Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened; we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- India’s data centres look to the salty seas

- The ₹10 battery with a ₹50 crore problem

India’s data centres look to the salty seas

Recently, The Hindu BusinessLine ran an interesting story that caught our eye. India’s data center operators are looking to find new, innovative ways to cool their extremely thirsty buildings. Reliance, in fact, is looking to use seawater to do so for its AI data centre in Jamnagar.

It’s well-known that data centers consume a significant amount of water in order to cool servers. A large hyperscale AI facility can guzzle millions of litres a day. For instance, Google’s own reporting says that in 2024, its data centers consumed 31 billion litres of water, which is enough to irrigate 54 golf courses, or even supply to a small town.

India, too, is now in the middle of the most aggressive data center buildout in its history. Installed capacity has tripled from about 0.5 GW in 2020 to roughly 1.500 GW by 2025, and could cross 6 GW by 2030.

Now, India doesn’t necessarily face a permanent freshwater shortage, but this year’s monsoon is a reminder of how fragile the supply can be. The IMD has forecast below-normal rainfall under El Niño conditions, and groundwater tables in cities like Mumbai and Chennai have been dropping steadily. Maintaining the freshwater reserves that farms, cities, and industries depend on is hard enough without adding massive data centers to the queue.

The ocean, on the other hand, offers a practically infinite resource. But, even without data centres in the picture, turning seawater into something a data center can actually use is harder than it sounds. Few countries have managed to make it an industrial-scale process, and we were curious to know why that is.

A corrosive material

Let’s start with how data center cooling works.

Thousands of servers packed into a single facility generate enormous heat. Left uncooled, chips could fail within hours, even minutes. The most common solution is evaporative cooling. Here, cold water is pumped through pipes near the servers, absorbs the heat, and is pushed through cooling towers where it evaporates. The evaporation carries the heat away, but consumes the water in the process.

Now, assume this process uses seawater.

As the water evaporates, any dissolved minerals or salts left behind get progressively concentrated in the remaining water. Over time, those minerals form hard, chalky crusts on pipes and heat exchangers, clogging the system. Bacteria and algae thrive in warm, mineral-rich water, forming slimy biofilms that further choke the equipment.

In essence, seawater would wreck a conventional cooling system almost immediately. The salt would corrode metal components, the minerals would scale up the pipes, and marine microorganisms would foul the surfaces.

So data centers need water that’s clean enough to cycle through the system without leaving destructive residues. That means freshwater from rivers, reservoirs, municipal supply, or groundwater. Which is precisely the resource India can’t afford to divert in large quantities during poor monsoons.

The alternative is to take the infinite supply sitting offshore and strip the salt out of it.

Methods of desalination

Now, there are three main industrial techniques for seawater desalination, each with its own logic.

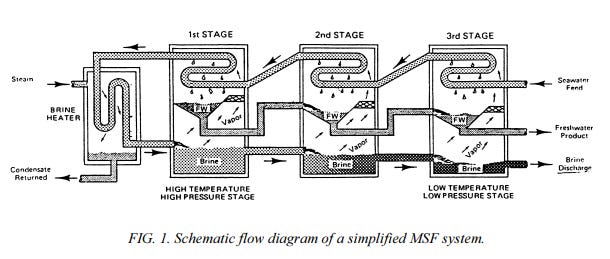

The oldest approach is Multi-Stage Flash distillation, or MSF. Think of MSF as a sequence of sealed chambers, each held at a progressively lower pressure. Now, seawater is heated and then fed into the first chamber. When it enters a lower-pressure environment, a fraction of it “flashes” into steam. That steam condenses on cold pipes and drips down as pure freshwater, which then flows into a separate channel.

Source

MSF is reliable and proven, but brutally energy-intensive: it takes close to 120 kilowatt-hours of heat to produce 1000 litres of freshwater, plus additional electricity for pumping. It also produces the most expensive water of the three methods.

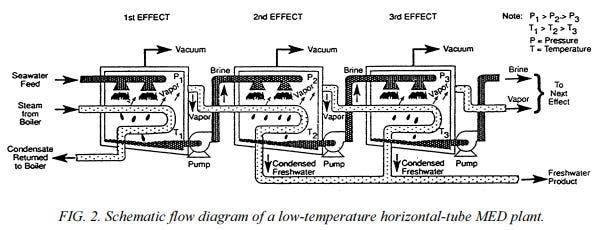

The second method is Multi-Effect Distillation (MED). It is a more efficient version of the same principle.

Instead of “flashing ”, it uses a staircase of evaporation effects . Steam produced in one stage heats a thin film of seawater in the next, which boils and produces more steam, and so on down the chain. Because MED transfers heat more efficiently through these thin films, it uses much less energy than MSF. Both MSF and MED produce extremely pure water, which is valuable for specialised industrial applications. But, while less expensive than MSF, MED still comes at a steep cost.

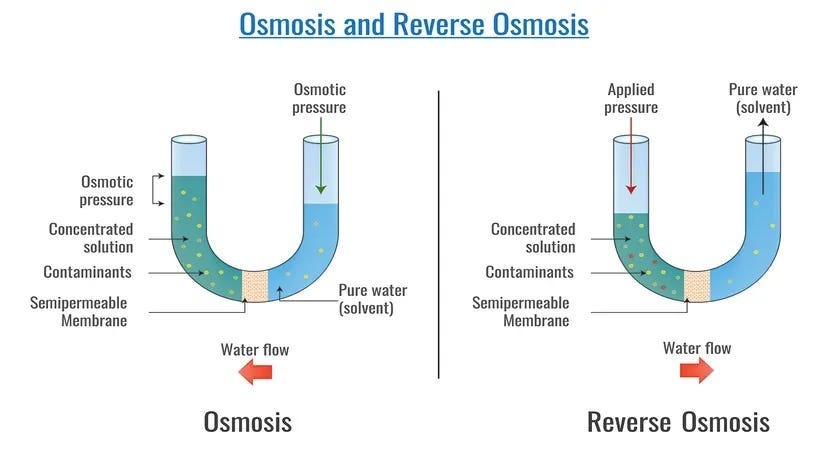

The third method, which also dominates modern large-scale desalination, is Reverse Osmosis (RO), the same technology used in your home water purifier.

Here, seawater is forced through semi-permeable membranes at extremely high pressure. The membranes have pores small enough to let water molecules through, but block the larger salt particles. Unlike MED and MSF, RO requires no boiling.

The trade-off here, though, is that while RO filters salt out, other impurities may require separate attention. The membranes demand rigorous pre-treatment of the incoming seawater — like chlorine to kill bacteria, coagulants to remove suspended particles, acids to prevent mineral crusts, and then de-chlorination before the water hits the membrane since chlorine damages the membrane material itself.

But RO’s ace, which also enables its large-scale application, is its energy bill. Because it doesn’t boil anything, it only needs about 4-5 kWh of electricity per cubic metre, just for the high-pressure pumps that force water through the membrane. That’s an order of magnitude less energy than MSF. Additionally, over the years, the RO process itself has become more efficient with time, making the unit economics of an industrialized process better.

Saltwater economics

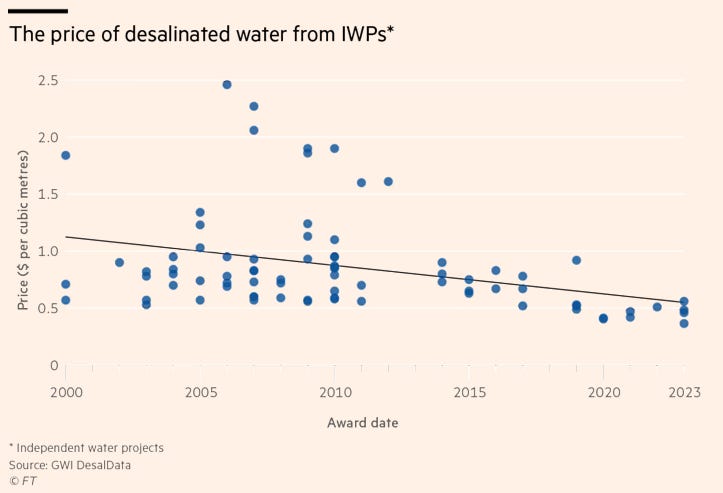

Even with RO’s efficiency gains, desalination remains significantly more expensive than drawing water from a river or an aquifer. Producing one cubic metre (or 1000 litres) of desalinated seawater typically costs between $0.50-$1.50, depending on energy prices, plant scale, and local conditions. Natural freshwater, where available, can cost as little as $0.10 per cubic metre.

The expense breaks down into two buckets. Upfront capital is large: building a factory-scale RO plant — with intake pipes, pre-treatment systems, membrane arrays, energy recovery devices, and brine outfall infrastructure — costs $1,000-2,500 per 1000 litres of daily capacity. A plant producing 1 lakh cubic metres a day might require $100 million to $250 million just to build. Then there’s operating cost, dominated by electricity, which accounts for 35-45% of ongoing expenses.

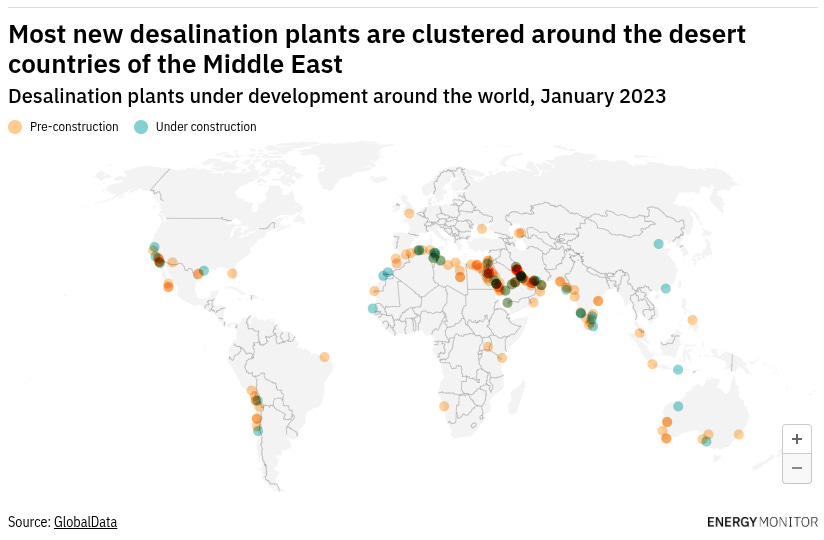

In the world, the countries that have pushed the desalination frontier the most are also the nations that were desperately starved of freshwater: the UAE, Israel, Saudi Arabia, and other countries in West Asia.

Israel, a country where 70% of the landmass is desert, now gets most of its drinking water from desalination. Israel has five large RO plants along the Mediterranean coast, which together produce about 600 million cubic metres a year, and supply 80% of Israel’s urban household water needs. In fact, Israel has such a huge surplus of desalinated water that, for the first time anywhere, it is now trying to refill a freshwater lake with the same.

Saudi Arabia operates on an even larger scale. Their al-Jubail desalination plant is one of the largest in the world, converting over 1.4 million cubic metres of water a day. It’s also not entirely a coincidence that it also has the world’s largest oil capacity. Oil refineries already possess ports, power generation, pipelines and industrial utilities that can also support desalination.

The Indian experience

India’s experience with desalination is real, if less celebrated. Most of our capacity is concentrated in one state: Tamil Nadu.

Our first desalination plant was built at Minjur, Tamil Nadu, and could deliver 100 million litres a day (MLD). After a near-catastrophic water crisis in 2019, Tamil Nadu has doubled down on desalination capacity. The town of Nemelli has two plants which can collectively deliver 250 MLD.

A fourth plant at Perur will add another 400 million litres per day by early 2027. Once operational, it will be one of Asia’s largest seawater RO plants, and desalinated water will supply roughly half of Chennai’s drinking water.

Meanwhile, in Kalpakkam in Tamil Nadu, the Bhabha Atomic Research Centre has been running a hybrid nuclear desalination plant since the early 2000s, coupling both MSF and RO processes to the Madras Atomic Power Station to produce 6.3 million litres a day. BARC has also deployed smaller solar-powered RO units in remote villages and emergency barge-mounted plants for disaster relief after the 2004 tsunami.

Reliance has been in the desalination game for longer. They’ve been operating captive MED and RO plants at its Jamnagar refinery complex since the 2000s, built with Israel’s IDE Technologies and VA Tech Wabag. The oil refinery needed ultra-pure water for processing; now the same infrastructure extends to the data center campus next door.

Does solar change the equation?

Here’s where the story gets interesting for India specifically. The single biggest cost in running a desalination plant is electricity. Those costs used to be elevated with coal power. But two of India’s largest data center builders — Reliance and Adani — happen to also be the country’s two biggest renewable energy developers.

Reliance is building a massive integrated renewable energy ecosystem in Gujarat: solar PV manufacturing in Jamnagar, battery storage systems, and multi-gigawatt solar farms in Kutch that the company says will be among the world’s lowest-cost sources of round-the-clock green electricity. Using your own solar power at rock-bottom cost to desalinate seawater for your own data center improves the economics significantly compared to a municipal utility buying electricity at grid rates to run a desalination plant for a city.

Adani has a similar structural advantage. AdaniConneX, the group’s data center joint venture, is explicitly building renewable-powered facilities. Adani’s position in power generation, solar manufacturing, and transmission gives it the same kind of vertically-integrated cost structure. Both companies can, in principle, co-locate data centers, solar farms, and desalination plants on the coast, turning sunlight into compute with seawater as the coolant.

A recent study of a large RO plant in the Mediterranean backs the economics up. Powering a desalination facility with a hybrid mix of solar, wind, and grid electricity cut the cost of water production by about 20% compared to relying purely on the grid. The renewable setup also acted as a hedge against fossil fuel price volatility. On top of the cost savings, the hybrid plant cut its carbon footprint by about 35%.

Conclusion

Desalination won’t solve India’s water problems. It’s expensive, it only works for coastal regions, and dumping the brine by-product out of desalination back into the ocean damages marine ecosystems if it isn’t managed carefully.

But for data centers, which need massive amounts of water in predictable, uninterrupted supply, and which are increasingly being sited on India’s coastline anyway, it offers independence from the freshwater grid at a time when that grid is under growing pressure.

Even then, however, when it comes to the data center buildout, a desalination strategy only makes sense only in a few places. Mumbai and Chennai, two of India’s biggest cities, and also next to the sea, will benefit from this. Jamnagar is also a coastal town. For inland areas like Hyderabad and Bengaluru, though, the water problem may have to be solved differently.

What also remains to be answered is whether Reliance’s vertically-integrated model at Jamnagar becomes the template for India’s data center buildout, or remains an exception that only large conglomerates can afford.

The ₹10 battery with a ₹50 crore problem

Panasonic has been making batteries in India since 1972, filling our TV remotes and wall clocks with AA and AAA cells. But last week, it said it might have to stop.

Not because demand collapsed or there was immense competition, but because of a recycling rule. It told Business Standard that its only Indian battery plant, in Pithampur, Madhya Pradesh, may become unviable under the country’s Battery Waste Management Rules.

By all means, this is no small operation. The plant employs 283 people, makes 54 crore batteries a year, and holds about a fifth of India’s ₹4,000 crore dry-cell market share. Last year it earned a net profit of ₹3.49 crore. But the compliance bill it’s now staring at could be around 8 times that.

Panasonic’s own auditor has also flagged the issue, qualifying the FY26 numbers because the company hasn’t set aside any money for what the rules will eventually cost. When the auditor gets nervous and issues a qualified opinion, something is real. But what’s the big deal about these rules?

What the rules actually ask for

We’ve covered before about how India’s e-waste rules went from an idea to a real, enforced market. Batteries followed a similar script, too, anchored by a concept called extended producer responsibility, or EPR.

In simple terms, what EPR meant was that if you made money selling something, you’re also on the hook for what happens to it when it dies. Under the Battery Waste Management Rules of 2022, every producer has to make sure a slice of what it once sold gets collected and recycled. For dry cells this year, that slice is 50% by weight of what it sold three years ago. Next year, it will climb to 60%, and the year after, 70%. So, if you sold 100 kgs of dry cells in FY23, you are responsible for 50 kgs of them to be recycled by the end of this year.

How does a producer actually pull this off? There are two ways. You can either do it yourself by building the collection network, gathering the dead batteries, and getting them to a recycler. Or you can let someone else do all of that and pay them for it.

The second route runs on something called an EPR certificate. Think of it like a carbon credit. A registered recycler does the actual recycling, the government’s portal issues a certificate for the quantity processed, and the producer buys that certificate to prove it hit its target. The recycler gets a fair sum, the producer takes responsibility for their waste, and the government manages to get the circular economy of batteries up and running.

What a producer can’t do is nothing. Miss the target and you pay a penalty called environmental compensation . What’s more, paying the penalty doesn’t erase the obligation because the shortfall will simply roll over to the next year.

This is the very system pulling India’s lead-acid and lithium batteries into the formal economy. It sounds simple enough, but the trouble starts the moment you ask what kind of battery is subject to this rule.

A rulebook written for lithium

When we say “battery “, we’re using one word for three completely different businesses.

A lead-acid car battery, for instance, is heavy, expensive, and full of lead worth real money. When it dies, a mechanic or scrap dealer is happy to take it, because there’s cash inside. Amara Raja, one of India’s biggest lead-acid makers, spent ₹700 crore building its own recycling plant precisely because recovered lead is cheaper than buying it fresh. For lead-acid, recycling is much less a burden than it is a raw-material procurement strategy.

But a lithium battery — the kind in your phone or an EV — is newer and harder to recycle, but it’s packed with critical minerals like lithium, cobalt, and nickel. India imports almost all of those, much of it from China, so the government badly wants them recovered at home. There’s a whole apparatus pushing this along, including a ₹1,500 crore incentive scheme for recyclers, customs duty waived on battery scrap, and the National Critical Minerals Mission treating recycling as a strategic priority.

And then there’s the humble dry cell with zinc and manganese, worth pennies.

The problem lies in the fact that the EPR rules treat all three the same way.

Go back to those two routes. To actually comply, a producer buys certificates — and the government has fixed what those cost, metal by metal. The price varies sharply by chemistry: it’s ₹18 a kilo for lead, and a whopping ₹2,400 for lithium. Fair enough on paper, because trickier, costlier chemistries should cost more to handle. And for lithium, a high number does real work — it pulls more players into recycling, because the recovered metal is genuinely valuable and the government is pouring money in behind it. The price is a magnet, and it’s meant to be one.

But zinc, the main metal in a dry cell, with a much simpler chemistry, sits right at the top of that ladder, at lithium’s level, at ₹2,400 per kg. Such high prices should

Now, you’d expect a price that steep to fix its own problem. ₹2,400 a kilo should pull recyclers toward zinc exactly the way it pulls them toward lithium — that’s the whole reason it was set there. It should summon a zinc recycling industry into being.

It hasn’t. And the reason has nothing to do with the price.

The batteries nobody wants to collect

Before any of this matters, you have to physically get the batteries back. And dry cells are almost engineered to vanish.

See, a dead car battery goes back through a dealer. Even a dead phone has resale and scrap value. But a dead AA battery, which is much smaller than a car battery or a phone battery, usually ends up in the kitchen bin with the vegetable peels, and inevitably to a landfill. No dealer, no deposit, no reason for anyone to fish it out. Even India’s enormous network of kabadiwalas, who are so good at grabbing value out of waste that they outbid the formal recyclers, won’t touch a dry cell, just because there’s nothing in it for them.

India sells somewhere between 2.2 and 3 billion dry cells a year. Even the companies running pilot collection drives are recovering only about 20% of them. But the rules ask for 50%, starting now.

The industry keeps pointing at the countries that did this properly. Switzerland and Belgium reached 70% collection. But that took 10-15 years of patiently building the bins, the habits, and the logistics. India set a 50% target in year one, with none of that in place. As the head of Nippo put it, these systems are usually phased in over six or seven years, not switched on overnight.

The math that doesn’t work

So here’s the trap closing. To earn a certificate, a recycler first has to collect — and collecting a billion twenty-gram batteries out of a billion kitchen drawers, with no return channel and no scrap value to fund the effort, costs far more than the ₹2,400 a kilo at the end can ever cover. So the recyclers don’t come, the certificates that are supposed to exist never get created, and the few that do get bid up toward that ceiling.

Its problem was never really recycling. It’s been handed the cost of a collection system that nobody has built.

Virgin zinc costs around ₹300 a kilo. The regulated unit cost of zinc recycling, Panasonic says, runs about 240% higher than that. So you’re paying a steep premium to recover a metal you could simply buy cheap. The recycling loses money before you’ve even counted the cost of collecting anything.

For Panasonic specifically, if it had to meet the full 50% target by buying certificates, it estimates the cost could reach around ₹50 crore. Against a ₹3.49 crore profit, that wipes out the business several times over. And the penalty rises 10% every year, so the squeeze tightens on its own.

It would be easy to read all this as one foreign company complaining, but it isn’t. Eveready, Nippo and Duracell, all well-known household names, all have raised the same alarm.

They’re not asking to scrap the rules. Instead, they want three fixes: lower the first-year target, phase it in over years instead of demanding 50% on day one, and reprice the compliance cost for zinc to reflect what a dry cell is actually worth. Now, that’s not what lithium is worth, but that wouldn’t attract enough recyclers, so that’s another problem.

Some are floating ideas to kick-start collection, like handing out free batteries in exchange for used ones, or pooling a single collection network across the whole industry.

Is this only a dry-cell problem?

The dry cell is the worst case. But the flaw underneath it runs through the whole framework. The flaw of the rule that assumes a recycling market already exists, which clearly doesn’t. Especially EVs.

From 2027-28, makers of lithium batteries will have to use a minimum share of domestically recycled lithium, cobalt and nickel in their new cells. Sounds great. Except India today formally recycles less than 3% of its lithium-ion batteries. And most of the EV batteries sold so far are still sitting in cars on the road and they won’t die for years yet. So the rule will demand recycled content that, physically, barely exists. Same shape as the dry-cell problem: the mandate shows up before the material does.

The difference is that with lithium, everyone actually wants to solve it. The metals are valuable, India needs them for its own security, and the state is pouring money in to build the recycling industry ahead of the mandate. Lithium can grow into the rule. But dry cells get the rule without the help.

What the fight is really about

When you strip away the noise, you can see that both sides actually agree on the principle. Batteries shouldn’t end up in landfills. Producers, not taxpayers, should pay for the cleanup. EPR is a good idea, and India’s version of it does seem to work for the batteries worth working on.

The disagreement is narrower than it looks. Whether you can demand a mature recycling market before you’ve actually built one, and whether a rule priced for lithium should land, unchanged, on a metal worth a fraction as much.

How the government answers that will decide a lot more than Panasonic’s fate. Because if a rule designed to build a circular economy ends up closing the factories at its low-value edge, the Panasonic plant won’t be the only loss for India. We’ll also be left with the same two-and-a-half billion dead batteries a year without those who we need to come and collect them.

Tidbits

- E-scooters may soon get BEE energy efficiency star ratings

The Bureau of Energy Efficiency (BEE) has proposed a voluntary one-to-five star rating system for electric two-wheelers, similar to ratings for appliances. The labels will help buyers compare energy efficiency while encouraging manufacturers to build more efficient e-scooters.

Source: Business Standard

- Adani Group to enter nuclear power, targets 10 GW by 2035

Adani Group plans to enter the nuclear power business through Adani Atomic Energy, targeting 10 GW of capacity by 2035. The company also announced a ₹2 lakh crore power expansion plan, higher data centre capacity, and new investments in hydropower and digital infrastructure.

Source: The Economic Times

- Indian drugmakers gear up for Keytruda biosimilar opportunity

Biocon, Zydus, Dr Reddy’s and other Indian drugmakers are preparing to launch biosimilar versions of Merck’s cancer drug Keytruda as its patents begin expiring from 2028. Lower-cost alternatives could cut treatment prices by 50-80%, making the therapy accessible to many more cancer patients.

Source: Business Standard

- This edition of the newsletter was written by Manie & Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Subtext by Zerodha

Subtext by ZerodhaBrad Setser on the dollar and the world’s trade imbalance

The role of the dollar, and its influence on global trade, is a complicated story that has constantly changed over time. To make sense of all this, we spoke to Brad Setser, Most of Twitter knows Brad is one of the sharpest voices on all things balance-of-payments. He is a senior fellow at the Council on Foreign Relations. He also served at the US Treasury and the National Economic Council.

We recorded this conversation while the Iran war was unfolding and oil markets were watching the Strait of Hormuz, and not long after Trump and Xi had met in Beijing to negotiate a trade deal. We used the moment to ask him about the things he thinks about most: why the dollar is really strong, what an AI bust would do to it, how the manufacturing surpluses of China, Korea, and Taiwan quietly finance the American deficit, and what China would have to do to rebalance.

Watch the full podcast episode below, where Brad breaks down the sources of dollar demand and the future of global trade imbalances

You can also listen to the full conversation on Spotify and Apple Podcasts. The full transcript of the podcast is below if you prefer to read.

We’re always chasing the day’s biggest stories. But every now and then, we come across a dataset that deserves a closer look than a Daily Brief allows.

That’s what Points & Figures is for.

It’s where we step back from the news cycle and use data visualisations to tell stories about the Indian economy, financial markets, and investing. Stories that are difficult to tell in a ten-minute podcast or a daily newsletter.

Our latest edition traces how large language model usage changed over the past eighteen months, through the public usage data of one busy AI marketplace.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()