Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Why did IndusInd fall more than 25%?

- Hyundai India Under the Scanner

Why did IndusInd fall more than 25%?

See, in banking, or really anything that’s related to finance, trust is everything . It’s the product you sell, in a sense. You don’t deposit money in a bank because they have some superior way of storing money; you do it because you trust that your money will be safe. Investors buy bank stocks for the same reason — they believe the numbers on the balance sheet are accurate. And that’s why, when a bank suddenly says, “Oops, we found an accounting issue,” the market doesn’t take it lightly.

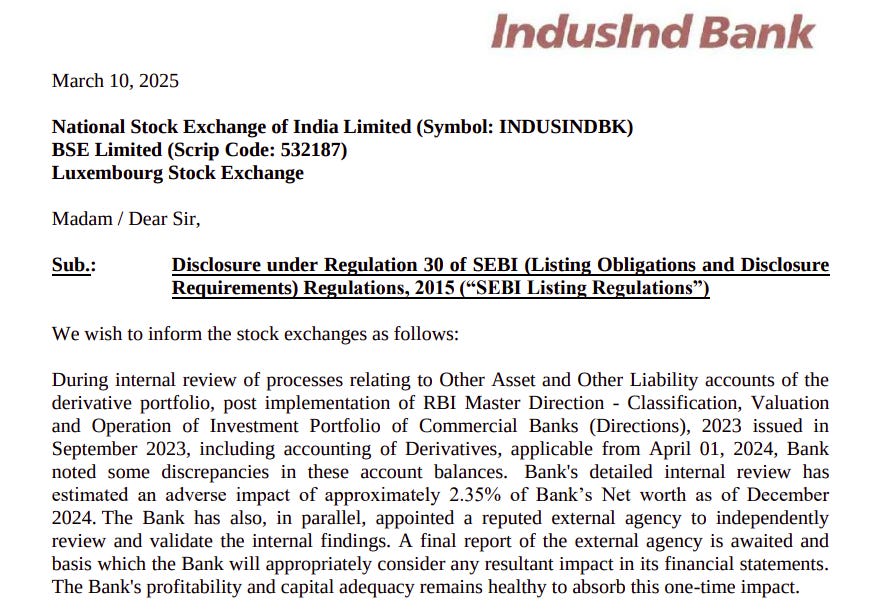

That’s exactly what recently happened to IndusInd Bank — India’s fifth largest bank. A problem with how the bank accounted for certain derivative transactions has forced it to take a hit of roughly 2.35% to its net worth. In rupee terms, that means that overnight, around ₹1,500–2,000 crore of shareholder value simply disappeared from its books.

Source: IndusInd Bank’s Disclosure

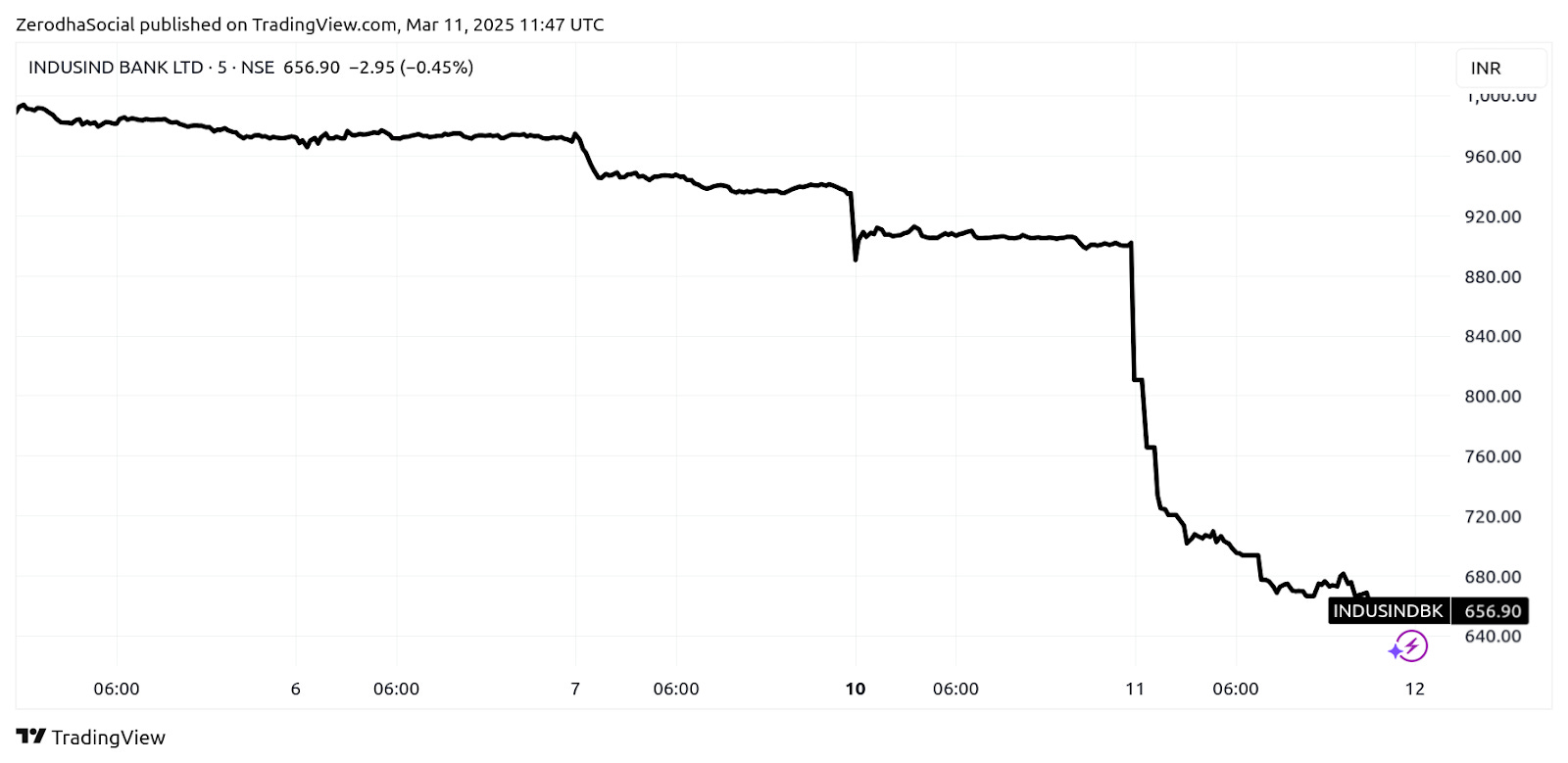

The moment this news hit, IndusInd’s stock collapsed by ~25%.

Now, as far as we can see, the bank isn’t in danger of going under. But the problem is simple: if a bank miscounted something as fundamental as its derivatives exposure for years, how do we know it hasn’t miscounted something else? That’s possibly why investors panicked.

Making matters worse, IndusInd Bank’s CEO, Sumant Kathpalia, was up for reappointment right about now. The board wanted him to stay for three more years. The RBI gave him only one. It’s hard not to see a connection. While the regulator didn’t outright say, “We don’t fully trust you,” with a one-year extension instead of the standard three, it seems like the RBI is hedging its bets.

Put all of this together, and IndusInd suddenly looks like a bank that’s stable on paper but that has just lost the trust of both regulators and the market. So, what exactly happened? What was this accounting mistake? And is IndusInd actually in trouble?

Here’s our best take on what’s going on. Now, before we dive deeper into this, FYI: this story is still unfolding. We’ve already edited it a bunch of times to keep up with the news that’s come in. We’re sharing what we know so far based on what’s publicly available. As more details emerge, things might look very different.

Banks are traders too

Let’s start with the basic question: What is a derivative, and why was IndusInd using them?

Just like you and us, banks trade, too. They have ‘proprietary trading desks,’ or ‘prop desks,’ where they trade using their own money. Banks have various reasons for trading—some prudent, like hedging risks, and others purely speculative, aiming to profit from market movements.

According to reports, this entire controversy came up around forex derivative and swap transactions that IndusInd’s prop desk was engaged in, which were meant to hedge their forex deposits and debt. The CEO & MD, Sumant, in the aftermath of this whole thing, in an interview with CNBC TV18, said that there was a mismatch between its “internal desk” and “external desk”.

All of this might seem unintelligible. So, let us simplify what it means.

Basically, IndusInd held a lot of money in foreign currency. It also seems to have taken loans from abroad. This creates a massive risk for a bank. Imagine, for instance, that the Rupee strengthens against international currencies. Suddenly, the value of those foreign deposits might drop. Similarly, if the Rupee falls in value, its foreign debts might suddenly become a lot more expensive to pay back. All of this adds additional headaches for a bank. Running a business in one currency is hard enough — but the complexity only multiplies if you’re also dealing with exchange rates you have no control over. And so, banks like stability.

From what we can tell, IndusInd was trying to gain that stability — by using currency derivatives and swaps. In simple terms, these contracts would let the bank lock-in a certain exchange rate for the future. Whatever might happen next, this would let them operate with some foreseeability instead of simply crossing their fingers and hoping for good exchange rates.

The big mis-match

Now, IndusInd’s problem wasn’t that it used derivatives. The problem was this: When you’re using derivatives and other such instruments, you sometimes gain money and sometimes lose it. Only, the bank wasn’t accounting for both in the same way.

How did this happen? Basically, there were two levels at which IndusInd was hedging its forex risk: inside the bank and outside the bank.

As per the bank’s CEO, the bank had an “internal desk” for hedging its own foreign currency borrowings and deposits. Here, different departments of the bank would contract with each other to manage each of their forex risks — presumably at internal rates rather than the market rate. This internal desk followed “hedge accounting”, where it could spread gains and losses gradually.

Here, for years — five to seven years, in fact — the bank did something odd. Often, when the bank had notional, mark-to-market gains, it promptly booked those gains. On the other hand, a lot of the money that it notionally lost was parked with its “other liabilities ” — where it would get lost amongst a lot of other short-term payments it was due to make. So basically, any gains from prop trading looked like income, but it dressed losses up so that they didn’t look like lost money.

Meanwhile, it also had an “external desk,” which dealt with trades it was making outside the bank. Here, it used a daily mark-to-market approach, where it was updating values in real time.

Because each desk booked derivative results differently, somewhere, a mismatch started to happen. While its external operations were reported accurately, there were issues in its internal operations. Essentially, the bank began over-reporting some profits but under-reporting certain offsetting losses. This created a growing gap that went unnoticed.

The RBI spoils the party

At first, this might not have mattered. These mismatches weren’t visible from the bank’s accounts, and the bank kept running as usual. The bank could have smoothened the losses in its “other liabilities” over several quarters — by recognising them over months. Instead of one large number, the bank may have shown minor trading losses over the span of years — which people may have considered trivial.

But then, the RBI came in its way. In April 2024, the RBI implemented new rules for how banks must classify and value these derivative contracts. This forced banks to mark all their gains and losses to market rates every day. It also banned internal hedging contracts — now, if banks wanted to hedge foreign exposure, they would have to go to the markets. Suddenly, banks lost the freedom in how they could recognise their trading profits and losses. IndusInd, like every bank, had to reassess its books under the new framework.

And when it did, it realized the problem: there were major mismatches in how the bank’s internal derivatives transactions had been reported all along. When those were corrected, the bank’s net worth was suddenly 2.35% lower than previously reported.

Why did we just find out all this?

The moment IndusInd applied the new standards, the mismatch became obvious. But why are we learning of it now — in March 2025 — rather than in April of last year, when RBI’s regulations kicked into action?

It appears that IndusInd itself stopped its internal hedging in April 2024.

Even after this, however, CEO Sumant Kathpalia said that the bank wasn’t fully confident in how it had been accounting for these internal trades. So, in October 2024, it hired an external agency to verify and validate the bank’s numbers. This review took several months, and by early 2025, IndusInd concluded that its net worth was overstated by about ₹1,500–2,000 crore.

That’s a huge number. This isn’t necessarily a liquidity crisis, but it does mean that for years, IndusInd’s books looked better than they actually were.

According to him, as soon as a number value was available, it was disclosed to the board. And immediately thereafter, they also informed the stock exchanges.

How will they perform this quarter?

Incidentally, that 2.35% figure of how much the bank’s net worth might fall is in itself an estimate. IndusInd’s final numbers will depend on what the external review finally says.

IndusInd Bank says it plans to absorb the entire discrepancy in its derivative accounting during 4QFY25, subject to the external agency’s final review. That said, IndusInd is confident that it’ll survive this fiasco. As it said in its stock exchange filing, “The Bank’s profitability and capital adequacy remains healthy to absorb this one-time impact ”.

Despite this planned adjustment, CEO Sumant Kathpalia maintains that the bank will remain profitable this quarter and even over the full fiscal year will end in positive territory. He adds that capital adequacy will stay above 15%, even after factoring in the one-time impact.

Meanwhile, Ashok Hinduja, Chairman of IndusInd International Holding, a key promoter entity, characterized the ₹1,600 crore impact as relatively small in the grand scheme of the bank’s financials. He emphasized that no margin calls have been triggered on the promoters’ pledged shares and reaffirmed that the promoters’ pockets are “very strong.” Hinduja further reiterated that promoters stand ready to infuse more capital should the need arise.

If this is all true, IndusInd will get over this fiasco. But honestly, the question now isn’t whether IndusInd survives this. The real question is how long it takes to restore trust. And that, as always in finance, is the hardest thing to earn back.

Hyundai India Under the Scanner

You can flip through any classic investing book or listen to lectures from the smartest professors—there’s one thing everyone agrees on: Corporate governance matters. And not just a little bit; it’s often make-or-break for a company.

Countless studies across different markets and eras have consistently linked strong corporate governance with better shareholder returns. Even here in India, academics have repeatedly shown that companies with good governance typically treat their investors better. This is especially true of listed companies. When shareholders don’t get to see how the companies they own are run, there’s no guarantee that their interests will be protected. There’s every chance that someone takes advantage of them not being around.

Honestly, you don’t need fancy studies to tell you that—especially here. India’s investing history is littered with horror stories of corporate governance gone wrong. It could be outright fraud, like cooking the books, or something sneakier, like quietly moving money around to benefit insiders.

Either way, minority shareholders like you and us end up paying the price.

But why are we talking about this today? Hyundai is currently facing the heat for a series of ₹31,526 crore worth of Related Party Transactions, because of which it’s being alleged of suspicious activity.

What’s up with Hyundai?

Hyundai is one of India’s largest auto manufacturers. Naturally, they buy and sell tons of parts to build their cars. But here’s something interesting: a big chunk of these transactions happens within Hyundai’s own global family. In fact, ~40% of their business involves other Hyundai group companies, most of them directly controlled by Hyundai’s global parent.

A ‘Related Party Transaction (RPT)’ is when a company does business with entities it already has close ties with — either through ownership, management, or control.

Now, RPTs aren’t automatically bad. Sometimes, they make sense — for instance, you might only trust companies from your own group if you’re sourcing specialized components and want them to work perfectly.

But things can get tricky. Consider these cases:

- The pricing is not fair — for example, if Hyundai India is overpaying its related parties. This could increase the expenses of the Indian entity and reduce profits while benefiting its related parties.

- The profit of the Indian unit is being shifted to these related entities, which may be based in tax havens.

- The deals do not go through competitive bidding or any other such transparent process. There’s no way to verify if Hyundai India is getting the best value for money — you just have to take their word for it.

Source: Business Standard

Now, we don’t actually know what’s happening. But investors are worried that we could actually be seeing something problematic like this play out. If Hyundai India’s profits are artificially being lowered, the returns for investors here shrink, while the global parent might be quietly benefiting. Add in a lack of transparency, and suddenly, investors have every right to wonder what’s really happening behind the scenes.

Now, here’s the catch: SEBI rules say companies can’t just slip these big related-party deals through quietly—they need shareholder approval first. And that’s exactly how Hyundai’s tricky situation came into the spotlight. One of the proxy advisory firms thinks that Hyundai is in the wrong here.

Enter Proxy Advisory firms

So, we know shareholders get a say when companies do big related-party deals. But what if you’re an investor holding many dozens of stocks? Imagine trying to closely track annual meetings and voting on resolutions for, say, 40 different companies—won’t you be exhausted? You’d have to analyze reams of reports, resolutions, and financial data related to every single company to make informed voting decisions. If you manage a portfolio of something like 40 different stocks, this voting becomes a full-time job.

In the US, they even have a term for this hectic period—“proxy season”—between mid-April and mid-June. It’s when most big publicly traded companies host annual shareholder meetings and vote on important stuff.

This can even be a problem for big institutions: Imagine you’re a mutual fund manager with multiple portfolios—it’s literally impossible to do it alone. And things get even trickier if you manage a passive fund. The whole point of passive investing is that you don’t actively pick stocks or manage the portfolio. But thanks to SEBI, even passive fund managers have to vote during these meetings.

Clearly, investors can’t handle this alone—they need some help. Enter proxy advisory firms.

Proxy advisory firms are independent research groups that sift through dense financial documents and corporate resolutions, providing clear recommendations on how investors should vote.

In India, there are three main players in this space:

- Institutional Investor Advisory Services (IiAS)

- InGovern Research Services

- Stakeholder Empowerment Services (SES)

And that brings us back to Hyundai.

SES has flagged Hyundai’s related-party transactions as potentially problematic. Their concern? Many of Hyundai Motor India’s related entities rely almost entirely on business from Hyundai itself. This dependence raises questions, as SES pointed out, about whether these transactions are structured in the best interests of all shareholders or if they benefit promoter-linked entities.

SES believes these transactions aren’t in shareholders’ best interests and recommended voting against them. Interestingly, another advisory firm, IiAS, saw it differently and voted in favour of all seven resolutions. So, the jury’s clearly still out.

What are proxy firms, really?

But let’s talk more about these proxy firms for a second.

Proxy advisors hold serious power. When they speak, companies—and investors—pay close attention. Their recommendations can genuinely sway important corporate decisions. For instance, back in 2018, based on the proxy firm recommendations, foreign investors opposed the appointment of Deepak Parekh as the non-executive chairman of HDFC.

So yeah, proxy advisors have significant influence, but their differences of opinion can lead to serious friction. As a result, SEBI has stepped in with clearer rules around how companies can address grievances related to proxy advice. In India, their emergence has paralleled the growth of institutional investments, leading to increased shareholder activism and improved governance standards.

It’s a fascinating and underappreciated part of capital markets—one that deserves way more attention. But for now, let’s keep things simple.

Here’s why proxy advisors matter: Their presence encourages more retail investors to participate in corporate voting, helping markets become truly inclusive.

As for Hyundai? Well, we’ll only know the outcome of those controversial transactions once voting wraps up on March 17. But whichever way it swings, one thing’s for sure—the impact of proxy advisors is underrated.

Tidbits

- India’s Edible Oil Imports Hit 4-Year Low, Stocks Drop to 3-Year Low

Source: Reuters

India’s edible oil imports in February 2025 fell to 899,565 metric tons, the lowest in four years, driven by a 36% decline in soyoil imports to 283,737 tons and a 20.8% drop in sunflower oil imports to 228,275 tons, according to the Solvent Extractors’ Association of India (SEA). Palm oil imports, however, rose 35.7% from January to 373,549 tons. The decline in total imports for the second consecutive month has pushed edible oil stocks down 14% to 1.87 million tons, marking the lowest inventory in over three years. Palm oil’s share of India’s total vegetable oil imports fell from 66% a year ago to 43% in the first four months of the current marketing year, which ends in October 2025. With inventories depleting, the industry anticipates increased imports in the coming months, potentially influencing global palm oil prices and U.S. soyoil futures.

- IndusInd Bank Loses ₹190 Billion in Market Value After Accounting Discrepancy

Source: Reuters

IndusInd Bank’s stock plunged 27.2% on Tuesday, marking its steepest decline ever, erasing approximately ₹19,052 crore ($2.18 billion) in market capitalization. The drop followed the lender’s disclosure of discrepancies in derivatives accounting, which resulted in a 2.35% reduction in net worth as of December 2024. Analysts estimate the financial impact to be between ₹1,500-2,000 crore. The issue stems from internal swap trades involving 3/5-year yen and 8/10-year dollar borrowings, which were not marked-to-market due to low liquidity. IndusInd International Holdings, the bank’s promoter, has assured liquidity support if needed, while PwC India has been engaged to review the matter.

- Demat Account Additions Hit 21-Month Low Amid Market Turmoil

Source: Business Standard

New demat account openings dropped to 22.6 Lakhs in February 2025, marking the lowest monthly addition since May 2023 as market volatility dented investor sentiment. The decline comes amid a ₹40 Lakh Cr. market value wipeout, with Nifty 50 falling 6%, Nifty Midcap 100 down 11%, and Nifty Smallcap 100 slipping 13%. Trading activity also saw a slowdown, with cash market ADTV declining 10% MoM to ₹91,661 crore, while derivatives ADTV dropped 2% to ₹188 Lakh Cr. From their peak, ADTV in cash and derivatives segments has declined by 44% and 51%, respectively. The IPO pipeline weakened, with monthly issuances dropping from eight in 2024 to five in 2025, further dampening new investor participation.

- This edition of the newsletter was written by Krishna and Kashish

Have you checked out One Thing We Learned?

Have you checked out One Thing We Learned?

It’s a new side-project by our writing team, and even if we say so ourselves, it’s fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That’s all. It’s chaotic, it’s unpolished - but it’s honest.

So far, we’ve written about everything from India’s state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you’re looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()