Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened; we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- India’s bullet train: kickstarts and standstills

- India tries to dent the world’s aircraft leasing market

India’s bullet train: kickstarts and standstills

At long last, India shall soon have its own bullet train, running between Mumbai and Ahmedabad.

It took us some time to get here. The Mumbai-Ahmedabad bullet train was supposed to be operational by 2023. We’re now three years past that deadline, and roughly 83% over the original budget.

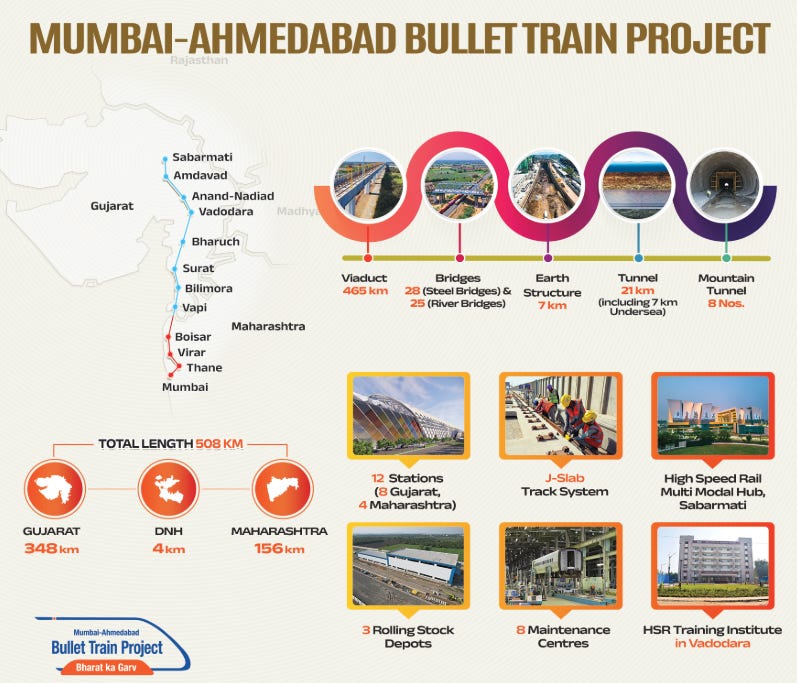

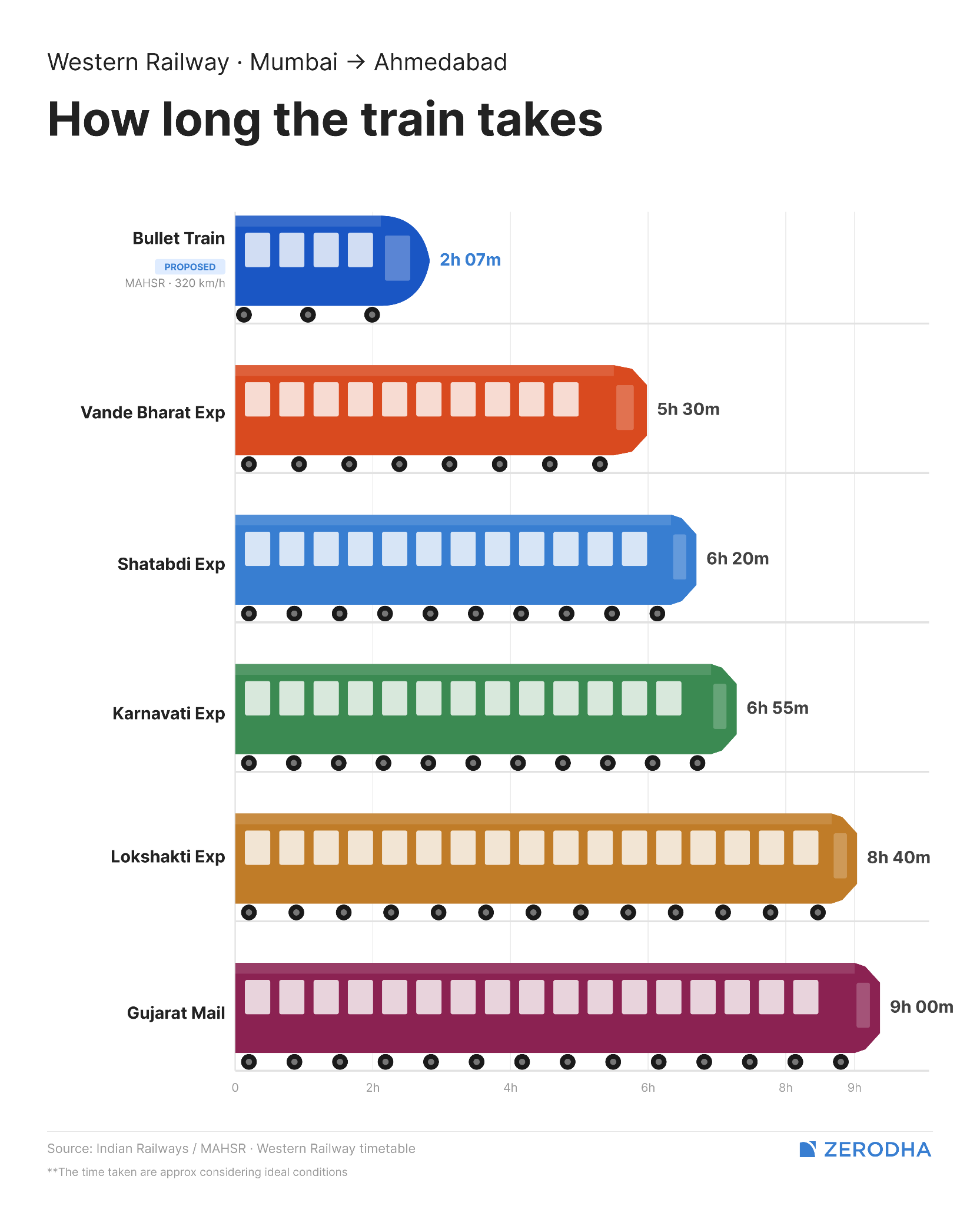

None of that changes the scale of the achievement, though. Chances are, by August 2027 or thereabouts, India could open the first section of the full 508 km corridor. As of now, the fastest train between the two cities takes roughly 6 hours. But the new train, with operational speeds reaching 320 km/hour, could cut the trip down to under two hours, according to the National High Speed Rail Corporation Limited (NHSRCL).

Of course, compared to the totality of the Indian railways, this achievement looks tiny . India runs trains on a network spanning roughly 1.3 lakh route kilometres, carrying crores of people every day. It will be a long time before bullet trains cover anywhere close to a large share of that traffic. But this is a break from the past that signals the way ahead: it is the first time India is building a railway with a completely different rulebook, on a narrower track, with faster signalling, and in a speed class the country has never seen.

What does it take to actually build something like this? That’s the story we’re telling today.

What’s a “bullet train”?

Before putting this piece together, frankly, we couldn’t tell you what a bullet train is: all we knew is that these trains ran fast, and had those sleek, pointy noses.

We aren’t alone in that. The word “bullet train “ comes from Japan. The country debuted its rocket-fast ‘Shinkansen’ system just before the Tokyo Olympics in 1964, connecting Tokyo and Osaka at speeds that rivalled commercial aircraft. These brand new trains came with a streamlined, bullet-shaped nose cone. That gave them their nickname in English.

The more technical (and boring) term is “high-speed rail” — and whether you have one is a matter of the train’s speed, and the systems built around it. The term generally refers to trains that can run at 300 to 350 km/h day in and day out. That’s only possible on tracks specially built specifically for that purpose, with nothing else sharing the line — no freight trains, no slow passenger trains, nothing.

To run at those speeds safely, these entire corridors must be sealed off from the outside world. There can be no level crossings where cars and trucks cross the tracks. These must have continuous fencing so no human, vehicle, or animal, can wander onto the line. And you can’t rely on a driver reading trackside signals. At 320 km/hr, a train covers nearly 90 metres every second — far too fast for a human to spot danger and react in time.

Why don’t we have one already?

The Shinkansen came out of a specific time in Japanese history. After the destruction and humiliation of the second World War, the country was finally finding its footing. The country’s economy was booming, its pride was finally restored, and the country wanted a transport system that matched its growth. A high-speed train fit that ambition.

That wasn’t our reality. In the decades after independence, India was solving a different and more basic problem: how could we move huge numbers of people as cheaply as possible?

That priority never really went away. For most of its history, the Indian Railways have been run like a public service, not a business. To government after government, keeping fares cheap mattered more than making trains fast or convenient. In 2024-25 alone, the government absorbed a passenger subsidy of ₹60,239 crore.

That amounts to an average concession of 43% to every person who travels on the network. If it costs Indian Railways ₹100 to actually ferry you from station to station, you’re only charged about ₹57. Some of that gap is filled by charging freight customers more than it costs to move their goods. The rest comes from the taxpayer.

This arrangement kept fares low. But it also meant there was no spare capital lying around for something as expensive or ambitious as high-speed rail. These priorities reinforced behaviour. The average Indian traveller rarely clamoured for speed, but every rate hike would spark protest. There was little political pressure to change the equation.

But then, things began changing.

India’s economy grew far bigger than it was a decade ago. A growing number of Indians could now afford to pay a premium for speed and comfort. With trains stuck at a low-level equilibrium, wealthy Indians defected wholesale to aviation instead. At the same time, the government began leaning into big, visible infrastructure as a symbol of national capability.

A bullet train was finally possible.

Why did it take so long?

Ambition alone, however, didn’t make the train any easier to build. Before the Mumbai-Ahmedabad corridor came anywhere near completion, it had to navigate years of land disputes, legal battles, and engineering problems nobody in India had solved before.

The single biggest obstacle was land. The project needed almost 1,400 hectares across Maharashtra, Gujarat, and Dadra and Nagar Haveli. It went through thousands of plots, each of which was a negotiation in itself. As the Railway Ministry told the Parliament, delays in Maharashtra’s land acquisition held the project back until 2021. Acquisition could only pick pace through 2022.

Several turned into drawn-out legal fights. These came from two directions. At one end, big companies fought for better compensation. Godrej and Boyce contested the acquisition of about 10 acres of its land in Vikhroli, Mumbai. As the case snaked its way through the Bombay High Court, the compensation demand climbed from an initial ₹572 crore to nearly ₹2,000 crore. On the other side, local communities fought to keep their land. In Maharashtra’s Palghar district, for instance, tribal communities pushed back against losing ancestral agricultural land, with at least five villages passing formal resolutions opposing the project outright.

That delay showed up in the budget. When the project’s foundation stone was laid in September 2017, its costs were estimated at ₹1.08 lakh crore. Officials now expect the final cost to touch twice as much — at ~₹2 lakh crore, driven by land costs and years of inflation.

Where land wasn’t the problem, engineering was.

Here’s one example: at one end, the corridor needed to get around the terrain near Mumbai. This took a 21-kilometre tunnel, including a stretch running under the sea floor near Thane Creek. We had never tried something this ambitious. It took three dedicated tunnel-boring machines, along with equipment and expertise India’s construction industry had never needed before.

How is India paying for this?

We couldn’t have funded all of this on taxpayer money. Luckily, however, we found a willing financier in the original home of the bullet train: Japan . The Japanese government — through its Japan International Cooperation Agency (JICA) — gave us exactly the kind of long, cheap loan a project like this needs.

The terms of that loan are unusually generous. The interest rate is just 0.1 percent, which is to be paid across 50 years. India even gets a 15-year grace period before it has to start repaying the principal. This is about as close to free money as sovereign financing gets. For comparison, a typical infrastructure loan from a multilateral lender runs at several percentage points of interest with a much shorter repayment window.

This generosity, however, was tied to a specific strategic relationship and a specific project. Future corridors will need their own financing arrangements.

Why not upgrade existing tracks?

Why go through all this, however? Why not speed up the trains India already has, instead of building a brand new corridor?

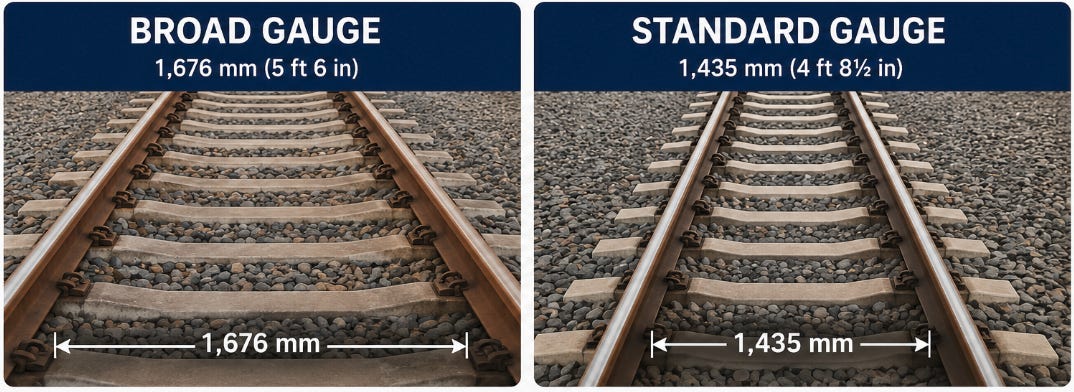

The answer is partly physical. The distance between a train’s parallel tracks — its track gauge — determines what trains can run on it. The Indian Railways runs almost entirely on what’s called Broad Gauge, where the rails sit 1,676 mm apart. Meanwhile, across the world, bullet trains run on the Standard Gauge, at a narrower 1,435 mm.

India began incorporating the wider gauge back in the 1850s — partly because it was believed to be more stable in the cyclone- and flood-prone stretches of the country, and partly because it was thought to be better suited for hauling heavy freight. That made sense 170 years ago. But it also means today’s tracks are physically incompatible with the lighter, narrower trains built for speeds above 300 km/hr.

Gauges aside, the shape of existing tracks have become another dead end. Those old lines were laid to snake around hills, rivers, and towns. They had tight curves everywhere. You can’t curve at bullet-train speeds, however. That would generate forces strong enough to seriously injure passengers or even derail the train outright. Straightening them would mean acquiring fresh land along nearly the entire route anyway, which is functionally the same as building a new line.

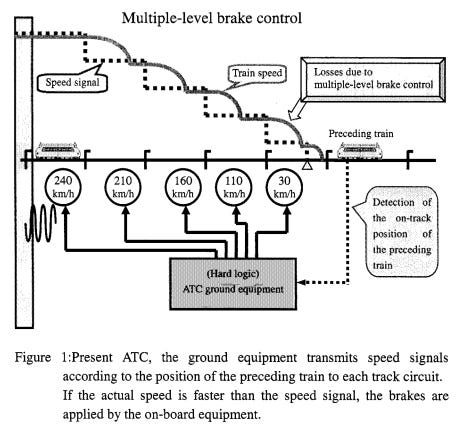

Signalling is another wall. Ideally, radio devices on the track and on the locomotive are supposed to talk to each other — with the human driver taking up the primary job of watching for signals. If the driver fails, missing a signal or running too fast, there’s a back-up system — Kavach, which can step in and brake the train. We’ve explained how it actually works in an earlier Daily Brief piece.

At 320 km/h, this breaks down completely. A driver physically cannot see a trackside signal in time to react to it. Meanwhile, the backup, Kavach, is only certified up to 160 km/h even in its newest version. That’s why the Mumbai-Ahmedabad corridor doesn’t use Kavach at all, and instead uses Japan’s Digital Shinkansen Automatic Train Control system, where the track continuously sends speed and braking instructions straight into the train’s controls. This isn’t a back-up. Trains adjust themselves without waiting on a human decision, removing the driver’s signal-reading job entirely.

And finally, there’s the matter of what surrounds the track. India’s existing network is mostly open and unfenced, allowing dangers of all manners to sneak onto the track. Sealing it off to bullet-train standards would cost close to as much as laying new track altogether.

What comes next?

The Mumbai-Ahmedabad corridor is a proof of concept : a training ground for India to learn how to build tunnels, lay track, create train-signalling engineers, and manage a project of this scale.

Now that this is close to completion, we can build further on this experience.

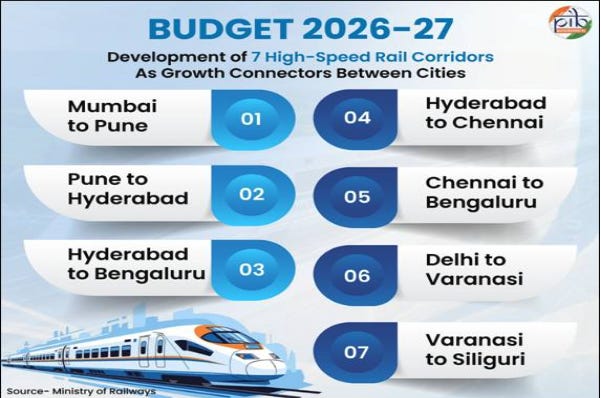

The 2026-27 Union Budget has already announced plans for seven new high-speed corridors — nearly 4,000 kilometres of new track connecting cities well beyond the western coast. This includes genuinely ambitious segments, like a 9.4-kilometre tunnel on the Delhi-Varanasi route, running to an underground station beneath the Jewar airport.

We’re learning from the lessons of this first attempt. To avoid repeating Mumbai-Ahmedabad’s slow, custom-built approach, for instance, the government is pushing for standard designs for bridges, tunnels, and elevated sections across all seven routes, so that each of them doesn’t have to solve the same engineering problems from scratch.

It’s important that we take these lessons to heart, and execute every next corridor a little faster — otherwise, at our current pace, building out the full 4,000-km network could stretch well into the 2050s or 2060s.

But can we? That’ll take serious effort. For one, we need to tighten our land acquisition processes, so that future corridors — like so many other infrastructure projects — don’t run into the same unending disputes. We’ll also need to arrange financing, finding money on terms as cheap as Japan’s.

But if we can make this fall in place, India could have a real high-speed rail network within a few decades. A sluggish welfare service, at long last, will turn into a 21st century mode of transport.

India tries to dent the world’s aircraft leasing market

Sometime in October last year, we looked at the chaotic world of global aircraft leasing, which includes the most envious tax breaks of any industry, iron-clad contracts, and how much geopolitical chess is part of the market functioning.

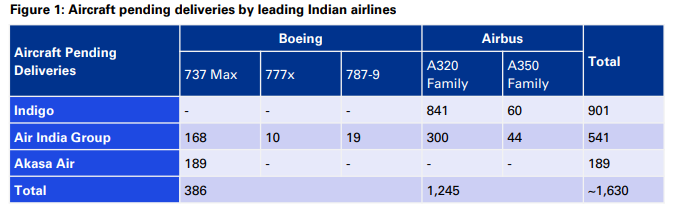

But India, one of the fastest-growing aviation markets on the planet, was missing in that story. Our passenger traffic has more than doubled in a decade to over 170 million by 2024. Indian carriers have one of the largest order books in the world, with over 1600 aircraft pending deliveries as of May 2026.

Source

Yet, roughly 80% of India’s commercial fleet is leased, which is far higher than the global average of about 53%. Almost all of it through entities based in Ireland or Singapore. That’s billions of dollars in lease rentals flowing out of the country every year. As per estimates, Indian airlines were paying roughly $1.6–1.8 billion annually in lease rentals to international lessors before COVID.

India has been trying to change this by building a domestic aircraft leasing market from scratch. But getting there has meant grappling with a set of problems that go far beyond tax incentives.

Paranoid terms & conditions

To begin with, building a leasing market, regardless of the country, is hard because of all the things that give aircraft lessors sleepless nights.

As we covered in our previous story, an aircraft is an asset that depreciates extremely quickly in physical wear, and therefore also in market value. A lessor’s entire business model depends on preserving the residual value of that asset across multiple lease cycles. Every penny saved goes a long way.

That’s why a typical leasing arrangement is also extraordinarily strict in favor of investors.

See, the most common method by which aircraft are leased is called a sale-and-leaseback . Here, an airline buys a plane from Airbus or Boeing at a discounted price, immediately sells it to a leasing company for a profit, and leases it right back. The airline gets the aircraft without the balance sheet burden, while making some quick cash on the side. The lessor gets a long-term, dollar-denominated rental stream with interest, and gets back the aircraft by the end of the lease.

Both sides are happy, until something goes wrong, which, with aircraft, can be often. In that case, to protect the value of their asset, lessors write contracts that are stacked heavily in their favour. Here’s a small list of those:

- As per the “hell-or-high-water” clause, the airline must keep paying rent no matter what — pandemic, engine failure, regulatory grounding, rain or shine.

- The airline is expected to make monthly, non-refundable payments, which are set aside in escrow, to pre-fund major future maintenance. If the airline doesn’t return the plane in the agreed state, the penalties are enormous.

- There are restrictions on flight hours, modifications to interiors, where the aircraft can fly, and which vendors can touch the engine.

This is also why the global leasing industry has clustered in investor-friendly hubs, like Ireland, Singapore, and Dubai. These jurisdictions do offer envious tax breaks and subsidies, but they also offer legal systems that preserve the rights of lessors, deep capital markets to finance the purchase, and an established ecosystem of lawyers, auditors, and asset managers who know the business. It took the respective countries decades to build such hubs.

The India side

The Indian economy, meanwhile, has fundamentally lacked all of this.

The biggest problem was creditor rights. After all, aircraft leasing is an act of trust: a lessor hands over a $100-million-plus asset to an airline in another country, betting that the legal system will let them get it back if the airline defaults. All the major leasing hubs adhere to an international set of rules called the Cape Town Convention, which protects the rights of aircraft creditors.

India ratified the convention in 2008, but never passed domestic legislation to actually implement it. That meant Indian courts had no clear legal framework for enforcing the Convention. Additionally, when our Insolvency and Bankruptcy Code (IBC) kicked in, it imposed a blanket moratorium on all asset recovery, including aircraft . A lessor couldn’t take back their plane while the airline was going through insolvency proceedings, which could drag on for years.

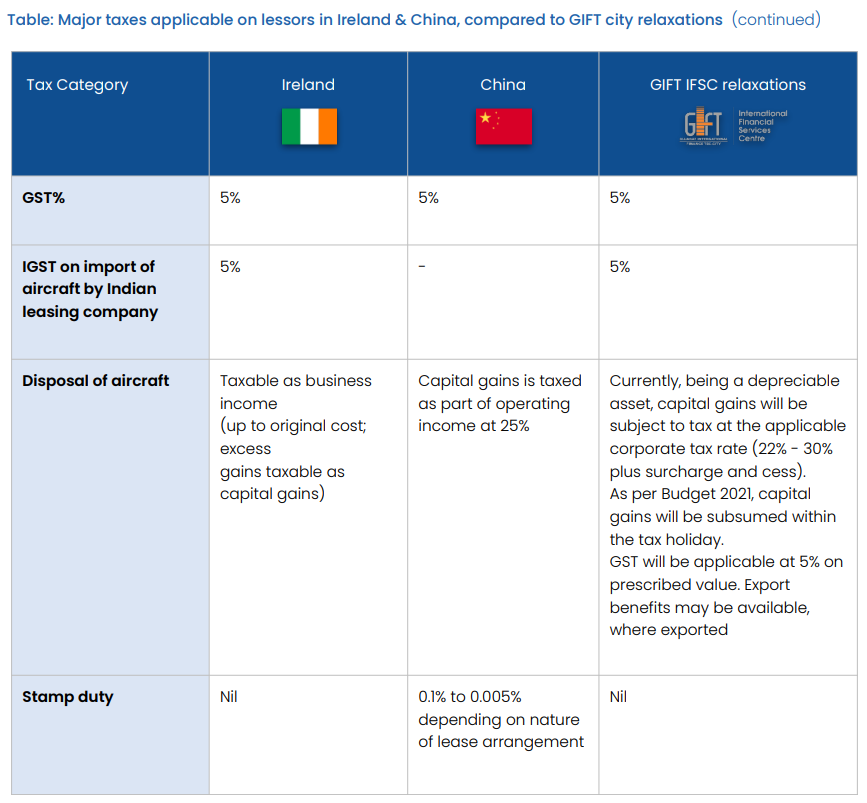

Then, there were the tax inefficiencies. Lease rentals paid to foreign lessors attracted withholding tax in India, which raised the effective cost of leasing. Now India had a double taxation treaty with Ireland which mitigated this, but it also meant every lease had to be structured through Dublin anyway, reinforcing the very dependence the government wanted to break.

On top of this, the indirect tax structure actively penalised anyone who tried to lease onshore. Under the old GST rules, if an Indian leasing company imported an aircraft, it paid a 5% Import IGST, but couldn’t offset that against the output GST it charged on lease rentals. The rules of input tax credit didn’t apply to aircraft back then. But an airline importing the same plane under an offshore lease from Ireland was exempt from import IGST entirely.

A third constraint was more physical, and in hindsight, rather absurd. Any product that was imported by a unit located in a Special Economic Zone had to be physically brought into the SEZ to qualify for tax exemptions. But that makes no sense for aircraft , which flies between regions, and can’t be located anywhere else other than an airport.

And finally, India simply didn’t have the financial depth. Aircraft leasing is a capital-intensive business. Global lessors raise billions through bond markets, asset-backed securities, and bank syndications. India’s capital markets, while growing, didn’t have the depth or sophistication to support aircraft-backed financing at scale. Indian banks were reluctant to enter a segment they found extremely risky.

Two landmark cases

These weren’t hypothetical risks. Two spectacular airline collapses turned them into lived experience for the global leasing community.

The first was that of Kingfisher Airlines in 2012. The airline’s founder Vijay Mallya had built a flashy, full-service carrier that haemorrhaged cash. When Kingfisher stopped flying, foreign lessors moved to recover their aircraft immediately, but Indian law turned days into months.

The DGCA refused to deregister the aircraft, citing outstanding government dues — airport parking charges, navigation fees, ground handling costs that Kingfisher owed to government entities. Kingfisher itself objected to deregistration, claiming it had accumulated ownership rights through lease payments. Lessors had to fight through Indian courts, meet with the Ministry of Civil Aviation, and negotiate payoffs to government creditors; all the while, their aircraft sat idle on Indian tarmac, losing value by the day.

Only one lessor, DVB, only managed to repossess a plane, that too only because it happened to be outside India at the time.

Then came Jet Airways in 2019.

At its peak, Jet was India’s largest private carrier, and was brought down by crushing debt to file for bankruptcy. Lessors filed claims worth over ₹14,400 crore, but only ₹2,290 crore was admitted, and even that went unpaid . The IBC moratorium kicked in, freezing the aircraft in place. The insolvency dragged on for over five years before the Supreme Court finally ordered liquidation. Lessors couldn’t get their planes back, couldn’t lease them to someone else, and watched the aircraft depreciate while the legal process ground on.

After each of these episodes, and that of Go First later in 2023, the global leasing industry recalculated the India risk premium as leasing rates for Indian airlines crept higher: 8-10% above what airlines in Cape Town-compliant countries paid.

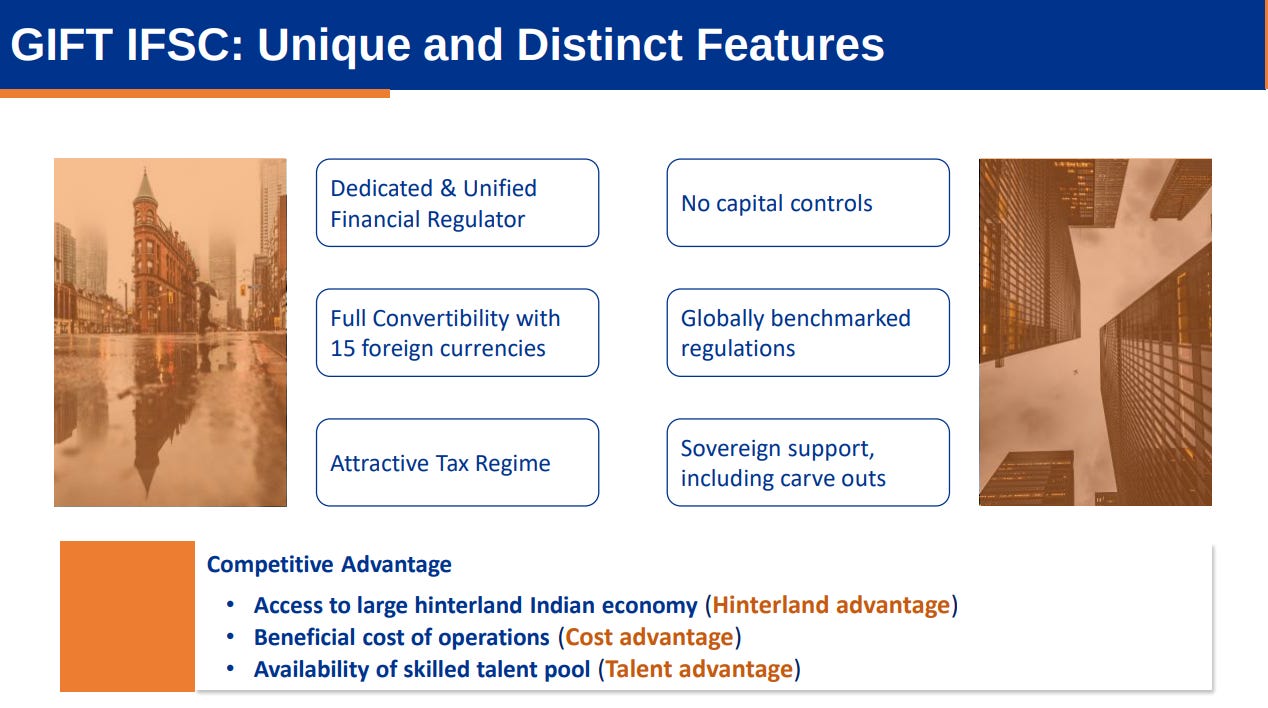

Gift for the market

India’s first strong answer to all of this was Project Rupee Raftaar , a working group set up by the Ministry of Civil Aviation in 2018. They published their landmark report in 2019, which laid out the case simply: India was one of the world’s biggest consumers of leased aircraft, but all the economic value of those leases was being captured elsewhere.

The solution it pitched was to build a competing ecosystem inside India, anchored at what is now known as GIFT City.

What followed the report was a rapid sequence of reforms, of which we’ll cover just a few.

The foundation

In April 2020, India established the IFSCA, or the International Financial Services Centres Authority, as a unified regulator for GIFT City, replacing the patchwork of approvals that had previously been required from four separate regulators (including SEBI and RBI). In October 2020, the government designated “aircraft lease “ as a financial product under the IFSCA Act.

By February 2021, the leasing framework was in place. Lessors could register at GIFT City with a minimum capital of just $200,000 for operating leases, transact in foreign currency, and access a suite of tax incentives: like no withholding tax on lease rentals to non-residents, no customs duty, no stamp duty, and a tax holiday on profits.

In fact, the tax holiday itself was initially 10 years out of the first 15 years of operations. That was a concern for an industry where aircraft leases ran for around a decade while the lifespan of an airplane is around 20-25 years. So, the 2026 Union Budget doubled it to 20 years out of 25, with a concessional 15% rate thereafter.

Along with repairing the issues of input tax credit and SEZ placement that plagued imported goods earlier, GIFT City came closer to tax parity with Ireland and Singapore.

Arguably the biggest reforms came on the legal side. In April 2025, Parliament passed the Protection of Interests in Aircraft Objects Act, finally giving domestic legal force to the Cape Town Convention. Under the new law, lessors can repossess and deregister aircraft within two months of a default. The Act explicitly overrides conflicting domestic laws, and aircraft transactions are also exempt from the IBC moratorium.

Winning deals

These changes didn’t take long to make real impact in terms of deals, either.

In September 2023, Air India acquired India’s first Airbus A350 widebody through a finance lease structured via its GIFT City subsidiary. That was a proof of concept that the onshore framework could handle complex, high-value transactions. By October 2025, Air India’s GIFT City leasing arm had secured a $215 million structured loan from Standard Chartered and Bank of India to finance six Boeing 777-300ERs. This was the first large-scale commercial bank financing with a GIFT City borrower.

And in March 2026, IndiGo completed the first-ever onshore Japanese Operating Lease with Call Option (JOLCO) for two Airbus A320s — a sophisticated financing structure that had previously only been possible through offshore hubs.

By December 2025, GIFT City had 38 registered lessors and had facilitated about 370 leased aviation assets valued at roughly $5.8 billion. Air India, IndiGo, and Akasa Air have all set up leasing arms inside the hub, and between them plan to lease over 200 additional aircraft through GIFT City over the next few years.

The tests

However, scepticism around India’s aircraft leasing ecosystem still persists, and for good reason.

Most of the leasing activity through GIFT City so far has been driven by Indian airlines themselves setting up captive leasing subsidiaries. The large international lessors who dominate global aviation finance (like AerCap and SMBC Aviation) still route the bulk of their business through Dublin. They have deep relationships there that are incredibly hard to replace even with fancier subsidies.

Indian banks are beginning to finance aviation transactions from GIFT City, but the depth of capital markets remains thin compared to Dublin or Singapore. Several registered leasing entities at GIFT City have struggled to arrange funding and haven’t yet become operational.

And lastly, as we’ve covered in our GIFT City primer, there are situations where the IFSCA, which was always intended to operate independently, often gets overridden by SEBI, RBI, and other agencies that oversee the rest of India.

If tax breaks and generic benchmarks of investor-friendliness built an aircraft leasing hub, this would just be a race to the bottom. But those are just the foundation that brings investors in. They’re simply enablers of the factor most crucial to success: trust. And that requires decades of practice and maybe even a few situations where those foundations get stress-tested.

- This edition of the newsletter was written by Vignesh and Manie

Tidbits

- Adani Defence Breaks Ground on ₹2,500 Crore Missile Plant in MP

Adani Defence and Aerospace laid the foundation for a missile and propellant manufacturing facility in Shivpuri, Madhya Pradesh, at a cost of ₹2,500 crore, expected to generate over 4,000 jobs.

Source: The Hindu - India’s Critical Mineral Auctions Keep Failing

The government cancelled 9 of 19 blocks in its seventh critical mineral auction round — 2 received zero bids, 7 had fewer than three qualified bidders — continuing a pattern across all previous rounds.

Source: ET - India and Japan Agree to Jointly Develop Defence Equipment

Japanese PM Sanae Takaichi’s New Delhi visit produced a joint defence co-development commitment, backed by Japan’s new parliamentary rules permitting lethal weapons exports to 17 countries, including India.

Source: BS

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Points & Figures by Zerodha

We’re always chasing the day’s biggest stories. But every now and then, we come across a dataset that deserves a closer look than a Daily Brief allows.

That’s what Points & Figures is for.

It’s where we step back from the news cycle and use data visualisations to tell stories about the Indian economy, financial markets, and investing. Stories that are difficult to tell in a ten-minute podcast or a daily newsletter.

Our latest edition traces how India’s digital economy got here, through the data buried in Jio’s IPO filings.

Join us on WhatsApp, where we share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops so that you can read or watch it right away.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()