Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Inside India’s Largest Highway InvIT IPO

- India’s inflation targeting: a work in progress

Inside India’s Largest Highway InvIT IPO

Raajmarg Infra Investment Trust — RIIT — is looking to raise up to ₹6,000 crore from the public. Their proposition, however, is somewhat different from the average IPO: they’re selling investors the right to collect tolls on five operational national highway stretches, across 260 kilometres. It will become only the 7th Infrastructure Investment Trust, or “InvIT”, to ever come to public markets since 2014, when SEBI first opened this path.

Despite the space crossing ₹5-6 lakh crore in assets under management, most investors are still fuzzy on what an InvIT actually is. We thought we’d help give you a sense of things. A few months ago, we broke down how REITs work, using the Knowledge Realty Trust IPO as an example. InvITs are REITs’ less-famous cousins — they have the same trust structure, but instead of office buildings and rent cheques, you’re paying for infrastructure assets and their associated cash flows.

So, this time around, we’ll use RIIT as our running example to understand how an InvIT works, what you’re really buying, and where the risks hide.

What are InvITs?

An InvIT pools investor money to buy income-generating infrastructure assets. Think of it like a mutual fund, but instead of buying into a pool of money that holds stocks, you’re investing in a pool of money that buys infrastructure — highways, power transmission lines, telecom fibre, that sort of thing.

Of course, there are other ways of betting on infrastructure. You can, for instance, buy the shares of an infrastructure company like Larsen & Toubro or IRB Infrastructure. But when you do so, you’re betting on their business . You’re betting on their ability to win contracts, build assets on time from ground up and manage costs, all while making a profit.

When you invest in an InvIT, on the other hand, you’re buying into an already completed and revenue generating asset . The roads are already laid, the power lines already transmit electricity. You’re simply buying the rights to collect the tolls or tariffs on those operational assets. There’s no construction drama here. There’s a predictable cash flow — at least in theory.

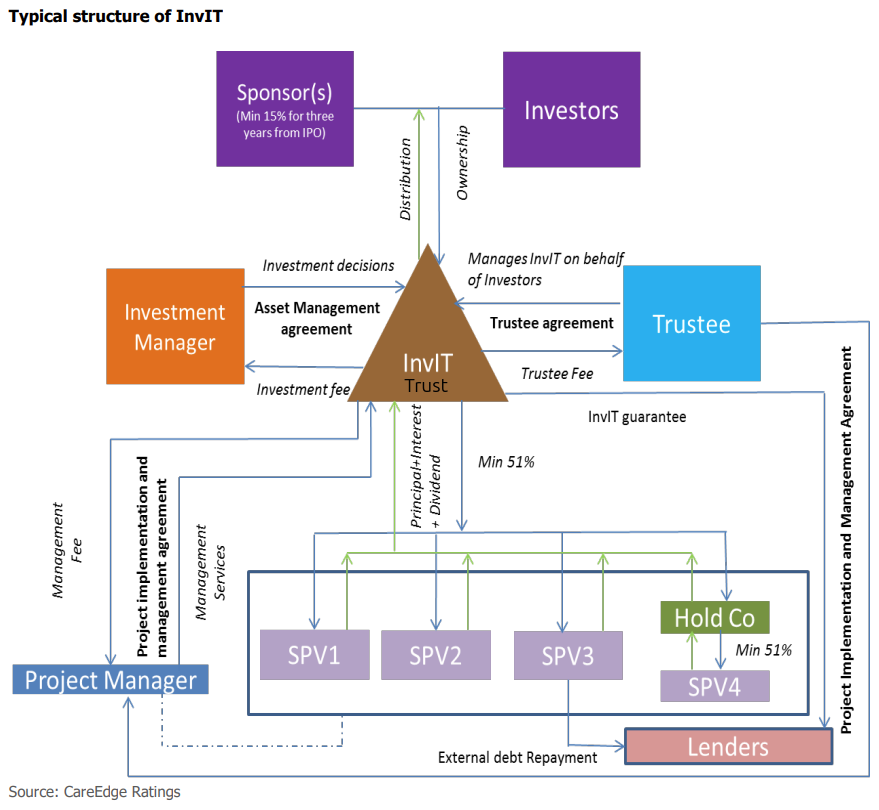

But who are you trusting for your money? Like REITs, InvITs have a cast of characters.

At the centre sits the trust itself: the legal entity you buy “units” in. In our case, it’s Raajmarg Infra Investment Trust.

That trust has a sponsor : the original developer who built the assets, and is transferring them to the trust. For RIIT, that’s NHAI, the National Highways Authority of India, who built these roads in the first place, and now wants to monetise them to free up cash for new projects. This is the whole point of the exercise, from NHAI’s perspective: it wants a lump sum today, in exchange for future toll revenues, so that it can redeploy that money immediately into building more roads, without waiting years for money to trickle in.

But the sponsor doesn’t give the highways directly to the trust. A trust simply is too messy, legally, to hold massive infrastructure assets. It is, largely, a fiduciary arrangement, not a full-fledged business. And you don’t want the InvIT’s many projects, and their liabilities, by extension, to be concentrated in that single entity.

So, the trust creates a Special Purpose Vehicle (SPV) for every single project — this is a company specifically created to hold that project’s agreements and tolling rights. Financially, each SPV is firewalled from all others. It has its own balance sheet, which means the liabilities of one project can’t spill over and infect the rest of the trust.

The trust has a Trustee ; an independent watchdog who looks out for your interests as a unitholder. Its financial brains, meanwhile, are in the hands of an Investment Manager , who manages its money and plots future acquisitions. On the ground, meanwhile, a Project Manager fixes potholes and runs toll plazas for all the assets under SPVs.

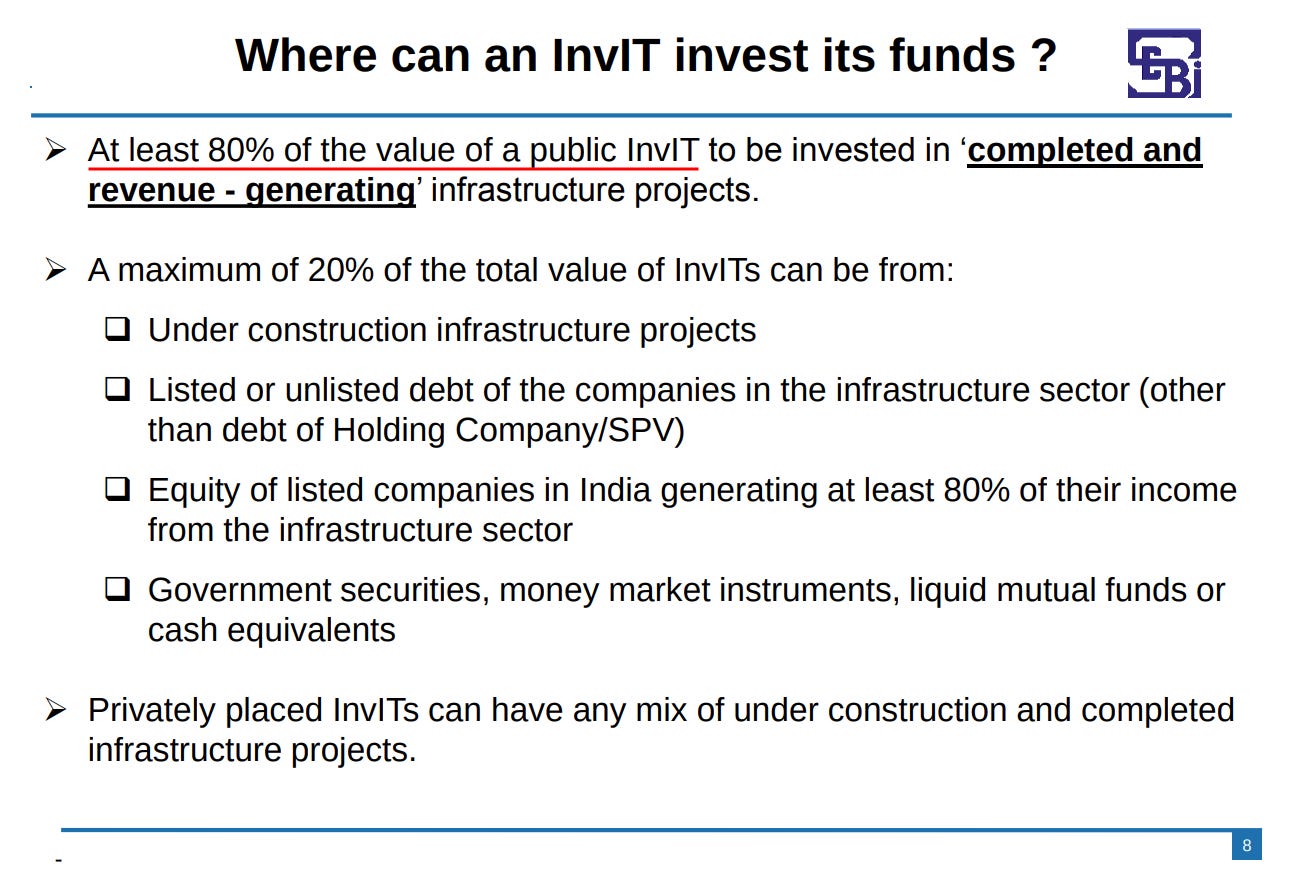

By SEBI regulation, every six months, an InvIT must distribute at least 90% of its “Net Distributable Cash Flow”, or the leftover cash once operating expenses and debts are paid off, to unitholders.

The broad InvIT risk landscape

In the infrastructure world, the type of asset dictates the majority of the risk InvITs undertake.

India currently has about six major publicly listed InvITs. They broadly fall into two camps: power transmission and roads . The difference between these two is enormous.

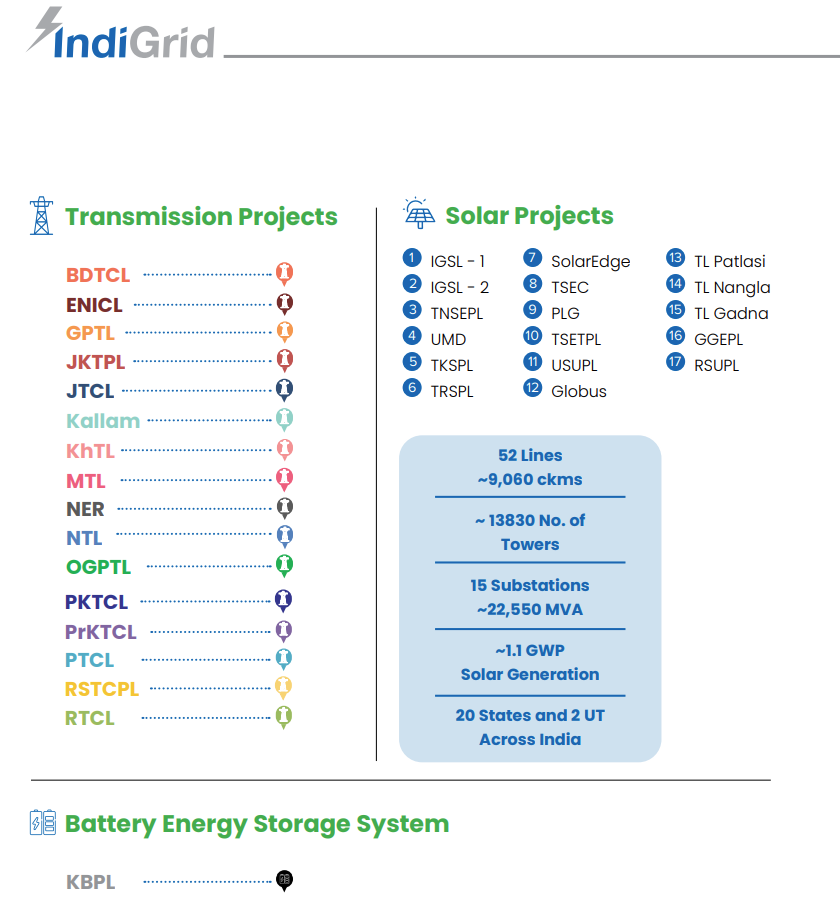

Power transmission InvITs — like IndiGrid and PowerGrid InvIT — resemble a regulated utility. They own tariff rights for electricity transmission lines and substations. They earn money for simply keeping the lines operational. It doesn’t matter whether the economy is booming or in recession; as long as the grid is running, the cheques come in. Their cash flows are exceptionally predictable, and the lives of their assets are long — 35–40 years. There’s very little that can disrupt them. That’s why institutional investors overwhelmingly prefer them.

IndiGrid, for example, owns 50 transmission assets spread across multiple states, mostly on long-term regulated tariffs.

Road InvITs — like RIIT — are a different animal. Revenue, here, depends on actual traffic volume and toll collections. If the economy slows; if fewer trucks are driving, for instance, tolls drop. If fuel prices spike, commercial traffic thins, and tolls drop. If an alternate route opens up nearby, cars shift, and tolls drop. Roads are economically sensitive in a way that power lines aren’t .

To sweeten the deal, however, road InvITs have historically offered higher yields than power InvITs — you’re being paid more for taking on more uncertainty.

On top of that, the economics of every road is different. We’ve covered these in detail before. RIIT, specifically, takes already built , operational roads and sells their future toll cash flows to investors through a Toll-Operate-Transfer (TOT) structure, wrapped in an InvIT. The road already exists. You’re buying the right to collect its cash flows. It’s a monetisation play, not a construction bet.

Evaluating an InvIT

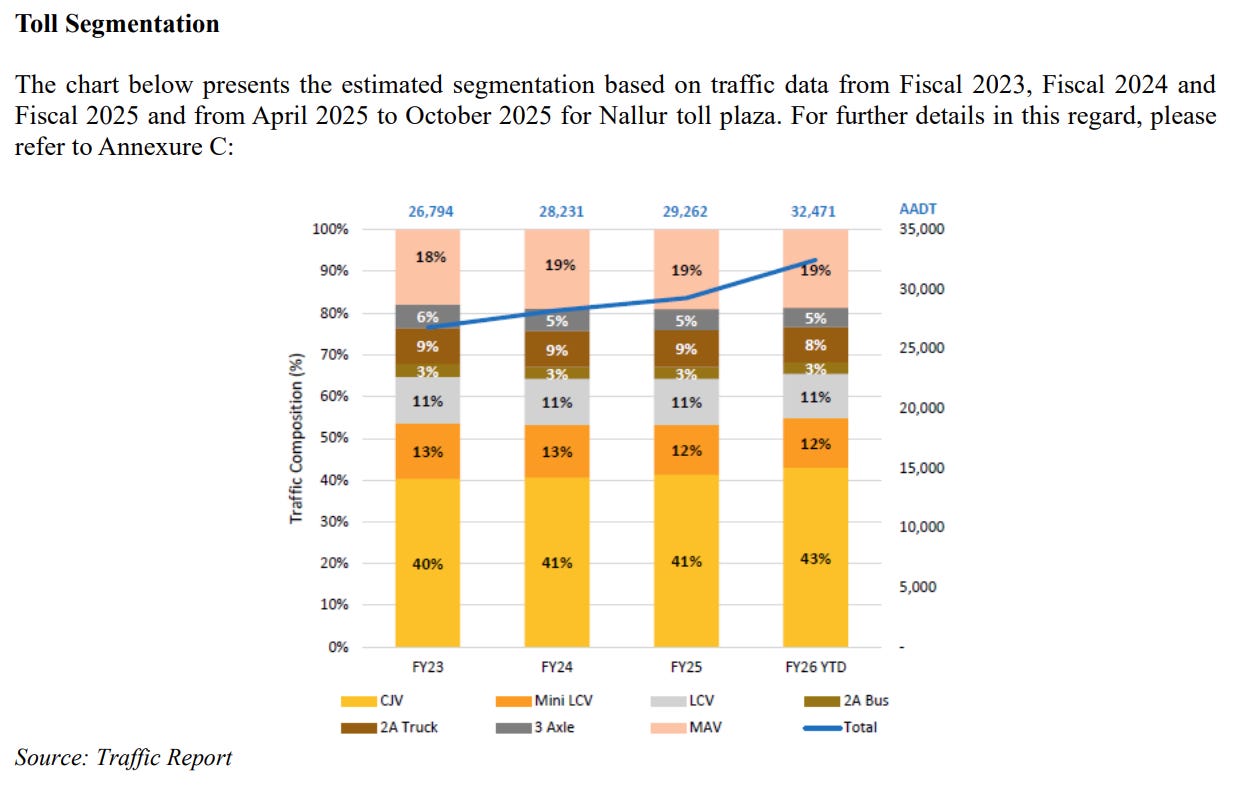

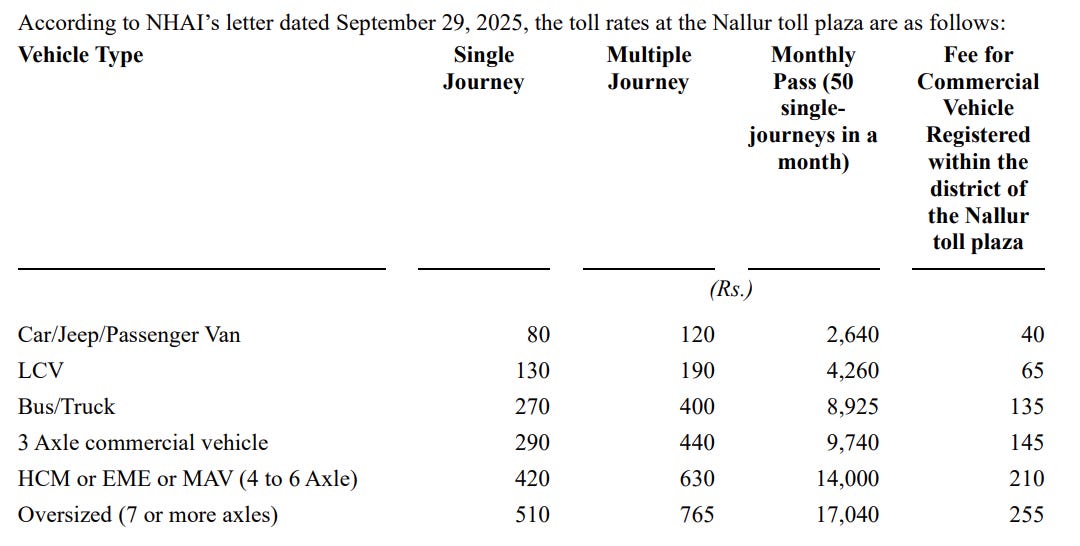

To evaluate this InvIT, then, you’re basically asking: how much toll do those roads generate , over the next many years? This analysis is very different from a typical stock. When we dug into RIIT’s offer document, most of our time went into studying the underlying assets. There was years of traffic data for each of the five roads, broken down by vehicle type: two-wheelers, three-wheelers, commercial trucks, passenger cars. It also had information on the current toll charges for each road stretch.

Traffic report for Nallur Toll on NH-16

Toll rates for Nallur Toll on NH-16

These are the numbers that feed into 15-year cash flow projections. They’re what you, too, would spend most of your time on. This investment is, really, a question of how you might underwrite an asset.

Here are a few things to note:

First, quality of assets.

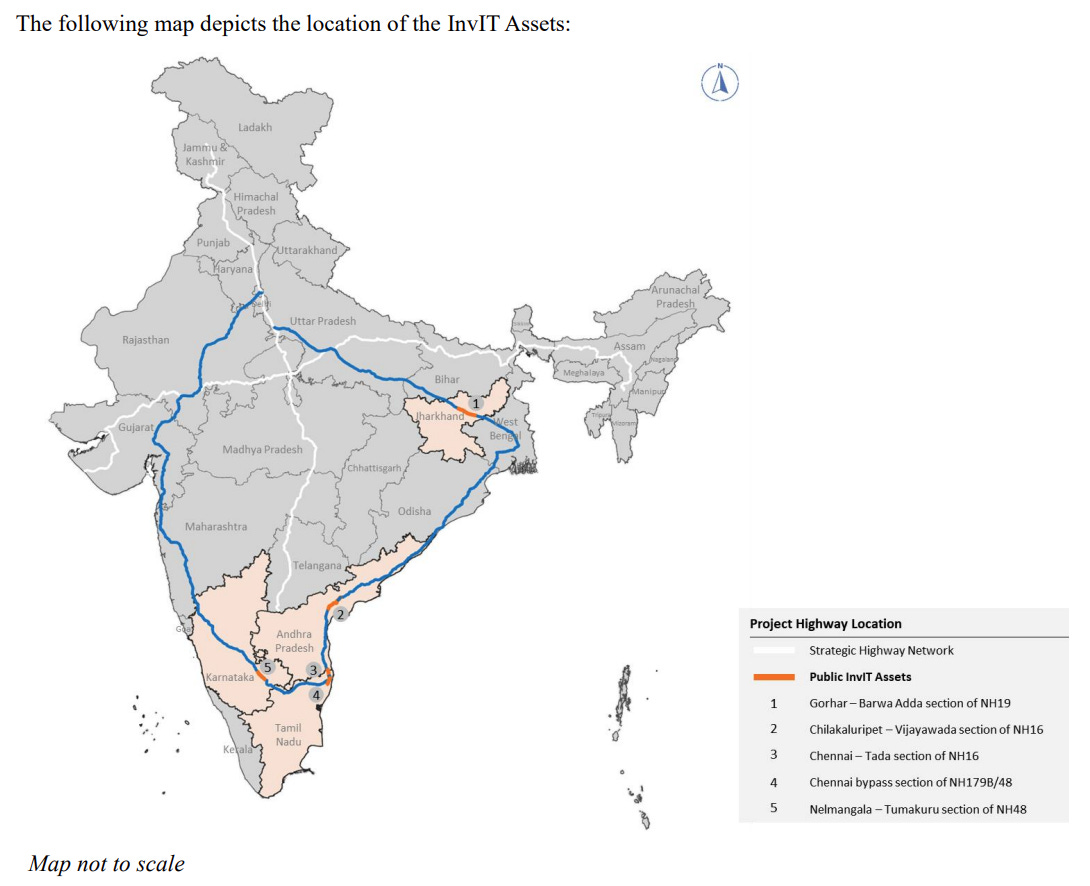

RIIT holds five operational toll roads on the Golden Quadrilateral, spread across four states — Jharkhand, Andhra Pradesh, Tamil Nadu, and Karnataka. These roads are spread out over a large enough spread to be somewhat diversified. But the portfolio leans heavily on the Neelmangla–Tumkur stretch. This is projected to bring in nearly 34% of its initial FY27 toll revenue. If traffic on that one stretch disappoints for any reason: from a local economic slowdown, to a new competing road or trainline, you’ll feel it across the entire trust.

Notice how different this is from power transmission. Power transmission lines are natural monopolies: you can’t build multiple competing high-voltage lines along the same corridor. Highways, by contrast, have what you might call “moderate monopoly” power. While they might hesitate to do so, there’s a point at which users might shift to alternative free roads or railways. One toll hike that feels too steep, or a few months of congestion that makes detours worthwhile, and alternatives start biting into the RIIT’s business.

Meanwhile, NHAI has approved a pipeline to offer RIIT an additional 1,500 km of operational highways over the next 3 to 5 years. That gives a clear roadmap for scaling up — assuming the acquisitions happen at reasonable valuations and the trust can raise capital to fund them.

Second, agreement terms.

Unlike a REIT, where lease terms can run for decades, infrastructure doesn’t generate cash forever. RIIT has a fixed 15-year concession for all five assets. That is how long it will collect tolls on these roads for. When it expires, those assets go back to NHAI.

Think of it this way: every year that passes is a year’s worth of toll income that has been exhausted. With a 15-year concession, five years in, you’ve already burned through a third of your income life. With a 40-year transmission asset, in contrast, five years is barely an eighth . The value of your units erodes more noticeably with each passing year.

Third, income stability and growth.

Over that period, its cash generation potential varies over time.

Toll revenues are traditionally volatile. Temporary inconveniences, like fuel price shocks or monsoon disruptions can swing traffic numbers, and thus toll collections. More broadly, when you run a highway, your cash flow comes from a diversified mix of passenger cars and commercial trucks. This ties the InvIT’s fortunes directly to the broad Indian economy. This is its appeal — it’s a general bet on India’s growth — but it’s also a vulnerability, exposing you to anything that slows growth down. If a recession eats two out of a road’s fifteen years, that’s two years you will never get back.

But RIIT has a somewhat unusual stabiliser: a Transitional Support Agreement. For the first 30 months after acquiring each asset, NHAI continues to run the existing tolling contracts. Under those contracts, NHAI was collecting a regular fixed fee, while the daily traffic risk was borne by subcontractors responsible for tolling. Now, instead of NHAI, the SPV collects those fixed payments.

When they come off, though, RIIT takes on full traffic risk. Its revenue, then, grows in two ways: natural increases in traffic volume, and annual toll rate hikes linked to the Wholesale Price Index (WPI). But it also means your returns become a bet on how many trucks actually use these roads, and how often the government tinkers with toll policies, exemptions, or competing routes.

Final thoughts

InvITs offer a genuinely different way to earn yield in India — backed not by corporate earnings or rental income, but by the country’s physical economic engine. But not all InvITs are created equal. A power transmission InvIT and a highway toll InvIT are almost different asset classes wearing the same legal costume.

So the question for any investor looking at RIIT — or any road InvIT — isn’t just “what’s the yield?” It’s whether that yield adequately compensates you for the traffic risk after the 30-month safety net expires, the maintenance burden that compounds over a 15-year concession, and the reality that when the concession ends, you’re left with nothing.

Does the payout justify what you’re signing up for?

India’s inflation targeting: a work in progress

Every few months, the RBI’s Monetary Policy Committee meets to answer one central question: is inflation too high, too low, or just right? Since 2016, the answer is supposed to revolve around one number — 4% inflation, give or take 2 percentage points either side.

For much of last year, though, inflation was under 2% — just outside the RBI’s tolerance band of 4% ± 2%. If inflation falls too fast, that might indicate that people aren’t buying things enough. There were even a few rate cuts from the RBI last year to spur consumer demand.

But what we wanted to understand was how inflation targeting became the RBI’s central operating framework in the first place. We covered its basics in a Daily Brief story from August last year. But India’s inflation targeting journey was formally enshrined only in 2016 — barely 10 years old. How did India’s central bank pursue its objectives before that? And how does inflation targeting clash with other objectives of the RBI?

A paper by economists Radhika Pandey, Ila Patnaik, and Rajeswari Sengupta offers the most comprehensive audit yet of how India’s inflation targeting regime has actually worked. It’s a huge paper, and we won’t be able to cover all of it. We recommend reading it in full, but we’ll summarize the most important takeaways here.

A brief history

To understand why the adoption of inflation targeting in 2016 was such a watershed, it helps to understand how Indian monetary policy worked before.

Before 1991, India’s economy was more centrally-planned by the state. Nationalised banks were directed primarily to fund government spending. And most importantly, there weren’t many differences between monetary policy and fiscal policy. In effect, the former was meant to serve the latter.

What do we mean by this? Well, the government ran high fiscal deficits at the time. And the RBI basically printed money to cover it — this is also known as fiscal deficit monetization. However, as a result, the system often suffered from high bouts of inflation. For instance, average wholesale price inflation ran at 8-10% through the 1970s, ‘80s, and early ‘90s. While there were attempts to change this approach to monetary policy, they didn’t work.

Then, in 1991, the economy opened up to foreign capital and deregulated interest rates. And in the new paradigm, fiscal deficit monetisation was phased out gradually. The RBI moved to what it called a “multiple indicator approach “ — instead of targeting a single variable like money supply, it would watch a dashboard of data: credit growth, capital flows, exchange rates, inflation, etc.

For about a decade, this approach worked well. Average GDP growth was around 7%, while inflation hovered around 5.5%.

But then came 2008, which triggered a rush of capital out of emerging markets. Foreign investors pulled money out of India, putting sharp downward pressure on the rupee. The RBI, which had been intervening in currency markets to stabilise the exchange rate, began burning through reserves and eventually had to step back. The government was also issuing fiscal stimulus to prop up demand.

But capital outflows weren’t the only issue at hand. Food prices surged, and CPI inflation stayed above 10% for years. People stopped believing that prices would stabilise, and started pricing that expectation into their wages and savings decisions — which only made inflation worse. Alongside this, the fiscal stimulus only worsened the inflation further.

As a result, India’s monetary policy lost its “nominal anchor “ — the reference point that tells markets and households what the RBI is actually trying to achieve. In earlier years, the rupee’s exchange rate occasionally acted as an informal anchor for policy. But under the multiple indicator framework, the RBI was never formally committed to any single target. Markets did not know which one ultimately mattered most.

Multiple expert committees came to the same conclusion: the RBI needed a single, clear, legally-mandated target, and not an assortment of things.

Lines in the sand

And that’s where inflation targeting comes into the picture.

The logic behind inflation targeting is straightforward. Businesses invest and hire more confidently when they know what prices will look like in three years. Households don’t need to demand higher wages every few months to stay ahead of rising costs. Banks can offer longer-term loans without building in massive uncertainty premiums. Stable prices, in other words, are the foundation on which economic growth rests.

This was the argument that finally prevailed. After successive reports recommended giving the RBI a clear price stability mandate, the machinery slowly moved. In 2015, the government and the RBI signed the Monetary Policy Framework Agreement, and the Finance Act of 2016 formally amended the RBI Act to enshrine inflation targeting in law.

Under the new framework, the RBI’s primary job is to keep CPI inflation at 4%, with a tolerance band of ±2%. The instrument is the repo rate — which is the interest rate the RBI charges banks for short-term loans, which flows through to lending and deposit rates across the economy. If inflation breaches 6% or falls below 2% for three consecutive quarters, the RBI must formally explain itself to the government.

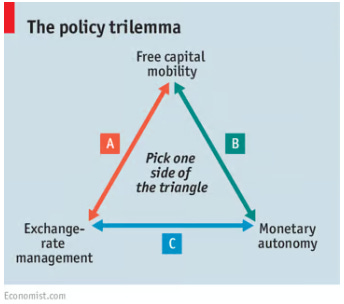

The impossible trilemma

The new framework brought clarity and a clear-eyed vision, but it came with its own set of problems. The biggest of them is something economists call the Impossible Trilemma . We covered this trilemma in depth in a previous story, but we’ll briefly touch upon it again here.

The trilemma works like this. Say that a country has the following three policy goals:

- An independent monetary policy , to set interest rates to suit your own economy

- A stable exchange rate , to keep the rupee-dollar rate from swinging wildly

- Free movement of capital , letting foreign investors move money in and out freely

The problem is you cannot have all three simultaneously, and at any given time, can only achieve two of them. That’s because free capital movement links interest rates across countries in ways that break the other two goals. The mechanism by which this trilemma manifests is a little complex, but bear with us as we try to explain it.

Imagine that the US Federal Reserve raises interest rates sharply. Higher US rates make dollar-denominated assets more attractive, so global investors sell rupees and buy dollars. The rupee comes under currency depreciation pressure.

Now the RBI faces a dilemma. If it raises rates to match the Fed, it’s effectively letting US monetary policy drive Indian monetary policy — not independent at all . If it doesn’t raise rates, the rupee depreciates, making imports costlier and potentially stoking inflation.

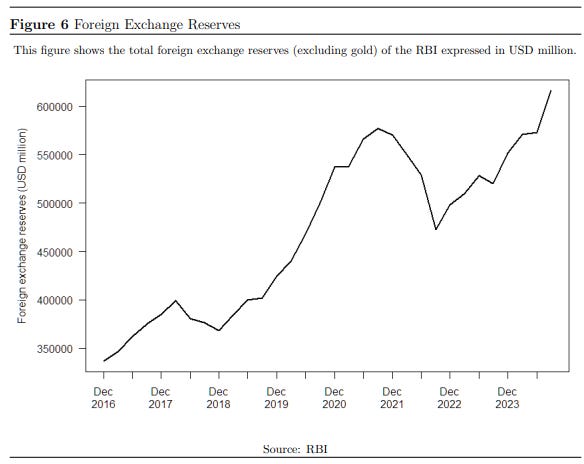

There is a third option: the RBI can intervene in the forex market by selling dollars to support the rupee. But that only works for as long as the RBI’s own reserves of the dollar hold, and capital outflow pressure is often stronger than any central bank’s reserves.

Moreover, RBI’s foreign exchange actions change the domestic money supply, which itself is intricately connected to inflation. For instance, when the RBI buys dollars, it pays for them with rupees. This prevents the rupee from appreciating, but also injects rupees into the system, which may have inflationary consequences. In fact, in 2023, the RBI was buying dollars at the same time it was keeping the repo rate high at 6.5% to fight inflation. In effect, both levers were pointing in opposite directions .

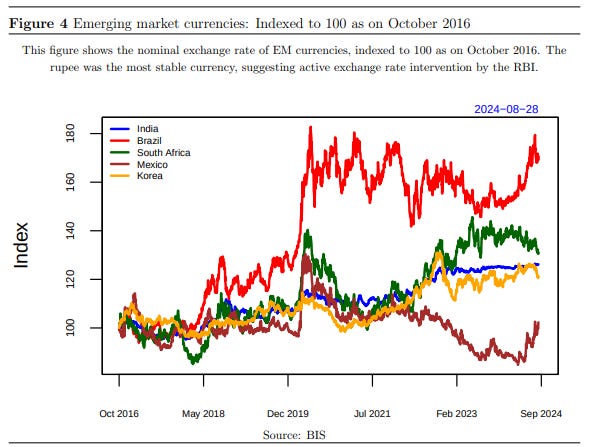

India has been trying to have all three, and the paper documents this tension in striking detail. Between April 2023-July 2024, the rupee’s annualised volatility was just 1.9% — the lowest in three decades. By comparison, the long-term average volatility over 2000-2020 was 5%. The RBI achieved this by massively scaling up its intervention in currency markets; in FY2024, the rupee was the third-most stable Asian currency against the dollar, behind only the Singapore dollar and the Hong Kong dollar.

Serving two masters

There is another built-in structural tension in the Indian economy that may dampen the effectiveness of inflation targeting: the RBI simultaneously manages monetary policy and manages the government’s debt .

As India’s central bank, the RBI’s job under inflation targeting is to raise interest rates when inflation is high. But, as the government’s debt manager, its job is to keep government borrowing costs in control. Higher interest rates may make it more expensive for the government to service its debt. And when India runs higher fiscal deficits, it needs to borrow more.

Every expert committee that has reviewed the framework since the 1990s has recommended fixing this by setting up an independent Public Debt Management Agency to take over debt management from the RBI. PDMA provisions were included in the Finance Bill 2015 — the same year the inflation targeting framework was adopted. But the RBI pushed back, and the clauses were withdrawn before the Bill was passed. The government promised a separate roadmap. It never came.

This tension shows up in the bond market. Between May 2022-February 2023, the RBI hiked the repo rate by 250 basis points. But the yield on the 10-year government bond — which should move up when rates rise — barely budged, rising by only 24 basis points. One possible explanation for this was that the RBI was buying government bonds in the secondary market to keep government borrowing costs from rising too fast.

The result was a nearly flat yield curve, and in some periods an inverted one, which sent confusing signals to the broader market about where rates were headed.

The report card

Now, how did inflation targeting perform as an intended policy objective?

The first MPC under the new inflation targeting regime (2016-2020) had a relatively smooth run. Average inflation during its tenure was 4.2% — perfectly in the RBI’s band. The committee mostly kept rates steady, cut them when growth slowed, and brought the repo rate from 6.5% down to 4% as the economy weakened.

The second MPC (2020-2024), however, had a much harder time. It inherited a pandemic, navigated a supply-chain crisis, and then faced the inflationary shock from Russia’s invasion of Ukraine in 2022, which pushed global commodity prices through the roof.

Average inflation during this MPC’s tenure was 5.8%, which was dangerously close to the top of the RBI’s band. In fact, in 2022, the RBI officially breached its mandate for the first time, as consumer price index (CPI) inflation exceeded 6% for three consecutive quarters from January to September. Naturally, the central bank had to write a formal letter of explanation to the government.

The data does support a modest positive verdict. Compared to the pre-inflation targeting period (2012-2016) when average headline inflation was 7.3%, the post-2016 average of 4.9% is meaningfully lower. Inflation has also become less volatile. And there is some evidence that households’ inflation expectations have started to anchor more closely to actual inflation, though India still lacks long-term expectations data.

Whether the good news is entirely due to inflation targeting, or partly due to lower global commodity prices and better-behaved food markets, is genuinely debatable. What seems fair to say is that the framework provided a credibility floor that kept expectations from spiralling the way they used to.

What the third MPC inherits

The third MPC was constituted in October 2024, and it began its work with inflation finally near the 4% target. The RBI cut the repo rate in early 2025 for the first time in several years. But the structural questions the paper raises haven’t gone away.

India may need to decide what combination of the Trilemma it wants to live with. A fully floating rupee would give the RBI genuinely independent monetary policy, but it would mean accepting more exchange rate volatility — something policymakers have been reluctant to do. Setting up the long-promised independent debt management agency would remove a genuine conflict of interest, but it requires political will.

None of these are insurmountable. But in a situation with increasing geopolitical rivalry and fragmenting world trade, it’s going to be even harder to manage the trilemma. A framework on paper and a framework in practice are two different things, and the gap between them is where the next set of reforms need to go.

Tidbits

- Daikin, Voltas, Blue Star, LG and others are hiking air conditioner prices just before peak season, driven by surging copper costs, a weaker rupee, higher freight costs and new energy efficiency norms.

Source: ET - The auto PLI scheme requires OEMs to have a minimum global revenue of ₹10,000 crore and fixed asset investments of ₹3,000 crore — thresholds that lock out EV startups like Euler Motors despite their being among the top players in electric cargo vehicles. Euler’s CEO is asking the government to count total investment, not just fixed assets, toward the eligibility criteria.

Source: BS - Karnataka will end its decades-old system of fixing liquor retail prices and move to an alcohol-content-based tax structure — the first Indian state to do so. The reform cuts pricing categories from 16 to 8 and lets producers set their own prices.

Source: Reuters

- This edition of the newsletter was written by Kashish and Manie.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Subtext by Zerodha

Subtext by ZerodhaWe’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()