When I compare the performance of actively managed large-cap funds and passively managed index funds (like Nifty 50, or S&P BSE Sensex ones), I notice that by and large the actively managed large-cap’s performance has largely been better performing, even while taking the higher expense ratio into account. Now I understand that past performance should not be taken as any indication of future performance, but if I look at the current top-3 ranked actively managed funds, their performance over 10yrs have almost entirely been better than index. Why do then people recommend Index funds ? Or am I looking at wrong parameters ?

Investment is a very personal journey. Each one has a different perspective and based on each individual need and nature, they invest in products which might meet their needs. Index investing is one such option. If your requirement is high returns which obviously come with high risk, no one will advise you to invest in Index MF on the contrary if a person is quite ok with reasonable returns better than FD without much risk, they might go for Index funds as the commission is relatively lower and if they wish to hold it for long period.

According to me investing in NPS is the best asset allocation in one fund, but many do not like it because they feel a portion is invested in debt and gilts when in fact they wish to invest majority in equity. Also unable to withdraw until age 60 and a portion going to annuity would be a dampner to them. But this is exactly what I want.

There is another post in this forum which says that 90% of traders lose money. When the fact is that 90% lose, why do people still trade?

The products are there and people recommend various products, but the choice is yours to make based on your needs.

Disc: Invested in Index ETFs. Fully convinced about the product which fits my requirement perfectly. Also it is not exactly fair to compare a Nifty 50 with a large cap actively managed fund where the fund manager has the discretion to exit/enter at any time a large cap stock whilst with a Nifty 50 this luxury is not there.

Thanks for replying here. Completely get it that it is an individual choice, individual approach. Also understand the reasons why Large-Cap actively managed funds can perform better than passively managed. However, the volatility of Index funds, the downdrops seem to be worse/higher than the top-rung active large-caps, and XIRR over extended periods are more favourable, so I still don’t get what advantage exactly do Index funds offer ? I understand the advantage that ETFs offer being traded like common stocks, but I was hoping that there’d be more in form benefits.

If you are referring to Niftynext 50, yes the volatility is greater as these stocks behave like a midcap, though they belong to the top 100. However for Nifty50 I am invested and did not find any great volatility… The dips are quite normal.

Every business has same success probability. CA has only one percent pass probability and we still have so many of them trying. Every sport also has same probability of making it to higher levels.

People want to try what others couldn’t. Unless you take risk, you won’t get return.

Most people don’t even do the work and verify before committing large money.

They might waste years and stay busy with new things - but doing what you need to do is always a jump too far. If they did that most would know that they don’t have edge or if they do, perhaps they are risking too much mistaken by small sample data.

Its hard to stay through tough periods without doing the work.

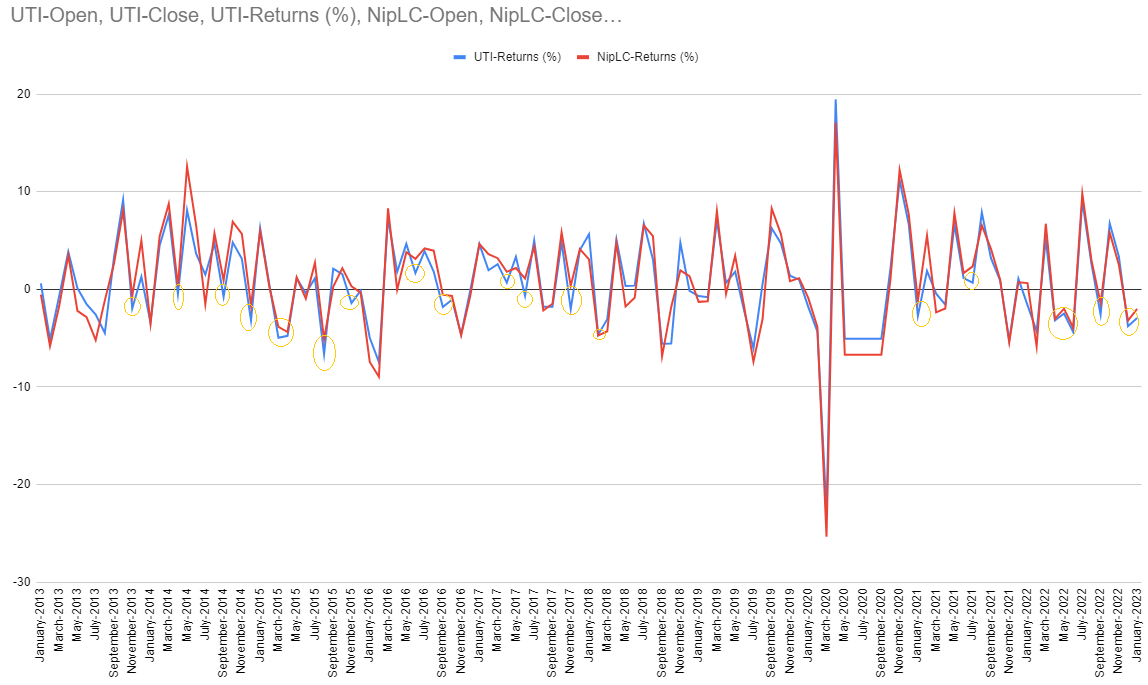

So it is completely possible that I was interpreting some of the charts I saw incorrectly. I tried to put together a comparison of 2 funds, i.e. “UTI MF Nifty 50” (as a passive index fund) and “Nippon India LargeCap Growth (Direct)” (as an actively managed fund), with what public data I could find (I’ve mentioned the source, using Google Doc’s built in scraping function) in this spreadsheet here.

The only kind of data I could find (or that seemed relevant at macro level) was the opening & closing NAV of the 2 funds, apart from the returns %age. I am not quite sure how the returns are calculated.

Following graphic is a plot of the month by month returns from the 2 funds, and we can see that the blue-line (index fund) has several deep drops compared to the red-line (managed active fund). Those deeper drops (many giving -ve returns) are marked in yellow-orange circles. I am not claiming this to be conclusive by any measure, but it is one of the reasons for the questions in my mind.

All very hard earned, white and limited money – which is why I am trying to educate myself as much as possible. At the end of the day I do want to see my money grow and hold it’s value. I am just to trying to understand things based on facts, and avoid falling in fallacy traps.

sorry, my reply was to the out of topic conversation that branched out regarding futility of trading.

Regarding topic itself, i don’t think we can micro analyze too much, and this move by move comparison is meaningless to me. More than 10-15 years ago, active funds could beat indices very easily, we used to expect 20% pa performance. All of that has come down drastically and any out performance is generally minor.

csv’s reply is spot on. I don’t have equity investments anymore so have not really looked at it for some time, but one or two years ago i think a large portion of funds in large caps were struggling against index funds.

A lot of this depends on what you are looking at and when. So previously growth funds were doing well and value was not and in last 2 years value has come back strongly. HDFC top 100 i think was similar to HDFC Equity which i had owned for many years. HDFC Equity was struggling quite a bit against index for many years and all numbers would have looked bad. Then 1 strong year flipped it around as value stuff came back strongly and now the numbers look respectable. So these kind of holdings are long term in nature and short term out performance or under performance can affect your 5-10y window returns. So what looked bad some years ago is now looking decent - all because of a year or so of better returns. Mirae Large cap used to be have much stronger numbers vs HDFC Equity/FlexiCap and now they look similar.

Point is - a lot of this is futile, its hard to predict these things, and expenses make it harder. If the out performance was as large as it used to be, then active funds would have been a no brainer. But that’s not the case anymore, at least for large cap funds.

Now, perhaps you can trust your favorite established funds manager and hope he can show results over long window, and hold through periods where funds look bad ( i did with HDFC Flexi cap and got lucky as it came back in time before my exit) . Or just invest in Indices with low expense ( 0.05 in ETF ) and you probably will beat ( or atleast be very close to) most of the funds most of the time.

I don’t have numbers with me, but i think this is what is happening in large cap space. freefincal is a good blog, perhaps you might find some useful numbers there.

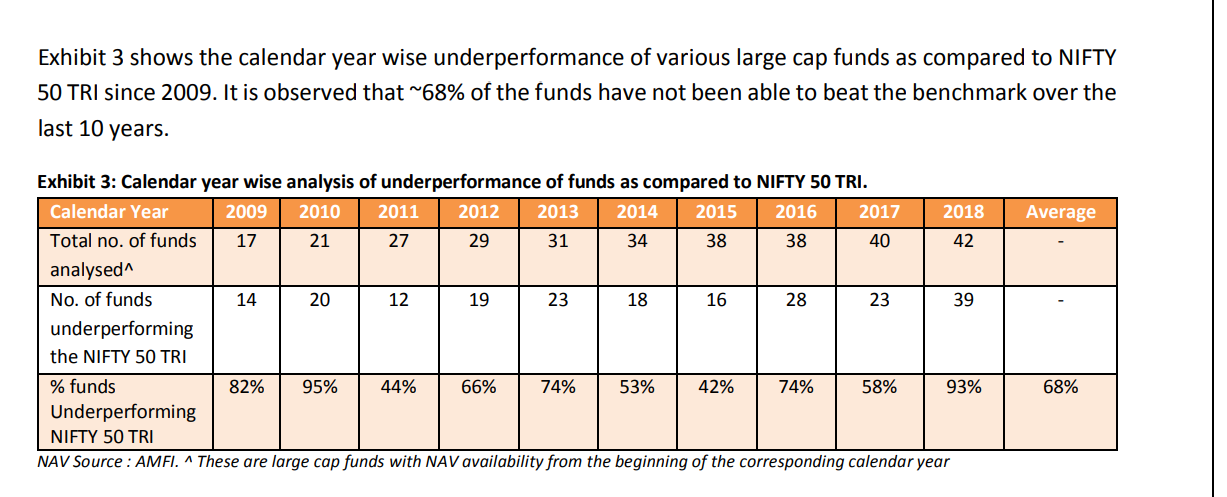

I was trying to understand if NIFTY50 was outperforming mutual funds and came across interesting data that says NIFTY has outperformed actively managed large caps (atleast that’s what I understood) . Please let me know what you think about this.

One un-said thing I’ll add is that in my opinion all Govt’s past and present try to protect the main Indexes (using LIC, State owned MF houses, EPFO etc) from falling too much as these are considered a proxy for how well the economy is doing… But in markets everything is very very subjective so I might be totally wrong in my assumption