I am aware of the impact of most of the corporate actions on ETF. But I am missing something to understand the impact of buy back on index ETFs

Now lets say I hold Icici IT ETF and infy announces buyback. Post buyback free float of the company reduces and that reduces the weight of the stock in the index. My question is how is this adjusted in ETF since the acceptance ratio is known only after all bids are received.

Am sure this is well taken care of and it will still track the index. If somebody could explain with some numerical I would really appreciate.

Thanks in advance.

PS: I am a active reader in this forum. But I never posted a query before. But this one is really troubling me. And yeah, I had to create an account here.

Simply put the weight of that particular stock is adjusted by the index provider and the ETFs will track it. And if these stock become ineligible due to any proposed corporate action, it will be removed from the index like Motherson Sumi will be removed

To add to the above answer, from the information that I could find (Page 139 of Methodlogy document), Nifty Indicies would only reflect the impact of corporate actions like share repurchase (aka buybacks) on a quarterly basis (if less than 5% of free float is effected by such a corporate action) -

All singular instances of changes in equity shares arising out of additional issue of capital, such as ESOPs, QIPs, ADR/GDR issues, private placements, warrant conversions, FCCB conversions, buy-back, forfeiture of shares etc. which have an impact of 5% or more on the issued share capital of the security are implemented after providing a three trading days’ prior notice.

Changes entailing less than 5% impact on the issued share capital or a free-float are accumulated and implemented from the last trading day of March, June, September and December.

As the ETF that you mentioned as an example (aka ICICI Prudential IT ETF) is benchmarked against the Nifty IT TRI, so when the Index Service Provider (aka Nifty Indices Limited) informs the ETF’s AMC about the change in the weight of the stock in the index due to the share buyback, the ETF scheme would reflect the same in their portfolio by rebalancing it. This is also mentioned in its Scheme Information Document (Page 47) -

Investment Process

The Scheme will track the Underlying Index and is a passively managed scheme. The investment Decisions will be determined as per the Underlying Index. In case of any change in the index due to corporate actions or change in the constituents of the Underlying Index (as communicated by the Index Service Provider), relevant investment decisions will be determined considering the composition of the Underlying Index.

To take the example of Infosys, which has a buyback program that is currently ongoing. As per its announcement, it is looking to buyback 5,25,71,428 shares. This is less than 5% of the of their total outstanding shares (4,25,88,88,852 shares), hence the effect of this buyback should start reflecting in the index on the last trading day of June. As of 28th June 2021, they have already purchased 21,86,000 shares. Maybe to estimate the likely effect of the buyback, we can track the change in weightage of the index in the upcoming days. The SBI MF’s website for its IT ETF (on the Unit Creation tab) that is also benchmarked against Nifty IT TRI shares the exact number of underlying stocks required for making its Creation unit (4000 units of the ETF). That would likely show some changes. Currently, it is as follows -

I really appreciate the answers given by both @Bhuvan and @Prayag. I have understood the procedure followed by ETFs

However there is still one thing on which I would like a clarification in my interpretation.

In the ongoing buyback by infy, the buy back is in the nature of open offer. Now lets say it was a tender offer to buyback at 1800. From the links provided by you I understand that etf will not participate in the buyback. They will simply rebalance when there is official notification from nse. Isnt that an opportunity foregone by the fund? If I was a shareholder I would have probably tendered my shares at 1800 and buy at cmp. Yes I know I will have to adjust to acceptance ratio.

Or lets talk about reliance right issue. ETFs tracking nifty 50, did they apply for right shares? Did they sell the right? Or they let it expiry? Post right issue, theoretically a share holder stands to lose if he doesn’t buy the right shares or renounce the right.

I came across an article, which mentioned that index funds had sold their right entitlements -

Index funds, who can’t hold partly paid-up shares, had sold their rights entitlement using the stock exchange platform available to sell these entitlements

ETFs too would have sold their REs as they are also categorized in the same Mutual Fund category as Index Funds. Also, checking the latest monthly Portfolio disclosure for Nippon’s NiftyBees ETF and SBI Nifty 50 ETF confirms that they don’t hold any Reliance REs

I am not completely sure about this. But from what I understand, this might vary depending on the ETF scheme. In the Scheme Information Document for NiftyBees ETF (Page 5-6), it is mentioned that they would participate in corporate actions if advance notice is given for the same -

iii) Corporate Action and Proxy Voting

From time to time, the issuer of a Security held in the Scheme may initiate a corporate action relating to that Security. Corporate actions relating to equity Securities may include, among others, an offer to purchase new shares, or to tender existing shares, of that Security at a certain price. Corporate actions relating to debt Securities may include, among others, an offer for early redemption of the debt Security, or an offer to convert the debt Security into stock. Certain corporate actions are voluntary, meaning that the Scheme may only participate in the corporate action it elects to do so in a timely fashion. Participation in certain corporate actions may enhance the value of the Scheme.

In cases where the Fund or the Fund Manager receives sufficient advance notice of a voluntary corporate action, the Fund Managers will exercise their discretion, in good faith, to determine whether the Scheme will participate in that corporate action. If the Fund Managers do not receive sufficient advance notice of a voluntary corporate action, the Fund Managers acting on behalf of the Scheme may not be able to timely elect to participate in that corporate action. Participation or lack of participation in a voluntary corporate action may result in a negative impact on the value of the Scheme.

This answers my question. I looked all over the Internet to get answers for this. Now I know all that I had to do was read scheme documents.

To conclude, the fund manager will act in good faith to enhance the value of the scheme. So my contention that theoretically there is loss of value is not valid.

However the above conclusion gives rise to one more doubt.

Since the fund manager will take this action in good faith, the tracking error of the scheme to the underlying index may increase. May be the this error will be positive for the scheme. But, shall this be one of the limitations of considering tracking error while evaluating the scheme?

From what I understand, having a low tracking error over a long time period is considered a good thing as it means that ETF tried to track its underlying index as perfectly as possible. For example, even if a fund manager decided to take part in a corporate action, believing that their action would eventually lead to better tracking of the index, then the increase in their ETF’s tracking error would be temporary and their ETF’s tracking error would become lower than other ETFs in the longer term (given that their decision was correct).

On the other hand, if a fund manager had decided not to take part in a corporate action and still kept their tracking error low, then it would have meant that they achieved their ETF scheme’s objective (aka tracking the underlying index) to a higher degree in comparison to other fund managers.

Also, tracking error isn’t solely dependent on participation or non-participation in corporate actions. This article briefly touches upon this topic -

The aim of the ETFs is to track the index constituents and attempt to deliver identical returns. Tracking error points to the discrepancy between the ETF performance and index performance.

This can be caused by a variety of reasons such as cash held by the ETF, time lag in investing dividends, rebalancing due to exit and entry of stocks from the index, corporate actions, and so on. Fund houses strive to keep the cash position low in order to match the index returns.

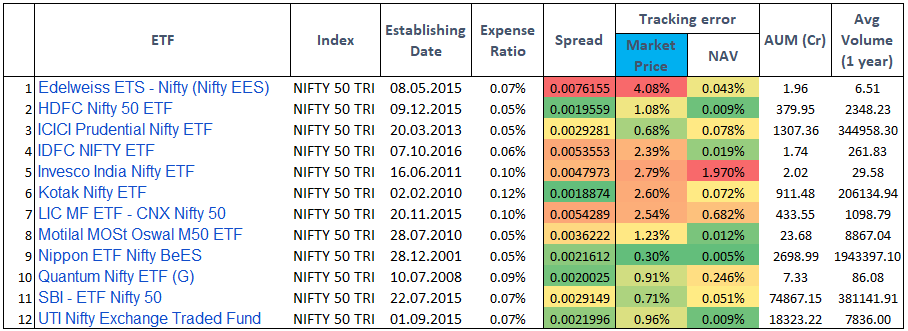

Also, another thing to keep in mind is that tracking errors being reported by ETFs are in regards to their NAVs. But as ETFs trade on the exchanges, the investors might experience higher/lower tracking errors while purchasing/selling the ETFs in case the market price is not in sync with NAV. There was a recent article, which had compared the NAV vs. market price tracking error of Nifty 50 ETFs in the last 5 years -

Also, on days where the market becomes extremely volatile, the tracking error can become even more pronounced. An example of this was the last year’s crash -

Also, sometimes the fund manager might take decisions that are completely out of sync with the ETF’s objective. A recent example of this was SBI’s Nifty 50 & Sensex ETF issuing dividends -

This went against the ETF’s core objective as they are all benchmarked against the Total Return Index variant of their respective benchmark index (which only allows reinvestment of dividends back into the ETF). There was an article by @deepakshenoy which explained why this happened -

The change: EPFO’s Accounting forces our hand

Out of the blue, the SBI Nifty ETF gave three dividends last year, adding up to about 4% or so. This sucks because dividends are taxed now.

Why did they do it? A complex accounting reason:

EPFO invests in the SBI Nifty ETF

EPFO must invest 15% of flows into the equity funds

EPFO also decided to give a huge 8%+ return for the last year.

How can it, when even government bonds, which are the largest chunk of EPFO holdings, are only giving about 7%?

The answer: sell some of the equity funds bought earlier – the SBI ETF was one

But if you buy 15% and sell 5%, the net purchase is only 10% (of whatever money EPFO gets every year).

Which violates EPFO’s requirement of minimum 15% of net inflows.

So EPFO went to SBI and said, please give us dividends instead.

And SBI complied, thulping the rest of us with a taxable dividend. (EPFO pays no taxes)

This is likely to continue next year as well.

Lastly, do check out the Varsity chapter authored by @Bhuvan relating to exchange-traded funds as it goes into details about many practical aspects when choosing an ETF to invest in -

In my last post all that I was saying is this may have impact on tracking error. And its not right to take decision solely based on this factor as we do not why exactly tracking error exits.

My last question was answer in itself.

Having said that, I must admit your replies are very informative.

Thank you for all the information and references. I really appreciate it.