Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- A quarterly temperature check for Indian IT

- Will India’s bets on solar manufacturing pay off?

A quarterly temperature check for Indian IT

Yet again, it’s Indian IT results season. And once more, the industry faces the same existential questions it’s been grappling with for a long time.

Indian IT has been caught in a crossfire for all of last year. US tariffs loom over client budgets. A potential global slowdown has tightened discretionary spending. On top of all that, Indian IT’s business model faces an existential threat from AI, which has taken a huge leap between this quarter and the last. None of these are new problems.

But, the directions each company is taking to escape this mess have become clearer this quarter. We’ll be digging into the latest Q3 FY26 results of Infosys, TCS, HCLTech and Tech Mahindra (TechM) to see how they’re rising to the occasion. We’ll also separately cover smaller midcap IT firms soon.

The numbers

Let’s start with the figures.

Now, in a one-off event, the profits of most large IT firms were hit by the new labour codes, so their overall figures show a decline. But when adjusted for this, the picture changes mostly in their favor.

TCS posted revenue of over ₹67,000 crore, up ~5% year-on-year and 2% from last quarter. The net profit was down by 14% year-on-year to ₹10,657 crore. But the absolute profit adjusted for one-off costs actually grew 8.5%, while operating margins held steady. The highlight of TCS’ results lies in their much-awaited disclosure of AI services revenue — which is $1.8 billion (~₹16,000 crore) on an annualized rate.

For Infosys , revenue rose to ~₹45,500 crore, up ~9% y-o-y. Net profit was down slightly. However, in a show of confidence, Infosys raised its future revenue guidance to 3-3.5% in constant currency, up from 2-3% earlier. They won nearly twice the deals as last year, and more than half of it was net-new business.

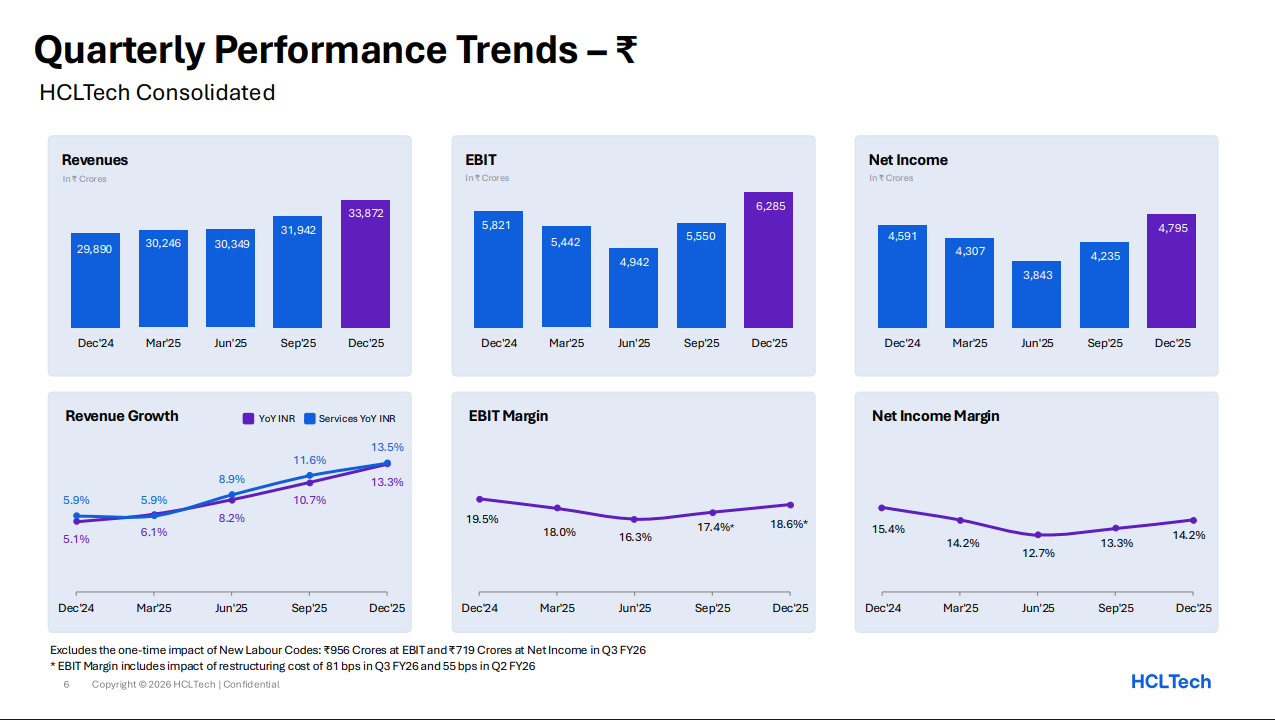

HCLTech has had a strong quarter, despite a decline in net profit. Revenue jumped by 13% y-o-y to ₹33,872 crore, while adjusted EBIT margins rose by one percentage point to 18.6%. As per management, HCLTech’s order book is the strongest it has been in the last 4 years. And, it has reported a ~20% quarterly increase in its “Advanced AI ” business.

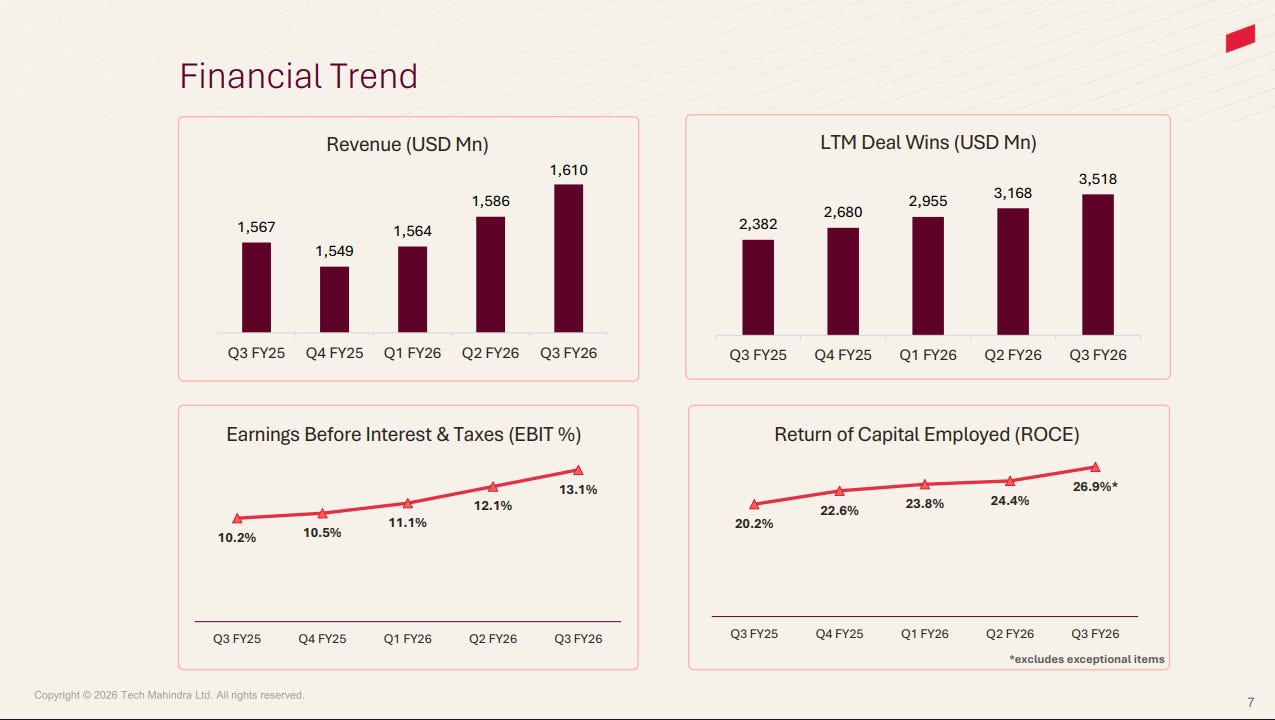

Tech Mahindra had a strong quarter as well. Revenue grew ~8% YoY to ₹14,393 crore, while net profit rose 14% YoY to ₹1,122 crore. This was the ninth consecutive quarter that TechM expanded its EBIT margins. Deal wins were up 47% from last year — the highest it’s been in five years.

All 4 companies have had mostly positive sentiments to write about. But how do we rate what’s happening within those results?

Tr(ai)ning period is over

This quarter’s results mentioned AI more than ever before. Now, large-cap Indian IT’s approach to AI has mostly been a black-box for outsiders. But it’s worth reading between the lines to demystify this maze.

To do so, we first decided to look at a more optimistic case for AI adoption in Indian IT, and then the not-so-optimistic side of things.

History doesn’t repeat itself, but…

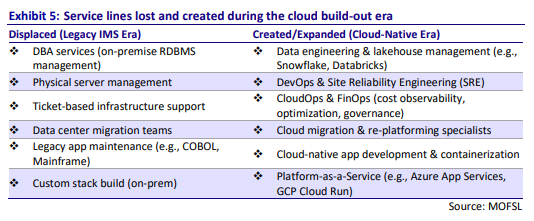

Recently, Motilal Oswal came up with an interesting argument for why Indian IT will ride the AI wave successfully. They believe there’s a historical parallel for what’s happening now, that is Indian IT’s adoption of cloud technology .

See, around 2016, Big Tech firms — the very same building out AI data centers are rapid speed today — were at the forefront of building non-AI data centers. During this phase, cloud seemed to deflate the revenue streams of Indian IT firms. For more on this history, do watch the IT breakdown by our friends at Zerodha Varsity. For instance, before cloud, companies hosted their data on large, local servers, and Indian IT firms maintained these servers. But with cloud, there was no need to keep — or maintain — locally-hosted servers.

But, companies did eventually need help in figuring out how to integrate cloud with their own systems. That’s where Indian IT jumped in, as cloud opened up new revenue streams for them to tap.

That, Motilal Oswal says, is what could happen with AI. We are now in the phase where AI data center capex is aggressive, slowly reducing Indian IT’s strengths. But, once the additional benefit of more capex reduces and deployment takes priority, it will unlock new revenue streams. And then, Indian IT firms shall have the unique benefit of fully understanding the technology stacks of their long-term clients — some of the world’s biggest firms.

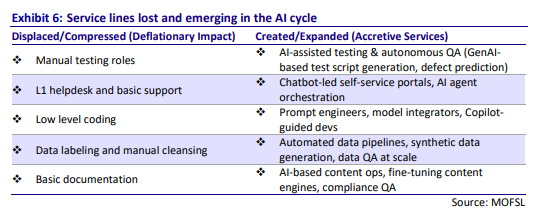

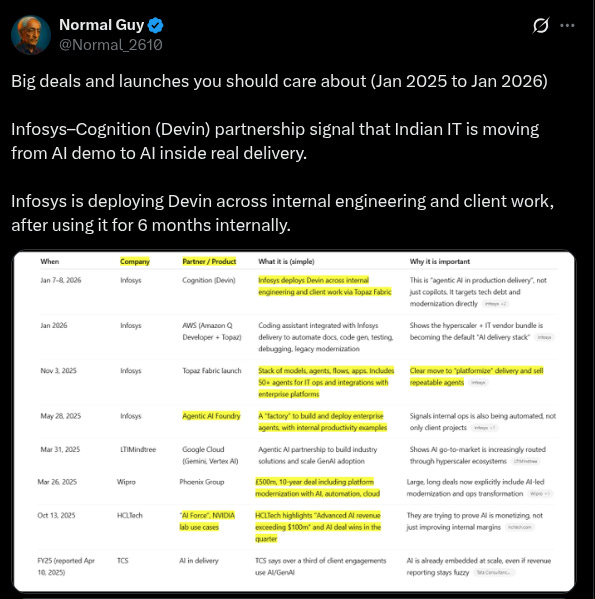

This quarter, we might be seeing some early signs of this hypothesis play out. The management of Infosys, for instance, identified 6 key new value-pools that AI is generating for them. Infosys has also partnered with AI firm Cognition to deploy their autonomous software engineer, Devin , across client work — perhaps, to automate low-level coding.

Meanwhile, TCS is also showing real-world use cases of AI agents, particularly in BFSI and retail. Their turnaround times for AI deployments are getting much faster.

![]()

HCLTech has a somewhat different AI playbook, owing to its unique ties with the AI hardware and semiconductor supply chains. For one, HCLTech’s robotics solution was selected by a European client to manage their robot fleets. It is also helping a global tech major manage some of its AI data center workloads, linking it to the AI capex boom.

A prediction often made is that AI will remove Indian IT’s old ways of billing clients based on headcount and hours. Instead, outcome-based pricing will become the norm. Now, this hasn’t happened yet, but Indian IT is taking this idea very seriously. TechM, for instance, now makes half its revenue from fixed-price , outcome-based deals . Not all of these deals will be AI-linked, but this is certainly worth watching out for.

…does it rhyme?

Though Indian IT is clearly moving from AI pilots to actual deployment, particularly with AI agents, it cannot shed its burdens overnight. These are still bureaucratic, slow-moving companies, struggling to integrate AI at large-scale.

Recently, we listened to a great podcast by The Ken with Sidu Ponnappa, the founder of an AI startup aiming to revolutionize IT services. Ponnappa’s key argument is that AI is moving much faster than IT companies can decide which AI vendor (like OpenAI or Microsoft) to buy or lease from. The winner won’t be the one that picks the best tool at a given time. Anybody can rent such a tool and build their own AI agents — large IT firms won’t have an edge here. The best IT firm, Ponnappa argues, would be the one that builds a flexible operating system (OS) that can swap between AI tools quickly. It’s the only way they can build a unique moat.

This quarter, multiple Indian IT firms have made big AI procurement decisions — Infosys with Devin, TechM with Gemini, and so on. These tools get procured at mass after months of internal testing . But, they could become redundant with a single big AI development.

Now, each IT firm seems to have an AI suite of its own, which could be their OS which manages such redundancies. For instance, Infosys’ AI platform is called Topaz , TCS has WisdomNext , etc. But how flexible these are, and how much revenue can be attributed to these platforms alone, are still vague and unknown.

So, the answer to “Does Indian IT have a defensible AI business ” is still very unclear. This time may not be the same as the cloud era. And without a moat, the new value-pools that AI opens up for Indian IT could be taken away by others.

Rewiring hiring

Let’s move on to hiring trends.

Out of these four, Infosys was the only outlier in terms of actually adding to its headcount. It added a net of over 5,000 employees this quarter (including freshers). And it will hire more going forward.

Everyone else, though, lost headcount . To some degree, this is cyclical — and even voluntary. But there are also some structural reasons for this.

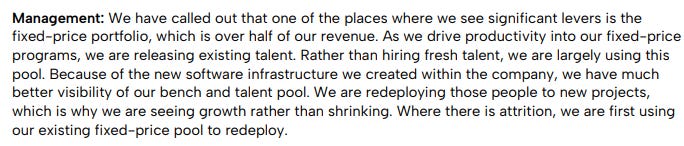

Let’s start with TCS, which laid off 12,000 people two quarters ago. This number increased to nearly 20,000 in Q2 — or 3% of TCS’ entire workforce. This quarter, they released 1,800 more employees, for the same official reason as the last two times — they couldn’t be redeployed due to skill mismatches. At the same time, though, TCS is going through a huge restructuring in the wake of AI. The past layoffs weren’t strongly linked to AI, but TCS has indicated that they won’t be looking at mass-hiring in the near future. Their focus, they say, will now be on reskilling existing workers instead.

TechM might already be ahead on that front, as their headcount fell by over 3,000. One of the biggest reasons for this is their fixed-price deals strategy , which avoids pricing by headcount. These deals, they say, are increasing their productivity to such a degree that it is releasing lots of internal talent that they can readily tap into instead of hiring externally .

Perhaps, we are seeing the beginning of Indian IT decoupling headcount from revenue, in a world where Indian IT was already getting selective about hiring. We aren’t sure how this will play out over time, but this is a notable inflection point.

Finger in every pie

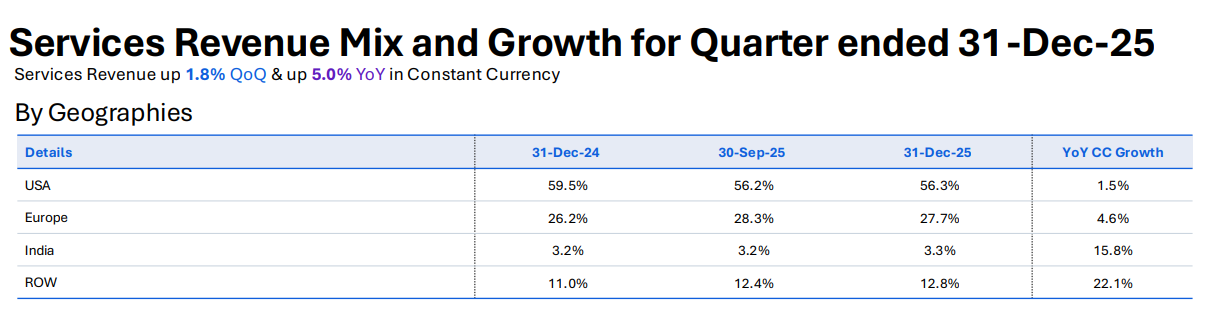

Lastly, let’s take a look at the geography of Indian IT’s business. Unlike smaller firms, large Indian IT firms are not as reliant on the US to drive business, and are quite-well diversified. This quarter, in the face of US tariffs, they only strengthened their hedge.

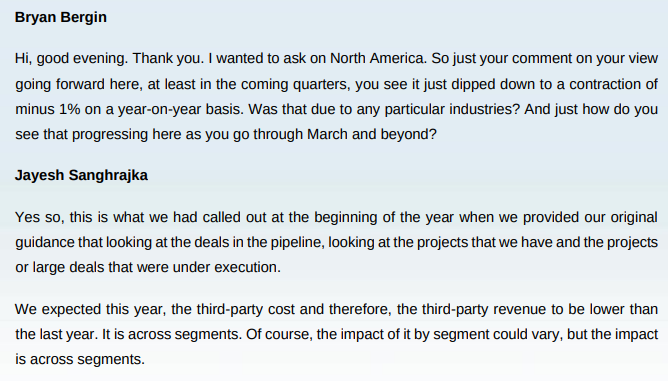

Take TCS, for instance. It saw its US business plateau, but Europe was its brightest spot. The same stood for Infosys, whose European business grew by 7.2% y-o-y, while its North American business actually contracted a little. Meanwhile, TechM’s Europe business grew by an impressive 11% y-o-y.

But Indian IT isn’t just looking at the Western world for business. TechM, for instance, is focusing on priority markets like Japan, South-East Asia and Australia. In these markets, revenues grew by ~13% y-o-y. HCLTech, meanwhile, reported a whopping 22% annual increase in business from regions that aren’t the US, Europe, or India. These are the new areas of fast growth for Indian IT.

This diversification also reflects what their clients really want. For instance, the idea of a sovereign AI cloud has been a consistent theme across these companies. Many firms (and nations) want to reduce dependency on American cloud providers by building their own. For example, TechM was chosen by a Middle Eastern telecom group to build “sovereign AI infrastructure ”. HCLTech also noted an uptick in its marketing automation platform because its “clients wanted sovereign solutions” .

Conclusion

Last quarter, we covered how Indian IT might be recovering after a bout of disappointing results. They have indeed continued their recovery into this quarter.

On AI deployment, Indian IT seems to be doing more than just tacking on LLMs to client work. But this doesn’t mean the industry has found its AI moat. At the same time, Indian IT isn’t hiring like before. Partly, it’s because of a general slowdown of business. But maybe, the effect of AI driving internal productivity is also catching up.

Indian IT is also becoming more resilient to the global landscape, continuing its hedge away from the US. Europe is slowly becoming an anchor, while other regions are growing extremely fast.

Indian IT’s giants continue to fight against the growing tide of uncertainty, trying to avoid becoming dinosaurs.

Will India’s bets on solar manufacturing pay off?

In 2021, India began a massive series of bets on building its own solar manufacturing industry. Over the next couple of years, we committed ₹24,000 crore to the project, through a production linked incentive scheme executed through many tranches.

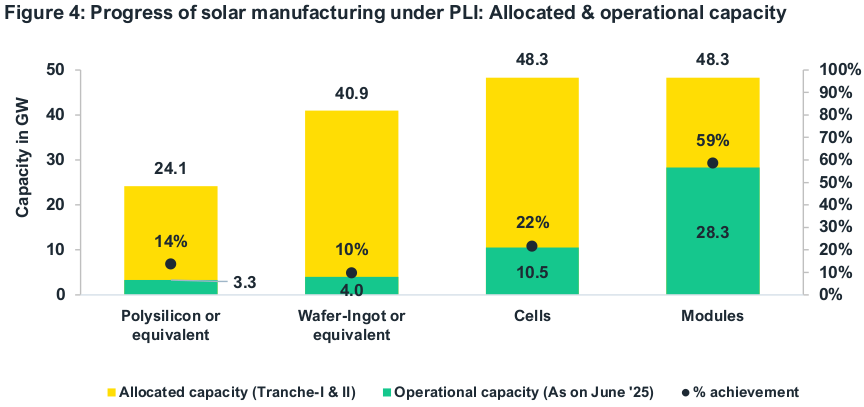

Four years into this bet, the results are mixed. The scheme did succeed at getting some capacity online. But we came nowhere close to what we had once hoped. Today, only 29% of capacity we had targeted is operational. And the most critical parts of the value chain — where the argument for self-reliance is the strongest — is barely off the ground.

What holds us back? Well, as happens so often, our industrial policy collided with economic reality. It’s never easy to create an industry from scratch, and it’s even harder to do so when the space has been consumed by a giant like China.

To understand where our plans have run aground, we’re looking at a report published by the Institute for Energy Economics and Financial Analysis, in partnership with JMK Research and Analysis.

Here’s what we learnt.

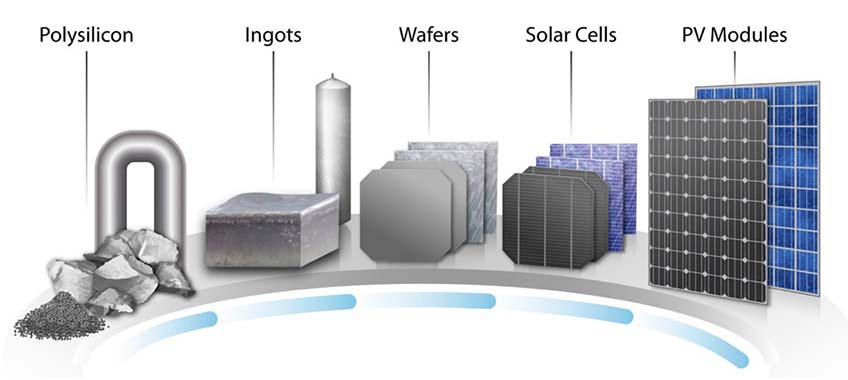

The solar industry is a long, difficult chain

Before we get to where we’re falling short, you need to understand what we’re trying to build.

To get to the humble solar panel — silicon wafers arranged in a weatherproof frame — you need to go through a lengthy and murderously difficult manufacturing process.

Solar panels are made of silicon for a simple reason: pure silicon arranges itself in a perfect crystal lattice. Its 3D structure is so neat and regular that electrons can zoom through it smoothly. That flow, ultimately, is electricity. Impurities, though, break the crystal structure. A single wrong atom among a million silicon ones can start blocking electrons in their way.

This is why, to make a solar cell, you have to begin with exceedingly pure, semiconductor-grade silicon. That isn’t easy to create. You need to heat it at 2,000°C, and then refine it chemically. This consumes enormous amounts of energy and chemicals, making it the most expensive part of the process.

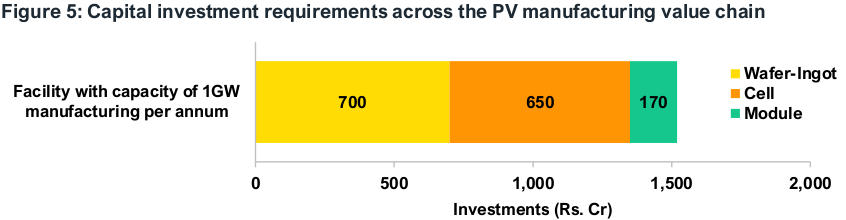

Think about it like this: if you want to make enough pure silicon to feed one gigawatt of solar module capacity, your capital expenses come up to ₹800-1,000 crore.

{kind=link}

This gives you “polysilicon” — large chunks or rods of pure silicon. But it isn’t useful yet. It doesn’t have the crystal structure we need.

For that, we need to create ingots ; we melt polysilicon at 1,400°C, and then let it arrange itself into a giant crystal. Then we slice these with diamond saws into wafers that are thinner than a couple of sheets of paper. The capital expenses for a wafer plant, per gigawatt of module capacity, costs another ₹700 crore.

{kind=link}

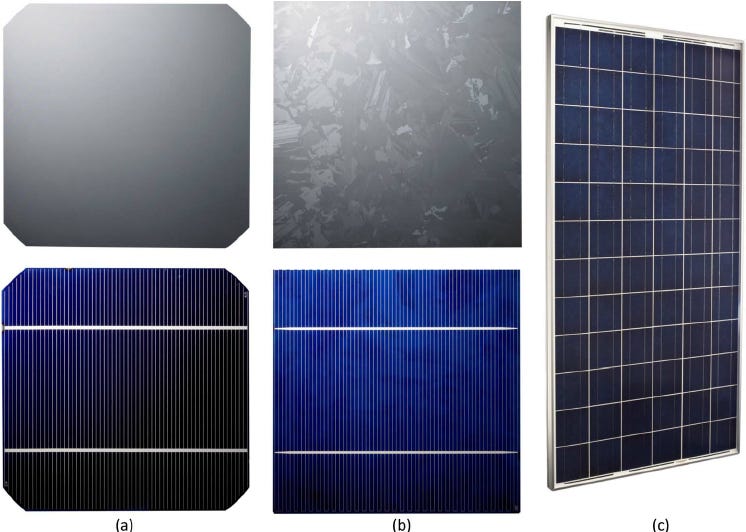

These are still not good enough to conduct electricity, though. For that, these wafers need to be turned into cells . You need to deposit layers of other material atop these: chemicals that create a charge, anti-reflective coatings, metallic connectors, and so on. This, again, is an expensive process — requiring cleanrooms and special machinery. For each gigawatt of module capacity, the capital expenses for cell-making are roughly ₹650 crore.

From wafers, to cells, to modules

At this point, you already have the building blocks you need to create solar energy. Now comes the simplest part of the process: fitting the cells together . You solder the cells, laminate them between glass and insulation sheets, frame them, and fit electrical connectors. This is laborious , but it isn’t exotic. To churn out a gigawatt worth of modules, the capital costs come to just ~₹150 crore. Compared to the rest of the process, this is cheap.

That’s where our problems begin.

India’s solar ambitions

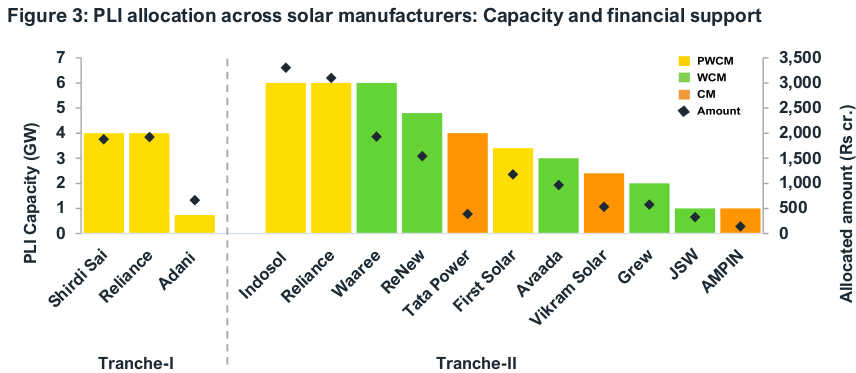

Back in 2021, the government announced incentives worth ₹4,500 crore, for those who could set-up integrated factories that could manufacture everything end-to-end, from polysilicon to modules. The response was heartening. Three players — Reliance, Adani and Shirdi Sai Electricals — were eventually selected to go ahead with the program, to set up ~9 gigawatts of capacity. But the bids it received where for nearly six times as much.

The response was so good, in fact, that the government soon came up with a much more ambitious program. This time around, you could choose what you wanted to do — whether you wanted to run the entire supply chain, or source wafers and turn them into modules, or if you just wanted to assemble modules alone. Many more companies applied, this time around, and eleven were selected — including Waaree, Tata Power, JSW, and others. In total, they were allocated nearly ₹14,000 crores.

The scheme, it seemed, was off to a flying start. By the end, the government projected, we would have 65 gigawatts of solar capacity. It would bring in ₹94,000 crore in new investment, and give employment to nearly 2 lakh people.

But reality has a bad habit of never meeting government expectations.

By June 2025, we just had 29% of the capacity we hoped for. That number, too, inflates things. Most of our new capacity was concentrated in the easiest link of the chain, in making modules . When it came to the harder, more capital intensive parts, we were doing worse. We only have 14% of the polysilicon capacity we hoped for. Similarly, we can only make 10% of the wafers we set out to.

Of everyone that was inducted into the scheme, only two — Tata Power and First Solar — have fully commissioned their awarded capacities. Meanwhile, at the other end, even established manufacturers like Waaree have operationalised none of what they planned.

Something had gone wrong.

Growing under China’s shadow

There’s an uncomfortable truth to the solar industry — any domestic solar industry, today, has to grow under the shadow of China’s monumental presence. It’s hard to overstate how dominant they are. 80% of the world’s polysilicon is made there. As are 95% of its wafers, and 85% of cells.

If you’re competing against giants, you have zero room for error.

Our dependence on China is complete . Indian solar manufacturing plants import most of their inputs from China, from key components like polysilicon, ingots and wafers, to smaller, more ancillary components, like glass or insulation sheets. When we set up factories, the manufacturing equipment comes from China. We need Chinese engineers to install and commission them, and we need Chinese technicians to teach us how to use them. If anything breaks, the spare parts come from China.

And China is many things, but it is not a reliable trade partner.

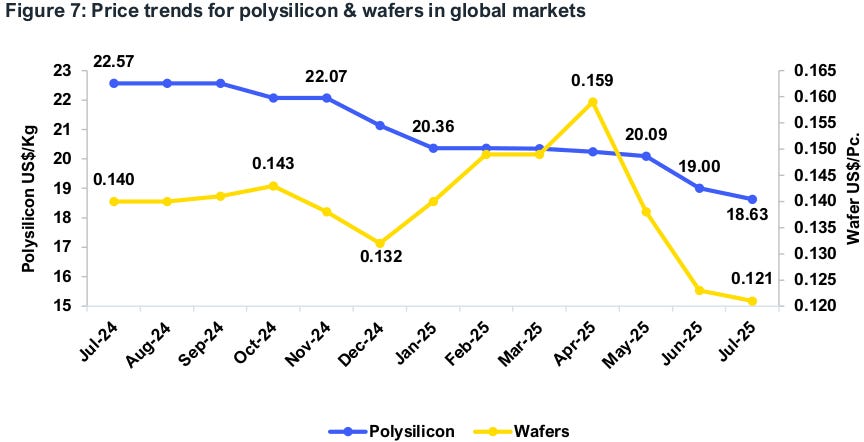

When China makes policy decisions — from rebates and subsidies, to industrial cycles — Indian manufacturers have to absorb all the downstream price and supply shocks. In November 2024, for instance, China reduced export tax rebates on its solar products, from 13% to 9%. Within weeks, Indian manufacturers that imported Chinese wafers suddenly saw their costs spike, from $0.132 per piece to $0.159. That was a sudden 20% jump in their raw material costs.

Or more recently, in China’s “involution” wave, the prices of solar cells cratered. From $0.12 per watt-peak in March 2023, they had quartered , to $0.03 by FY25. If you planned to make cells, in that moment, your calculations would be worthless by the time your factory was up.

How, then, do you plan multi-year, thousand-crore investments?

In an ideal world, we would combat the uncertainty with fast, responsive policy. But we’ve fallen short, in many ways.

To compete against China, you need Chinese scale. Take polysilicon, for instance. It’s only economically viable to make it if you’re pushing out more than 40,000 tonnes per year. Leading Chinese manufacturers operate at 100,000+ tonnes. However, the maximum allocation under the PLI only translates to 25,000 tonnes per year. If you were relying on government subsidies to break into a horribly difficult industry, you wouldn’t even get to the minimum viable size. This is perhaps why low-capital module assembly is the only space we’ve truly made headway in.

We’ve tried blocking Chinese imports in the past, through the “Approved List of Models and Manufacturers”, or ALMM. If you want to sell to government-backed solar projects in India — the biggest there are — you have to get onto this list. In theory, this gave a massive advantage to Indian manufacturers. Except, right as the second tranche of companies were being inducted into the PLI, we suspended the program for a year. Anyone that made their bids assuming protection suddenly found cheap imports flooding in. The economics of investing in a new plant instantly stopped making sense.

Ideally, as PLI awardees would set up their plants, a range of raw material suppliers would mushroom around them. This is perhaps the idea with which the scheme was designed, because it contained strong “local value addition ” requirements. In the first year, 68% of one’s products’ value had to originate in India, which would grow to 90% by year five. Only, with all this uncertainty, a local ecosystem failed to appear. There’s no way manufacturers can hit those targets.

There’s a long list of such issues. And collectively, they have held our solar ambitions back.

The cost of getting it wrong

At its heart, the solar manufacturing PLI came with two promises: one, it would catalyse massive investments and create lakhs of jobs; and two, it would make green electricity dramatically cheaper. Neither has come true yet.

We once expected the schemes to bring in ₹94,000 crore in investment — that is, every taxpayer Rupee spent would bring in three more from the private sector. Instead, we got half as much. Similarly, instead of the promised two lakh jobs, the program only created 38,500 — barely 20% of what we hoped.

Meanwhile, solar power prices have barely fallen. Back in FY 2021, solar tariffs hit record lows of ₹ 2–2.2 per kilowatt-hour. Even though component prices have fallen drastically since, they’re higher today, sitting at ₹2.5–2.7 per kilowatt-hour.

And now, the industry is only heading into harder times. A big source of revenue for the industry, until recently, was the United States. The country had blocked solar imports from China, giving our industry a massive advantage. In fact, as much as 97% of our exports went there. But Trump’s 50% tariffs on India have effectively shut that route down, by creating a massive relative advantage for rivals like Vietnam. That was roughly 3.5–4 gigawatts of capacity that no longer has an outlet. Some fear that the resulting slump could cause severe over-capacity within India.

Where do we go now?

This is a wicked problem to solve. Even the government is aware of this — it is now working hard to plug the industry’s many holes, from expanding the ALMM list upstream, to extending PLI timelines.

But if this were a matter of poor policy design alone, fixing things would not be so hard. The harder task ahead of us is to grow out of China’s shadow . That won’t happen anytime soon. For the foreseeable future, we still rely on them for everything from equipment, to raw materials, to expertise. Industrial policy, no matter how well designed, cannot wish economic realities away.

The challenge, now, is to find a structural answer: either find enough scale to actually put up a fight, somehow, or give up on our dreams of complete self-reliance and find niches where we can actually compete.

Tidbits

-

India, UAE ink a comprehensive set of agreements, targeting $200 billion trade by 2032. The headline agreement is a 10-year LNG supply deal worth $3 billion starting 2028, which would make India the UAE’s largest LNG customer. The two sides also signed a letter of intent for a strategic defence partnership. Previously, India and the UAE had forged strong ties with a trade deal in 2022.

2.Source:* CNBC -

Government removes QCO on textile machinery imports The Centre has withdrawn the Quality Control Order on textile machinery — a major relief for an industry that imports 50-100% of its high-speed looms and embroidery machines. The move follows the rescinding of QCOs on polyester, viscose, and other raw materials late last year. Source: The Hindu

-

The IMF upgraded India’s growth projection by 70 basis points to 7.3% for FY26, citing stronger-than-expected Q3 performance and sustained momentum. However, it expects growth to moderate to 6.4% in FY27 and FY28 as cyclical tailwinds fade. Inflation is expected to return near target levels after a sharp decline in 2025.

4.Source:* Reuters

- This edition of the newsletter was written by Manie and Pranav.

Tired of trying to predict the next miracle? Just track the market cheaply instead.

It isn’t our style to use this newsletter to sell you on something, but we’re going to make an exception; this just makes sense.

Many people ask us how to start their investment journey. Perhaps the easiest, most sensible way of doing so is to invest in low-cost index mutual funds. These aren’t meant to perform magic, but that’s the point. They just follow the market’s trajectory as cheaply and cleanly as possible. You get to partake in the market’s growth without paying through your nose in fees. That’s as good a deal as you’ll get.

Curious? Head on over to Coin by Zerodha to start investing. And if you don’t know where to put your money, we’re making it easy with simple-to-understand index funds from our own AMC.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()