Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- SEBI (temporarily) bans Jane Street

- India’s bid for energy security

SEBI (temporarily) bans Jane Street

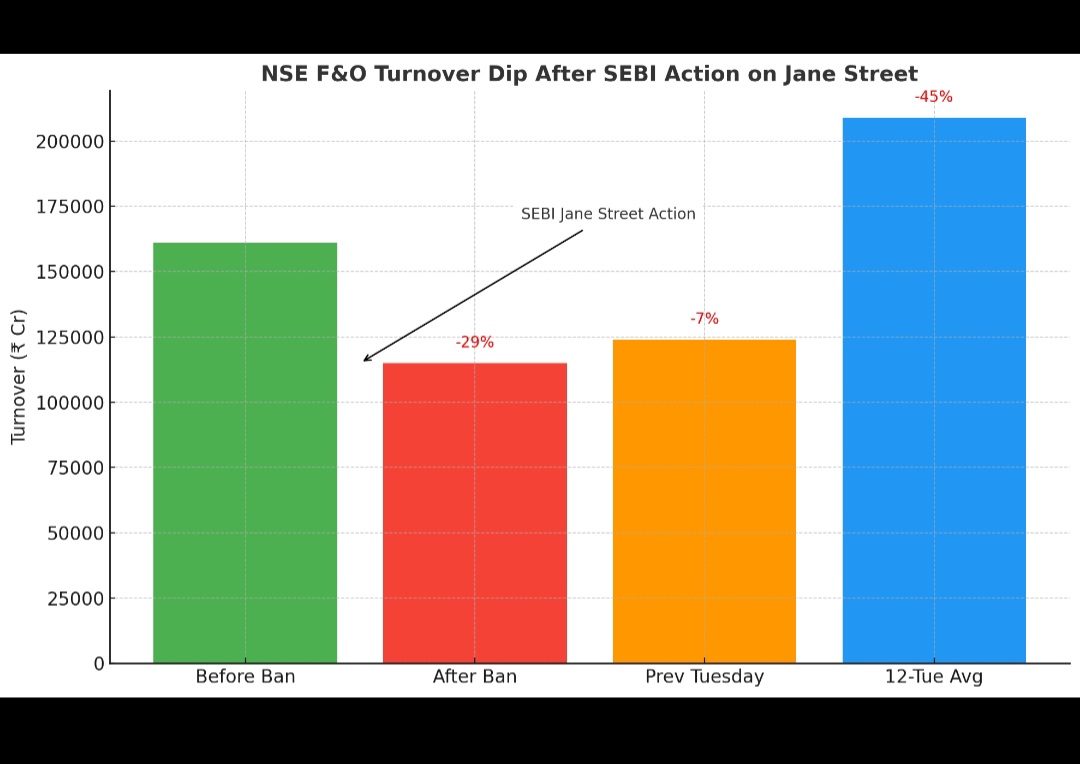

On July 3, 2025, SEBI temporarily banned the hedge fund Jane Street from the Indian markets, saying it had manipulated index options, netting hundreds of crores in profits — unfairly, and repeatedly.

This is huge . Jane Street is no ordinary entity. It’s one of the world’s most prominent proprietary trading firms. It’s famed for its secrecy, its math-driven culture, and elite talent pool drawn from top academic institutions. It brings all of this to bear in markets across the world. That is who SEBI has now gone after.

But what exactly did Jane Street do? What was this strategy? Why did SEBI come down so hard?

Let’s walk through everything, step by step.

How it all started

It all began in a New York courtroom.

In early April 2024, Jane Street had filed a lawsuit against another hedge fund — Millennium Management. It accused Millennium of stealing a proprietary, multi-billion dollar trading strategy. Specifically, the strategy involved trading index options in Indian markets.

The two Wall Street giants quickly settled the case. But the case caught everyone’s attention.

Until then, nobody really knew what Jane Street was doing in India. And they definitely didn’t know that Jane Street’s involvement went to a level where they felt the need to sue someone over a “secret” strategy. What was so special about this strategy? Why did Jane Street seem to think it was worth billions?

SEBI saw that lawsuit too. And the fact that the strategy in question involved Indian index options — something SEBI actively regulates — made it impossible to ignore.

SEBI starts digging

SEBI started studying the matter in April 2024. They went through Jane Street’s trading data, looking especially at expiry days — when weekly index options like BANKNIFTY would settle.

There were many trades Jane Street would make. But among them, it found one repeated pattern:

- Jane Street would buy and sell the stocks that made up BANKNIFTY aggressively.

- On the same days , they made massive profits in BANKNIFTY options — especially in those that expired the same day.

- The two, it seemed, were linked. They would buy stocks aggressively to push the index up. At the same time, they would bet against the index using cheap options. Then, they would dump the stocks. As the index fell, they’d book their profits.

This all looked like a coordinated, pre-planned strategy. So SEBI expanded its investigation. It reached out to NSE, asking for the full set of data for expiry days. That’s when SEBI saw just how perfectly Jane Street’s stock and options trades lined up on expiry days, when things escalated.

Eventually, SEBI asked NSE to formally look into these patterns as well. NSE issued a formal letter of caution to Jane Street in February 2025, asking them to refrain from large expiry-day trades, and the specific patterns that SEBI found suspicious.

Jane Street responded, claiming the trades were legitimate, and based on “proprietary strategies”.

SEBI didn’t buy that — especially not after seeing the data. In all the trades the firm made, there was a strand where the trading patterns just seemed too consistent, too perfectly aligned, and too profitable, in a way that suggested Jane Street had found a loophole, and was exploiting it repeatedly.

The investigation deepens

SEBI went through a long stretch of Jane Street’s trading activity — 18 different expiry days between October 2023 and March 2025. One particular day stood out: January 17, 2024 . This was Jane Street’s single most profitable day, where the fund earned a staggering ₹734.93 crore from index options alone.

The kind of number demanded a closer look.

The day seemed to showcase the full version of what the regulator later called the “Intraday Index Manipulation ” strategy — a pattern that re-appeared on 15 out of the 18 days it was looking at.

On that day, the market had opened on a weak note. HDFC Bank’s earnings seemed disappointing, the night before. But then, for a couple of hours, the BANKNIFTY index bounced back sharply, only to crash again.

Jane Street’s own trades, SEBI realised, lined up exactly with that reversal. We’ll get to that shortly. But first, you need to understand two key ideas:

- The first has to do with the BANKNIFTY. The value of the BANKNIFTY index depends entirely on the prices of its twelve underlying bank stocks. Some of those, like HDFC and ICICI Bank, make up more than a quarter of the index. If you can push just those stocks up, the entire index goes up. Push them down, and the index drops. That link — between the stocks and the index — is exactly what Jane Street exploited.

- The other key detail is the importance of the expiry day. On that day, any position that hasn’t been closed or squared off is settled based on where the index trades during the last half hour of the day. And so, options are extremely sensitive to moves in the underlying index. On these days, the options market goes wild. Volumes explode. For example, on Jan 17, BANKNIFTY options saw around ₹10,000 crore worth of premium turnover — 353 times the value of the trades in the actual stocks themselves.

So What Did Jane Street Do?

On Jan 17, Jane Street did two things, one after the other. Together, they tell the full story of the strategy that earned SEBI’s ire.

Part I: The rise (9:15 AM – 11:47 AM)

That morning, Jane Street started buying large quantities of BANKNIFTY stocks — Axis Bank, Kotak, ICICI, and others — in both the cash and futures markets. Their orders were so aggressive that they pushed prices up, leading to a temporary rally in the BANKNIFTY index.

SEBI found that in many of these stocks, Jane Street’s buying made up 15–25% of total market volume over that time. At that very time, though, they were also betting on the index falling :

- They were selling call options, or bets that the index won’t rise

- They were buying put options, or bets that the index will fall

Together, this meant Jane Street was positioning itself for a fall, while whipping up the illusion of a recovery for the rest of the market. This is what SEBI calls deceptive .

Part 2: The fall (11:49 AM – 3:30 PM)

At this point, they flipped the script. They started selling all those banking stocks and BANKNIFTY futures they’d bought earlier.

It was expiry day. The smallest movements in the index had an outsized impact on the value of some options — especially the ones that were At The Money (ATM).

An ATM option is one where the strike price — the level at which the contract becomes profitable — is very close to the current price of the index. These are the most sensitive to last-minute moves. There’s no time left, and they’re at the very edge of profitability — just a few points can decide whether they end up worth lakhs or expire worthless.

When Jane Street dumped those stocks in the final hours of the session, it pushed the index way down. Their bets had come true. The put options they bought were suddenly exploding in value. They went from being borderline worthless to deep in-the-money , all in the space of an hour or two.

And since they held a lot of these, the payoff was huge . Those put they bought became massively profitable. The calls they sold became worthless. All told, on that one day, Jane Street made ₹734.93 crore in net profits from options alone.

But the thing is, Jane Street wasn’t lucky. It didn’t get a prediction right. It made its own luck, in a sense. It created the very market move that it had bet on.

That move — where someone trades heavily in the last 30 minutes to push the index in a certain direction — is called “marking the close”. It is globally considered market manipulation, and is illegal. If you want to know more about this, check out this thread from Varsity.

Across all 18 days that SEBI studied, their options profit added up to roughly ₹43,000 crore, while losing ~₹7,500 crore in the other segment while implementing this strategy.

Why was that wrong?

Here’s SEBI’s view: Jane Street was shaping the market. Jane Street’s trades were so large, and placed so aggressively, that they moved prices on their own. In many of the BANKNIFTY’s constituent stocks — like Kotak, Axis, ICICI — Jane Street alone accounted for a fifth of all trading activity in short pockets of time. That was enough to push the market wherever Jane Street wanted it to go.

When they started aggressively buying those stocks that morning, they had an agenda: make other traders think more demand was coming in . Prices started rising, pushing up the index.

That was the setup. Behind the scenes, Jane Street was aggressively betting that the index would fall by the end of the day.

As others bought into the idea that the index would keep rising, Jane Street reversed their trades, dumping the same stocks they’d just bought, pushing the index back down. They bet on an outcome and then forced it to happen.

In SEBI’s eyes, that’s the wrong way to win a bet.

The aftermath

SEBI’s banned Jane Street from the Indian markets, for now. They’ve also impounded ₹4,840 crore, money that it thinks definitely came from the strategy.

Here’s what Nithin thinks about this entire issue: SEBI’s move was necessary — but it also shows how heavily the market leans on firms like Jane Street. They drive nearly half of all options volumes. When someone of this scale pulls back, the entire market feels the tremors.

https://x.com/Nithin0dha/status/1941069171216752792

Other market actions by SEBI

Meanwhile, SEBI is actively trying to reduce the volatility caused by weekly options, especially on expiry days. In November 2024, they introduced rules that limited weekly options trading to just two major indices—NIFTY and SENSEX—and added extra margins on expiry day, along with other risk-control measures.

Then in May 2025, SEBI brought in another set of reforms. These included a new way of calculating market open interest using option delta. They also raised position limits for individual firms. The goal was to reduce the risk of any single participant impacting the market too much.

Together, these steps reflect SEBI’s broader push to keep expiry-day chaos in check and make the options market more resilient.

India’s bid for energy security

India is building six giant, new underground caverns across the country, to fill with oil. This might sound like a weird detail, but it could have huge consequences. It could well determine how we get through the next world-wide oil crisis.

Our plan is to set up giant, hidden oil banks deep in the ground, which can "take India’s reserve capacity beyond 90 days " — the international standard set by the International Energy Agency (IEA). These banks — technically ‘Strategic Petroleum Reserves’, or ‘SPRs’ — will act like national back-up fuel tanks. If the world’s oil supply is suddenly cut off, and we land up with a national oil shortage, the government can release some oil from these stockpiles. That will keep our economy running for an extra 90 days — enough breathing room to think through our options and find alternatives.

This is in recognition of a wider problem: to India, oil is a national pressure point. Oil shocks are a threat we have to hedge on every possible front. We’re buying more oil from more countries than ever before. We’re letting private traders co-invest in our oil reserves. And we’ve quietly ramped up domestic exploration — drilling hundreds of wells.

This multi-pronged strategy — part diplomacy, part infrastructure, part speculation — is all aimed at one goal: making sure India never finds itself staring at an empty tank in a crisis.

Why build fortresses of oil?

India’s energy security is fragile. This has always been one of our great national weaknesses.

We use around 5.5 million barrels of oil every day. We produce just ~1 million. 85% of our oil — almost everything we need to run our cars, factories, and power plants — comes from other countries. This reliance makes us dependent on foreign countries for our energy needs.

In good times, this shows up in a hefty import bill. That isn’t ideal , but it’s the kind of thing we can manage.

In a time of crisis, though, things can get way worse. Imagine if 85% of your household’s groceries came from your neighbor’s house. Only, your neighbor was in an ugly, take-no-prisoners gang fight, and was hardly paying any attention to you. That’s kind of what’s happening right now.

About 40% of our oil imports travel through the Strait of Hormuz. We’ve covered this before, but to recap: that’s a thin stretch between Iran and Oman which handles 20% of global oil. If you stop ships from plying this thin route, all that oil is suddenly stuck.

Oil markets understand this risk very well.

In June 2025, as the Israel-Iran conflict escalated, Brent crude prices surged from under $70 per barrel to $81.40 per barrel within 11 days. This doesn’t just make it more expensive to fill up your fuel tank. Everything runs on oil. When oil prices go up, within days, everything from plane tickets to food gets more expensive.

We’ve seen this script play out before. In the 1970s, the Middle East was rocked by deep political instability, crushing us under a series of oil crises. Then, in 1990, the Gulf War sent oil prices sky-rocketing. India was pushed to near bankruptcy — we barely had enough money to pay for three weeks of oil. In fact, this a big reason we were forced to liberalise our economy.

The diversification play

This time around, though, if India was panicking about spiking oil prices, it didn’t show.

Amid all the chaos, as energy ministers across the globe scrambled and markets panicked, India’s Petroleum Minister Hardeep Singh Puri calmly stated there would be “no shortage of crude oil”. India had actually diversified its oil imports before the crisis struck, he noted, spreading its energy purchases across multiple countries and regions. In his words, "only 1.5 to 2 million barrels now come via the Strait of Hormuz, while 4 million barrels are sourced through other global routes ".

Most of our confidence is fairly recent.

Back in February 2022, when Russian troops marched into Ukraine, just 0.2% of our oil came from Russia. But then, the world tried isolating Russia with sanctions, forcing it to find new buyers for its oil. It began offering steep discounts of $18-20 per barrel below global prices. India was happy to accept the windfall. In just three years, Russian oil grew to over 35% of our oil imports. The country had suddenly become our largest oil supplier.

This wasn’t without controversy — the US and Europe have been pressuring India to cut down on Russian oil. Lately, in fact, we’ve even been threatened by 500% tariffs. Some day, if those threats get serious, these might change our national calculus. For now, however, we’ve asserted that we’re just trying to keep energy affordable for Indians, with no horse in the conflicts of others.

Apart from being cheaper, though, Russian oil has another big advantage: it avoids the volatile Strait of Hormuz entirely. It ensures that a big chunk of India’s oil supply no longer depends on Middle Eastern stability.

But that’s just one prong of our strategy. We’ve built in other layers of protection: from strategic storage, to alternative energy development.

Phase I: The first three underground fortresses

The crisis of the 1990s made it clear that India needed a plan around our oil dependence.

This became all the more urgent at the turn of the millennium. The world had briefly isolated India after the Pokhran-II nuclear tests in 1998, imposing sanctions and cutting off aid. It was a wake-up call. What if oil, too, was used to pressure us? The Atal Bihari Vajpayee government began drawing up formal plans to secure us from that possibility.

In 2004, we set up a new government company, Indian Strategic Petroleum Reserve Limited (ISPRL), to build new oil fortresses. Over a decade, it created three massive underground rock caverns — in Vishakhapatnam in Andhra Pradesh, and Mangaluru and Padur in Karnataka. Together, these facilities can store 5.33 million metric tonnes of crude oil, catering to 9.5 days of India’s emergency oil consumption.

As of last December, these hold ~3.6 million metric tons of oil.

![]()

It’s worth pausing for a moment to appreciate just how impressive these structures are. Imagine caverns the size of airplane hangers, carved deep into solid granite rock, hundreds of feet below the Earth’s surface. These start as underground salt deposits. We drill holes into these deposits, and then pump in water until all that salt dissolves, leaving giant, hollow cavities in the ground.

Each cavity can hold millions of barrels of crude oil — enough to supply oil to the entirety of India for days. They’re engineered to withstand earthquakes, and sealed so tightly that not a drop can escape for years. This makes them the safest vaults for a nation’s energy lifeline.

These are not our only store of oil. Our oil refiners store another 64.5 days of crude oil for their commercial operations. Together, our total buffer reaches around 74 days.

But that wasn’t yet enough .

Phase II and Beyond: Closing the Gap

In July 2021, the government approved two additional SPR facilities.

We planned to set up a new reserve from scratch in Chandikhol in Odisha, while expanding Karnataka’s Padur reserve. Together, these would add 12 additional days of coverage. This would bring our total reserves to around 87 days — close to the 90 day IEA standard.

But recently, especially in light of growing tensions in the Middle East, we’ve decided to surpass this 90-day requirement. The government is now building six additional strategic petroleum reserves. The government has asked the PSU, Engineers India Limited, to prepare feasibility reports for new reserve caverns. Soon, we may begin new projects in states like Rajasthan and Madhya Pradesh.

But that’s not all. These reserves are only as valuable as the opportunities taken to fill them. And that’s another place we’re looking for creative solutions.

Filling in the reserves

While it makes sense to have healthy reserves of oil, you also want to be strategic in how you build them. If you’re just buying oil to store in the ground for emergencies, it makes no sense to buy it when it’s expensive.

Building a reserve, therefore, is also a question of market timing.

One such opportunity came in April and May 2020, at the very start of the COVID-19 pandemic. For a brief while, global oil prices went negative. Producers were literally paying buyers to take oil off their hands. Demand had crashed, after all, and they had no place to store any more oil. It was like getting paid to fill up your gas tank.

India seized the opportunity like a savvy investor buying stocks during a market crash. The government used that period to fill our Strategic Petroleum Reserves to full capacity. This led to savings of approximately ₹5,000 crore, compared to filling them at normal prices.

We’ve since used up some of those reserves. As of early 2025, only about 67% of these reserves are actually filled. We’re now looking for another market bottom to make fresh purchases.

But that sparked a different idea: can we get storage to pay for itself?

To this end, we’re now experimenting with a new Public-Private Partnership (PPP) model. The government will outsource the work of investing in, building, and operating reserves to the private sector. In ordinary times, private companies will invest in and operate these facilities. If there’s an emergency, though, the Government of India will have the first ‘right of refusal’ over their stock.

We’ve already tried this sort of thing. The Abu Dhabi National Oil Company (ADNOC) has stored 5.86 million barrels of crude at the Mangalore facility since 2018. Similarly, HPCL has taken over 0.3 million tonnes storage capacity at Visakhapatnam as part of its refinery operations.

But now, we’re ramping things up. Some of the world’s biggest oil trading companies — including Trafigura, BP, Shell, and more — have expressed interest in entering such an arrangement. These companies are like the middlemen of the energy world; they buy oil from producers and sell it to refiners all over the world. A giant, strategically located oil reserve in India gives them a safe place to store their inventory, and optimise their supply chain in one of the world’s largest oil markets.

We might just find our own oil

There’s one final link to our oil independence strategy. We might be at the cusp of finding our own oil.

Petroleum Minister Puri believes India could have "several Guyana-sized reserves " of oil near the Andaman islands. These could add up to 11.6 billion barrels of crude oil.

Guyana is the ultimate oil discovery success story. It used to be a small, poor country. But after finding massive oil reserves, it practically became wealthy overnight — turning into one of the largest oil exporters in the world.

We might be close to a discovery of this scale. It looks like we’ve found some encouraging signs. Last year, ONGC drilled 541 wells in FY24, the highest in 37 years. This could be a generational jackpot, changing the very fabric of our economy. Hardeep Puri, in fact, claims the find could potentially expand India’s economy from $3.7 trillion to $20 trillion.

In closing

India’s energy strategy today is far more layered, resilient, and future-facing than it’s ever been. We’re no longer just passive buyers in a volatile market — we’re stockpiling reserves, diversifying our sources, and drilling our way to sovereignty.

None of this guarantees safety. But it gives us something we’ve long lacked: the ability to wait out the storm of oil shocks when others are scrambling.

Tidbits

- Just months after we broke down the public sector bank miracle, there’s now a push to take that miracle offline—literally.

The Finance Ministry has nudged PSBs to ramp up their physical branch presence to match the aggressive expansion by private and small finance banks. Why? Because while digital banking is the future, physical branches still play a vital role in building customer trust, improving service delivery, and mobilising deposits—especially in semi-urban and rural India.

So far in FY25 (till December 31), PSBs have opened 1,391 new branches—more than FY24 and FY23 combined. Yet private banks are still ahead with 1,552 new branches, led by HDFC Bank and Axis Bank. SFBs aren’t far behind either, clocking 1,272 new branches during the same period.

It’s part of a larger “phygital” vision that Finance Minister Nirmala Sitharaman outlined last month—combining the reach of digital with the reassurance of physical presence. The Northeast, with its lower banking penetration, is also in focus for new PSB branches.

The timing is interesting. PSBs’ fundamentals are stronger than ever—NPAs down to 0.52%, profits up to ₹1.78 lakh crore, and dividend payouts nearly doubled. Now, the next battle seems to be about reach—one branch at a time.

Source- Business Standard

- We’ve spoken before about how the world is entering the Age of Electricity — and how, despite pouring trillions into renewables, we’re hitting a roadblock: the grid.

One of the most promising fixes? Batteries. Specifically, utility-scale Battery Energy Storage Systems (BESS) that can store excess solar or wind energy and release it when needed. But in our last deep dive, we flagged a key issue — that even batteries, no matter how advanced or fast to deploy, still need to be connected to the grid, and that’s where delays often arise.

This week, there’s a step in the right direction.

The International Finance Corporation (IFC), part of the World Bank Group, just committed ₹460 crore ($55 million) in long-term funding to IndiGrid for India’s largest standalone BESS project in Gujarat. This system is designed to help stabilize Gujarat’s power grid and support renewable energy delivery during periods of peak demand. The financing includes concessional support from the Clean Technology Fund — a sign that global climate capital is now targeting the grid resilience problem more directly.

IndiGrid’s Managing Director Harsh Shah called BESS “central to the future of energy in India,” adding that this project is a strategic milestone in building next-gen infrastructure that’s “clean, resilient, and future-ready.”

It’s still early days — but moves like this hint at a slow but steady shift: from just building green energy, to building the systems that can actually deliver it.

Source: Business Line

- This edition of the newsletter was written by Krishna and Mridula.

Join our book club

Join our book club

We’ve started a book club where we meet each week in JP Nagar, Bangalore to read and talk about books we find fascinating.

If you think you’d be serious about this and would like to join us, we’d love to have you along! Join in here.

Have you checked out The Chatter?

Have you checked out The Chatter?

Every week we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Go check out The Chatter here.

“What the hell is happening?”

We’ve been thinking a lot about how to make sense of a world that feels increasingly unhinged - where everything seems to be happening at once and our usual frameworks for understanding reality feel completely inadequate. This week, we dove deep into three massive shifts reshaping our world, using what historian Adam Tooze calls “polycrisis” thinking to connect the dots.

Frames for a Fractured Reality - We’re struggling to understand the present not from ignorance, but from poverty of frames - the mental shortcuts we use to make sense of chaos. Historian Adam Tooze’s “polycrisis” concept captures our moment of multiple interlocking crises better than traditional analytical frameworks.

The Hidden Financial System - A $113 trillion FX swap market operates off-balance-sheet, creating systemic risks regulators barely understand. Currency hedging by global insurers has fundamentally changed how financial crises spread worldwide.

AI and Human Identity - We’re facing humanity’s most profound identity crisis as AI matches our cognitive abilities. Using “disruption by default” as a frame, we assume AI reshapes everything rather than living in denial about job displacement that’s already happening.

What the hell is happening?

What the hell is happening?Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()