money from SteelCo. It negotiates settlements, restructures the debt, auctions its assets, or does whatever else it needs to. After a whole lot of work, the ARC successfully recovers ₹130 crore within the next two or three years.

Where does that money go? First, the recovered money is used to cover the ARC’s management fee (typically around 1.5%-2% annually). After that, the remaining funds are shared proportionally among anyone who holds SRs — the ARC, the Bank, or whoever the bank sells those SRs to — based on their respective stakes.

Now, the total recover of ₹130 crore exceeds the ₹100 crore initial cost. After redeeming all the SRs, there’s still a surplus of ₹30 crore. This money is usually shared according to an incentive structure that rewards the ARC for successful recoveries.

Let’s say things don’t go this well, though — and the ARC only recovers ₹80 crore. What happens then? Both the ARC and the bank would bear proportional losses on their share of the SR holdings, highlighting the ARC’s own risk exposure.

Now, here’s the thing: before 2014, RBI required ARCs to pay only 5% upfront. They were, in a sense, not too accountable, especially compared to the bank’s huge 95% stake. But the RBI increased this requirement to 15% in 2014. Suddenly, ARCs now had significant “skin in the game”. Their interests were now aligned far more closely with banks and investors. In theory, that ensures more diligent and active recovery efforts.

What did the headline mean, then?

With all this context, let’s get back to the headline once more. When ARCs successfully recover bad loans, the Security Receipts they issued are redeemed (or paid back). So, if there’s an increase in redemption rates, the bad loans ARCs bought from banks are finally paying off — by 6% more than before.

A final bit of nuance worth highlighting, here, is the difference between corporate and ‘retail’ NPAs.

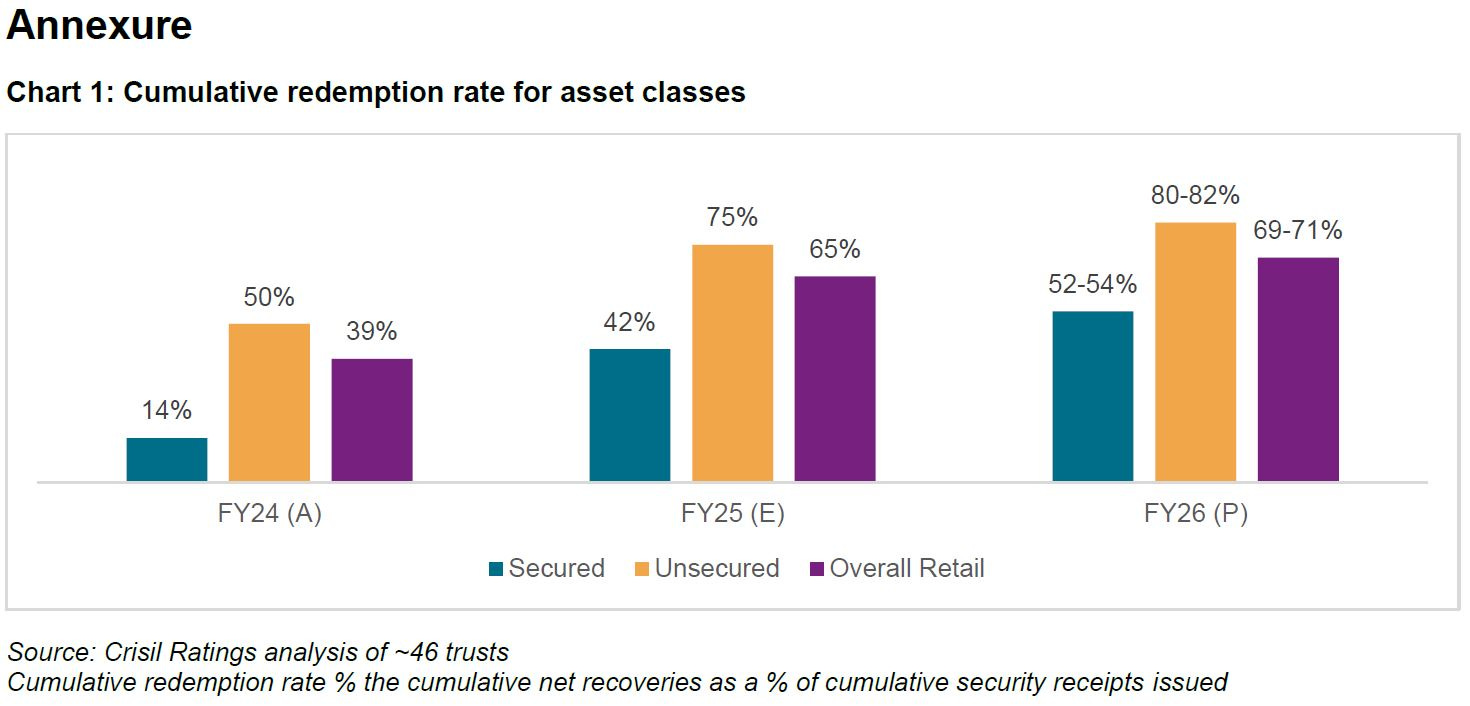

‘Corporate’ NPAs — NPAs by corporations, as the name suggests — typically involve larger, more complex loans. Naturally, they usually have slower redemption rates, given that they involve lengthy legal proceedings and complicated restructuring. For corporate loans acquired before or around the introduction of India’s bankruptcy law (IBC), the redemption rates hover around just 30–40%.

In contrast, retail NPAs — that is, NPAs for home loans, personal loans, vehicle loans, small business loans etc. — perform much better. When, during the asset quality review (AQR) of 2016, banks discovered a high rate of corporate defaults, they shifted their focus toward retail lending.

According to recent CRISIL data, redemption rates for these retail SRs are expected to rise by around 6% points. They’ll reach approximately 69–71% next fiscal year. Retail loans are easier and quicker to resolve, as borrowers generally prefer settling defaults quickly to save themselves from hassles and maintain their creditworthiness.

This divergence shows a structural shift in the ARC industry. With corporate NPAs becoming tougher to handle due to competition and complexity, ARCs are now focusing more on smaller, retail loans. These loans offer quicker turnarounds, predictable recoveries, and less complexity—exactly what ARCs prefer.

And that’s exactly what that cryptic Crisil headline was all about!

Tidbits:

- Bharti Airtel has announced the landing of India’s 20th undersea cable, part of the 2Africa Pearls system, in Mumbai. The cable, with a data transfer capacity of 100 terabits per second (Tbps), will connect India to Africa and Europe via West Asia. Spanning over 45,000 km, the 2Africa system is set to be the world’s longest subsea cable. This development follows Airtel’s landing of the 21,700-km-long SEA-ME-WE 6 cable in Chennai last month, which connects India to Singapore and Marseilles with a global capacity of 220 Tbps. Airtel has partnered with Meta and center3, a subsidiary of the Saudi Telecommunications Company, for the project. The company said it is diversifying its global cable network, which currently spans 400,000 route km across 50 countries and five continents. The cables are expected to integrate with Nxtra by Airtel, the firm’s data centre arm.

- The Reserve Bank of India is considering doubling the investment cap for individual foreign portfolio investors (FPIs) in listed Indian companies from 5% to 10%, according to internal government documents. The aggregate ceiling for all foreign individual investors may also rise from 10% to 24%. This move comes as India has seen over $28 billion in equity outflows since the Nifty 50’s September peak. The new proposal aims to extend them to all foreign individuals. The Securities and Exchange Board of India (SEBI) has raised concerns that 10% holdings by individual FPIs, especially when combined with associated entities, could cross the 25% takeover threshold, triggering mandatory open offers under existing rules. The RBI and the Finance Ministry are reviewing the proposal urgently in light of disrupted capital inflows.

- India’s media and entertainment sector generated ₹2.5 lakh cr in revenue in 2024, recording a 3.3% year-on-year growth, according to the FICCI-EY report. Indians spent a collective 1.1 lakh cr. hours on smartphones last year, averaging nearly 5 hours daily per user, with 70% of that time spent on social media, gaming, and video content. Digital channels surpassed television for the first time since 2019, becoming the largest segment of the industry. Advertising grew by 8.1%, while the events segment expanded 15%, crossing ₹10,000 crore in revenue. However, subscription revenues declined, and Pay TV lost 60–70 lakh homes. The animation and VFX sector contracted 9% following international production slowdowns. The industry contributed 0.73% to India’s GDP and is projected to grow at 7.2% in 2025, reaching ₹2.68 lakh cr.

- This edition of the newsletter was written by Kashish and Pranav

Join our book club

Join our book club

We’ve recently started a book club where we meet each week in Bangalore to read and talk about books we find fascinating.

If you’d like to join us, we’d love to have you along! Join in here.

Have you checked out One Thing We Learned?

Have you checked out One Thing We Learned?

It’s a new side-project by our writing team, and even if we say so ourselves, it’s fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That’s all. It’s chaotic, it’s unpolished - but it’s honest.

So far, we’ve written about everything from India’s state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you’re looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()