Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Bottles and bureaucracy: India’s alcohol business

- When the sun makes electricity free

Bottles and bureaucracy: India’s alcohol business

The alcohol business is a fascinating one. That isn’t because of how it’s manufactured — while connoisseurs care deeply for tiny details like how many barrels you’ve used to age your whisky, when you compare it to the other business we cover here, alcohol is still relatively simple to make. The business is ultimately a play on a handful of basic commodities like barley, neutral spirits, glass and the like.

Everything around the business, however, adds layer after layer of complexity.

Alcohol brands face all the complexities of running a consumer business, but dialled up to an extreme. While all of your customers are looking for a good time, their expectations vary wildly. Your mass-market customers who want the cheapest buzz possible. At the same time, you’re also catering to aspirational drinkers, who seek status and experience with their high.

Add to this the fact that alcohol, unlike most consumer businesses, is deeply political — each state is a market in itself, with its own rules and challenges.

All of this makes India’s liquor market endlessly interesting to watch.

That’s exactly what we’re doing with the latest results from the three big alcohol companies we’re looking at today — United Breweries, United Spirits and Radico Khaitan. Each has a different position in the market. United Breweries is a beer specialist. United Spirits is a hard liquor giant with a vast portfolio. Radico is the insurgent, punching above its weight, while going all-in on premiumisation.

Let’s dive in.

The core numbers

To begin with, let’s take a look at the results of the three companies.

United Spirits , meanwhile, had a steady year. For FY25, its standalone net sales value (NSV) grew 8.6% year-on-year to ₹11,610 crore. That is, by the way, the actual revenue of a company, once you deduct things like discounts. The company’s EBITDA rose faster — going up 20.5% to ₹2,058 crore. All of this translated into a net profit of ₹1,558 crore, up 18.8% since last year.

The company ended the year with a strong fourth quarter. Its standalone NSV grew 11.9% year-on-year to ₹2,983 crore. Its EBITDA grew a solid 39.5% to ₹505 crore, with an EBITDA margin of 17.1% for the quarter, up considerably from 13.6% last year. This translated into a net profit of ₹451 crore.

United Breweries had a steady year, buoyed by its push for premiumisation. For FY25, its net sales were up 10% year-on-year, to ₹8,907 crore. EBITDA rose 14% to ₹875 crore, while net profit went up 8% to ₹441 crore.

In the fourth quarter, United Breweries reported a 9% increase in net sales — reaching ₹2,321 crore. The company’s EBITDA grew 15% to ₹194 crore, and net profit rose 20% to ₹97 crore. The company’s EBITDA margins for the quarter were slightly tight, at 8.4%, but was better than its 7.9% margin from the same quarter last year. Much of the company’s momentum came from its premium sales, which grew 24% year-on-year in the quarter.

Finally, Radico Khaitan had a stellar year. For FY25, its net revenue rose 17.8% year-on-year to ₹4,851 crore. Its EBITDA went up 31.8% from last year, to ₹668 crore, while its net profit went up 35%, to ₹345 crore.

It ended the year with its best ever quarterly showing. It sold more cases than ever before, pushing its net revenue up by 20.9%, year-on-year, to ₹1,304.1 crore. The company also has decent margins — its EBITDA margin for the quarter came in at 13.4%. That pushed its EBITDA up 38.9% year-on-year, to ₹174.5 crore. Ultimately, this translated into a massive 49.6% jump in what it calls its “total comprehensive earnings” — to ₹88.4 crore.

Sale channels

Companies in the liquor business see themselves as a special class of consumer goods companies. We got a fantastic opportunity to see just that in United Spirits’ earnings call. Its MD and CEO, Praveen Someshwar, worked at HT Media — a publishing business — until a few months ago. When asked about the shift to alcohol, here’s what he said:

“Even though I was in publishing, it was very much a consumer business. Overall, I believe this is a consumer product company with a difference. There’s legislation on pricing, route to market, and marketing. Once you embrace that reality, you learn to work with those. At times, it’s a handicap versus other FMCGs, but you build your brands through experientials, and that’s a powerful way of unlocking value. As you build your brands, you tend to build pricing power. ”

All the complications that come with that are present in the liquor business as well. Like companies in the FMCG space, here too, businesses try manufacturing in bulk, and then sell their products through as many channels as possible. Customer loyalty is fickle, and even die-hard customers aren’t guaranteed to keep buying what you sell.

One of the big puzzles to crack, then, is around how you reach customers . Here are just a few examples.

United Breweries, for instance, spends a lot of time thinking about whether it’s selling its beer in cans or bottles. There are states where selling canned beer is the only thing that makes sense. In a state like Rajasthan, for instance, people buy cans and then drink it in their cars, in what’s colloquially called car-o-bar . On the other hand, the classic way of drinking beer is to do so in an establishment where they serve you by the bottle. That’s when drinking beer is a social experience. This is something the company prizes, and wants to preserve.

Beer is also something that you drink cold. But to get cold beer to people, you need to set up fridges wherever beer is sold. So a big capex priority for United Breweries is to triple the amount it spends on fridges, especially in smaller cities.

United Spirits is trying to increase its focus on the “on-premise channel”. That’s a fancy way of saying it wants more of a presence in bars, restaurants, hotels — and all sorts of places where you drink “on-premise,” instead of taking a bottle home.

Why on-premise? Here’s what the company’s management says:

“it is a very, very important channel where you can drive sampling and build habit over a period of time. In terms of consumer spaces, as I call it, it’s a massive connect platform. ”

Apologies for the MBA-speak. But here’s what they mean: if you’re at a bar or a restaurant, you’re more likely to try a brand out for the first time. If you want to buy a full bottle to take home, chances are, you’re going to stick to a brand you trust. But if you’re ordering a single drink, you might be willing to have something new. That’s where a liquor brand can begin building a relationship with you.

These channels get more interesting as you go up in value.

Consider Radico. The company has recently made a major push with its premium brands — like Rampur Whisky or Jaisalmer gin. And so, it’s going around associating them with everything premium. It collaborated with everything from golf tournaments to BMW’s events. It partnered with major five-star hotel chains and high-end clubs. It also managed to place itself on the iconic Palace-on-Wheels luxury train.

Premiumisation

The FMCG-like nature of the liquor business also means that as a liquor company, the brands you sell can do a lot for your business. Most companies sell a range of brands at different price points, each of which is targeted at a different customer cohort. United Breweries, for instance, might sell Kingfisher beer to a wider market, while selling Heineken to its more upscale customers.

There’s a lot of competition at the lower end of the market. Here, people clamour for beverages that get them drunk quickly, for cheap. Cheap whiskies — priced at ₹85-100 dominate — and beat out lighter drinks like beer. Within beers, too, it’s the strong beers that win out. At this price point, brands are playing a volume game, and it’s hard to win too much of the market.

This is why bigger companies want to climb the socio-economic ladder. The more premium your brands are, the higher margins you can command, and the stickier your customers shall be. And so, over time, the single mega-trend we’re seeing in the alcohol business — one that’s visible across the companies we’re looking at today — is a shift towards premiumisation .

The companies we’re looking at are all making such plays. United Breweries, for instance, is betting big on Heineken — hoping to increase it to 7-8% of its portfolio. Radico Khaitan too, is teasing a series of premium offerings:

“The first quarter of FY26 marks an exciting milestone as we prepare to introduce two luxury brands projects that have been under development for two years. These launches represent a major leap in Radico Khaitan’s premiumization journey, reinforcing our confidence that the best is yet to come… Furthermore, within the first half of the year, we will also enter the super-premium whisky segment. "

In fact, Radico hopes to set Indian single malts apart, by creating standards for it through the Indian Single Malt Association. They’re even trying to get a buy-in from the government:

"So, the 4 founding members who are the pioneers and who have been promoting and working hard in creating this category, felt there is a need to set certain standards and norms to protect the authenticity and the goodwill of Indian Single Malt. So, that’s what the main objective is of this. And as we go along, we are in discussion with various Government authorities to set certain specifications and standards for Indian Single Malts, so that everyone conforms to that, and we do not dilute the equity and the brand image of Indian Single Malts in the global market. ”

These companies are even trying to premiumise their recognised mass market brands. United Spirits, for instance, has historically always positioned its McDowell’s brands as a mass offering. But it’s now trying to push the brand up the premiumisation ladder, releasing a new single malt, with the name McDowell’s X.

There’s a new variable that adds a new dimension to the premium end of the business: tariffs . India and the United Kingdom are on the verge of signing a new trade deal. One of the signature changes it brings is that we’re slashing down our duties on whisky and gin from the United Kingdom. A good scotch whisky, for one, will suddenly become significantly cheaper in the world’s biggest whisky market.

This is a big deal for Indian alcohol companies as well — because they don’t just manufacture alcohol, they also import scotch to sell in India. United Spirits, for instance, brings in spirits from Scotland, bottles them in India, and sells them through brands like ‘Black Dog’. That’s a premium business line that’ll suddenly become much cheaper. Sample this from United Spirits’ management:

“The reduction of duties from 150% to 75% will typically lead to a high single-digit reduction in consumer prices. We are of the view that we would want to pass on this benefit completely to the consumer, and therefore, keeping consumer spend constant, it’s reasonable to assume a high single-digit additional volume growth should occur in the BII [Bottled-in-India] portfolio. For the BIO [Bottled-in-Origin, i.e., imported] portfolio, the reduction might be slightly lesser, in the range of 4 to 5%. ”

Radico Khaitan, too, thinks its import prices will soon come down. They, however, want to pocket the margins rather than passing them on to their customers.

The politics of alcohol

Alcohol is a deeply political business. Every state sets its own laws for alcohol sales. And this is a power they exercise frequently. On one hand, states earn thousands of crores in revenue from liquor duties, which pushes them to promote sales. At the same time, alcohol can be a deeply emotional matter for regular voters, creating an incentive to curb sales. Together, both factors practically guarantee political confusion and regulatory pain.

And so, if you’re running a pan-India brand that sells alcohol, you should expect to see a constant tussle with state governments all across the country.

State regulations mean a lot for an alcohol business. Different states have different regulations around everything from where you manufacture liquor, to the taxes you pay, to where you transport it, to where you sell it inside a state. Your distribution and sales channels are all at the mercy of state laws. These regulations basically determine the entire trajectory of a company’s business in that state.

Every state, then, behaves as a completely different market, with its alcohol policy dictating how business happens. Every time you enter a new state, you need a whole new playbook. Here are a few examples:

-

For all of the last quarter, United Breweries did not have permission to manufacture Heineken beer in Karnataka. And that meant it was locked out of lucrative markets like Bengaluru, which would ideally give it a sizable customer base. Those permissions have come in now, however, and from mid-August onwards, that market will be open to it.

-

A few years back, Andhra Pradesh tried to curb alcohol sales in the state through a policy of phased prohibition. For five years, major liquor companies had to sit the market out. Then, late last year, the state came out with a whole new liquor policy. United Spirits rushed back with its “lower prestige” brands like McDowell’s, which added 3% to its growth figures. Similarly, Radico Khaitan’s re-entry to the state added 15% to its growth.

-

Late last quarter, Uttar Pradesh announced a new excise policy, which reformed liquor laws in the state. Before this, stores would either get a license to sell beer, or to sell liquor, but not both. The new policy, however, introduced “composite liquor shops” that could sell both. Suddenly, alcohol companies are seeing the UP market balloon. Radico Khaitan, for instance, noted a sudden increase of 40% in the outlets it could sell through.

-

Earlier this year, Telangana had an ugly spat with United Breweries. The state had set up a government company, TSBCL, which was given a monopoly over liquor wholesale in the state. This allowed it to dictate prices to alcohol companies — and it did exactly that, refusing to increase rates for over five years. It was only when United Breweries cut sales off to the state that it came to the negotiating table. We’ve written about this one before.

These are just a few of the many curious examples we saw from this quarter alone .

This dynamic, of course, adds a heavy pall of regulatory uncertainty over the business. To counter this, liquor brands have been stepping up their work of lobbying governments. United Breweries, for instance, set up the Beer Association of India, a platform it will use to make its case before state governments. As per the company:

“I think we have put a lot of effort in, launching Beer Association of India so that we have a voice as a beer industry, but also connecting with the state governments at various levels, and we’re already seeing some green shoots in the coming quarter as we talk about that. ”

A fascinating place where this uncertainty shows up, at least to us, is during elections. Whenever there’s a state election, there are all sorts of curbs on the liquor business. For instance, companies might be banned from running certain shifts at their factories, or bringing supplies in from another state. This can create sudden shortages, which these companies have no control over.

For example, United Breweries has two breweries in Rajasthan, while the company would bring in additional supplies from other states. During last year’s Lok Sabha elections, however, the state’s borders were shut. In a single month, the company’s market share went down by 10%, as it struggled to meet demand.

The bottomline

The Indian liquor market isn’t a business of constant negotiation. Companies must defend thin margins by anticipating customer tastes, while dealing with a confusing mass of state policy. And somehow, through all this, India’s top alcoholic beverages companies are getting by fairly well. Their main way to navigate this business is a single bet: find a way to capture an upscale market, and the margins will make up for the headache.

When the sun makes electricity free

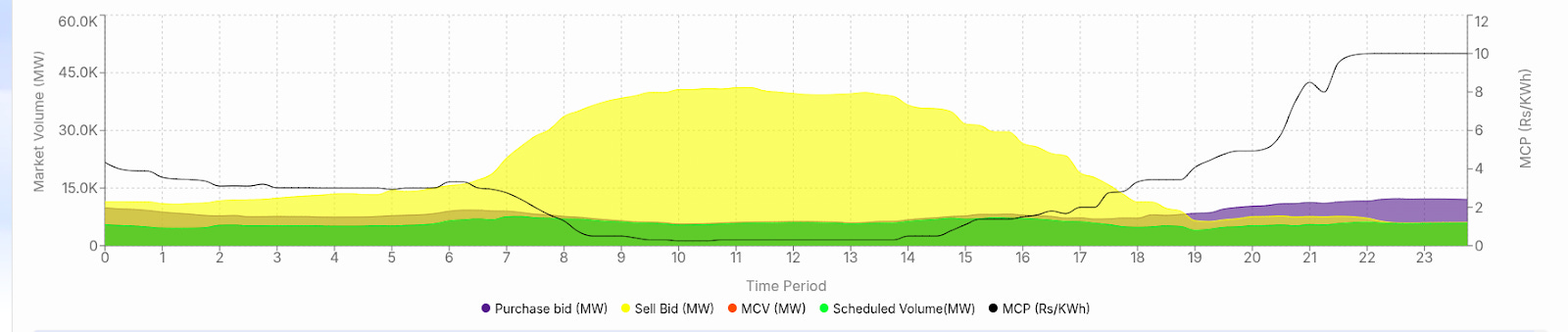

Something remarkable happened in India on May 26, which may have seemed impossible just a few years ago. On a pleasant morning, with gentle rains cooling the air across North and West India, electricity prices on the country’s power exchange crashed to almost zero. Not cheap – practically free .

For several hours between 9 AM and 1 PM, power was trading at practically nothing on the Indian Energy Exchange. The price hit rock bottom at just 11 paise per kilowatt-hour – less than the exchange’s own transaction fee. Generators were basically giving away electricity.

The culprit? India’s solar power boom. Let’s see why.

How electricity prices work

In India, a majority of the electricity comes from long-term contracts, mostly Power Purchase Agreements (PPAs). PPAs are a long-term contract between electricity generators (like coal, solar, or wind power plants) and electricity distribution companies (DISCOMs) that supply power to homes and businesses. Most of these contracts require DISCOMs to pay a fixed price for a fixed amount of electricity whether they actually need it or not, which they then supply to us at prices we see on our electricity bill.

But on top of this, though, there’s also a short-term market. And that works on something a lot closer to classical economic principles.

The short-term market accounts for around 15% of total electricity being consumed. Within that, the spot market — which comprises exchanges like the Indian Energy Exchange or the Power Exchange India Limited — is just around 8%.

But here, something interesting happens. Power plants and independent power producers (IPPs) sell all the excess power they have, while DISCOMs and large industries buy all the extra power they need to cover any shortages from their existing contracts.

While the economics of the power sector is generally convoluted, this operates like a regular marketplace.

Every day, power generators bid to sell electricity on the exchange. The bids are accepted in increasing order by cost — starting with the cheapest bid and moving up to more expensive ones, until there’s enough electricity to meet demand. The final price, called the market clearing price (MCP), is set by the most expensive power source needed that day.

At different times, different sources of power dominate this market. When the sun shines bright, and there’s lots and lots of solar power, solar plants have an inherent advantage due to lower running costs.

And one fine day, there was so much solar power that electricity prices nearly touched zero .

You can see it in the graph below. MCP hits rock bottom from 9 am to 1 pm.

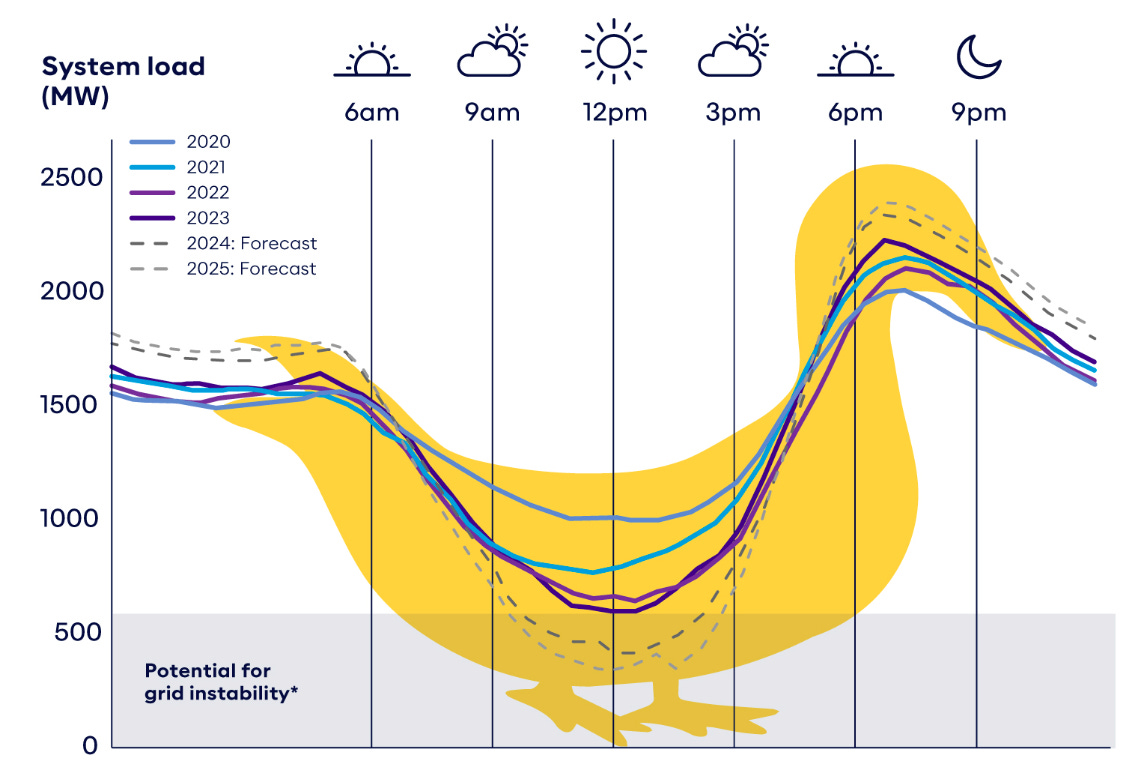

When the sun is blazing at midday, solar panels across India are cranking out massive amounts of electricity. Tens of gigawatts , that is – enough to power entire states. But here’s the thing: people don’t necessarily need the most electricity when the sun is strongest. They need it in the evening — when everyone’s home, turning on lights, air conditioners, television sets and more, while markets and streets all over light up.

This creates what experts call the “duck curve” – a graph that looks like a duck’s back, showing how electricity demand dips during sunny midday hours as solar takes over, then ramps up steeply in the evening when solar fades and everyone comes home.

This phenomenon gives us a classic supply and demand mismatch. There’s a massive supply of cheap solar power flooding the system, right when demand is relatively low during the day. And what happens when we have too much supply of anything? Prices fall!

Grid operators aren’t permitted to cut this excess supply off. India has declared solar and wind power "must-run " – meaning grid operators can’t just turn them off because they’re cheap or there’s too much of them.

So, during those sunny midday hours, all that solar power keeps flowing whether the grid needs it or not. If conventional power plants can’t ramp down fast enough, or if some have to keep running for technical reasons, there’s suddenly way more electricity in the system than anyone actually wants to buy.

Sometimes prices don’t just drop to zero – they can go negative . That is, generators actually pay people to take their electricity. Sounds crazy, but it makes sense when you think about it. Some power plants are so expensive to shut down and restart that they’d rather pay a small amount to keep running than face the massive costs of stopping and starting again. Many renewable energy projects still get subsidies or have long-term contracts that pay them regardless of market prices. A solar farm might get paid ₹3 per unit through its contract, so it can afford to sell excess power for free or even pay ₹1 per unit to get rid of it on the spot market — and still make money overall.

Prices haven’t become negative in India yet , but who knows? We might see that way as well, one of these days.

The battery gap

So you might think, this is great. Free electricity! We get it.

But unfortunately, zero prices are a problem.

-

Solar developers who depend on market revenues and not fixed contracts can’t recover their investments if power is regularly free. So they could go out of business. The more that happens, the worse off consumers will be at the end of the day.

-

Distribution companies lose money when they pay money to solar farms under contract, but can only sell it for pennies on the market. Let’s take a hypothetical example: suppose the state discom pays a solar farm ₹2.50 per unit under a long-term contract, but then has to sell that same power on the exchange for ₹0.10 during surplus hours. The discom basically loses ₹2.40 on every unit — losses that ultimately get passed on to consumers through higher tariffs or government subsidies.

-

Traditional coal and gas plants, meanwhile, are getting squeezed out of the market during midday hours, making it harder for them to recover their costs. In a worst case scenario, these might shut down permanently, which could create problems when we can’t depend on renewables.

-

States with lots of solar generation, like Rajasthan and Gujarat, are seeing more of these zero-price events. But they’re also seeing their electricity export revenues collapse as the value of their daytime power falls. Meanwhile, states that import power are benefiting from cheaper daytime electricity, but they’re becoming more reliant on weather conditions in distant solar-rich states. If it’s cloudy in Rajasthan , states all around might suddenly face higher prices or supply shortages.

So what’s the solution? Simple. Capturing all that free midday solar power and saving it for when people actually need it. On that day in May, when prices crashed to zero, excess solar energy that could have been stored was instead either being wasted — officially “curtailed ” — or sold for practically nothing.

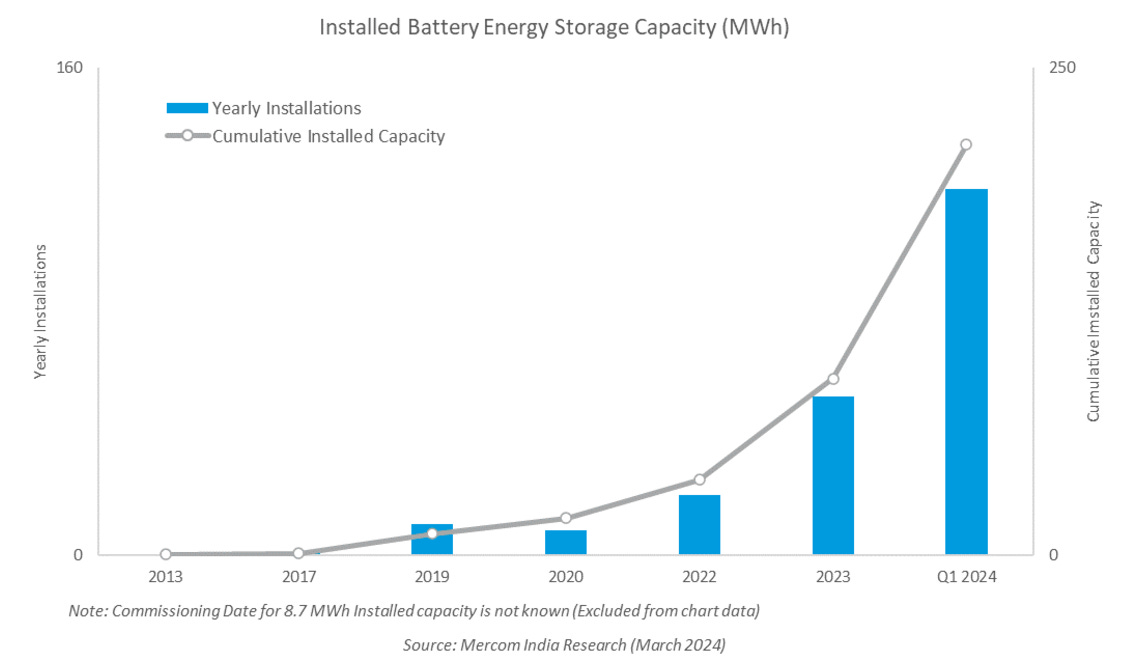

And that’s exactly what batteries do. But here’s the problem: there just aren’t enough batteries. Not even close.

India only had about 220 MWh of installed Battery Storage Capacity as of March 2024. That’s nothing compared to the thousands of megawatts of solar power flooding the grid each day. The government’s own estimates say India needs around 74 GW of energy storage by 2032 to properly handle its renewable energy targets.

The biggest barrier isn’t just technology. It’s economics . Battery systems are still expensive to build, and in India’s price-sensitive market, the business case doesn’t make sense .

This creates a chicken-and-egg problem. Battery developers say they need there to be bigger price differences between cheap and expensive hours, for a project to be viable. China dominates global battery manufacturing. Chinese battery prices have fallen dramatically — by about 90% over the past decade. But even those are still not cheap enough for widespread deployment in India.

There are some alternatives to batteries. There’s pumped hydro storage – you can essentially pump water uphill, to some reservoir, when power is cheap, and let it flow down through turbines when power is expensive. India has about 4.7 GW of pumped hydro and is developing more. But it’s never going to be enough. The brutal reality is that battery storage is the missing link that is holding India’s solar sector back. We’ve written a primer on batteries for some more context.

Beyond batteries, policymakers are trying to make this new reality work:

-

Time-of-Day Pricing: States like Rajasthan are introducing “time-of-day” pricing – making electricity cheaper from noon to 4 PM, to encourage people to use more power when solar is abundant. The idea is to flatten the duck curve by encouraging more midday consumption. But this faces resistance from consumers who are used to flat electricity rates. Many people work during the day and can’t easily shift their electricity use to midday hours.

-

Grid Infrastructure: The government is investing in transmission lines to move surplus solar power from sunny states like Rajasthan and Gujarat to places that need it, rather than letting it go to waste. The Green Energy Corridor projects aim to add over 10,000 circuit-kilometers of transmission lines by 2026. But building transmission lines is slow and expensive and environmental clearances can take years.

-

Market Reforms: Regulators are exploring new market mechanisms, like capacity payments – paying power plants just to be available when needed, regardless of how much electricity they actually produce. This could help keep backup power plants viable even as renewable energy pushes down electricity prices. They’re also looking at introducing more sophisticated pricing mechanisms that better reflect the true cost of electricity at different times and locations.

-

Storage Incentives: The government has announced various schemes to promote battery storage, including viability gap funding and mandates for renewable energy projects to include storage. But progress has been slow due to high costs and unclear regulations.

A global phenomenon

India isn’t the only country that has seen zero-prices.

California saw negative prices roughly 13% of all hours in 2024 in its Southern region, meaning generators were basically paying consumers for every megawatt-hour they produced at that time. In Australia, some states had negative prices about 24-26% of the time in 2024. Germany recorded 475 hours of negative prices in 2024, up from 301 hours the previous year. On one particularly sunny European holiday in May 2025, German prices hit negative €250 per megawatt-hour, while neighboring Belgium saw prices crash to negative €462 per megawatt-hour.

This is happening everywhere that’s gone big on solar and wind. The pattern is always the same: sunny or windy days with mild weather create a perfect storm of high renewable generation and low demand.

The Bottom Line

India is targeting 500 GW of renewable capacity by 2030, more than doubling what it has today. It is ironic — solar power has become so successful that it’s creating a new problem – too much cheap, clean electricity. It’s a good problem to have, but it’s still a problem that needs solving. Basically, the sun is giving us more energy than we know what to do with. The question is: are we smart enough to figure out how to use it?

Tidbits

- India Projects Record Wheat and Rice Output for 2025

Source: Reuters

India is set to produce a record 117.5 million metric tons of wheat in the crop year ending June 2025, surpassing the farm ministry’s earlier estimate of 115.4 million tons. The rise is attributed to farmers expanding cultivation of high-yielding seed varieties in response to higher market prices. In 2024, the country produced 113.3 million tons of wheat. Meanwhile, rice production is also expected to hit a new high at 149 million metric tons, up from 137.8 million tons last year. The combined food grain output is projected to reach 354 million tons, compared to 332.3 million tons in 2024. While the official data signals strong growth, a leading industry body has contested the wheat estimates, suggesting the actual harvest may be 6.25% lower. The government, however, states that current wheat stocks are sufficient to meet domestic needs without imports.

- Bajaj Auto Warns of EV Production Risk Amidst Rare Earth Magnet Delays

Source: Reuters

Bajaj Auto has raised concerns over potential EV production disruptions due to delays in the import of rare earth magnets from China. In its latest earnings call, the company stated that if the issue is not resolved, its EV manufacturing could be impacted by July 2025. The magnets, essential for electric motors, have been held at Chinese ports since April 4, following a change in China’s export policy requiring end-use declarations. Despite India implementing a civilian-use certification system, exports have yet to resume. Executive Director Rakesh Sharma termed the situation a “dark cloud on the horizon,” underscoring its urgency. Bajaj’s EVs, sold under the Chetak brand and through electric three-wheelers, are directly affected. The company had recently posted strong Q4 earnings, aided by exports and forex gains, but prolonged disruption could threaten its EV momentum.

- India’s Defence Production Hits ₹1.46 Trillion in FY25, Exports Reach Record High

Source: Business Standard

India’s defence production touched an all-time high of ₹1.46 trillion in FY25, marking a 15% rise from ₹1.27 trillion in FY24, according to the Ministry of Defence. Defence exports also reached a new peak of ₹24,000 crore, up 14% year-on-year from ₹21,083 crore. The private sector contributed ₹32,000 crore to total defence production, accounting for 22% of the total output, up from 20.8% in the previous year. The Advanced Medium Combat Aircraft (AMCA) project has received approval for a new execution model that allows private companies to co-develop fighter aircraft prototypes alongside public sector entities. Defence Minister Rajnath Singh credited India’s growing indigenous defence capability, particularly during Operation Sindoor in May 2025. He stated that the rising share of domestic production has enhanced India’s strategic response capability. Over the last decade, defence production has more than tripled while exports have grown approximately fortyfold.

- This edition of the newsletter was written by Pranav and Prerana.

Have you checked out One Thing We Learned?

Have you checked out One Thing We Learned?

It’s a new side-project by our writing team, and even if we say so ourselves, it’s fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That’s all. It’s chaotic, it’s unpolished - but it’s honest.

So far, we’ve written about everything from India’s state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you’re looking for a fascinating new rabbit hole to go down!

“What the hell is happening?”

We’ve been thinking a lot about how to make sense of a world that feels increasingly unhinged - where everything seems to be happening at once and our usual frameworks for understanding reality feel completely inadequate. This week, we dove deep into three massive shifts reshaping our world, using what historian Adam Tooze calls “polycrisis” thinking to connect the dots.

Frames for a Fractured Reality - We’re struggling to understand the present not from ignorance, but from poverty of frames - the mental shortcuts we use to make sense of chaos. Historian Adam Tooze’s “polycrisis” concept captures our moment of multiple interlocking crises better than traditional analytical frameworks.

The Hidden Financial System - A $113 trillion FX swap market operates off-balance-sheet, creating systemic risks regulators barely understand. Currency hedging by global insurers has fundamentally changed how financial crises spread worldwide.

AI and Human Identity - We’re facing humanity’s most profound identity crisis as AI matches our cognitive abilities. Using “disruption by default” as a frame, we assume AI reshapes everything rather than living in denial about job displacement that’s already happening.

What the hell is happening?

What the hell is happening?Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()