Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

The Daily Brief is stitched together by a tiny team, and as the year comes to a close, we’re taking a short breather to reset and recharge.

From December 26 to December 31, we won’t be running editions of The Daily Brief. Instead, however, we’ll introduce you to the people who run our writing room: those whose words you read here every day.

Our usual programming returns on January 1!

In today’s edition of The Daily Brief:

- Do Japanese Banks have a thing for Indian Lenders?

- India’s nuclear sector finally opens for private companies

Do Japanese Banks have a thing for Indian Lenders?

In just the last few weeks, Japan’s largest lenders have made major headlines, scooping up stakes in prominent Indian financial firms. Here are just a few:

- Mizuho Financial Group announced it will acquire a controlling stake in Indian investment bank Avendus Capital.

- Mitsubishi UFJ Financial Group (MUFG) is set to spend about $4.4 billion for a 20% stake in Shriram Finance, one of India’s biggest non-bank lenders

- Earlier this year, Sumitomo Mitsui Financial Group (SMFG) became the largest shareholder of Yes Bank.

And these are just a few examples, amidst a much larger flow of capital from Japan to India.

At first glance, it looks like Japan has suddenly fallen in love with India’s growth story. But there’s far more to the tale than “India is booming, let’s buy in ”.

Of course, India, the fastest-growing major economy in the world, is an attractive playground for global capital right now. Indian banks and lenders are benefiting from rapid digital adoption, pro-growth government policies, and a stable regulatory framework. That also explains large deals in this sector for the year. Japanese megabanks have openly voiced their enthusiasm towards this too.

However, the India story is only one part of the equation . The surge of Japanese money into India is also a broader symptom of a transformation happening in Tokyo. While you might be familiar with the Indian leg of these stories, let’s dive into what’s happening in Japan’s domestic market and corporate culture.

The Japan Discount

For years, many Japanese companies had stock prices so low that the entire company was worth less than the actual value of its assets on paper alone.

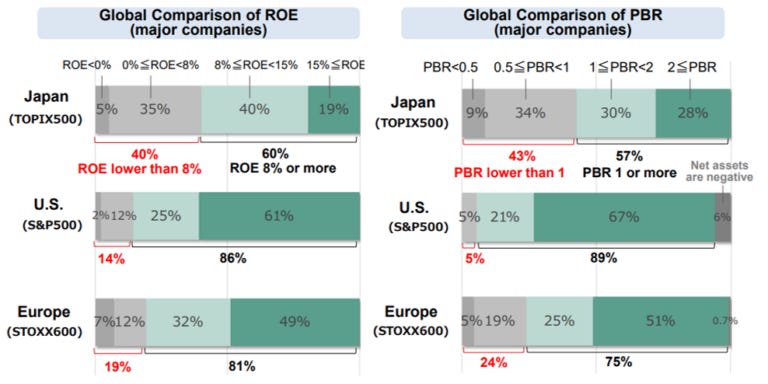

In mid-2022, roughly 43% of all companies on the Tokyo Stock Exchange’s (TSE) top tier traded below 1.0 times book value (P/B). That effectively means that investors think its management is actively destroying the assets it holds — and so, each dollar retained in the business is valued at less than a dollar . In other words, if you immediately tore those companies apart and sold them for parts, you could probably make more money than their respective managements were bringing in.

This is not normal. In the U.S., for instance, only about 5% of S&P 500 companies traded below book value in that period. Japan’s chronic undervaluation signaled a “ Japan Discount ” . It was an existential issue for Tokyo’s market attractiveness.

Why were Japanese stocks stuck in this rut? A big reason was capital inefficiency . Profits piled up on balance sheets rather than being reinvested or returned to investors. They simply couldn’t seem to find attractive avenues to deploy that capital. Many firms had low Return on Equity (ROE) – they weren’t generating enough profit relative to all the capital they held. This gave them lower valuations.

By 2023, Japanese regulators had enough. In March that year, the TSE took an unusually bold step to force firms into action. They basically said: if your stock price is languishing below your book value, you need to figure out why and fix it fast. Or as Siddhant from Persistent Capital told us:

Firms now had to execute their plans and report progress annually. And if the firms couldn’t do right by their shareholders*,* they would be publicly called out by the regulator as value-destroyers . This is as blunt of a name-and-shame campaign as it can get.

This was a paradigm shift for Japan. Suddenly, the cost of capital — basically the returns investors expect — became a real factor that Japanese CEOs could no longer ignore. And the TSE wasn’t alone; Japan’s Financial Services Agency (FSA) and the government as a whole were backing this push as part of a broader effort to reinvigorate the market.

Sayōnara Cross-Shareholdings

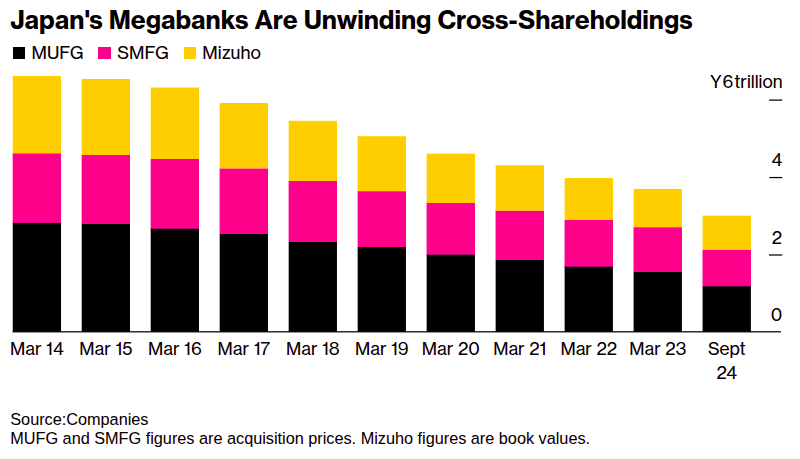

All this while, there was another structural change underway in Japan: the unwinding of cross-shareholdings. We covered this unique feature of the Japanese market in our edition on Japanese auto, but we’ll summarize it quickly.

Until recently, many Japanese companies — banks, suppliers, and industrial behemoths — mutually owned shares in one another. These weren’t investments to earn returns, but rather a way to cement long-term business relationships, secure friendly shareholders, share risks and get cheap loans. It also made hostile takeovers extremely difficult and insulated executives from outside pressure.

That system gave them stability while they grew fast. But today, it’s seen as dead weight. Why? Because these holdings tie up tons of capital and drag down financial performance. They simply sit on the balance sheet, bloating the asset base, without producing proportional income. This aggravated the “Japan Discount ”.

For years, the country made slow progress in unwinding these cross-shareholdings. But in 2024, a major scandal erupted in Japan’s insurance industry. Several of the country’s largest insurers, all of whom held parts of each other, were found to be colluding in setting prices. As the dirty details came out, regulators demanded that these insurers entirely remove their stockholdings in other firms.

The insurers committed to s elling all those shares in the coming years. Suddenly, trillions of yen worth of equity was slated to be released back into the market. That’s a lot of capital freed up for better uses.

And that’s where this story begins for our Japanese mega-banks, who were now flush with cash.

From Hoarding to Spending

First, firms began giving money back to their shareholders. A few years ago, the idea of conservative Japanese firms aggressively returning cash would’ve raised eyebrows, but not anymore. With these reforms, corporate Japan has gone from hoarding cash to showering it on investors.

The most immediate evidence is a record-breaking, even accelerating surge in share buybacks — when a company purchases its own stock from the market. In November 2024 alone, buyback announcements exceeded ¥2 trillion, a monthly record. Buybacks are a savvy move if you believe your stock is undervalued (which, as we noted, many Japanese stocks were). For companies trading below book value, buybacks are mathematically one of the most efficient ways to improve ROE and boost the share price.

Dividends are following a similar skyward trajectory. Total dividend payouts by Japanese firms hit roughly ¥18 trillion, another record high, last financial year — reflecting a much more shareholder-friendly stance than in the past.

This revolution signals that Japanese management teams are finally accepting the cost of equity as a real constraint. They’re realising that they can’t just sit on money — shareholders expect a return, and if they can’t get good returns on their cash, they ought to give it back.

No one is feeling this transformation more acutely than Japan’s megabanks — MUFG, SMFG, and Mizuho. These banking giants are sitting on mountains of cash . They’ve enjoyed record earnings recently, thanks to a resilient business at home and years of conservative management. On top of that, as we discussed, they’ve been selling off their cross-shareholdings, which is bringing in even more money.

But now, the megabanks have explicitly signaled they are pivoting from building up buffers of capital, to growth .

Only, even as they ramped up share buybacks and dividend hikes, they still had excess capital — well above what regulators require. They simply had too much cash for the growth they could generate. By now, they’ve also saturated the Japanese market, where loan demand is flat. As a result, all three major banks’ stock valuations have been stubbornly low, with P/B ratios still hovering around or below 1. The market isn’t convinced they can deploy their capital profitably.

Where could they find growth?

Now, these mega-banks have a mandate from both regulators and investors to go out of the country and chase growth. And that’s exactly what they’re doing: with their targets being the US, the rest of Asia, and, of course, India.

Arigatou, India & Abroad

Japanese banks have been in India for decades, but in a modest way — with simple branch operations or minority stakes. But now, we’re seeing the fresh, aggressive push as we highlighted at the start. Here’s what each mega-bank has done so far:

- MUFG has made India a core pillar of its Asia strategy, aiming to double loan exposure to ~$30 bn; it has courted large conglomerates like Reliance and Adani, taken a $333 mn stake in DMI Finance, and agreed to buy ~20% of Shriram Finance.

- SMFG has built a retail and banking presence by acquiring Fullerton India in phases and investing ~$1.6 bn for a 20% stake in Yes Bank, becoming its largest shareholder.

- Mizuho is expanding across consumer finance and investment banking, buying ~15% of Kisetsu Saison Finance (India) for ~$145 mn and acquiring control of KKR-backed Avendus Capital.

India offers Japanese banks a mix of what they want: high loan growth, an under-served retail credit market and big infrastructure financing needs. It’s one of the few places where these banks can deploy substantial capital for potentially solid returns.

More importantly, the interest isn’t just one-sided. India’s regulatory environment has been relatively welcoming to foreign investment in finance, too. There are discussions about making it even easier for outsiders to invest in our banks or get Indian banking licenses. So the door is open for the Japanese, perhaps more now than ever.

That said, Japan’s megabanks aren’t putting all their eggs in the India basket. Their other big focus is the United States, for whom Japan is the biggest source of FDI of all countries. But, their approach there looks very different. In North America, rather than trying to buy retail banks or loan books, Japanese banks are mostly aiming to expand in investment banking services. After all, the U.S. has by far the world’s largest fee pool for investment banking — there’s more business in advising mergers and acquisitions than in just handing out credit.

Can Japan Inc. Deliver?

With all this excitement about Japanese money on the move, it’s only fair to ask: what could go wrong?

There are certainly some risks and caveats to this story. For one, expanding in a foreign market – especially one as competitive as India’s banking sector – is not easy. In fact, the track record of foreign banks in India has been, at best, mixed .

Then there’s the issue of valuation discipline. It’s somewhat ironic: Japanese companies are being punished for being overly cautious and holding off on investments at home , but as they venture into growth markets, they might be tempted to splash out big sums for potentially overvalued companies . Thus far, the deals (like Shriram Finance at ~3 times book value for a stake, or the price for Avendus) seem to be done with a strategic rationale. But as more Japanese firms join the fray, paying too high a price for growth could undermine the very goal of better ROE.

Additionally, foreign expansion comes with geopolitical and currency considerations. The yen’s value, interest rate differentials, and geopolitical stability in host countries can all impact success.

What we’re witnessing is a remarkable and somewhat under-the-radar transformation in Japan’s corporate behavior, with ripple effects far beyond Japan’s shores.

India’s nuclear sector finally opens for private companies

For more than sixty years, nuclear power in India has been a government monopoly. All that private companies could do was manufacture equipment. They could never own a plant, never hold the fuel, never operate the reactor. This has now changed.

The Sustainable Harnessing and Advancement of Nuclear Energy for Transforming India Act, 2025 or simply the SHANTI Bill, was passed by Parliament during the Winter Session. It is now India’s nuclear energy law, the most significant shift in our nuclear policy since the sector was first brought under state control in 1962.

To understand what this means, you have to understand the system it replaces, because nuclear policy in India has never been straightforward.

See, nuclear energy has always evoked terror . It carries images of the destruction of Hiroshima and Nagasaki, even though those were weapons, not power plants.

Not that power plants have been without incident. There was Chernobyl in 1986 and Fukushima in 2011 — both civilian reactors, both globally traumatic. Because radiation leaves invisible but long-lasting effects, public anxiety has persisted for decades, even as reactor technology has advanced dramatically. Any government trying to expand nuclear power must work against this deep-rooted anxiety.

And in India’s case, there’s yet another layer: our complicated nuclear history.

How we got here

When India passed the Atomic Energy Act in 1962, the world was in the Cold War, and nuclear technology was inseparable from national security. India had just begun its atomic research programme under Homi Bhabha, and the state wanted total control over uranium, over reactors, over research; over anything that could conceivably be turned into a weapon.

So, the 1962 Act made nuclear energy a government preserve: only the central government or government-owned companies could mine uranium, process it, enrich it, build reactors, operate them, or handle spent fuel.

Private companies could only participate as contractors. L&T made pressure vessels, Godrej manufactured components, Walchandnagar supplied heavy equipment, and more. But they were vendors, not owners. They built to specification, delivered, got paid, and that was the end of their involvement. The government owned everything that mattered.

This arrangement held for decades. For much of that time, India was shut out of the global nuclear market entirely. When India first tested a nuclear weapon in 1974, the world’s nuclear suppliers stopped selling uranium and reactor technology to us. India had to build its nuclear programme in isolation.

That seemed like it would change in 2008, when the Indo-US nuclear deal gave India a special exemption. We could now buy fuel and reactors from abroad, even though we wouldn’t sign the Non-Proliferation Treaty. After years of being shut out, we were at the cusp of unlocking a new era of expansion.

But just as the doors were opening, a new law slammed them shut again.

In 2010, India enacted the Civil Liability for Nuclear Damage Act, meant to ensure victims would be compensated if an accident ever occurred. Most countries follow a simple principle: the operator of the plant bears all liability, and suppliers — the companies that provide equipment — are shielded. After all, once a component is installed, the supplier has no control over how it is used. Holding them liable for accidents decades later would be unreasonable.

Only, India took a different view.

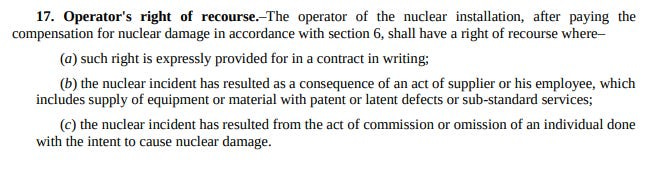

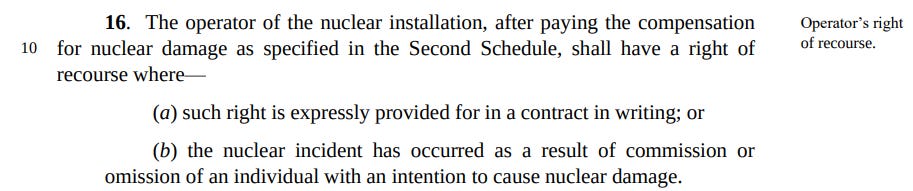

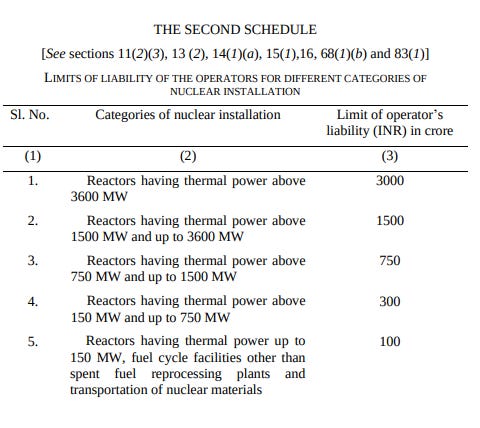

Indian lawmakers introduced a liability law that held all parties, including suppliers of nuclear technology and materials, responsible for damages in case of an accident. The law capped the operator’s liability at ₹1,500 crore, but its most controversial provision was Clause 17(b), which allowed NPCIL, the state-owned nuclear operator, to seek compensation from suppliers if their equipment was found to have caused an accident.

That legal uncertainty proved costly. International vendors hesitated to enter the Indian market, projects slowed, and capacity additions lagged — leaving India’s nuclear output stuck at around 8 GW, well short of what its energy needs and climate commitments demanded.

How does the SHANTI bill change things?

The new law consolidates the 1962 Act and the 2010 Act into a single modern framework. In doing so, it rewrites the rules of participation.

For one, the supplier liability issue was addressed by bringing India’s framework closer to global norms. Under the new law, the operator bears liability for any accident. Suppliers can only be sued if they explicitly accepted liability in their contract, or if they intentionally caused harm. The clause that allowed operators to chase suppliers for defective components is gone.

This may sound like a technical change, but it removes a fifteen year-old gridlock. Foreign vendors can now engage with India without fearing open-ended legal exposure far into the future. Domestic manufacturers can supply components without worrying that a valve used incorrectly by an operator will come back to haunt them.

Additionally, the new law also does away with its flat ₹1,500 crore liability cap. Now, liability is graded by reactor size; large reactors carry higher liability limits, while small modular reactors face much lower exposure (around ₹100 crore). This grading matters. A private company might be willing to risk ₹100 crore of liability for an SMR, but the earlier flat ₹1,500 crore exposure made private participation impractical.

There’s also another, deeper shift — in who can own and operate nuclear plants.

Until now, this was restricted to government owned companies. The SHANTI Bill opens this up to private Indian companies. That is, you might soon see Tata, or Reliance, or Adani, or L&T applying for licences to build, own, and operate nuclear reactors. Some of them were already manufacturing the equipment. Now, they can own the entire project.

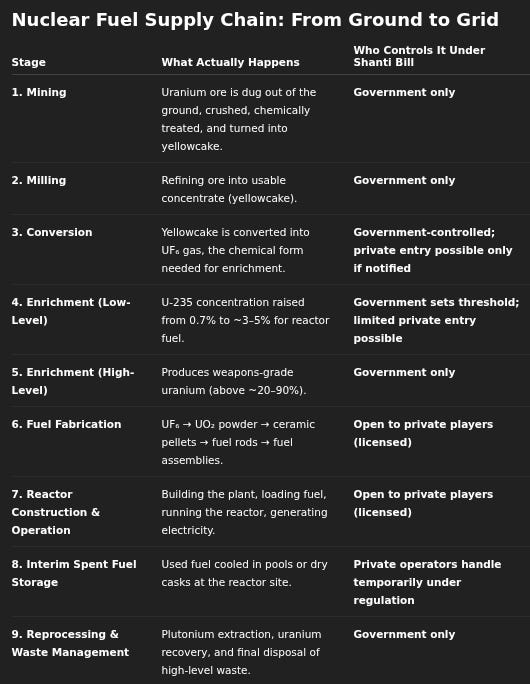

That’s a big deal. But it does not mean India has completely thrown open the nuclear sector. The government has been careful about where the lines are. To understand those lines, however, you need to understand how nuclear fuel moves from the ground to the grid.

It begins with mining.

Uranium exists in ores, mixed with rock, buried underground. In India, deposits are found mainly in Jharkhand, Andhra Pradesh, and a few other states. You dig up the ore, crush it, treat it chemically, and extract a concentrate called “yellowcake ”. This step — mining and milling — remains exclusively with the government, and private firms cannot touch it.

Next, you must turn that concentrate into reactor fuel . This requires two things: first, you must convert it into a usable chemical form, and then, you have to increase the concentration of the uranium isotope that actually produces energy.

Natural uranium mostly belongs to the U-238 isotope, which can’t sustain a chain reaction. Only about 0.7% is U-235, the isotope that splits and releases heat. That, however, is too little to actually do anything.

And so, reactor fuel needs to be “enriched” — that is, the concentration of U-235 has to be raised to 3-5%. The SHANTI Bill gives the government the power to decide how much of this work can be opened to private players. It can notify thresholds up to which private companies may participate. But the sensitive end of enrichment stays firmly with the state.

That’s for good reason. The same machines that enrich uranium to 5% can, if run longer, take it all the way to 90%. At that point, you have weapons-grade Uranium. It’s simply not acceptable for a private company to get there.

Once enriched, the uranium is shaped into fuel that can go into a reactor. This step is open to private players. And so is the next one: building and operating the reactor itself, generating electricity, selling it to the grid. This is the commercial heart of nuclear power, and this is where private capital can now flow.

But once you come to the reactor’s output , we’re in sensitive territory again.

Spent fuel — nuclear fuel that has been used up — is highly radioactive. It also contains plutonium, a byproduct of the fission process, which can be used to make a nuclear bomb. And so, under the new law, private operators store spent fuel temporarily while it cools, but must then hand it over to the government. The government handles all subsequent steps: reprocessing to extract usable material, and disposing of high-level waste that will remain dangerous for thousands of years.

Control without ownership

So the picture that emerges is not one of full-blown deregulation, but a controlled opening. The government keeps the front end of the chain (mining and milling), and the back-end (reprocessing and waste disposal) entirely to itself. But, it now allows private participation in the middle, where reactors are built and power is generated — the most capital-intensive part of the process.

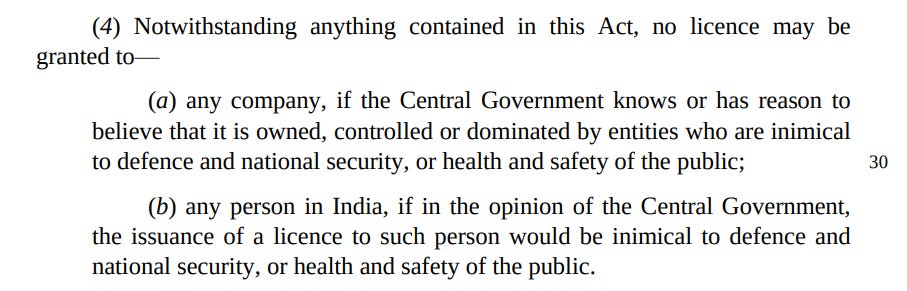

Even there, it retains enormous control. For instance, the Department of Atomic Energy can refuse a licence to any company it believes is controlled by entities “who are inimical to defence and national security “.

It can shut down any facility if it believes safety is compromised. If a private firm abandons a reactor after fuel has been loaded, all assets transfer to the government automatically, free from any claims by creditors. The government can classify information, declare areas off-limits, and even claim intellectual property created in sensitive domains. To a degree, this ensures safety and accountability, and hopefully can reduce public fear.

Now, a full-fledged nuclear policy is only as good as the body that regulates it. On that note, for the first time, the Atomic Energy Regulatory Board (AERB) now has statutory status as the de facto regulator — a meaningful upgrade from its earlier existence. It can now make binding regulations, conduct inspections, impose penalties, and recommend licence cancellations.

But, the AERB won’t be a fully independent nuclear regulator. The committee that selects AERB’s leadership is constituted by the Atomic Energy Commission, and the Department of Atomic Energy remains the central authority for all purposes under this law. In contrast, for instance, the US has the Nuclear Regulatory Commission, which is entirely separate (and independent) from the Department of Energy.

In sum, AERB continues to remain inside the atomic establishment it is meant to regulate. This could potentially create conflicts of interest.

And yet, even with all these controls, the SHANTI Bill represents a genuine turning point. It is an acknowledgement of the fact that India cannot meet its energy needs and climate commitments simultaneously, without dramatically expanding nuclear power and getting private actors onboard in some capacity.

With this new regime in place, we’re targeting 100 gigawatts of nuclear capacity by 2047 — up from under 9 gigawatts today. The budget already allocated ₹20,000 crore for small modular reactors. As we’ve written about before, this year, India rediscovered its nuclear ambitions. What was missing, so far, was a legal framework that allowed private capital and private execution to participate.

That framework now exists. That, in itself, is a monumental shift.

Tidbits

-

BPCL–Coal India JV for coal gasification in Maharashtra

BPCL has approved a JV with Coal India to set up a coal gasification project at Western Coalfields, Maharashtra. Coal India will hold 51% and BPCL 49%. The plant will produce synthetic natural gas (SNG) as a domestic substitute for imported gas, aligned with the government’s National Coal Gasification Mission.

2.Source* : ET EnergyWorld -

India slaps anti-dumping duty on Chinese steel

India has imposed a five-year anti-dumping duty on certain cold-rolled steel imports from China, ranging from $224 to $415 per tonne. The move aims to shield domestic steelmakers from cheap imports and follows rising pressure from industry over falling prices and excess capacity.

3.Source:* Reuters -

Cheap oil-linked LNG beats US gas for India

Indian buyers are favouring oil-linked LNG from West Asia over US gas as Henry Hub prices and shipping costs surge. Oil-linked LNG is currently 25–30% cheaper than US LNG, cooling interest in long-term American contracts—even as LNG remains central to India–US trade talks.

4.Source:* Business Standard

- This edition of the newsletter was written by Kashish and Krishna.

Tired of trying to predict the next miracle? Just track the market cheaply instead.

It isn’t our style to use this newsletter to sell you on something, but we’re going to make an exception; this just makes sense.

Many people ask us how to start their investment journey. Perhaps the easiest, most sensible way of doing so is to invest in low-cost index mutual funds. These aren’t meant to perform magic, but that’s the point. They just follow the market’s trajectory as cheaply and cleanly as possible. You get to partake in the market’s growth without paying through your nose in fees. That’s as good a deal as you’ll get.

Curious? Head on over to Coin by Zerodha to start investing. And if you don’t know where to put your money, we’re making it easy with simple-to-understand index funds from our own AMC.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()