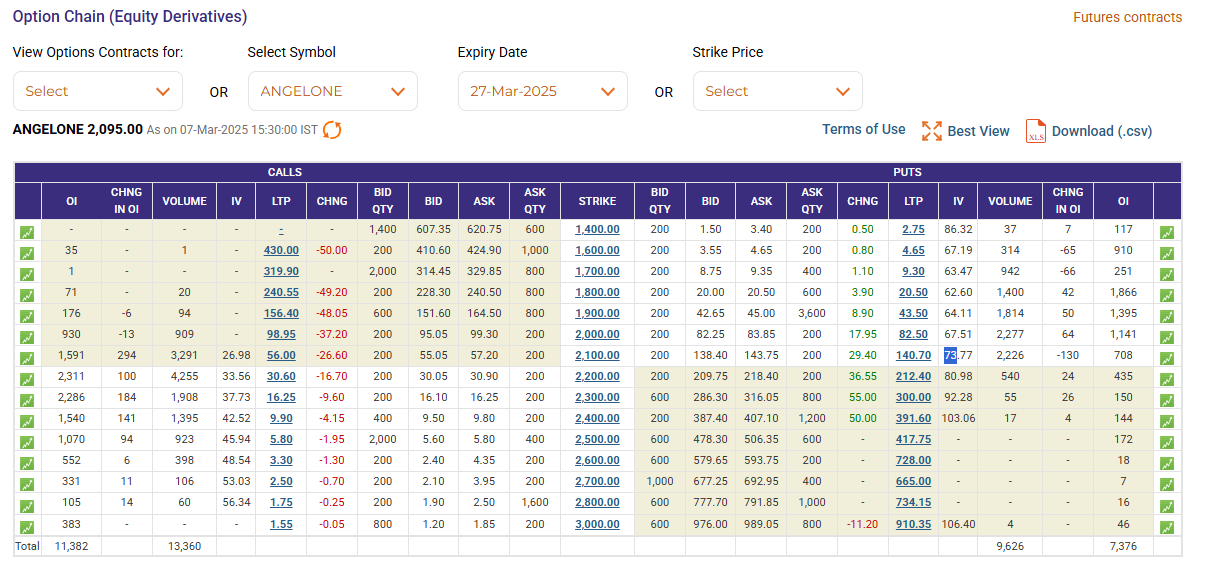

Hi Everyone,

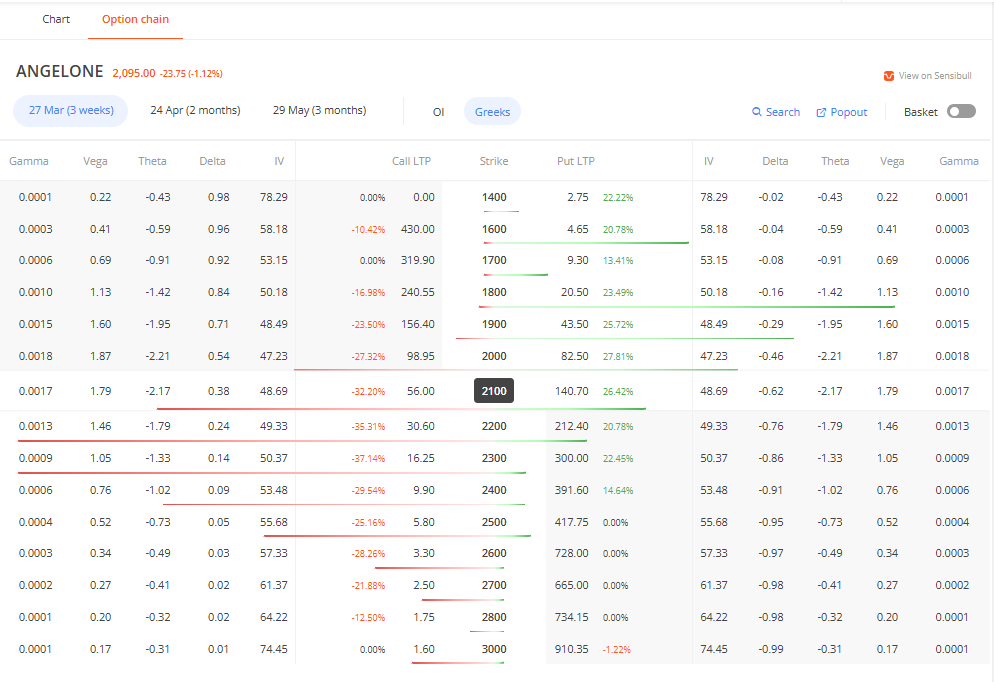

Can someone explain why zerodha ANGELONE option chain shows same IV (implied volatility) for ATM 2100CE (Rs 56) and 2100 PE (Rs 140.7). ( Data is for day end Friday : 7 Mar 2025)

I used a online calculator (with DTE = 20, R = 7%) which shows very different IV ( 27.06 for Call ) and (73.54 for put).

Even NSE website shows a very different IV.

I have noticed most of the Zerodha Stock Option chains have the same IV for call and puts of the same strike but different for Index options.