Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Banks recovered, but have new worries

- Empty recycling plants await a deluge of used batteries

Banks recovered, but have new worries

For four straight quarters now, we’ve been tracking the same handful of frictions in Indian banking. And every quarter, we’d end the piece with a “scoreboard” of things to watch in the next one, expecting part of the picture to shift.

Now, Q4 FY26 is the quarter where it might have shifted. Almost every friction we’ve been tracking through FY26 has either resolved or quietly evolved.

But just as all that good news arrived, banks started behaving like they were preparing for trouble by setting aside provisions for two things: one, the Strait of Hormuz crisis, and two, the possibility that rate-cut cycle might be already over.

So this quarter is two stories layered on top of each other. The first story is the resolution of everything we’ve been tracking. The second is the new worries that have emerged.

Let’s go through them.

The corporate comeback

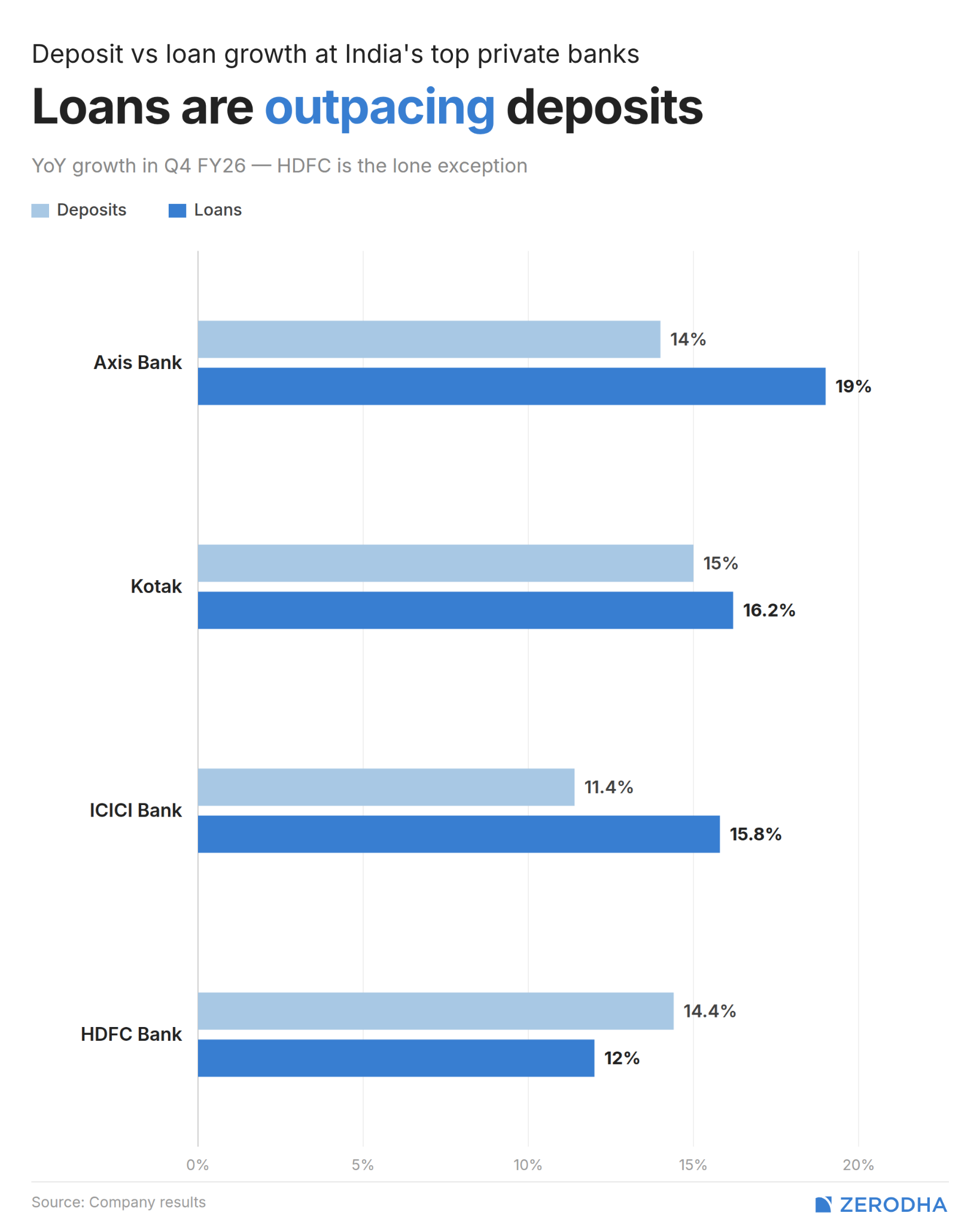

In our Q2 coverage, we saw that corporate growth across the four big private banks was running in the mid-single or low double digits. The story was that India’s private sector wasn’t doing much capex, and large companies were tapping equity markets and bonds instead of bank loans. Partly due to that, banks were left chasing growth in the retail and SME segment.

That description, however, doesn’t fit Q4.

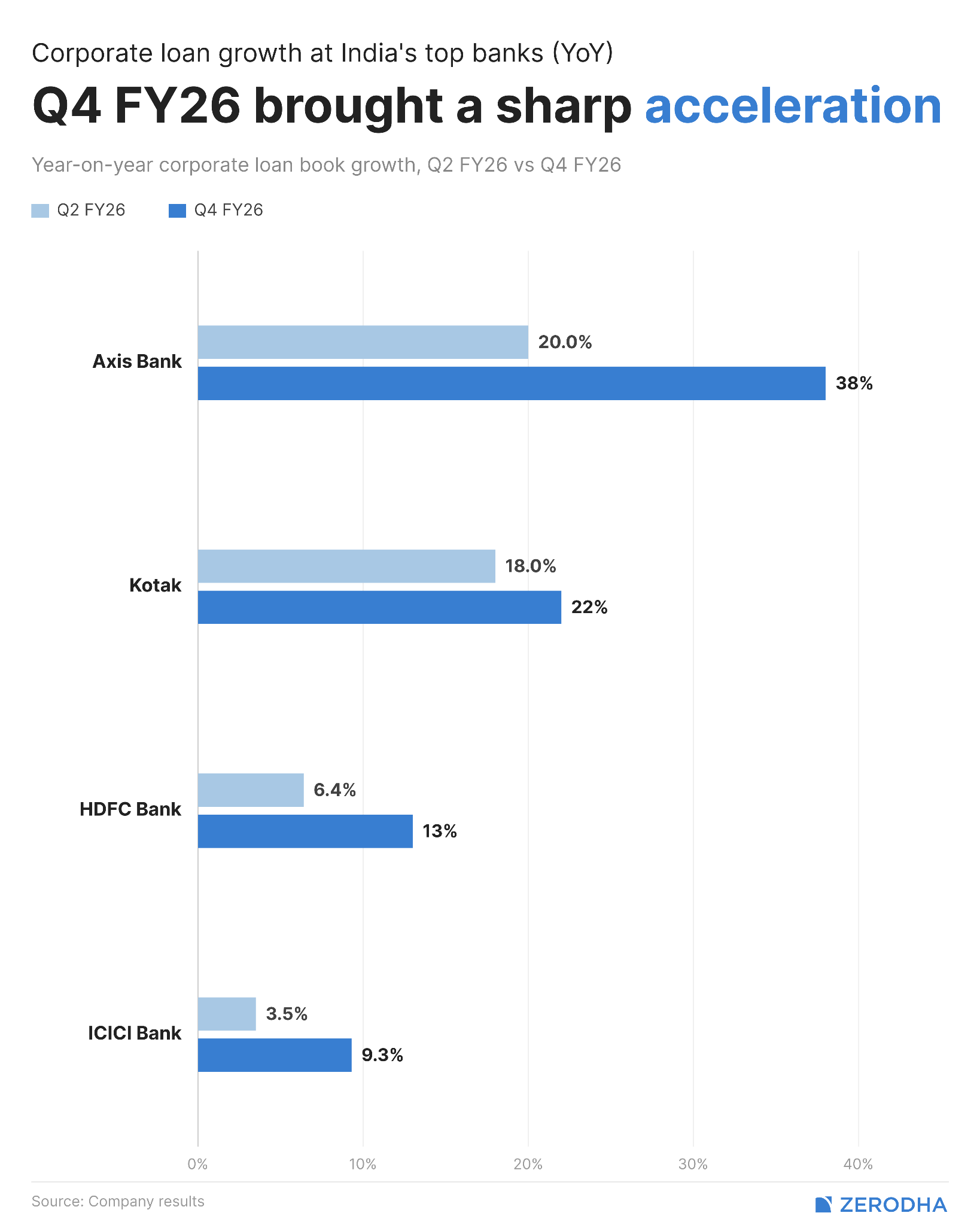

For instance, Axis’ corporate book grew a robust 38% year-on-year in Q4. ICICI’s domestic corporate grew about 9%, which doesn’t sound dramatic until you remember it was at 3.5% just two quarters ago. Kotak grew its corporate banking book 22% YoY. HDFC’s “corporate and other wholesale ” book grew 13%.

So what changed?

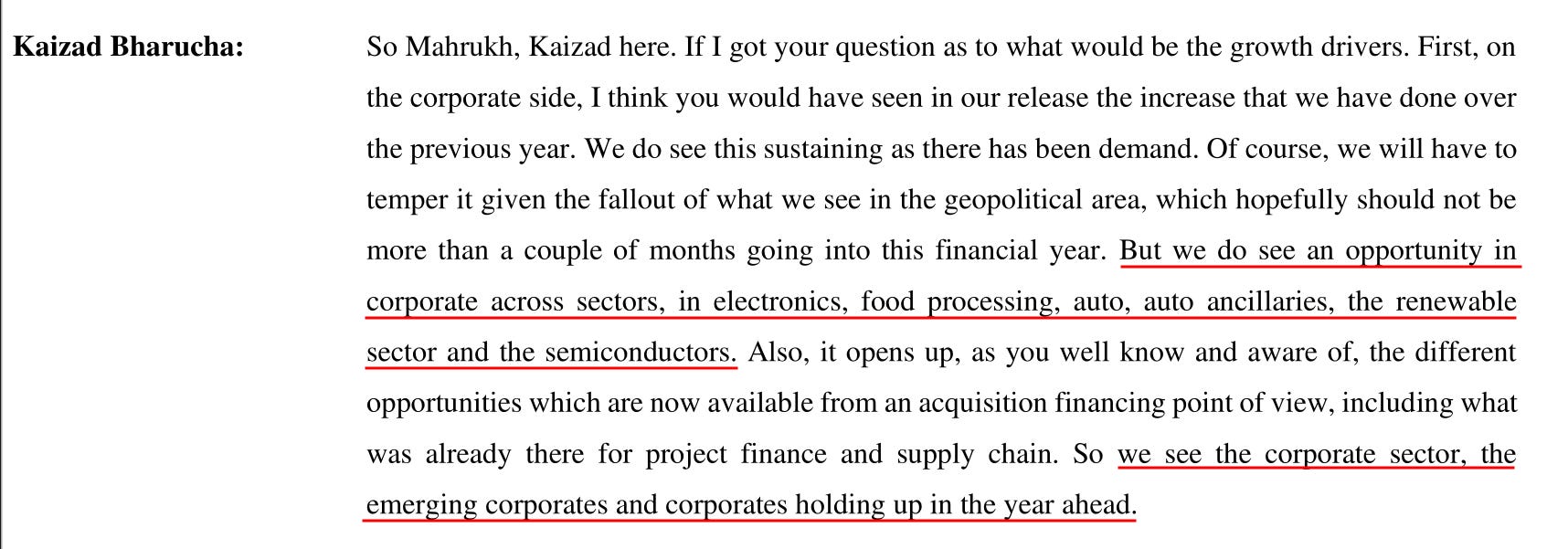

Part of it is genuine demand. For HDFC, activity came from electronics, food processing, auto, renewables, semiconductors, and acquisition financing. This is a list of structurally growing pockets of the Indian economy where companies are now borrowing again.

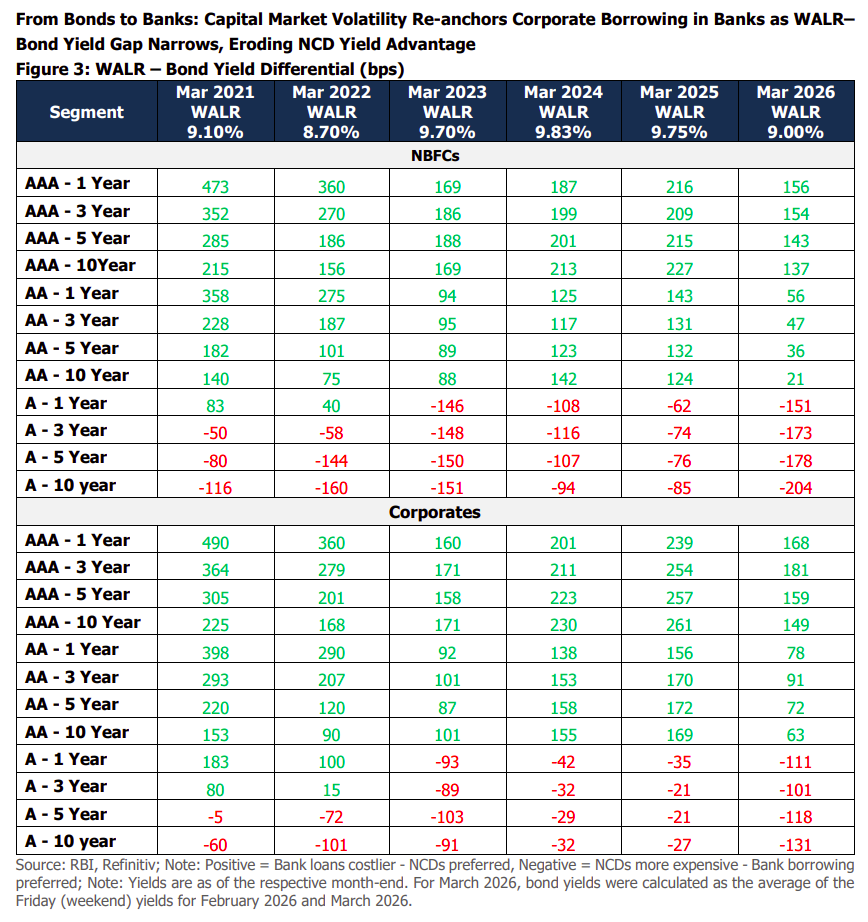

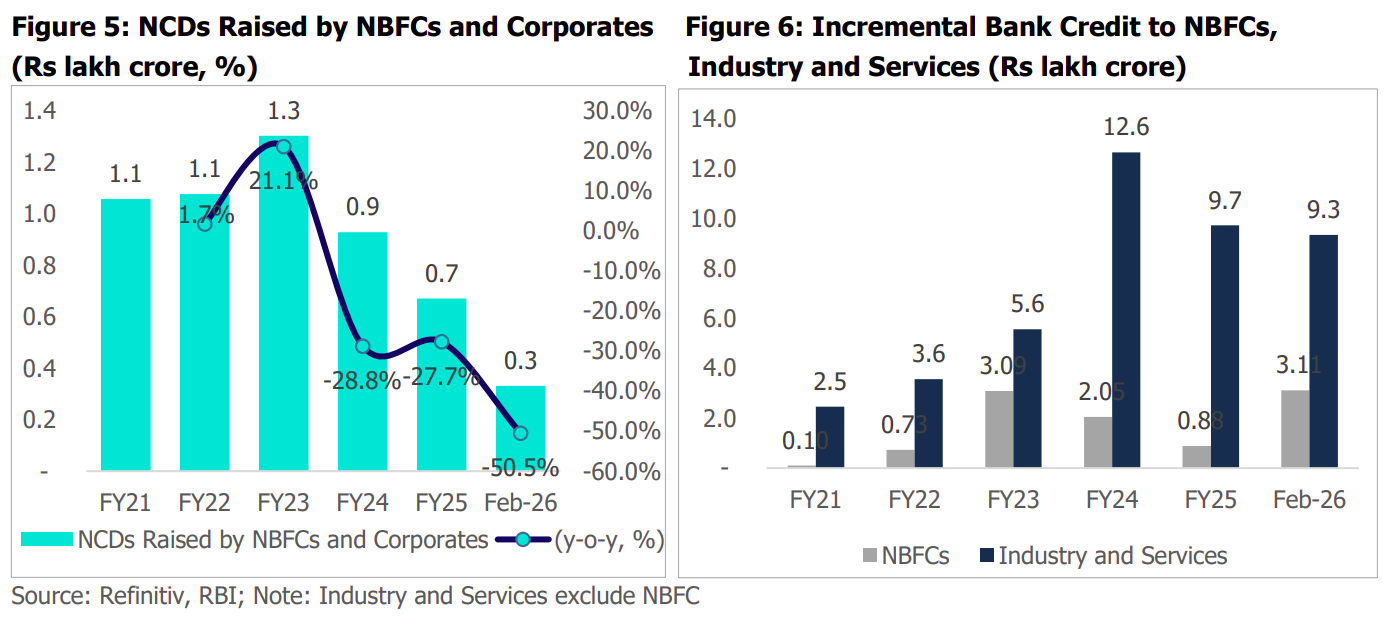

Part of it is an interesting cost story. As per CareEdge’s recent BFSI report, the cost advantage that bonds had over bank loans has largely disappeared.

See, 5 years ago, a AAA-rated NBFC borrowing for 1 year through a bond would have paid ~4.7% less than what banks were charging. But by March 2026, that gap had compressed to about 1.5%. For AA-rated borrowers, the gap is now barely 0.5% - 0.8%. And for A-rated corporates and NBFCs, bonds are now more expensive than bank loans.

This is no minor shift, either. Debenture issuances by NBFCs and corporates peaked at ₹1.30 lakh crore in FY23. That number has collapsed by ~75% by FY26 — to ₹0.33 lakh crore. Meanwhile, bank credit to industry, services, and NBFCs has done the opposite.

To a large degree, then, corporates came back to banks simply because it made more economic sense to shift from bonds. But that also tells us why this comeback might persist. As long as bond yields stay sticky and bank rates remain relatively stable, this rotation continues.

Now, this isn’t the kind of indiscriminate large-corporate lending that got Indian banks into trouble last decade. Back then, banks chased volume and market share, often pricing loans too cheaply for the risk they carried. When the cycle turned, the losses were brutal.

This time around, though, the discipline looks stronger, and banks wish to avoid mistakes of the past.

Axis’s CFO described their wholesale push as “risk-adjusted ” — in other words, they’re picking deals where the return justifies the risk, not just chasing growth. They’ve also been clear that the heavy wholesale tilt is a short-term call; over the next three years, they plan to rebalance back toward retail. HDFC keeps repeating that it won’t chase volume at the expense of pricing. Kotak actually walked away from large project finance deals last year because the pricing was too thin to make sense.

The deposit story finally relaxes

You may remember from our past banking stories that, through most of FY26, the deposit squeeze was the central worry. Q3 was the moment when banks openly admitted they were losing the deposit war. Kotak said deposits were leaking to the stock market, HDFC said it was choosing not to pay up for bulk deposits, and Axis said deposit and credit growth wouldn’t converge for 15-18 months.

In Q4, the squeeze finally let up.

The headline numbers are good across the board. For HDFC, in fact, deposits actually grew faster than its loans for the year — a structural shift the bank’s been waiting for since its merger.

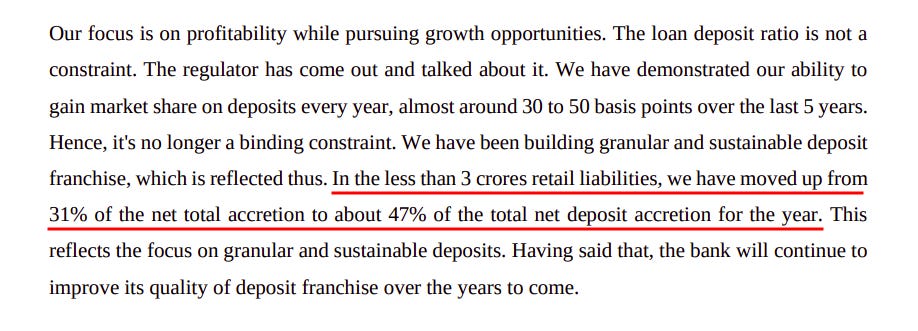

But beyond the headline, HDFC dropped a stat in the call that’s worth pausing on. Their sub-₹3 crore time deposits — which are the granular, sticky retail kind — went from being 31% of net incremental deposits in FY25 to 47% in FY26. That’s a dramatic compositional change in a single year.

This is the opposite of how the deposit war played out in Q3. Back then, HDFC was accepting it had fallen short of its deposit ambition but now, they’re saying they could have raised more — they just chose not to, because the deposits on offer were too expensive and not the kind they wanted. That’s a confidence shift.

Now, it’s worth noting that some of this Q4 strength is seasonal. The fourth quarter always benefits from year-end government spending, corporate tax flows, and balance sheet management, all of which inflate deposit numbers temporarily. The real test of whether the deposit franchise has actually improved will come in Q1 FY27, when those flows reverse. So while promising, we can’t say for sure that the deposit problem is fully solved.

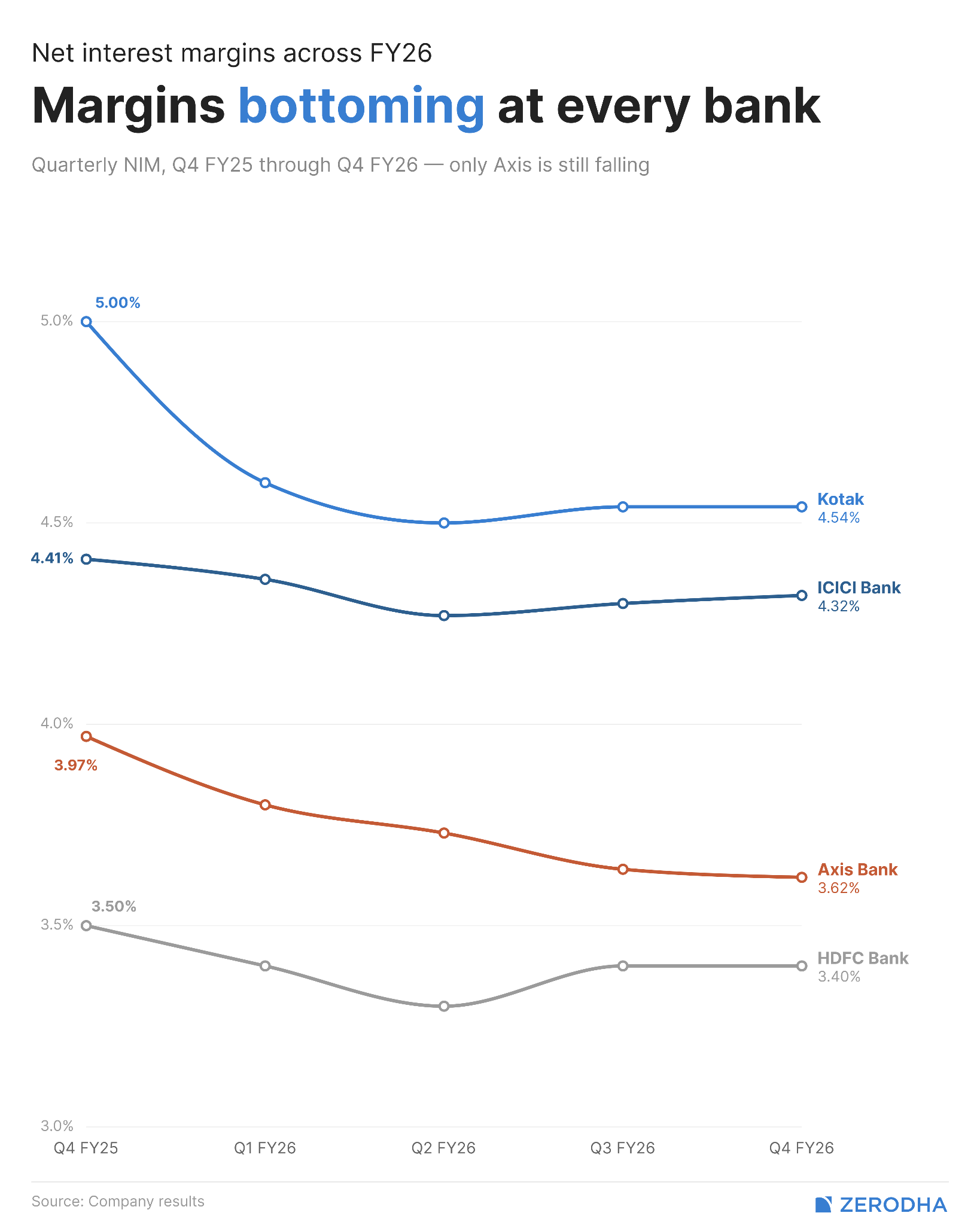

Margins stabilize, and the cycle quietly ends

Tracking the margin story across the year has been an exercise in waiting for the bottom.

Through the year we saw India’s repo rate fall from 6.5% to 5.25%. Resultantly, in Q1, the net interest margins (NIM) of banks were squeezed because asset yields fell faster than deposit costs after the repo cut. In Q2, there were “early signs of bottoming “, while the expectation in Q3 was that Q4 would be where the timing mismatch might finally be resolved.

Well, the bottom has finally arrived this quarter, and margins have stopped falling.

The mechanism is exactly what we outlined around a quarter ago. Asset yields had taken the full brunt of the repo cut earlier in the year. But deposit costs were the laggard, as it takes more time for a repo cut to translate into deposit rate changes. By Q4, the deposit repricing finally caught up enough to offset the asset-yield drag.

But there’s a wrinkle in the HDFC commentary that deserves attention, because it could matter quite a lot for FY27.

HDFC thinks the rate cuts may already be done. The bond market is pointing at rates going up, not down, partly because of geopolitical pressure on oil and the rupee. If they’re right, then the residual deposit-repricing benefit that everyone is waiting for is much smaller than the market expects, because banks won’t get a fresh tailwind of further rate cuts pushing deposit costs lower. In other words, NIMs will stabilize, but they may not expand .

The unsecured pause is ending

Throughout the past fiscal year, we kept tracking the deliberate slowdown in unsecured retail. Banks had pulled back after the RBI’s risk-weight tightening in late 2023. Personal loans, credit cards, and small-ticket consumer credit were all being rationed. Q3 was where banks said the books had been cleaned up, but they weren’t ready to grow them yet.

We even tracked this trend through the lens of microfinance (MFI) lending, where the downward cycle seems to have bottomed out. For more on this, do check out our Plotlines story, where we tracked the commentary of 18 companies across 8 quarters to make sense of the MFI cycle.

Similarly, Q4 became the first quarter where private banks began growing their unsecured books again — cautiously .

Kotak’s unsecured retail book, for instance, grew by ₹1,200 crores in Q4 — more than double the ₹517 crores added in Q3. Devang Shah, Kotak’s CFO, said the unsecured retail portfolio “started showing gradual growth in absolute terms “. Crucially, the share of unsecured lending in net advances stayed flat — which means they grew it without growing their risk profile.

However, within unsecured loans, personal loans , and not credit cards, are driving the growth. Credit card portfolios are still actively shrinking at two of the four banks.

Why does this matter? Well, unsecured lending is the only place where margin expansion can actually happen when rates have plateaued. If the rate cycle is done, and asset yields aren’t going to rise, then the only way to grow NIM is to mix the shift toward higher-yield products. Unsecured personal loans yield far more than mortgages or corporate loans. So this re-acceleration, if it sustains into FY27, is the most plausible source of the next leg of bank earnings growth.

The new worry

Despite all of the above, banks behaved as if they were preparing for something to go wrong — which did happen, in Iran. This wasn’t on our radar in Q3. The geopolitical situation has clearly escalated meaningfully between then and now. And in Q4, three out of four banks talked about it directly in their earnings calls.

One of them, Axis, even put real money behind it. Axis took a voluntary one-time standard asset provision of ₹2,001 crores this quarter. The provision isn’t tied to any visible credit stress, though — their CFO, Puneet Sharma, said as much. The biggest reason for this provision is the uncertainty from the tensions in the Strait of Hormuz. The provision is tied to an identified pool of accounts that Axis’ risk team flagged as potentially vulnerable to a West Asia shock.

So, it’s not a floating provision meant for general stress, but it’s earmarked. If accounts from that pool slip due to the crisis, this provision absorbs the hit. If the crisis fades, the provision can be written back.

The other banks didn’t create similar provisions, but the topic came up across all of them. Kotak’s Ashok Vaswani spent a meaningful amount of time speaking about the Strait of Hormuz, the impact of higher oil and gas prices on India’s macro, and the risk of a below-normal monsoon. HDFC pointed to West Asia as one reason why rates may have bottomed, and as something that needs to be factored into corporate growth expectations.

While every reported credit stress metric is at multi-year lows, the most important capital allocation decision in the quarter was a ₹2,001 crore preemptive provision for a stress scenario nobody is visibly experiencing. Banks may have stopped worrying about the present, but, of course, they (or anyone else) can’t do so about the future.

Scoreboard for Q1 FY27

So, what are the things we should watch heading into the next quarter?

First, does the corporate comeback sustain or was it lumpy? Q1 will tell us whether banks were front-loading FY26 disbursements or whether the demand is genuinely durable. Second, does deposit growth honestly hold up after Q4 seasonality fades? Third, has the rate cycle actually bottomed? HDFC thinks it has, and if they’re right, the margin tailwind everyone is expecting won’t come, and margins may remain flat from here rather than expand. Fourth, the West Asia trajectory. If it de-escalates, Axis writes back its provision and books a tailwind. If it escalates, the question becomes whether the other three banks need to follow Axis’s lead.

So Q4 FY26 isn’t the start of an easy stretch. It’s the moment when the things we’d been worried about for a year finally got resolved, and the things we weren’t worried about took their place.

Empty recycling plants await a deluge of used batteries

The world’s battery industry has scaled at a pace that’s hard to picture. As recently as 2020, manufacturers deployed just 180 gigawatt-hours of battery capacity globally. By 2024, that figure had boomed to 1,100 gigawatt-hours — a six-fold expansion in four years. By 2030, it’s projected to more than triple yet again.

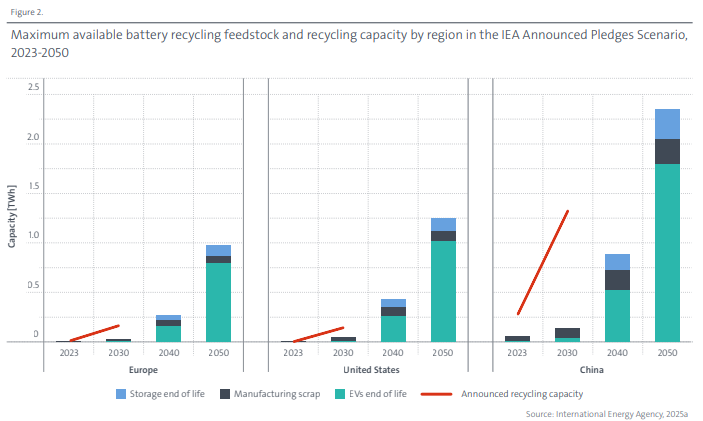

The reason for this is obvious. More than one in four cars sold globally last year was electric. And today’s EV wave is a battery trash wave for tomorrow. Every one of those cars has a battery with a finite life. They’ll have to be disposed of in the near future. Around 1.2 million EV batteries will reach the end of their lives in 2030. By 2040, that number shall rise to 14 million. By 2050, 50 million.

Think about that: fifty million dead car batteries a year, packed with key minerals like lithium, nickel, cobalt and copper. If we don’t learn how to recover those minerals, all of that shall be locked up in landfills. The only sensible response before us is to learn how to process and recycle those batteries. That’s the subject of a fascinating new report from the International Energy Agency.

But before we get there, we’ll have to deal with a paradox: we have nothing to recycle just yet . Take China — it aggressively built out recycling capacity. But now, it has so much overcapacity that if every available battery in the country were collected and processed tomorrow, its plants would only run at 20% of capacity.

A recycling wave is coming, but the plants are half-empty.

Why recycling is the only sensible path

Put simply, the green transition doesn’t happen unless we master recycling. The technologies we bank on to power our future all require a range of minerals — many of which are in short supply. It’s hard to outrun these challenges with mining alone. Opening a new mine takes a decade and costs billions, apart from the severe environmental and political baggage it comes with.

As we’ve written before, recycling is arguably the only realistic path for us to step up supply quickly and for cheap. It’s also much lighter on the planet — producing roughly 80% lower greenhouse emissions than primary mining.

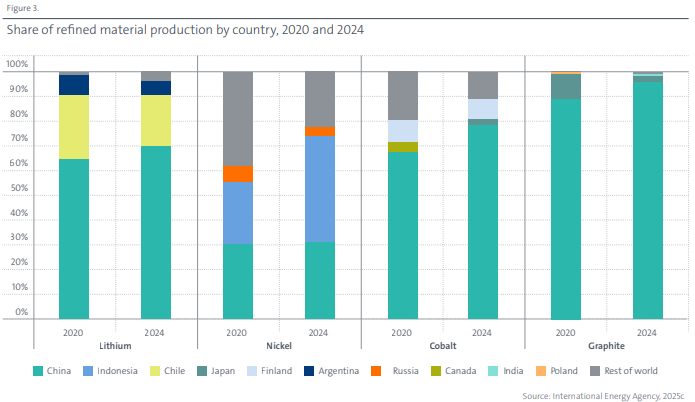

Recycling is also smart geopolitics . The supply chain for battery materials is one of the most concentrated in the global economy. China dominates the refining of 19 of the 20 strategic critical minerals that power these systems. The top three countries in these supply chains own 86% of the supply. And this concentration is getting worse , not better.

Individual countries own entire mineral supply chains. Two-fifths of the world’s nickel comes from Indonesia alone. Two-thirds of the world’s cobalt comes from the Democratic Republic of the Congo. As recent months have taught us, dependencies like this can turn into a global crisis in the space of days. Meanwhile, according to the IEA, if we set up enough recycling infrastructure, by 2040, all that secondary supply could meet over 20% of lithium, nickel and cobalt demand.

Recycling may not help us eliminate our dependencies, but it can give us a valuable lifeline.

A puzzle without solutions

We’ll soon go into the progress we’ve made with setting up recycling infrastructure, and the roadblocks we face on that journey. Before we get there, however, it’s helpful to have a sense of what recycling actually entails.

We begin this process with dead batteries, of the sort you’re probably familiar with. We want to pull out everything valuable we can from them — all the lithium, nickel, cobalt, copper, manganese and graphite still locked in there, in a form that’s pure enough to make a new battery.

But there are a lot of problems along the way.

A used battery is a dangerous thing. It still carries charge. It tends to heat up uncontrollably until it spontaneously blows apart. It has horrible chemicals inside that can cause harm. A leak or a burn can release fluorinated gases that can kill you if you breathe them in. Before you can do anything with that battery, you need to drain its remaining charge, isolate it, and transport it safely — often handling it using robots so that you’re safe if it catches fire mid-process.

At this point, you run into the next problem: a battery is engineered to not come apart. The valuable bits — the cathode and anode powders that hold most of the critical metals — are coated onto thin metal foils, glued together with polymer binders, and sealed inside packaging designed to last a decade in a moving car. You need to strip all of that away to get to what you actually want. For that, you shred the battery in controlled conditions, remove most of what you get, until you’re left with what’s called “black mass” — a concentrated grey-black dust where almost all the battery’s value lives.

This black mass is a mess. It has all the minerals you want, but mixed in is a lot of other stuff: graphite from the anode, copper and aluminium from its foil, plastic from the binders, residues from the electrolyte, and more, all mixed together. This becomes a chemistry problem: you need to put that black mass through a series of chemical processes until you’re left with battery-grade output — not low-grade scrap, but something that’s pure enough to go back into a new cell.

We’ve described some of these chemical processes before.

A series of regulations is pushing the world’s recycling industry towards one of these — “hydrometallurgy ” — where the black mass is dissolved in acid, and then all the metals we want are pulled out as salts.

This is, in other words, a fairly difficult process to master. We’re still in the early stages of learning how to do so at scale. A lot of the technology we need to do this effectively is being invented right now. Unfortunately, the numbers don’t make it very easy to do so just yet.

The valley of death

By all accounts, we’re going to be hit by an enormous wave of used EV batteries in the mid-2030s.

If we want to meet that wave head-on, we must begin preparing for it now . Recycling infrastructure takes 5–10 years to build. It requires capital investment, regulatory approvals, a trained workforce, and the supply chains and relationships that make it useful. Once the dead batteries start rolling in, we’ll no longer have the time to set all of this up.

If we do build all this now, however, we’ll be building for raw material that doesn’t exist yet. In fact, we don’t currently recycle EV batteries at scale. Almost all of today’s recycling feedstock comes from manufacturing scrap — the offcuts and rejected cells from battery factories. Most of the world’s electric vehicles aren’t old enough for their batteries to need recycling. And they won’t be, for years.

This puts us in a bind: what the IEA terms a “valley of death”. If you’re an early mover, you’ll lose money for years before the wave arrives, running expensive plants without any feedstock. If you wait, you’ll struggle to scale fast enough to handle the deluge. There’s no clean, rational middle path.

This is why Chinese recycling plants, today, are practically empty. It’s simply the outcome of a structural bind. China just has it worst because it built its infrastructure out the fastest.

When the wave of batteries comes, the winning companies are those that could afford to wait, operating at a loss and biding their time.

The race to innovate

But that wave will eventually come. All the BYDs and electric Tatas or Mahindras you see on the street, today, will eventually grow old. Their batteries will stop working. They’ll all pile up in some factory somewhere, waiting to be dismantled. When that time comes, companies that figure out the necessary technology today will be best positioned to deal with it all.

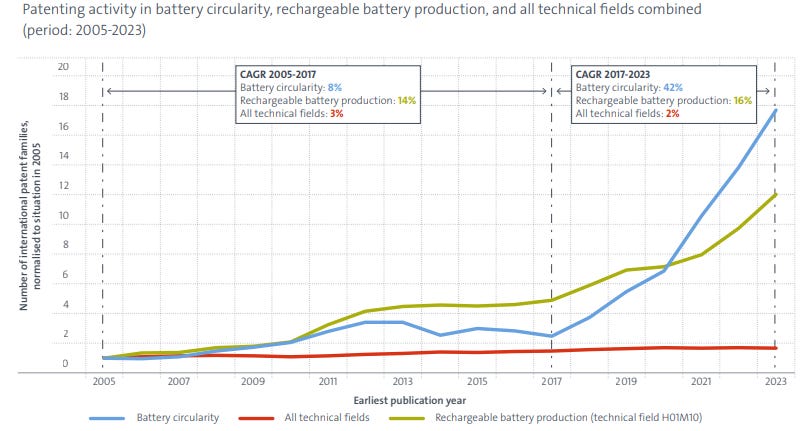

There is, in fact, already an ongoing race to put those technologies together. The IEA has been using patent records as a proxy for how things are coming along. As it found, the number of international patent filings around battery recycling have been growing at 42% a year between 2017 and 2023. Compounding . That’s considerably faster than innovations in making batteries — which are growing at 16%. For perspective, across the board, patent filings only grow by ~2% per annum.

Asia, led by China, is at the forefront of this wave of innovation. 63% of the world’s patents in the field come from the continent.

The big innovators in this field, until as recently as 2019, used to be companies from Japan and South Korea, like Toyota or LG. But then, China burst into the scene. In 2013, one in twenty international patent applications would come from China. By 2023, they made up almost a third.

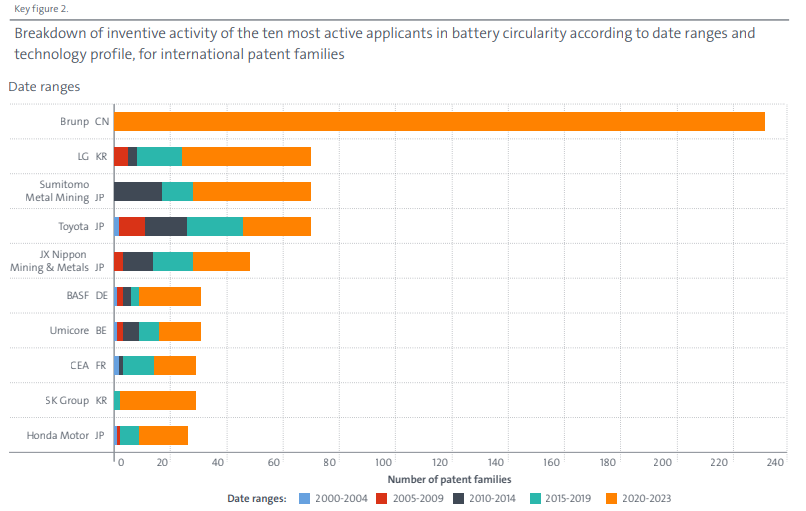

Much of this innovation comes out of China’s formidable battery-making industry. The Chinese company CATL, for instance, is the world’s largest battery manufacturer. Its recycling subsidiary, Brunp, is a giant in its own right; it controls roughly 5% of global recycling capacity — twice the share of its nearest competitor. That has given it the pole position in recycling innovation; the company has filed more international patents in 2020–2023 than Toyota did in two decades.

That’s hardly a surprise. While we’re still in the valley of death, one of the only ways of getting a steady supply of feedstock is to be in proximity to a battery manufacturer. CATL’s factories produce manufacturing scrap, which keeps Brunp’s plants running.

The other major centre of innovation is Europe, which holds about 20% of international patents — which it has maintained for over a decade. Europe’s innovations are very different from those of China, though. Where China’s patents lie in actually processing battery material, Europe has occupied another niche; the dangerous front-end: of handling used batteries before they’re processed.

European inventors hold 34% of the world’s patents in “remote handling”, or running the robots used to deal with damaged batteries. They hold another 30% of the patents for isolating and immobilising those batteries, and another 26% for the pre-treatment that goes in before chemical processing.

This, too, makes sense. Europe doesn’t have the battery mega-factories that can sustain recycling output this early. But it’s well ahead of the world in regulation . A range of laws — the EU Battery Regulation, hazardous waste rules, recycled-content mandates — creates demand for recycling. And so, Europe is obligated by law to take up the capital-intensive, fire-risk-heavy work of getting those batteries out of cars, and into a shape that one can work with. Europe is also willing to fund these companies, keeping them alive through the valley of death.

The rest of the world lags this race. There are a couple of American companies that are likely to be in the global top 10 for recycling capacity by 2030, but it isn’t completely committed to setting up a recycling industry. And India is largely absent.

What the data is really showing

Tracking these patents isn’t a matter of intellectual prowess or R&D chops. It tells us something very specific: about who has the wherewithal to keep innovating before the battery wave hits and recycling becomes a profitable venture.

That simple fact points to many things: where capital sits, where regulations favour a recycling industry, and where the economics allows such a project to be subsidised years in advance. When the battery wave comes, those are the corners of the world that you should expect to take off.

Those that aren’t in this race, meanwhile, will see the future being decided for them.

Tidbits

- Bengaluru-based space-tech startup Pixxel has secured a contract from the US National Reconnaissance Office (NRO) to deliver hyperspectral imaging capabilities — making it one of very few Indian companies to win a contract from a US intelligence agency. Pixxel’s Firefly satellite constellation uses hyperspectral imagery to uncover insights about materials, environmental and soil conditions, and so on.

Source: The Hindu BusinessLine - The Indian government has notified a new Standard Operating Procedure which specifies a 12-week limit for processing foreign direct investment applications that require government approval, in a bid to cut red tape and improve ease of doing business. The timeline is binding on concerned ministries and departments once an application is complete in all respects.

Source: The Hindu - A sharp selloff in UK government bonds pushed the 30-year gilt yield to its highest level since 1998, as investors grew increasingly wary of Britain’s fiscal trajectory amid elevated debt levels, high inflation, and global bond market pressure. The move partially reflects a broader repricing of long-duration sovereign risk that has hit several developed markets this year.

Source: Bloomberg

- This edition of the newsletter was written by Pranav and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Subtext by Zerodha

Subtext by ZerodhaPranay Kotasthane on Navigating the New Uncertain World

If you enjoy The Daily Brief, here’s something we bet you’ll like. We recently spoke to Pranay Kotasthane, one of the sharpest minds we read to understand India and its place in the world. We’ve often featured his insights on this newsletter. This time around, we got him on for a long conversation — one that spans a wide breadth of topics: the world India now has to play in, why the panic around critical minerals is overdone, what’s actually holding back manufacturing, what an India-shaped opening in AI might look like, why Bengaluru feels as stuck as it does, and more. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()