Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube.

In today’s edition of The Daily Brief:

- New Restrictions on Bangladesh Imports

- The RBI intends to tread lightly

New Restrictions on Bangladesh Imports

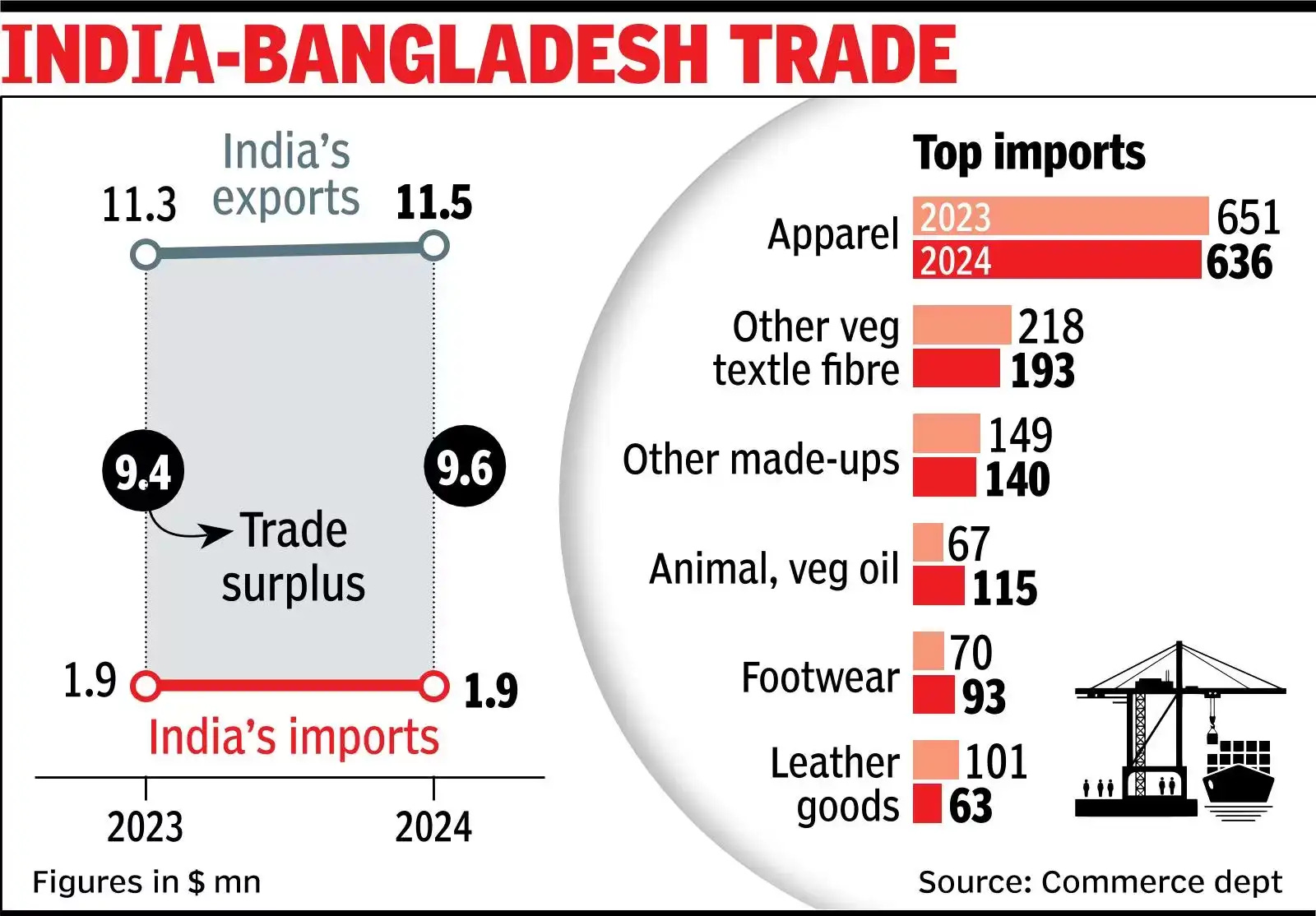

In a bold move, India has imposed sweeping new trade restrictions on imports from Bangladesh, suddenly tightening the screws on nearly 42% of its inbound goods from Bangladesh . This aggressive policy step targets a huge chunk of Bangladesh’s exports to India – valued around $770 million – and it’s being seen as much more than a trade tweak.

It’s a big move with a big message, coming after a period of rising friction between the two neighbors. India’s decision didn’t emerge in a vacuum; it’s a direct response to recent actions by Bangladesh and shifting geopolitical winds in the region.

India-Bangladesh Trade Relationship

To understand the impact, it helps to know how trade between India and Bangladesh usually works. India imports about ~$1.7-1.9 billion worth of goods from Bangladesh each year, and a huge portion of that is clothing. Bangladesh is a global giant in apparel – it’s the world’s second-largest garment exporter after China, with the sector accounting for over 80% of Bangladesh’s export earnings . Last year alone, Bangladesh exported roughly $40–47 billion in ready-made garments worldwid.

By comparison, the Indian market is a drop in the bucket for Dhaka – India buys only around 2% of Bangladesh’s total garment exports , roughly about $700 million in clothes out of that $40+ billion haul.

In short, Bangladesh’s garment industry is massive and vital to its economy, but India has been a relatively small customer .

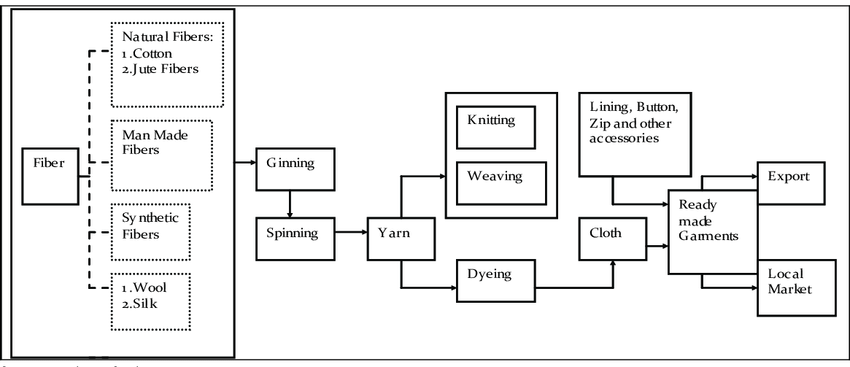

That said, the trade ties between the two countries’ textile sectors are somewhat complementary . Bangladesh’s apparel boom has been built on assembling finished clothes from imported raw materials. And guess who one of the key suppliers of cotton, yarn, and fabric is? India.

Indian yarn and fabric often flow into Bangladesh , where factories turn these inputs into T-shirts, trousers, and other garments, which then get shipped out across the world – sometimes even back to India. This value chain means India and Bangladesh aren’t just direct competitors; to an extent, they feed into each other’s industries.

Until now, India had allowed Bangladeshi imports with virtually no special restrictions or barriers. Cheaper Bangladeshi goods – especially garments – enjoyed duty-free access under regional trade agreements, and Bangladesh’s status as a less-developed country gave it certain trade perks. Indian consumers got inexpensive clothing, and Bangladeshi businesses found a growing market next door. However, Indian garment manufacturers have long grumbled about this arrangement. From their perspective, Bangladesh’s exporters have an unfair edge – they can import Chinese fabrics duty-free and get government export subsidies, making their final products 10–15% cheaper than Indian-made clothes.

All these trade dynamics set the stage for the current standoff. Despite close ties, under the surface there were tensions about market access and fairness. And recently, as we’ll see, the political winds shifted in Bangladesh, leading Dhaka to take steps that irked New Delhi – eventually provoking this striking counter-move by India.

Bangladesh’s Recent Moves

So, what changed? In short, Bangladesh itself started playing hardball on trade in the past few months, and it did so in ways that clearly ruffled India’s feathers. The timing was no coincidence.

Last year, Bangladesh went through a tumultuous political transition. Longtime Prime Minister Sheikh Hasina – who had been considered friendly toward India – was forced to resign after mass unrest (often described as a student-led uprising) in August 2024. Hasina even left the country for India amid the chaos, and the new authorities in Dhaka later sought her extradition back, to no avail.

In her place, a caretaker government took charge, led by Chief Adviser Muhammad Yunus (yes, the same Nobel laureate known for microfinance) who has been a long-standing rival of Hasina’s. This interim regime quickly began to reset Bangladesh’s foreign policy , tilting away from India’s orbit.

Under Yunus’s interim government, Bangladesh started taking steps that squeezed Indian interests on the trade front. In April 2025, Dhaka suddenly banned the import of Indian yarn via at least five key land border ports. This was a big deal because Bangladeshi textile mills import large quantities of Indian yarn to feed their garment factories. The ban meant Indian cotton yarn be replaced by yarn from elsewhere. Bangladesh didn’t stop at yarn. Around the same time, it tightened restrictions on rice trade and banned dozens of other Indian products from its market. Basically, Dhaka threw up a host of import curbs targeting Indian goods.

Why would Dhaka do this? Part of the answer lies in geopolitics. The new interim leader, Yunus, has been charting a course closer to China , which is India’s strategic rival in the region. In late March 2025, Yunus visited Beijing and came back with a basket of deals: China pledged some $2.1 billion in loans, investments, and grants to Bangladesh .

At the same time, Bangladesh has been dialing down its dependence on India . The yarn ban is one example – Bangladeshi mills have reportedly turned to Chinese yarn and fabric to replace Indian supplies almost overnight.

In fact, China has swiftly grabbed India’s market share in Bangladesh’s textile input market. By early 2025, China was supplying over 95% of Bangladesh’s imported yarn, while India’s share plummeted to near zero , which was more than 50% in 2024. It’s a dramatic shift from just a year earlier, when India was a top supplier.

In short, Bangladesh’s interim government spent the last several months raising trade barriers against India and cozying up to China . The cumulative effect was a sharp deterioration in India-Bangladesh relations. What had been a warm partnership started turning into a tit-for-tat dynamic.

By mid-May 2025, India decided it had had enough – and it chose to retaliate in kind, using the trade lever.

Overnight, India’s Ministry of Commerce effectively choked off land-route access for key Bangladeshi products. Ready-made garments (RMG) – Bangladesh’s flagship export – along with categories like processed foods and plastics, can no longer freely enter India through the usual land border crossing. Instead, they now must be shipped via just two seaports – Kolkata or Nhava Sheva (Mumbai) – barring them from the land trade corridors that Bangladeshi exporters heavily rely on.

Economic Impact and Reactions

For Bangladesh, the immediate economic impact of India’s curbs is significant but not catastrophic – more a strategic pinprick than a knockout blow. Ready-made garments are by far the biggest item India buys from Bangladesh, but as noted, that’s only around 2% of Bangladesh’s total garment exports.

The lion’s share of Bangladesh’s $40+ billion clothing exports go to markets in the US, Europe, and elsewhere , not to India. So, losing smooth access to the Indian market for RMG isn’t an existential threat to Bangladesh’s overall garment industry.

However, for certain exporters in Bangladesh, the pain will be real. Particularly hit will be small and medium-sized Bangladeshi manufacturers who had found a niche selling to India – often to nearby Indian states via land routes. These businesses benefited from quick, cheap truck shipments across the land border.

On the Indian side, reactions from industry have been largely positive – especially among domestic textile and garment producers. Indian manufacturers have long argued that Bangladesh’s duty-free access and incentives gave it a big advantage in the Indian market. Now, with Bangladesh’s goods facing hurdles, Indian companies hope to reclaim market share.

The new restrictions effectively act as a protective barrier, giving Indian garment makers (including many micro, small, and medium enterprises in the textile hubs) a better shot against Bangladeshi competition.

It’s important to note that the overall volume of trade at stake, $770 million, is small for India’s economy. In fact, that figure is just about 0.5% of India’s massive apparel market. Indian consumers likely won’t notice much difference on store shelves or in prices. The Indian market can absorb this change, and alternative suppliers (including domestic ones) can fill the gap.

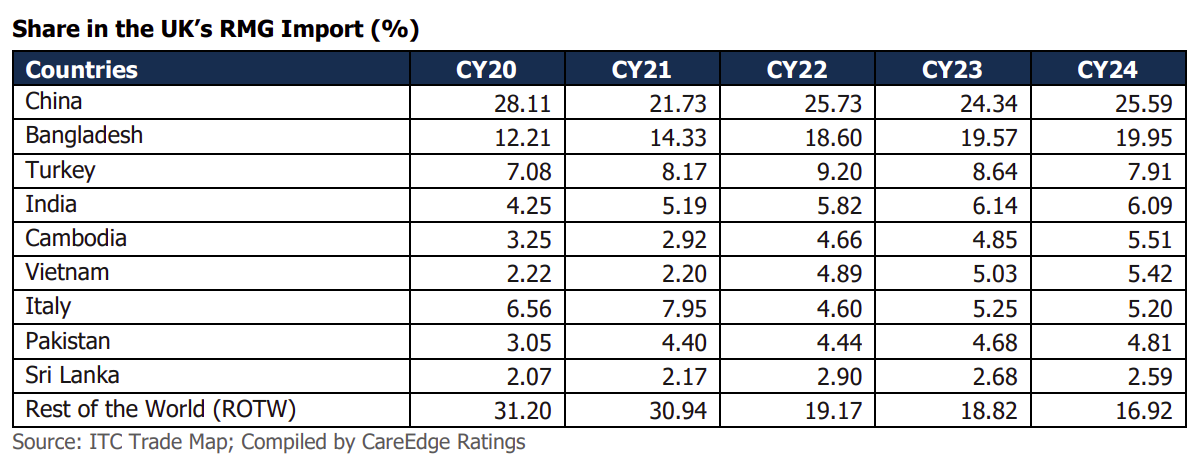

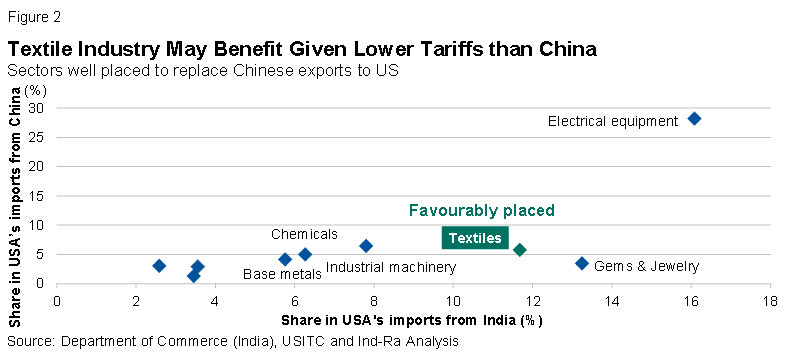

Interestingly, Indian garment exporters also have recent positive developments globally. The India-UK Free Trade Agreement (FTA) offers India a 12% tariff advantage over China in the UK’s $20 billion ready made garment market, creating a level playing field against key competing nations.

This FTA is expected to nearly double India’s market share in UK garment imports from 6% to 12%, translating to an additional $1.1–$1.2 billion annually according to CareEdge analysis. This is being said keeping in mind that after the Vietnam-UK FTA effective from 2021, Vietnam’s share in UK’s RMG imports increased from 2.22% in 2020 to 5.42% in 2024.

Moreover, recent US tariff adjustments favor India significantly. The US has imposed tariffs making Indian garments and home textiles comparatively cheaper than those from China and other competing nations. With India already holding about 28% of its textile exports market share in the US, this tariff shift might further benefit Indian garment makers, boosting exports significantly.

Conclusion

At the end of the day, India’s new import restrictions on Bangladesh are about more than just trade – they’re a geopolitical signal . New Delhi is effectively telling Dhaka: if you restrict our goods, we can play that game too. It’s a reciprocal move , almost tit-for-tat, meant to “restore equality” in the trading relationship.

The economic damage from this single step is not huge in the grand scheme (Bangladesh isn’t losing its top export markets, and India isn’t losing critical supplies), but the message is loud and clear . By targeting 42% of Bangladeshi imports to India, Delhi is pushing back against what it sees as Bangladesh’s tilting toward China and hostile trade posture.

It’s a region where trade and geopolitics are tightly woven. This “big move” by India is both a retaliation and a warning , delivered through the language of trade policy. We’ll be watching this space closely to see if cooler heads prevail and if the two partners can find a balance – or if this marks the start of a more fraught economic relationship in the days ahead.

Is this the end of the dollar?

Today, we’re diving into a topic that’s been causing quite a stir in financial circles: de-dollarization. It’s a term that might sound abstract, but it has profound implications for the global economy, financial markets, and potentially even your everyday financial decisions.

This matters to us directly here in India, where the Reserve Bank of India holds over $690 billion in foreign exchange reserves, with a significant portion – estimated at over $200 billion – in U.S. Treasury securities. Any shift in the dollar’s global status could have major implications for these holdings and for India’s position in the international financial system.

The Dollar’s dominance

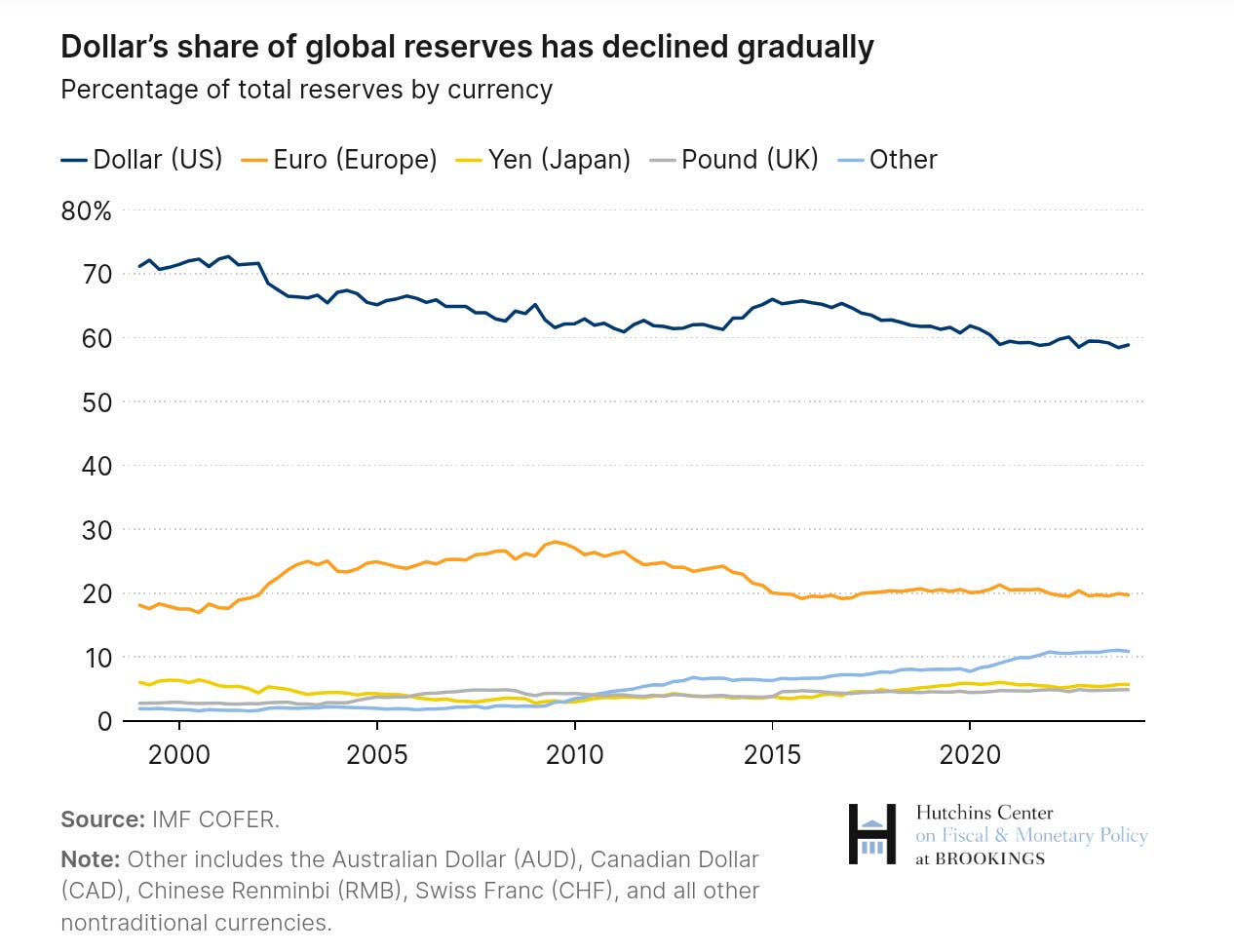

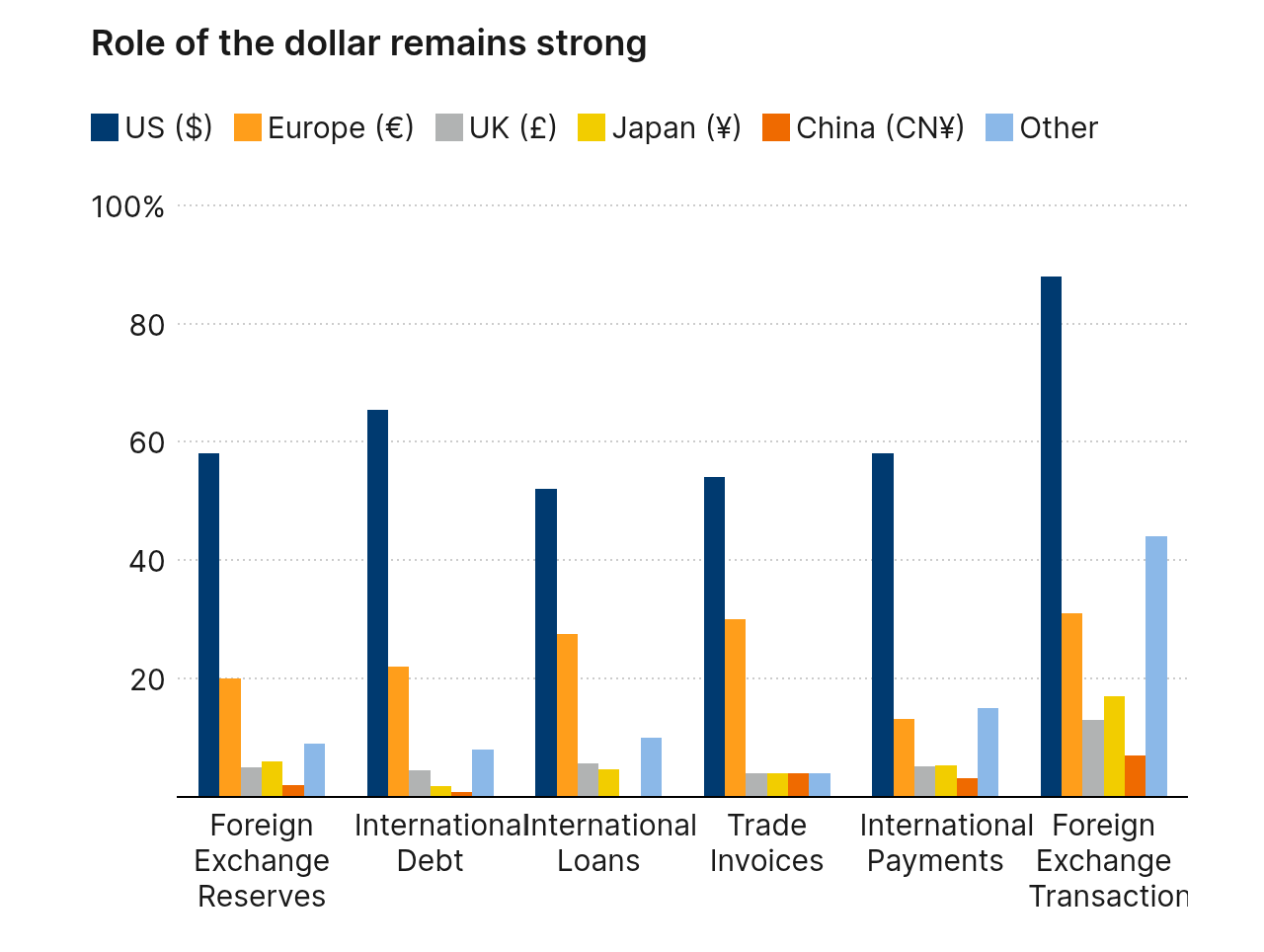

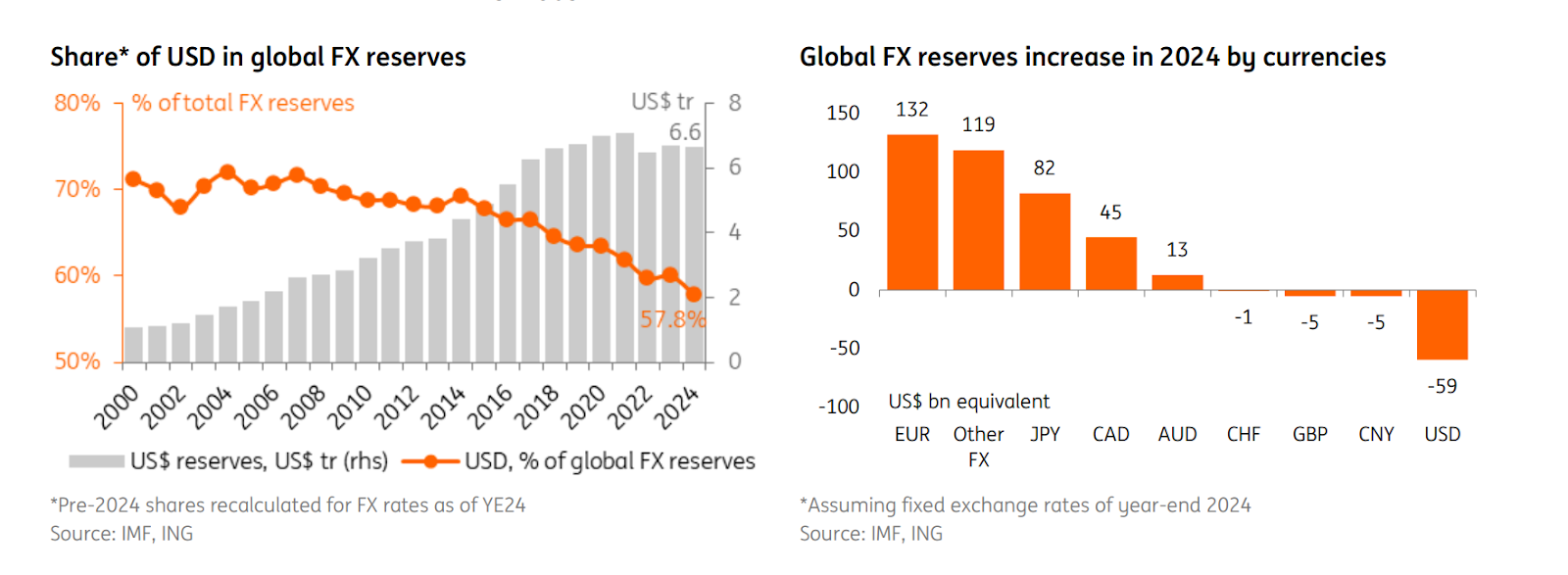

Let’s start with the basics. The U.S. dollar is, without question, the world’s dominant currency. According to data from the IMF, the dollar accounts for about 59% of global foreign currency reserves. The euro, its closest competitor, makes up just about 20%.

But the dollar’s dominance extends far beyond reserve holdings. According to a recent Brookings Institution report, 54% of global trade invoices are denominated in dollars. Think about that – even when neither the buyer nor seller is American, they’re often using dollars to settle the transaction. In foreign exchange markets, the dollar appears on one side of 88% of all currency trades.

In international debt markets, the picture is equally striking. According to the Bank for International Settlements, 64% of the world’s debt is denominated in dollars. And about 58% of international payments, excluding those within the eurozone, are conducted in dollars.

This dominance isn’t an accident. It’s rooted in the post-World War II financial architecture established at Bretton Woods in 1944, where the dollar was positioned as the anchor of the global monetary system. Although the direct link to gold ended with the “Nixon Shock” in 1971, the dollar maintained its central position due to several key advantages:

First, the sheer size and strength of the U.S. economy – still about 26% of global GDP.

Second, America’s deep and liquid financial markets, particularly U.S. Treasuries, which function as the world’s premier safe asset during times of stress.

Third, strong property rights, political stability, and the rule of law, which give global investors confidence.

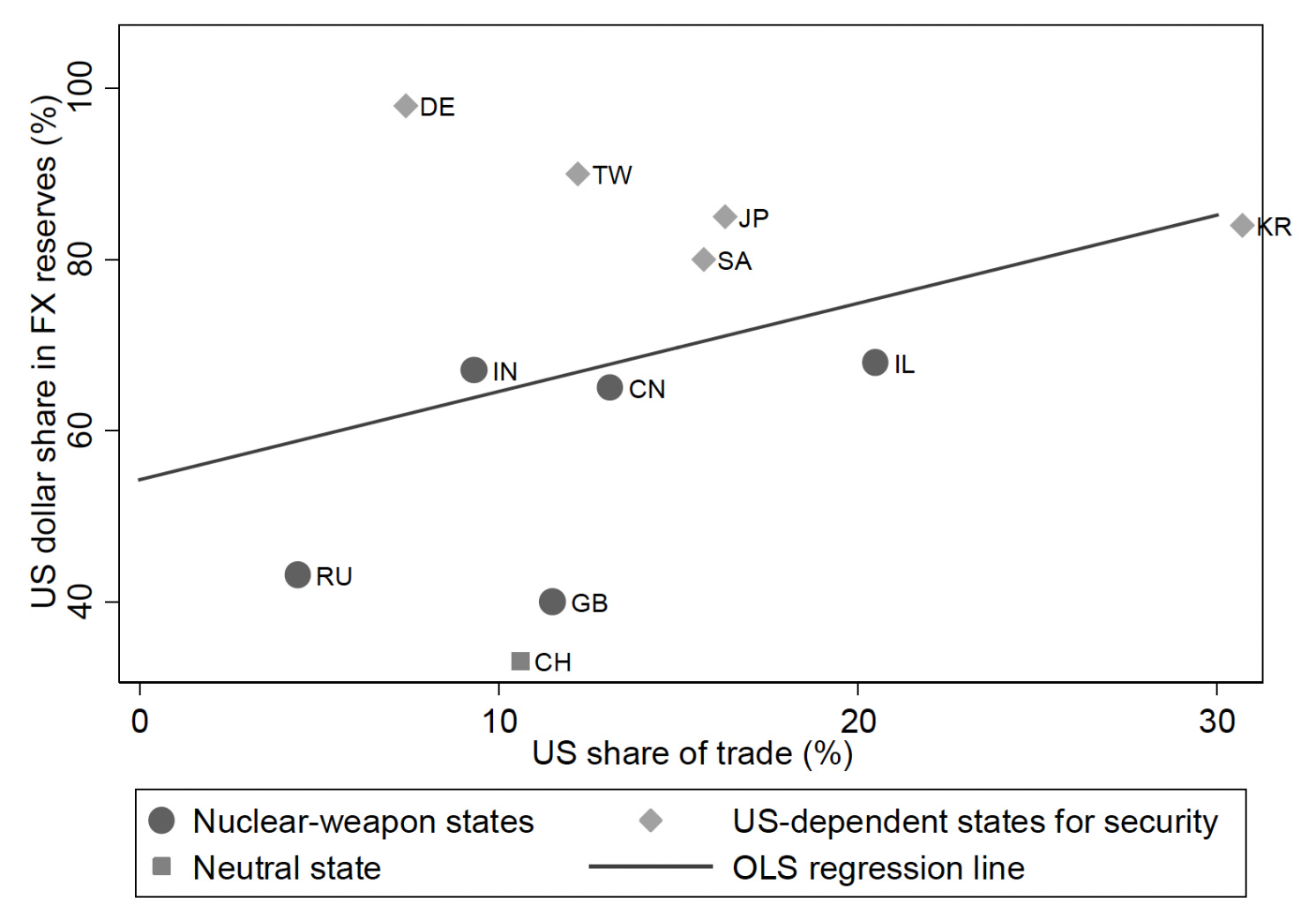

And fourth, though often understated in economic analyses, America’s security umbrella and global military presence. As Barry Eichengreen’s research shows, countries that rely on the U.S. for security tend to hold significantly more dollar reserves.

The Trump factor

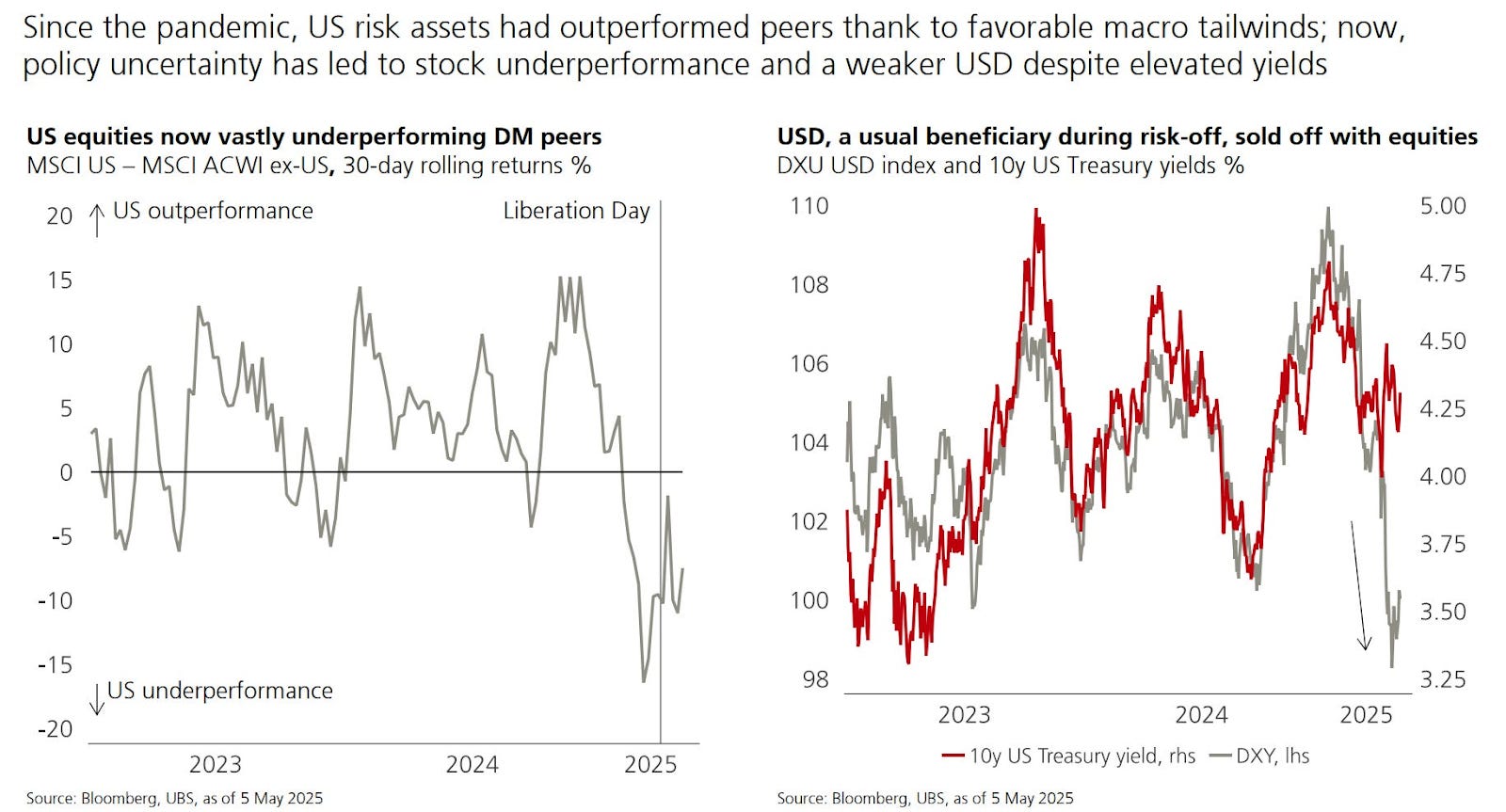

Now this dollar hegemony is facing new challenges. When Donald Trump unveiled his “liberation tariffs” on April 2nd this year – announcing a blanket 10% tariff on all imports and threatening specific countries with much higher rates – it sent markets into a tailspin.

What made this moment particularly notable wasn’t just the tariffs themselves, but how U.S. Treasuries performed during the market turbulence. Typically, when risk assets fall, investors flee to the safety of U.S. government bonds. But this time, Treasuries failed to provide that safe haven offset – a worrying sign for the foundation of the dollar-based financial system.

As Maurice Obstfeld of the Peterson Institute for International Economics noted in a recent conference, this episode was reminiscent of the 1971 Nixon shock. Back then, Nixon imposed a 10% import surcharge and took the dollar off gold to force trading partners to revalue their currencies. But today’s situation is even more consequential because Trump’s tariff actions are occurring in a much more globally integrated economy.

Perry Mehrling, professor of international political economy at Boston University, put it bluntly in a recent interview: “Trump is replaying the Nixon handbook.” But unlike 1971, when the dispute was primarily between the U.S. and Europe, today’s conflict involves a truly global economic ecosystem with complex supply chains and financial linkages.

What’s particularly concerning for financial markets is the uncertainty. As Mehrling puts it, “this attempt to play games with market valuations by announcing tariffs and then taking them off… is very bad for market liquidity.” Why would dealers take the other side of trades if policy could suddenly change?

Perspective on De-Dollarization

So how seriously should we take the threat of de-dollarization? Expert opinions vary significantly on both the likelihood and timeframe.

Ken Rogoff, former IMF Chief Economist and Harvard professor, offers a blunt assessment: “De-dollarization is less about how countries hold foreign exchange reserves and how much are in dollars… it’s about how money is being settled.” In a recent interview, he emphasized that while headlines have warned about the dollar’s decline for decades, what’s different now is the policy volatility.

“I strain for choosing words about how stupid it is,” Rogoff remarked about the current tariff approach. “The cure is worse than the disease.” He notes that throughout history, the dollar system has been counted out many times, yet consistently returned stronger after each crisis. However, he warns that the combination of fiscal pressures, attacks on Fed independence, and unpredictable trade policy creates a particularly dangerous mix.

Maurice Obstfeld adds another dimension, explaining that the biggest threat isn’t necessarily from direct competitors to the dollar, but from fragmentation of the global economy itself. “There’s a breakdown of the international monetary system where you don’t have stable exchange rates,” he explains. This instability makes planning difficult and disrupts capital flows, trade, and long-term investment decisions.

Obstfeld points to historical parallels with the “hot money” periods of the 1930s, when speculators would rapidly switch between currencies, destabilizing exchange rates and undermining the basis for international trade.

Josh Lipsky at the Atlantic Council offers a more nuanced view, suggesting we’re looking at the wrong indicators. He argues: “The dollar can be both healthy and weak at the same time, and what I think is happening is that we’re looking at the wrong indicators.”

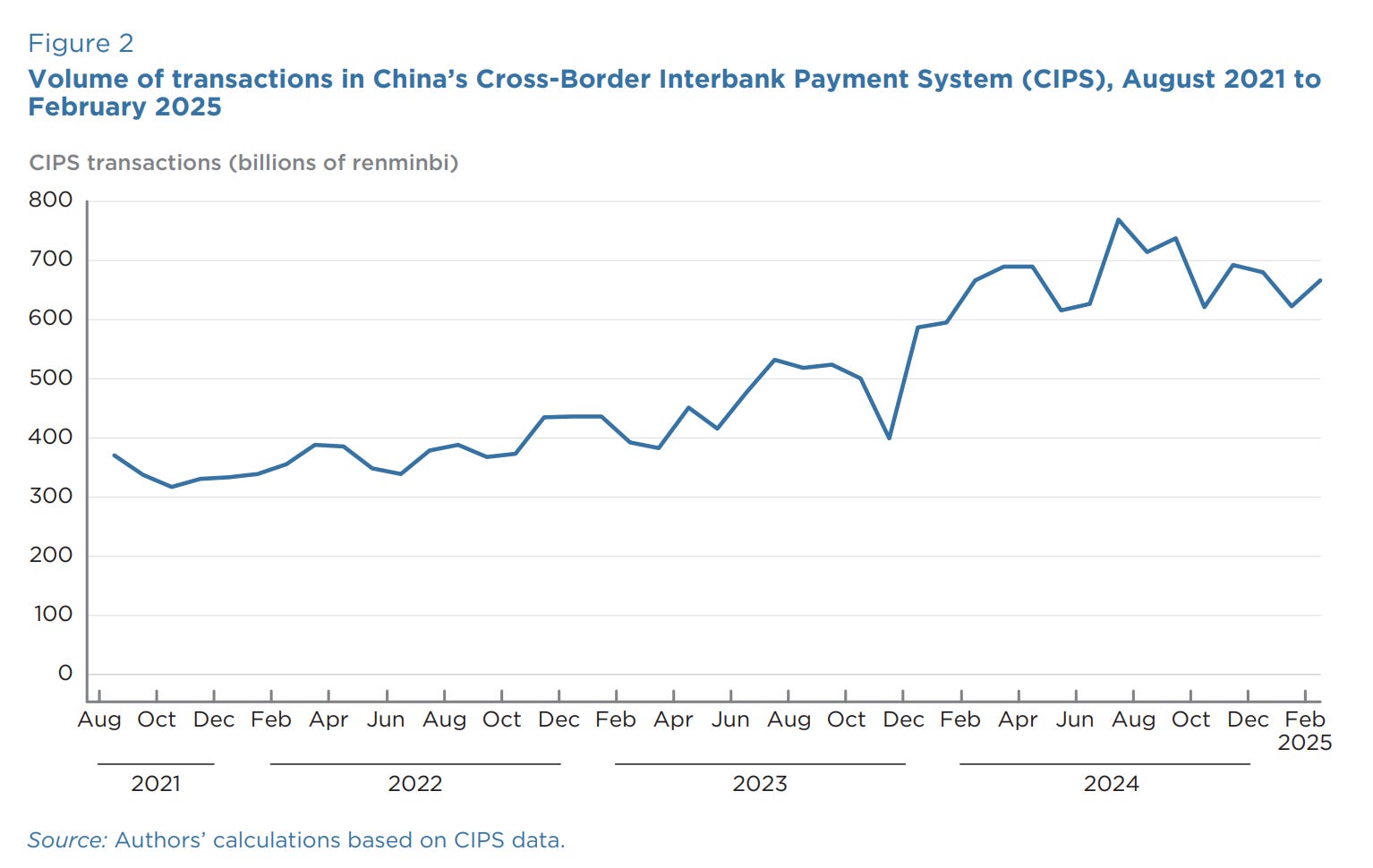

Lipsky distinguishes between lagging indicators like currency reserve shares and leading indicators like alternative financial plumbing. “These pipes that are getting built between commercial banks around the world don’t need dollars to settle,” he explains. Systems like China’s Cross-Border Interbank Payment System (CIPS) have doubled in size over the past two years, though they remain small compared to the Western SWIFT network.

Lipsky particularly highlights the development of central bank digital currencies, especially wholesale CBDCs for cross-border settlement. Projects like mBridge – involving China, Hong Kong, Thailand, UAE, and recently Saudi Arabia – could dramatically reduce settlement times and potentially lessen the need for dollars. “They can settle cross-border between these banks within a matter of minutes, as opposed to days,” he notes.

Markus Brunnermeier of Princeton University focuses on what he calls the “safe asset status” of U.S. Treasuries. This status allows the U.S. to run persistent current account deficits without having to pay them back – what Brunnermeier calls an “exorbitant privilege.” However, he warns that policy uncertainty and financial fragmentation could erode this status, raising U.S. borrowing costs.

According to Brunnermeier, “Uncertainty is like a tax without any revenue.” It creates risk premiums that make borrowing more expensive without generating any benefits. Recent policy volatility, he suggests, is creating exactly this kind of uncertainty tax on the U.S. economy.

The gradual shift scenario

Most experts agree that any de-dollarization will be gradual rather than sudden. A recent report from the Peterson Institute concludes that “the transition to a new multipolar world will be a long process.” The report notes that while de-dollarization in FX reserves continued in 2024, “what was new was that the euro was the key beneficiary last year.”

This echoes findings from a recent ING report, which observed that central bank holdings in euros increased by €128 billion in 2024, representing 40% of the global annual increase in allocated FX reserves. While the euro’s share remains below its early 2000s peak, this represents a notable shift in central bank preferences.

Christopher Waller, a Federal Reserve Governor, recently acknowledged the risks but maintained confidence in the dollar’s position: “Recent commentary warning of a possible decline in the status of the U.S. dollar raises concerns about the effects of sanctions against Russia, U.S. political dysfunction, the rise of digital assets, and China’s efforts to bolster usage of the renminbi.” Despite these concerns, he emphasized that “by standard measures of an international currency’s use, there has not been any notable erosion in the dollar’s dominance over the past couple of decades.”

Several factors could accelerate this gradual shift:

First, technological innovation. As Lipsky emphasizes, “Financial technology is finally catching up with the demand” for alternatives to dollar-based settlement. The development of CBDCs, blockchain-based systems, and improvements in cross-currency payments could reduce the need for a vehicle currency like the dollar.

The Brookings Institution highlights this point, noting that “transactions between pairs of emerging market currencies are becoming easier as financial markets and payment systems mature.” For example, direct exchange between Chinese renminbi and Indian rupees could soon become cheaper than converting both currencies to dollars first, reducing reliance on the dollar as a “vehicle currency.”

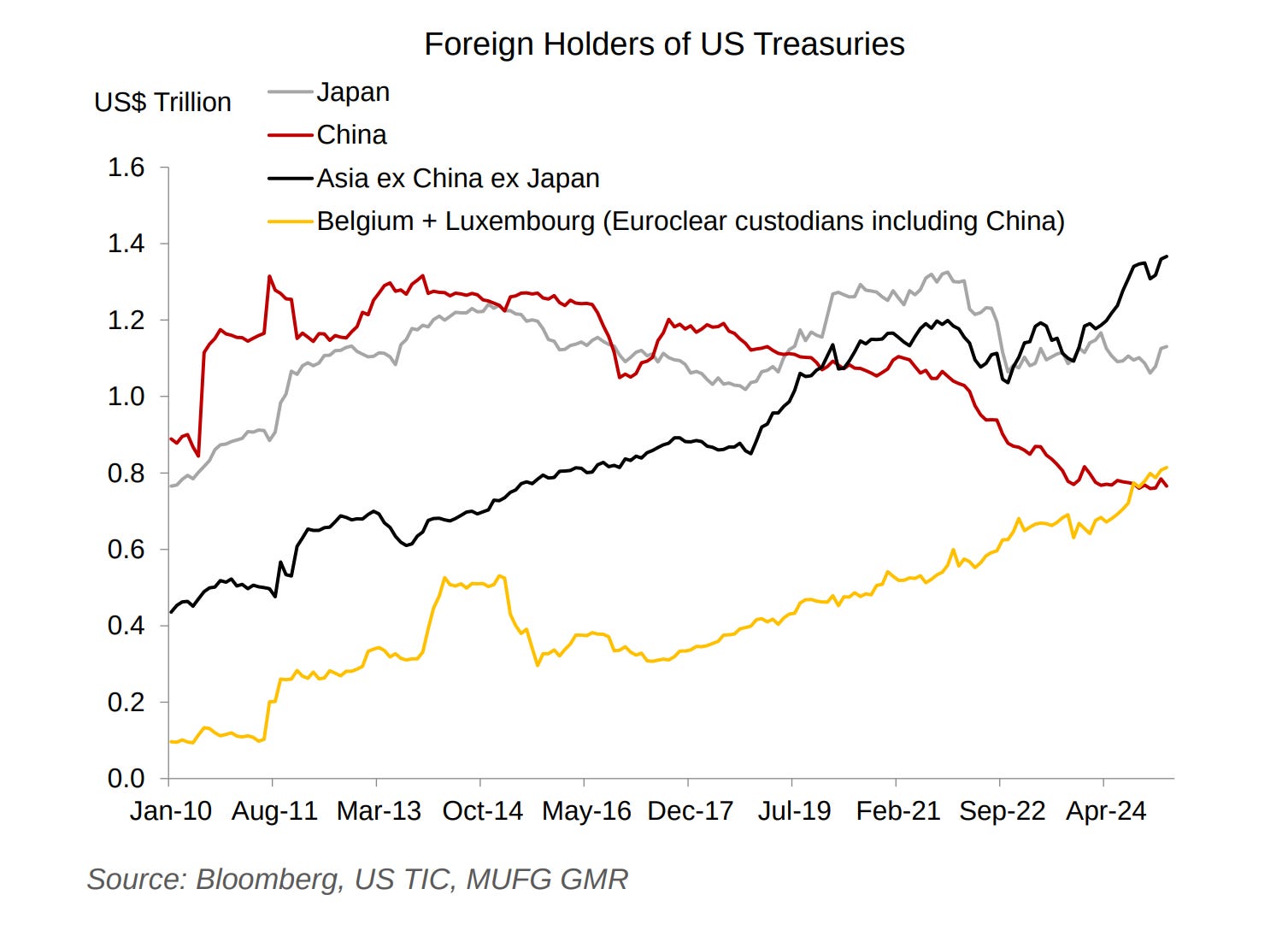

Second, the “domestication” of the U.S. Treasury market. According to Martin Chorzempa at the Peterson Institute, the share of foreign holders of U.S. Treasuries has gradually declined from 54% before 2008 to 33% currently. Foreign official holders – central banks and sovereign wealth funds – have seen their share more than halve, from 28% to 13%.

Chorzempa’s research shows that this shift isn’t just about the U.S. – it reflects changing patterns in global finance. China’s Cross-Border Interbank Payment System (CIPS) has grown rapidly, doubling in size over the past two years, though it remains small compared to Western alternatives. While SWIFT only handles messaging for payments, CIPS combines both messaging and settlement, making it potentially more efficient.

Moreover, projects like mBridge – involving central banks from China, Hong Kong, Thailand, UAE, and Saudi Arabia – are exploring blockchain-based wholesale central bank digital currencies that could bypass Western payment systems entirely. These developments may not pose an immediate threat to dollar dominance, but they show how digital technologies could reshape cross-border finance.

Third, shifting geopolitical alignments. Barry Eichengreen’s research shows that countries relying on the U.S. for security hold disproportionately more dollar reserves. As America’s security commitments come into question or as alternative security arrangements emerge, currency preferences could shift accordingly.

Fourth, the growth of regional trading blocs. As Warwick McKibbin noted in a recent presentation, the center of gravity in global trade has been shifting toward Asia for decades, and this could eventually affect currency usage as well.

Wrap-up

So what’s the bottom line on de-dollarization? It’s happening, but at a pace that’s more evolutionary than revolutionary.

The dollar’s network effects remain powerful. The more people use it, the more useful it becomes to everyone. And despite repeated predictions of its demise – like a 2011 headline declaring “Why the Dollar’s Reign Is Near an End” – the greenback has shown remarkable staying power.

Christopher Waller, a Federal Reserve Governor, recently made this point: “In times of global financial stress… there is almost always a flight to the dollar. This is the ultimate vindication that the U.S. dollar is the world’s reserve currency.”

But the landscape is shifting beneath our feet. We’re likely moving toward what economists call a “multipolar currency world” – not one where the dollar disappears, but where it shares the stage more evenly with currencies like the euro and perhaps eventually the renminbi.

As Helene Rey of the London Business School recently explained, we may be witnessing what she calls a “New Kindleberger Gap” – named after the economic historian Charles Kindleberger. In the 1930s, Britain, a fading hegemon, lacked the ability to provide global public goods like a stable currency, while the ascendant U.S. lacked the will. Today, the question is whether the current hegemon (the U.S.) lacks the will to provide a stable dollar while an ascendant power (potentially the EU) lacks the ability.

For investors, these shifts suggest gradually increasing exposure to non-dollar assets as part of a diversified portfolio. For policymakers, they underscore the importance of maintaining confidence in dollar-denominated assets through responsible fiscal and monetary policy.

The dollar’s exorbitant privilege isn’t guaranteed – it requires ongoing investment in the institutions and policies that made the dollar dominant in the first place. Whether the U.S. will make those investments remains an open question, and one that financial markets will be watching closely in the months and years ahead.

Tidbits

- India Aims for 5% Global Chip Share by 2030, Projects 91 Million Daily Output

Source: Business Standard

India has set an ambitious target to capture 5% of global semiconductor chip production by 2030 under its Semicon 2.0 strategy. The government has already committed funding from its $10 billion incentive package, with five projects cleared by the Ministry of Electronics and IT having a combined capacity of 75 million chips per day. An additional 16 million chips per day are expected from state-approved projects, pushing total projected daily output to 91 million. The Tata Group is leading with an investment of ₹91,000 crore for its fabrication plant, the largest among six upcoming facilities with a total investment of over ₹1.55 trillion. Companies like Polymatech, currently producing 6 million chips per day, and Micron, expected to start output by year-end, are also part of this initiative. The plan covers both fabrication and OSAT/ATMP operations, with India aiming to expand its presence across the entire semiconductor value chain.

- Apollo in Talks to Invest $750 Million in Adani’s Airport Bonds as Group Plans $1.5 Billion Fundraise

Source: Business Standard

Apollo Global Management is in advanced discussions to invest $750 million in bonds issued by Mumbai International Airport Ltd (MIAL), part of Adani Airport Holdings Ltd (AAHL). The investment is expected to be routed through Apollo’s insurance arm. Alongside this, AAHL is also looking to raise an additional $750 million in loans from international lenders. The funds will be used for capital expenditure and to refinance dollar debt maturing in September. This comes as Adani Enterprises outlines a ₹1.32 trillion capex plan for FY25–FY27, with ₹44,000 crore allocated to airports. The group aims to invest $100 billion by 2030 across infrastructure sectors. In April, Adani also secured $750 million from global lenders for acquiring ITD Cementation, with BlackRock contributing $250 million. The Navi Mumbai greenfield airport under AAHL is expected to become operational next quarter, and the company is considering an IPO in the next 2–3 years.

- Vodafone Idea Approaches Supreme Court Over ₹81,500 Crore AGR Dues Dispute

Source: Reuters

Vodafone Idea has moved the Supreme Court after the government rejected its request to waive over $5 billion in penalties and interest. The plea follows a formal rejection by the Department of Telecommunications on April 29, which stated that the relief sought “cannot be considered.” Vi’s CEO Akshaya Moondra, in a letter dated April 17, warned that without financial relief, the company would be unable to continue operations beyond FY26. The government currently holds a 49% equity stake in Vi following a debt-to-equity conversion of past dues. The company argues that the waiver is essential to ensure continuity in the telecom sector, citing public interest and the need to maintain competitive balance. This legal challenge brings fresh uncertainty to a dispute that originated from the Supreme Court’s 2019 AGR ruling, which expanded the definition of telecom revenues and sharply raised liabilities for operators.

- This edition of the newsletter was written by Kashish and Bhuvan.

Have you checked out The Chatter?

Have you checked out The Chatter?

Every week, we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Introducing “What the hell is happening?”

In an era where everything seems to be breaking simultaneously—geopolitics, economics, climate systems, social norms—this new tried to make sense of the present.

“What the hell is happening?” is deliberately messy, more permanent draft than polished product. Each edition examines the collision of mega-trends shaping our world: from the stupidity of trade wars and the weaponization of interdependence, to great power competition and planetary-scale challenges we’re barely equipped to comprehend.

What the hell is happening?

What the hell is happening?Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()