Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- India and UK, partners in trade

- Tata Motors’ amicable breakup

India and UK, partners in trade

The United Kingdom and India are just closing off a trade deal that has been many years in the making. This is a deal we’ve been trying to land since the COVID years, back when Prime Minister Modi and Boris Johnson, then the Prime Minister of the UK, announced that the two countries were launching an “enhanced trade partnership”.

After fourteen rounds of negotiations, under three different British Prime Ministers from two different parties, it finally seems like a deal is in the bag. We’re still not at the finish line — the legal text of the agreement hasn’t yet been finalised, and only once that is done can we actually sign the agreement. But at the very least, both countries are now on the same page. If nothing else wrecks our progress, now, the deal could kick into action within the next year (probably before we get GTA 6).

There’s a lot to celebrate about this deal, from tariff cuts to easier visas. But there’s something deeper to this moment as well. Over the last decade, both countries have tried to reset their approach to global trade. And now, during a moment of global economic uncertainty, they’re taking a bet on each other.

Here’s everything we’ve learnt about the trade deal, so far.

A longer term strategic shift

To both India and the United Kingdom, this agreement is part of a longer term shift in trade strategy.

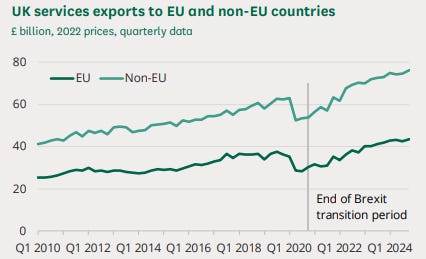

Consider the United Kingdom. For decades, the UK sold itself as Europe’s front‑office. It was a one-stop shop for high-skilled services — everything from legal support, to finance, to accounting — that catered to clients across Europe through so-called “passporting” rights. With 80% of its economy revolving around services, the United Kingdom was uniquely well-suited for such an economic model.

But then came Brexit, which snapped that cozy arrangement. As soon as the UK withdrew from the European market, passporting disappeared. While British banks and law firms quickly adjusted to this new reality, duplicating their licenses and establishing a presence in the EU, the country’s long-standing comparative advantage had waned. It could no longer bank on a huge and prosperous market by its doorstep.

Its much smaller goods market, meanwhile, has never recovered from Brexit.

This is why, over the last few years, the United Kingdom has been hunting for new, fast-growing markets as an alternative to its European business. The Indo-Pacific region is where it has concentrated the most. It recently signed new trade deals with countries like Australia and Japan, and has aggressively been courting new markets in the ASEAN region.

This new FTA is a part of that broader push.

India, meanwhile, has spent the last few years emerging from an era of inward-looking trade policy. Our many bilateral trade and investment deals, to the government, looked like they put us on the backfoot. Most of our trade agreements were heavily focused on goods — which meant that while we gave others an ever-larger market to export to, we did little to promote our own comparative advantages, in industries like pharmaceuticals and services. Meanwhile, after a series of high-profile arbitration losses, we lost faith in international investment agreements.

From 2016 onwards, we cancelled 75 of our 83 bilateral investment treaties, pushing others to sign agreements that were much smaller in scope. At the same time, on the trade front, we pulled out from free trade negotiations like those for the RCEP.

Instead, we attempted a more calibrated strategy. We focused our energy on securing specific deals with richer countries that had economic approaches which were complementary to our own. Our bet was that these countries would be less inclined to protect themselves from what India had to offer: labour-intensive exports and service professionals.

This new approach has informed our trade negotiations in the last few years. In 2022, we signed a free trade agreement with the UAE, followed by a limited agreement with Australia. We’re also negotiating trade bridges with other big Western economies — from the United States, to the EU, to New Zealand. An FTA with the United Kingdom, though, would be a new high watermark for our current approach.

Where we are today on India-UK trade

At least right now, India and the United Kingdom aren’t major trading partners. India is the UK’s 12th largest trade partner; while the UK is India’s 16th largest partner. Last year, all of the trade between the two countries aggregated to £42.6 billion, or a little under ₹5 lakh crore.

Notably, though, our bilateral trade activity has increased significantly in the last five years:

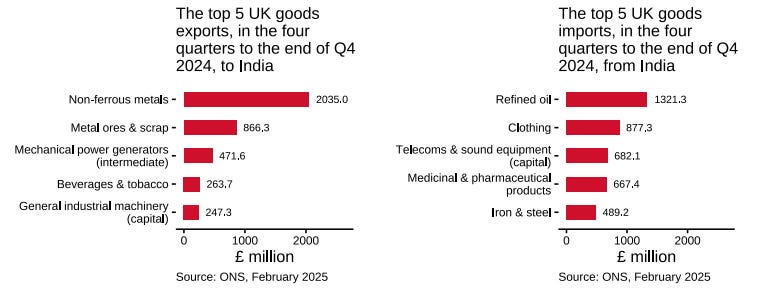

The United Kingdom’s goods exports to India, overwhelmingly, are those of metals. India sells the UK a more generalised basket of goods, with an emphasis on clothes and medicines.

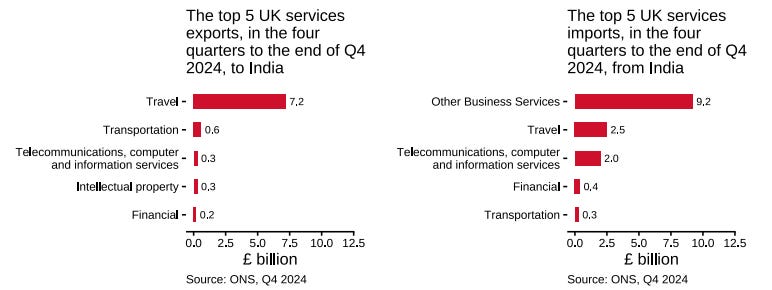

Much more of our trade is concentrated in services. The United Kingdom’s biggest service export to India, by a mile , is travel. That is, if you go to the UK for a vacation, that counts as a British export to India. In return, we sell the United Kingdom billions of dollars of business services, among other things.

Ultimately, this FTA just cements one trade partnership of the many we’re hoping to forge. The new agreement is a positive step, but not an era-defining one. Even in a best case scenario , where India-UK trade doubles by 2030 as a result of the FTA, the UK will barely break into our top five trading relationships. It is best seen as an attempt to hedge our economic bets in a time of deep uncertainty — as one among a basket of trading ties.

What the deal does

The final draft of the treaty isn’t in place yet, so we aren’t completely sure of what this deal does. But the United Kingdom has put out a fairly comprehensive policy paper, which outlines what you should expect.

Goods trade

Let’s start with goods.

India’s broad goal, through this deal, is to secure a wealthy market for its labour intensive exports. And to that end, this deal promises a lot of tariff cuts. With this deal, 99% of Indian goods exports to the United Kingdom reportedly go through duty-free. That’s frankly less impressive than it sounds, though: the UK’s average tariff rate is ~5%.

Some sectors do benefit from a small but notable drop in tariffs. Apparel, for instance, will soon be exempt from the current 9% duty they carry. India’s booming shrimp industry, too, could benefit from an 8% tariff cut.

The United Kingdom isn’t quite a goods export powerhouse. But two classes of exporters stand to gain substantially from the deal: food and beverage exporters (who’ll find it easier to sell everything from fish to chocolate), and specialised high-value manufacturers, who make things like aircraft engines and medical devices. There are two important concessions India has made, here:

-

We’re slashing our tariffs on whiskey from 150% to 75% — and plan to cut them down to 40% over the next decade.

-

We’re cutting down our tariffs on auto imports from 100% to 10% for British cars: but with a quota. Only 22,000 high value cars benefit from the deal.

Basically, if you’re keen on buying a Rolls Royce, or a nice bottle of scotch, the deal brings you some good news.

Services trade

We’re both service-oriented economies, though. Which is why a lot of the real action in this FTA has to do with who can sell which services, on what terms, and how easily people can move to deliver them. Here’s what caught our eye:

(i) Service guarantees

India has promised the UK that across a variety of service sectors — in everything from construction, to telecom — British firms will be able to operate in India without restriction. They won’t have to set up a separate presence in India, and won’t have to jump through any hoops that Indian firms don’t. This access will be “locked in” — that is, tomorrow, a different government can’t come and kick them all out again.

In return, India is getting similar guarantees for its IT professionals, consultants, and educators.

So far, professional services — things like accounting, law, auditing, etc — don’t yet see the same benefits. But both countries have agreed to negotiate for these as well. You may soon see bodies like the ICAI or the Bar Council of India dealing with their UK counterparts to figure out how to let them in. For instance, these bodies could soon give recognition to each other’s professional qualifications: which could mean that, in the near future, an Indian CA could go work at a British accounting firm without having to go through mountains of paperwork.

(ii) Easier movement

The UK will make life much easier for Indians that travel there for work. It’ll soon become much easier for business travellers to get short-term visas. Independent professionals like chefs or yoga teachers, too, will find it much easier to head to the UK.

A lot of Indians that lived in the UK, so far, faced an odd problem: they were paying for social security programs in both India and the UK. Now, the two countries are settling on a ‘Double Contributions Convention’. Basically, if you’re moving to the UK for less than three years, you don’t have to pay for their national health insurance. That’s a massive sum that UK-bound Indians will save — around 20% of their salary.

(iii) Others

There are two things that the British were really keen on, that we’ve offered.

One, the treaty hard‑codes acceptance of electronic contracts, e‑signatures and paper‑less customs forms. And it sets up a presumption of free cross-border data flows. If you’re a tech company that’s offering cross-border digital services, for instance, this will make life much easier for you.

Interestingly, it also pushes both countries to cut down on spam — something that’s probably meant for us much more than the UK.

Two, UK firms can now bid for Indian government tenders. They’ll have to set up a presence in India for that, but once they do, they can sell all sorts of services to the Indian government.

The bottom line

It’s easy to overstate what this deal means. Even if everything goes to plan — the treaty gets signed, the provisions kick in, and trade doubles by 2030 — the UK still won’t dominate India’s foreign trade relations. This treaty doesn’t mark a geopolitical pivot or a grand realignment. It’s just one milestone in a slow, careful strategy that we’ve been pursuing for years: signing targeted deals with rich, services-hungry markets that want what we have to offer.

But that doesn’t make it unimportant. In a world where trade is getting harder, and where global supply chains are fragmenting, securing predictable, long-term access to a stable market is worth celebrating. For India, it’s a hedge — a new market for its cheap, labour-rich exports. For the UK, this is a part of a long post-Brexit clean up. In that sense, the FTA is exactly what it looks like: a tidy, mutually useful arrangement between two countries that want to collaborate in an era of conflict.

Tata Motors’ amicable breakup

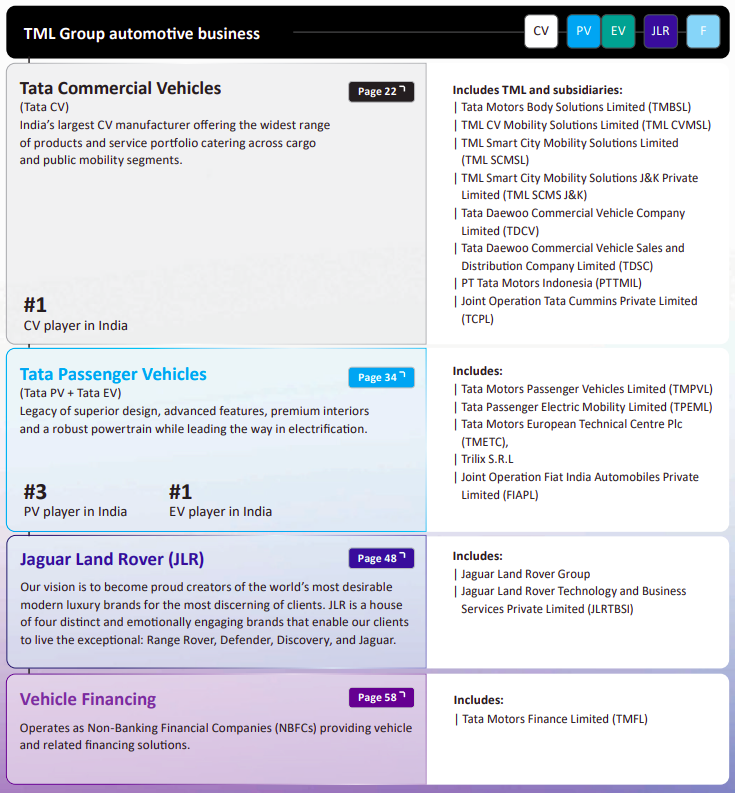

Tata Motors will soon demerge its commercial vehicles business into an independent listed entity, as per a recent exchange filing.

This decision has been years in the making, but it’s finally here. And so, when we came across the headline, we decided to investigate. More than what’s happening, we’re interested in why Tata Motors made this move, what led up to this moment and what it means for its future.

Here’s what we found.

Tata Motors needed a turnaround

The seeds of this demerger were planted under N. Chandrasekaran, who became Chairman of Tata Sons (and thus Tata Motors) in 2017.

His appointment had come amidst efforts to revive the automaker’s fortunes. At the time, Tata Motors was burdened by outdated passenger car models, quality issues, and poor service responsiveness, all of which hurt its brand perception. This was when Tata had just seen its dreams of making an affordable car for every Indian — the much-hyped but underwhelming Tata Nano — go up in flames. Meanwhile, fierce competition from giants like Hyundai and Maruti Suzuki ripped into its existing business.

These pressures triggered a period of soul-searching. There were internal reviews and restructuring efforts to unlock value. And it thus began a series of strategic moves.

In 2020, Tata Motors’ board agreed to carve out its Passenger Vehicles (PV) unit, including EVs, into a separate, wholly-owned subsidiary. This transition was completed in January 2022 — when Tata Motors Passenger Vehicles Ltd (TMPV) became its own entity.

Around the same time, in October 2021, Tata Motors raised $1 billion from TPG’s climate fund for a stake in a newly formed EV subsidiary, Tata Passenger Electric Mobility Ltd.

From 2021 onward, the company got to work, separating its three key segments into three different operational verticals:

-

Commercial Vehicles: This unit got Tata’s full range of trucks and buses, from small pickups like Ace to large multi-axle trucks and coaches.

-

Passenger Vehicles (TMPV): This unit was responsible for Tata-branded passenger cars and SUVs (Tiago, Nexon, Harrier, etc.) — both internal combustion engine (ICE) cars and EVs. The EV operations were housed in a step-down subsidiary, Tata Passenger Electric Mobility Ltd.

-

Jaguar Land Rover (JLR): A UK-based luxury car manufacturer acquired by Tata Motors in 2008. Structured as a wholly-owned subsidiary, Jaguar Land Rover Automotive plc (UK).

To provide greater autonomy and decision-making flexibility, Tata Motors appointed separate CEOs/MDs for each division.

This remained the company’s structure until the recent announcement.

The Demerger Announcement

On March 4, 2024, Tata Motors officially announced plans to split itself into two separate listed entities.

One entity will manage its Commercial Vehicles business. The other will encompass Passenger Vehicles, including both, its domestic PV/EV operations, and its line of luxury cars under JLR. If you’re a Tata Motors shareholder, you’ll receive one share of the new company for every existing Tata Motors share (1:1 entitlement) you already hold.

With this, the conceptual groundwork laid between 2017–2021 became a formal restructuring proposal, gaining shareholder approval on May 6, 2025. Here’s how things will play out:

-

First, Tata Motors will transfer its entire Commercial Vehicle business into a newly formed wholly-owned subsidiary, tentatively called TML Commercial Vehicles Ltd (TMLCV).

-

TMPV will then merge back into Tata Motors (the parent), bringing its PV assets directly under the Tata Motors banner — which will also continue to own JLR and the EV subsidiary.

-

To avoid confusion, the two resulting entities will be distinctly renamed after the demerger:

-

The Commercial Vehicle business will take the name “Tata Motors Ltd” (TML).

-

The Passenger Vehicle, EV, and JLR businesses will be renamed “Tata Motors Passenger Vehicles Ltd” (TMPV).

If this sounds technical, the essence is simple: Tata Motors will be broken into two entities, and the historic “Tata Motors” name will remain with the Commercial Vehicle business.

Why the demerger?

When Tata Motors reorganised itself internally in 2021, it created semi-autonomous business units within itself. Those semi-autonomous units showed stronger performance as independent entities than they did as a single unit. This is what the company now wants to double down on. Its management believes that a formal separation will further empower each business, giving them dedicated resources and greater agility.

But there seem to be some other motivations as well.

Externally, investor interest in EV and tech-driven auto businesses is booming . Tata’s EV arm secured high valuations (over ₹60,000 crore implied from the TPG investment). And those high valuations are going to come in handy — because the EV unit requires significant capital (~$2 billion) for its future growth.

Some analysts noted that the promising PV and EV businesses were being camouflaged within Tata Motors’ conglomerate structure, because of its large Commercial Vehicle segment. Investors evaluated the package as a whole, which meant that their passenger vehicles line wasn’t getting the interest it deserved.

A demerger can unlock value by enabling separate investor evaluation of these distinct units.

Moreover, the Commercial Vehicle business is inherently cyclical. Sales there are influenced by economic and infrastructure cycles. This volatility may have further diluted investor sentiment towards the steadier growth trajectories of the PV/JLR business. Once the two are separate, both businesses could attract different cohorts of investors, that will judge them differently based on their distinct growth profiles.

What about the demerged business?

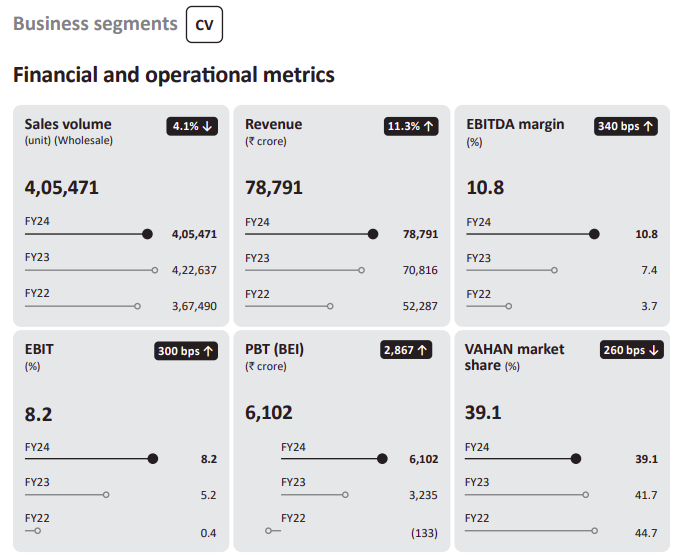

With all this cyclicality, and a dip in revenues last year, it might look like Tata Motors’ commercial vehicles, as a standalone business, might be under trouble. But that isn’t necessarily the case. It remains a market leader in this segment. Despite its declining market share, it is still the #1 player in India’s CV space, with presence across a broad product spectrum.

Last financial year, the division generated around ₹78,791 crore in revenue — nearly double its closest competitor. Even adjusted for exports and related operations, Tata’s commercial vehicle revenues remain the industry’s highest.

Importantly, the CV business is returning to strong profitability. In December 2024, EBITDA margins reached 12.4%, with EBIT at 9.6%. This reflects its effective cost management, and a lot of progress in how it runs its operations, made over prior turnaround initiatives. Comparatively, Ashok Leyland, another industry major, had similar margins, indicating Tata Motors has closed the profitability gap with its competition significantly.

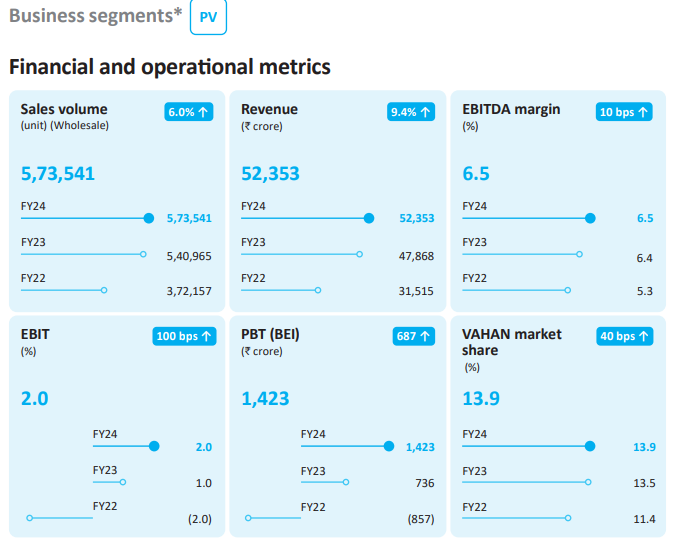

Compare this to its passenger vehicles business — which is growing in both profits and revenues, but has far thinner margins:

Overall, Tata Motors’ CV business appears robust as a standalone company—holding leadership, benefiting from scale, and maintaining profitability momentum.

Conclusion

Materially, this demerger does not significantly alter Tata Motors’ operational realities. Its commercial and passenger vehicle divisions were already functioning independently under separate management. They were simply housed under the same entity.

The key difference, now, is their formal separation into distinct entities. This introduces direct public investor scrutiny, a dynamic that previously was softened by being part of a broader conglomerate. But as an investor, it also gives you more choice around what you want to take a bet on.

Tidbits

Colgate Faces ₹200 Crore GST Dispute, Maharashtra Distributors to Halt Purchases

Source: Business Standard

Colgate Palmolive (India) is grappling with a major setback as its Maharashtra distributors, under the All India Consumer Products Distributors Federation (AICPDF), have announced they will suspend purchases of its products from May 12. The decision comes after distributors received GST notices demanding around ₹200 crore due to trade credit notes issued without corresponding GST. AICPDF claims this has placed distributors at legal risk with show-cause notices and tax recovery orders. Adding to the tension, the federation alleges Colgate is pushing stock into quick commerce channels, offering consumer discounts of 50–60%, which undercut distributor and retailer purchase prices. According to AICPDF, general trade volumes have dropped by over 50% in many districts, while field sales executives are seeing lost incentives and rising attrition. The suspension, currently limited to Maharashtra, could escalate into a nationwide protest. Colgate has yet to respond to media queries on the issue.

NLC India Renewables Signs PPA for 810 MW Solar Project at Pugal Solar Park

Source: Business Line

NLC India Renewables (NIRL) has signed a Power Purchase Agreement (PPA) with Rajasthan Rajya Vidyut Utpadan Nigam Ltd (RVUNL) for its 810 MW solar power project at Pugal Solar Park in Bikaner district. The project, awarded through a competitive tariff-based bidding process, is part of the Ministry of New & Renewable Energy’s Ultra Mega Renewable Energy Power Park Scheme. It is expected to generate around 2 billion units of green electricity annually and offset approximately 1.5 million tonnes of CO₂ emissions per year. The solar park’s total capacity is 2,000 MW, of which this project forms a major part. With this addition, NLCIL moves closer to its target of achieving 10 GW renewable capacity by 2030. The company is also exploring up to 2,000 MW of additional renewable projects and 375 MW of lignite-based thermal projects in Rajasthan. NLCIL’s CMD, Prasanna Kumar Motupalli, described the project as a “jewel” in its renewables portfolio and a pivotal milestone in its clean energy journey.

India Eases Coal Supply Rules to Boost Thermal Capacity

Source: Reuters

India has approved new rules allowing independent power producers to secure long-term coal supply contracts without needing power purchase agreements, aiming to accelerate coal-fired capacity expansion. Under the policy, producers can obtain coal through auctions for up to 25 years by paying a premium above the notified price. India’s current coal-fired power capacity stands at 222 GW, with a target to add 80 GW by 2031–32. In the past five years, the country has added nearly 28 GW of coal capacity, according to Central Electricity Authority data. Alongside coal expansion, India plans to increase clean energy capacity to 500 GW by 2030, up from the present 172 GW. However, the renewable sector faces challenges such as weak tender demand, land acquisition issues, and delays in agreements. The government also aims to promote coal plants near mine pitheads to ease transportation hurdles. The coal ministry said the measures are designed to encourage new thermal projects and strengthen future capacity.

- This edition of the newsletter was written by Pranav and Kashish.

Have you checked out The Chatter?

Have you checked out The Chatter?

Every week, we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Have you checked out One Thing We Learned?

Have you checked out One Thing We Learned?

It’s a new side-project by our writing team, and even if we say so ourselves, it’s fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That’s all. It’s chaotic, it’s unpolished - but it’s honest.

So far, we’ve written about everything from India’s state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you’re looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()