Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened; we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- India’s batteries are getting longer, not just bigger

- The patient investor runs out of patience

India’s batteries are getting longer, not just bigger

Between May and December last year, India let 2.3 terawatt-hours of solar electricity go to waste because the grid had nowhere to put it. Nearly 40% of that waste came in October alone, when the sun was strong, demand was soft, and the coal plants underneath the system simply couldn’t ramp down fast enough to make room.

But, you might already be familiar with this story because we’ve talked about the different versions of this problem countless times on The Daily Brief .

The obvious response is to build storage, and India has been trying to do that. The country added 4.6 GWh of battery storage in the first three months of 2026, more than nine times what it managed in the previous quarter, taking its cumulative installed base to 5.9 GWh by March. That sounds like a breakthrough until you set it against the target: the Central Electricity Authority reckons India will need 236 GWh of batteries by 2031-32. We have built, in our entire history, a little over 2% of the batteries we expect to reach within seven years.

So the gap is enormous, and you probably already knew that too.

But, the more interesting story is hiding inside the engineering. Because somewhere in the last 18 months, without much fanfare, the kind of battery India buys has changed. The grid has stopped asking “how many megawatts of battery do we need?” and started asking “how many hours of stored sunshine do we need?”

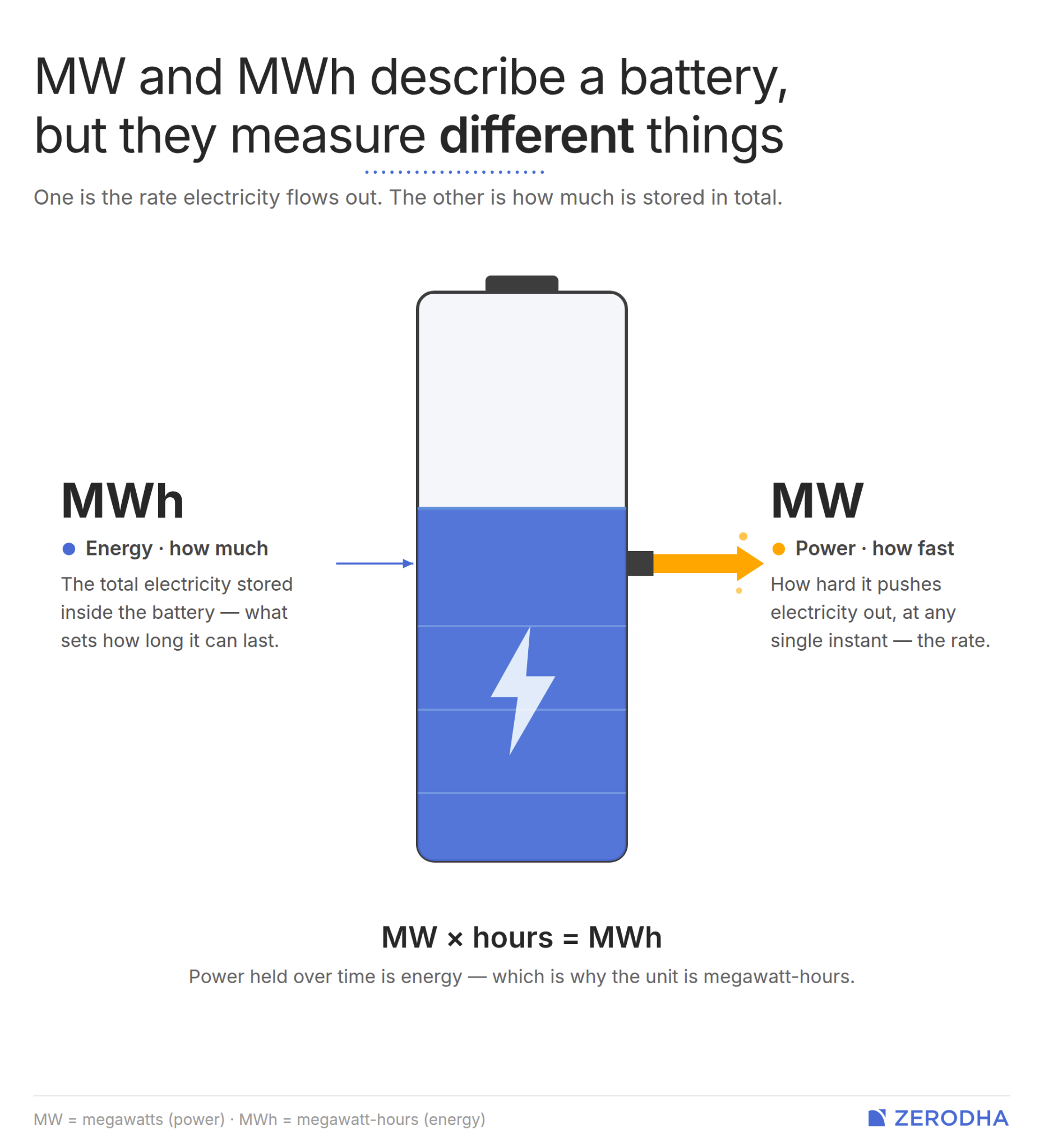

Today, we talk about that shift. To see it, you have to hold two numbers in your head at once.

The first is power, measured in megawatts (MW). It tells you how much electricity the battery can push out at any single instant. The second is energy, measured in megawatt-hours (MWh). It tells you how long it can keep pushing before it empties. Divide the second by the first and you get duration .

For example, a battery rated at 500 MW/1,000 MWh can deliver 500 MW for two hours. The same battery can give 100 MW of power for 10 hours. Give it the same 500 MW of power but 2,000 MWh of energy, and it becomes a four-hour battery.

All the time in the world

When India ran its first serious battery tenders, two hours was enough, but not anymore. And that’s because of the nature of solar power.

See, through the day, the sun is still doing much of the work. Because solar is cheaper than coal power, we buy most of the solar during that time and run coal plants at a minimum rate, so that supply matches demand. This also means that the more we install solar and rely on it during the day, the less coal we need, and the lower we keep those plants running.

But after sunset, solar falls away to nothing within an hour, just as people get home and switch on lights, fans, air conditioners and stoves. Demand climbs at the exact moment the cheapest source of supply disappears. Coal plants are left to fill the gap, but now, they’re running at low utilisation levels, and it’s hard to ramp them up quickly. So for a couple of hours after sunset, the system is stretched.

A two-hour battery solves this problem tidily. It charges through the day, when power is plentiful and cheap, and then empties itself in that evening crunch period. And for the grid India had a few years ago, that was enough. Solar was still small, so the evening crunch was short and shallow, as coal plants were still carrying a lot of the burden in the evenings, leaving only a modest peak. That was the thinking behind SECI’s landmark March 2022 tender: 500 MW for two hours.

But, a two-hour battery was never a complete fix. It was a peak-shaver, only clipping the very tip of the evening and nothing beyond it. If the shortfall ever ran longer than two hours, the battery was already empty. And that did eventually happen.

The more we depend on solar, the longer we need batteries for

Then solar grew, and the problem changed shape. The more we relied on solar, the less we leaned on coal, and the longer the crunch got, which only meant we’d need more and longer batteries.

As solar has crossed 100 GW, the evening peak has stopped being a single spike at all. It’s now an elevated zone, stretching from roughly 5pm to 11pm in winter and 7pm to past midnight in summer. A two-hour battery can only shave the steepest point of that zone, and then it’s empty. A four-hour battery would be more suited to this problem.

This is also why a piece of jargon called FDRE, or “Firm and Dispatchable Renewable Energy”, has started coming up in the energy transition conversation. It is a kind of contract where buyers aren’t just paying for a vague annual quantity of green units. They’re paying for guaranteed power, delivered in specific scheduled hours that match a DISCOM’s demand.

You cannot make that promise with a two-hour battery though; you need a longer-duration battery so that late-evening demand is also met. So every FDRE auction mechanically pulls developers toward four hours and beyond.

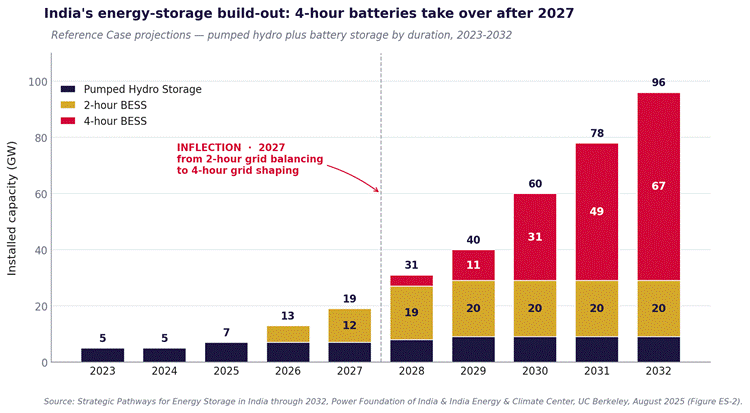

That’s probably why a 2025 study by the Power Foundation of India and UC Berkeley’s energy centre talks about 2027 as the year when four-hour batteries become the dominant design.

Double the storage, same price?

Now, doubling the battery duration would mean that more energy is stored, and hence it should be costlier than before, right? But it costs surprisingly almost the same on paper — and understanding why requires looking into the tender data.

In a government power tender, developers put out their bidding prices at which they can provide a unit of electricity, and the cheapest bid wins. So when a developer wins a solar-plus-storage auction , the headline number is a single tariff cost covering both the panels and the battery. To work out what the storage alone costs, you subtract a reasonable solar-only price — say ₹2.5 per unit — and whatever’s left is the “storage adder “.

Two auctions in 2024 show us what the storage doubling costs. A July 2024 auction paired solar with a two-hour battery and it was awarded at ₹3.41 per unit, which gives us an estimated storage adder of ₹0.81 per unit. A December 2024 auction paired solar with a four-hour battery and cleared at ₹3.52, which implies an adder of about ₹1. Doubling raised the final tariff by barely ₹0.19 a unit .

This cost advantage was partially made possible because of a brutal collapse in battery prices. What also helped was co-locating storage with solar so they share land and grid connections, and the government’s viability gap funding that helped subsidize 43 GWh of projects across two tranches.

But the flat tariff hides two things that don’t show up in the per-unit number.

The first is stress on the developer. A four-hour project at the same power rating holds twice the energy, which means twice the cells, twice the capex, and a longer wait to earn it back. This is why India’s tender pipeline and its actual construction have come unstuck: roughly 130 GWh of projects were awarded in 2025, against barely 9 GWh expected to physically switch on in 2026. Bidders win at very thin tariffs already, then a bigger asset puts them in the red.

The second is the extra demand for cells itself. Every gigawatt of four-hour storage needs twice the volume of cells needed then what’s needed for a two-hour system. This turns the duration shift into a far larger bet on India’s capability to make those cells in-house than the megawatt numbers suggest, just as the country tries to scale its cell capacity from around 13 GW today toward 100 GW by 2027.

Jack of all trades

There’s another reason longer-duration storage is hard to finance, because it doesn’t get rewarded with the revenue it probably can generate.

A battery can, in principle, earn money several different ways at once. It can buy cheap midday power and sell it for higher in the evening. It can sell ancillary services, which are split-second adjustments that keep the grid’s frequency steady. It can also earn money simply for being on standby during the hours the grid is most likely to fall short, whether or not it actually discharges. If you find that odd, don’t, because even coal plants make money this way.

Letting a single battery earn from several of these jobs simultaneously is called revenue stacking. But India mostly doesn’t allow it.

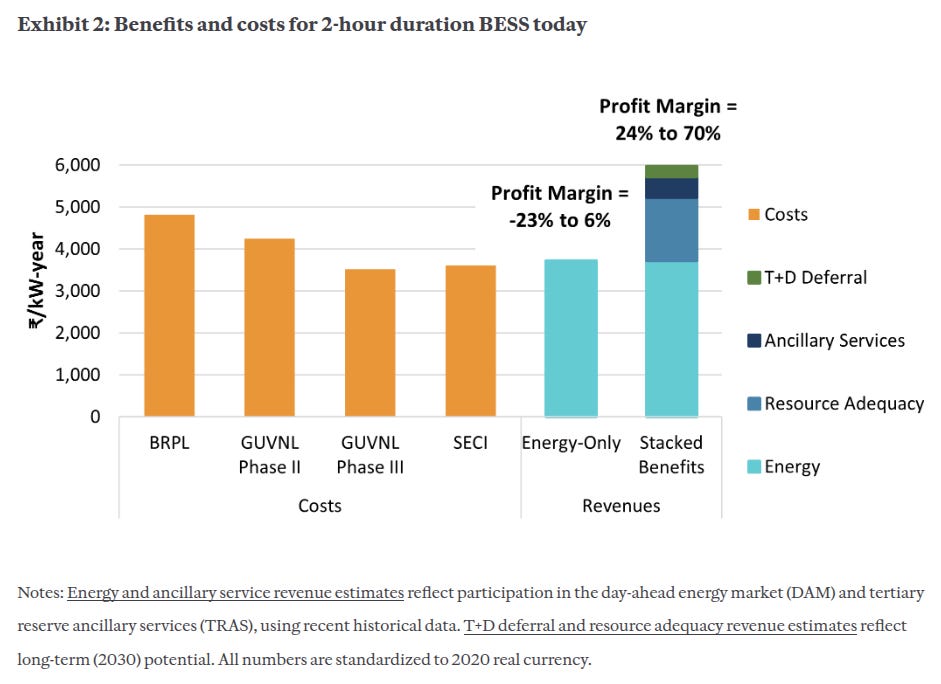

Here, a storage project here typically lives off one income stream: its contract with SECI or a state distribution company. There is no capacity market — no mechanism that pays a battery for standing ready. Time-of-day price differences are thin, so making money through arbitrage isn’t a very viable option. Plus, the intraday gap between cheap and expensive power doesn’t cover costs on its own. So the battery does multiple jobs for the grid, but only gets paid for one of them.

According to an analysis, BESS projects would make 24% to 70% margins if such revenue stacking was made possible, vastly improving the viability of battery projects.

A long journey

Even four hours doesn’t finish the job. It covers the evening, but it still can’t turn the middle of the day into genuine night-time power. As solar’s share of generation keeps climbing, the task becomes shifting bulk energy six, eight, even ten hours forward.

Here, the modelling finds another boundary: lithium-ion batteries stay the cheapest option only out to roughly four to six hours of daily discharge. Beyond that, the economics start to turn, and so does the choice of chemistry. Lithium-ion is the incumbent, and it keeps getting cheaper. But its weakness is structural: power and energy are welded into the same cell, so the only way to add hours is to buy more complete cells. That’s fine at two or four hours, but for more, you end up paying for an enormous stack of cells that discharges slowly, just once a day.

This is where flow batteries get interesting.

In a flow battery, the energy doesn’t sit inside solid cells; it sits in tanks of liquid electrolyte, pumped through a separate stack where the actual electrochemistry takes place. The elegance is that power and energy are pulled apart. The stack sets the power; the tanks set the hours. If you want ten hours instead of four, you can add cheap electrolyte and bigger tanks, while keeping the stack the same size. So the cost of each additional hour keeps falling, which is exactly why flow’s case lives at the long end, and why it does little for you at two or four hours.

But that also means it’ll do little for you in 2-4 hours. At the durations India is actually buying, flow is more expensive and less efficient, and its costs do sit above lithium even at four hours.

Which is why, for now, the whole flow story in India is a handful of pilots: NTPC’s three-MWh vanadium flow unit at its research centre, and a recent tender for a 100 MWh system — much of it built by Delectrik, the country’s only maker of flow batteries at meaningful scale, which our climate fund Rainmatter recently backed.

And that’s the tension underneath all of this. The cheaper lithium gets, the longer a “good enough” four- or six-hour lithium battery delays the jump to true long-duration — so falling prices may not be solving India’s storage problem so much as postponing the harder version of it. India has, at last, started building. The trouble is that the duration its grid needs keeps moving a step ahead of the batteries it’s buying.

The patient investor runs out of patience

American public pension funds, in theory, are the perfect institution for patient capital. They know how much money they’ll have to pay, and when, years in advance. They are the one institution that should never have to sell their assets in a hurry.

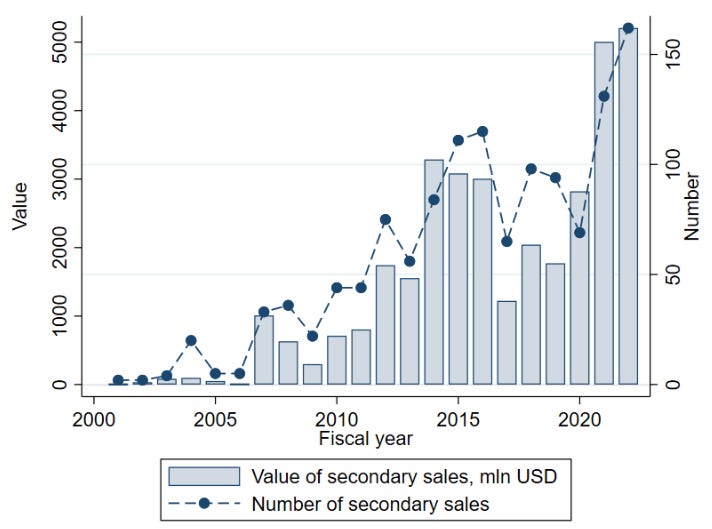

If you didn’t know any better, though, you would think they were caught in a panic. Since 2022, they’ve been off-loading their private equity investments at big discounts, as though there’s a fire sale.

None of those investments had perceptibly failed . They were supposed to be a perfect match for a pension fund’s risk appetite, in fact, structured to create returns for those investors that could hold on indefinitely. But something has punctured that convenient fable. When the economists Abuzov, Andonov, and Lerner studied over a thousand secondary sales of pension funds, they found a visible pattern: somewhere after 2021–22, many pension funds became more likely to sell their PE holdings .

On one level, this was a mathematical reaction. The American stock markets had fallen sharply between 2021-2022. As their public holdings bled value, these funds became far too concentrated in illiquid private markets. So, they brought those allocations down to comfortable levels.

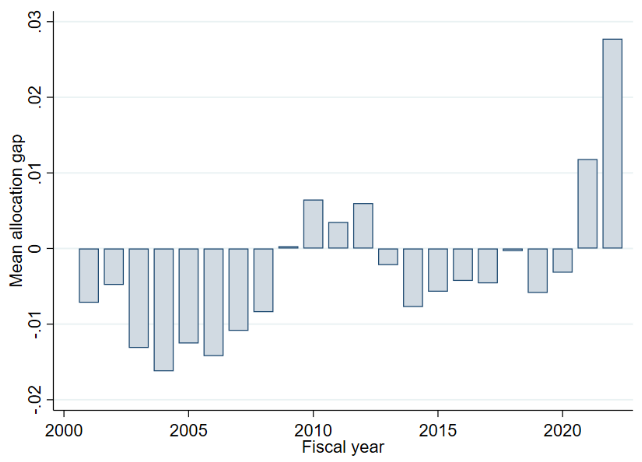

Pension funds overallocated in PE

There’s a deeper story underneath, though. It was a glimpse of a system cannibalising itself. It marked a decades-long drift, where some of the world’s biggest pools of capital — carrying the retirement savings of schoolteachers, firefighters, postal workers and the like — were increasingly drained into illiquid opaque vehicles.

The pledge to pay

The core idea of a pension is simple: workers contribute a chunk of their savings, locking them away for long periods of time. That money is put into long-duration assets. Many years later, when those workers inch closer to retirement, that locked money becomes their income.

There’s a symmetry to the arrangement. Workers need to be paid many years into the future. Long-dated assets beget returns many years into the future. You just need to match the two.

The archetype of this arrangement was the American “defined benefits ” pension plan. These made hard promises to retirees, backed by estimates of what their portfolios could generate. After the second world war, lots of government employees moved to these funds. Together, government-run pension funds now hold nearly $7 trillion in assets . That money has certainly percolated India’s public and private markets as well.

There is, however, a problem: while you can promise a fixed pay-out many decades into the future, generating the money for it is another matter. Markets change their character too fast. It’s hard to squeeze a predictable return out of any instrument for that long.

When bonds were no longer enough

Back in the 1980s, if you were looking for predictable, long-term returns, bonds were great. Government bonds offered sizable returns for almost zero-risk, even briefly paying returns in excess of 15% that decade. In a time like that, U.S. pension funds held close to 40% of their portfolios in bonds and other fixed-income securities.

But then, rates fell sharply, and funds had to turn to riskier securities. Many funds switched to equities and mutual funds instead. This kept things stable for a while, as American markets kept climbing higher between 1982 and 2000. But naturally, this approach was riskier.

This is why, through the 1980s, many companies slowly moved the risk to employees. Instead of guaranteeing defined benefits, they pushed workers into programs like the 401(k), where workers’ fortunes were linked to the market. India has been trying to move from the “old pension scheme ” to the NPS for the same reason.

Public sector unions fought for the old scheme to remain, and prevailed. This was also politically convenient, since it cost a politician nothing to promise a pension scheme whose payments were a future headache.

But where would the money come from?

Risk without reward

While one looked for answers, an accounting hack that kept the ship running.

Pension funds that promise defined benefits essentially fix a figure for how much they have to pay retirees far into the future, and then work backwards from there. That gives them how much cash they had to hold today to get to that number. For these calculations, they set estimates for what they “expect” their portfolio will earn in between.

But critically, you don’t have to account for how much risk you’re taking in your balance sheet . Your books can reflect how much return you expect, without even needing to show the potential downside.

This creates a weird incentive: it turns optimism into an accounting choice. Imagine you had to pay ₹1,000 twenty years from now. If you put your assets into bonds that would definitely yield 3% a year, you would need ₹554 in assets today. If you put it in real estate and private equity, that might probably earn 7% a year, you only need ₹258. Who knows, that downside could never occur, and dealing with that probability is tomorrow’s problem. This could become a problem for you later on, but for today, the riskier option looks better.

Until it wasn’t.

In the year 2000, the dot-com bubble burst. Stocks fell, and many pension funds linked to equities saw a hole blown through their asset base. They were still expected to pay out the same amount in the future, though. If they wanted to fix the equation, it only made sense to, well, be more optimistic about your accounting.

What that meant is that the most rational choice for a fund strategist was to shift to more risk, not less .

There was now a serious case to invest in “alternative assets ”. They came with huge downsides, but crucially, they promised better returns than anything public markets could offer.

The financial collapse

The real lift-off came with the 2008 financial crisis.

On one hand, the crisis destroyed the “funding ratios ” of these pension funds. While their future liabilities stayed in place, equities cratered. Worse still, to deal with the crisis, the government turned on the spending spigot. Risk-free rates stayed near zero for a decade. It paid nothing to lend to the government. Funds were left with fewer assets, and no safe options to plug the gap.

In an ideal world, you would either cut down the benefits you promised, or ask workers to increase the size of their contributions. Both options, however, were politically toxic, especially when the public was already upset with the economy.

The best-looking option a fund had was to create even riskier portfolios, promising even better returns.

As the economists Andonov, Bauer, and Cremers found, by 2010, public pension funds assumed they would earn ~2% more returns, per year, than corporate pension funds that were investing in the same market. Nearly three-fourths of their portfolio was now in risky assets. The more underfunded a pension fund was, the more likely it was to take higher risk.

Simultaneously, the crisis also created more alternative assets their money could go in. Take private credit. As banks turned risk-averse, and slashed their lending to mid-market companies, private credit funds stepped in. These, and others like it, became a new avenue for pension funds to deploy their money, slowly transforming into major markets in their own right.

The turn

As the financial markets clawed their way out of the crisis, public pension funds saw their identity change.

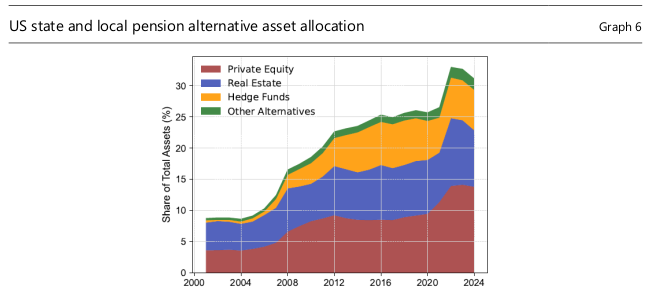

They no longer saw long-dated bonds as the answer to their future liabilities. As Begenau, Liang, and Siriwardane found, by the late 2010s, less than a quarter of their portfolio was invested in fixed-income securities. Their equity allocation, too, had fallen below half. Meanwhile, 30% of their portfolios now sat in alternative assets.

This was, in part, a story of accounting rules, and the risks they permitted.

To be clear, this didn’t actually translate cleanly into better returns. In fact, the returns from PE were comparable to those from the broader public markets. Some funds, even accounting for the extra risk they took on, did offer slightly better returns on average. But much of that difference was eaten up by fees. There was little added advantage to investing in them.

There were some weirder things fuelling this boom. As our boss, Bhuvan, loves to say, so much of finance is a matter of “monkey see, monkey do”. The move to alternatives slowly became a self-perpetuating story. Many fund managers were simply keeping up with industry standards. As Begenau and her co-authors found, every time a pension plan’s peers increased their alternative allocation by 10%, the fund would shift its own allocation up by ~5%.

But arguably, the biggest advantage PE funds came with was their lack of transparency. While public markets had similar returns, they were repriced every second. A fund would constantly have to mark its equity portfolio to the market, and adjust for every drop. This added a lot of volatility.

A private fund stake, on the other hand, would be marked periodically, using models, comparables, and manager judgment. Its actual value was unknowable, but on paper, its value barely moved. That took away most of the volatility. To a pension fund, it was as though they were buying an extremely stable asset with equity-like returns — even if this was just an illusion of how often its price was calculated.

The prestige

Meanwhile, in the background, a pension fund’s worst nightmare was coming true: its contributors were growing older. Every year saw more retirees drawing their money out, while fewer workers contributed to its coffers.

As the economists Andonov, Jansen, and Rauh found, by 2023, the average public pension fund had turned net cash negative . Each year, they now bled out roughly 2.4% of their assets.

Outflows like this have to be met with liquid cash . Paper holdings and notional returns can’t suffice. But by now, public pension funds had thin cash buffers. Cash, treasuries and other liquid securities made up just 9% of their holdings. The rest of their assets would take time to liquidate, and moreover, their sale could end up being negotiated to a discount .

Back when funds studiously matched the duration of their assets and liabilities, they could afford to be patient. They could afford the illiquidity premium on some assets, given just how long they were invested for. But by now, they had structurally morphed into something else. They were now structurally cash-hungry institutions, paying out more than they received.

This was how things looked when, after COVID-19, stocks and bonds fell together. The opaque private markets, on the other hand, hadn’t updated their valuations for the fall. As everything else dropped in value, mathematically, their private market exposure looked exaggeratedly large. The sell-off was a release valve, meant to release pressure off a system already at the brink.

While that may have soothed immediate pressures, though, the structural problem remains.

The world’s biggest pools of capital are underfunded, a fact that is hidden under opaque assets that hide the extent of the problem. According to some estimates, these funds are $4.6 trillion short of what they’ve committed to pay, if you account for it all properly.

When their payments come due, chances are, they wouldn’t liquidate these opaque assets. The risk will shift, instead, to wider markets, which have assets that are easier to unload. There, those losses will land on the portfolio of everyone.

This assumes that private markets themselves don’t see a violent turn. As we’ve discussed before, that is a live risk, which could puncture the books of public pension funds. The effects of that could branch out to everything those giant pools of capital have touched, including your own portfolio.

None of this comes from an individual act of carelessness. It has many roots: labour rights, declining populations, accounting rules, financial crises, zero interest rates, professional envy, and more. Collectively, though, they’ve created the ultimate irony: institutions built to hold safe assets indefinitely have morphed into those that might sell opaque assets in a panic.

Tidbits

- India has extended the bidding deadline for deepwater oil and gas blocks for the sixth time since the round was launched in Feb 2025. The government has extended bidding windows in order to attract foreign investors. The Strait of Hormuz crisis has only accelerated the need for domestic oil and gas production.

2.Source:* ET - Moody’s has flagged that India faces a huge credit exposure to water management because of poor infrastructure, groundwater depletion and fragmented governance. We received the highest, riskiest rating of 5 on the same from the agency. We also received a physical climate risk category of 4, reflecting heat stress and volatile monsoons.

4.Source:* BS - Hindustan Zinc has signed an MoU with Advantek Associates and Aero Eagle Automobiles to explore the use of hydrogen fuel in underground mining applications. By its own admission, it is the first company to do so. This is part of a larger decarbonization strategy on the company’s part to reach net zero by 2050.

6.Source:* ET

- This edition of the newsletter was written by Kashish & Pranav.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Subtext by Zerodha

Subtext by ZerodhaBrad Setser on the dollar and the world’s trade imbalance

The role of the dollar, and its influence on global trade, is a complicated story that has constantly changed over time. To make sense of all this, we spoke to Brad Setser, Most of Twitter knows Brad is one of the sharpest voices on all things balance-of-payments. He is a senior fellow at the Council on Foreign Relations. He also served at the US Treasury and the National Economic Council.

We recorded this conversation while the Iran war was unfolding and oil markets were watching the Strait of Hormuz, and not long after Trump and Xi had met in Beijing to negotiate a trade deal. We used the moment to ask him about the things he thinks about most: why the dollar is really strong, what an AI bust would do to it, how the manufacturing surpluses of China, Korea, and Taiwan quietly finance the American deficit, and what China would have to do to rebalance.

Watch the full podcast episode below, where Brad breaks down the sources of dollar demand and the future of global trade imbalances

You can also listen to the full conversation on Spotify and Apple Podcasts. The full transcript of the podcast is below if you prefer to read.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()