Here’s a detailed summary of the SEBI Ex-Parte Interim Order (WTM/KV/ISD/ISD-SEC-2/31727/2025-26) dated 15 October 2025, in the matter of Insider Trading in the scrip of Indian Energy Exchange Ltd (IEX):

1. Background

1. Background

- SEBI conducted a suo-motu preliminary examination after a sharp fall (–29.58%) in IEX share price on 24 July 2025, following a CERC order on market coupling issued after market hours on 23 July 2025.

- SEBI also received a complaint alleging insider trading in IEX before the announcement.

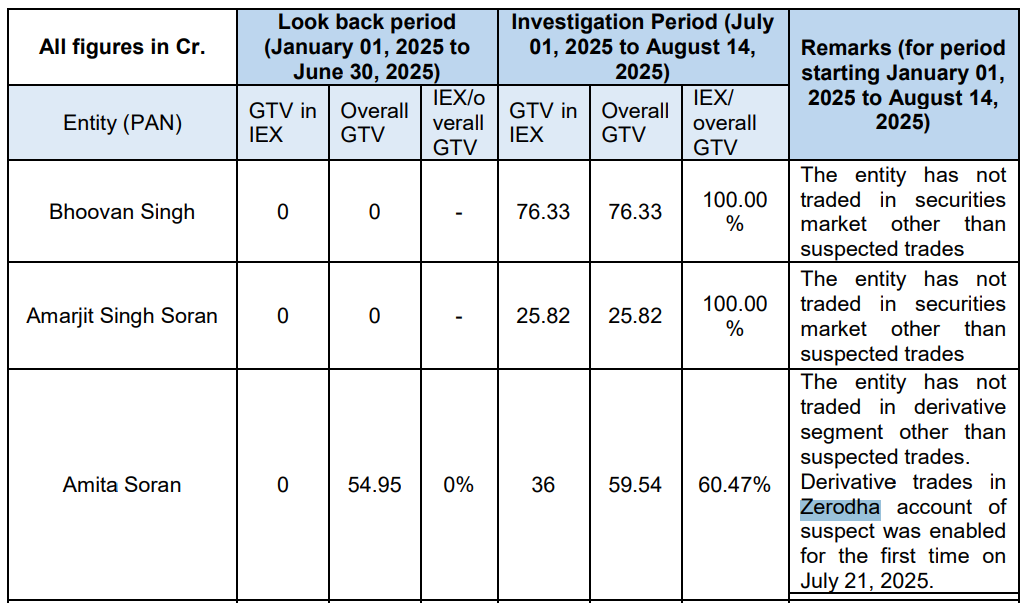

- Investigation period: 1 July 2025 – 14 August 2025.

- Search & seizure operations were conducted between 18–20 September 2025 at premises linked to the suspects.

- Digital evidence and statements were collected.

2. The CERC Order and UPSI

2. The CERC Order and UPSI

- CERC’s 23 July 2025 order introduced Market Coupling — a mechanism to centrally match bids from all power exchanges (IEX, PXIL, HPX) to form a single market clearing price.

- This meant IEX would lose control over price discovery and likely see reduced volumes.

- The information was not public before 23 July 2025, and caused a material impact (–29.58% fall).

Hence, it qualified as Unpublished Price Sensitive Information (UPSI) under SEBI (PIT) Regulations, 2015.

Hence, it qualified as Unpublished Price Sensitive Information (UPSI) under SEBI (PIT) Regulations, 2015. - Period of UPSI: 1 July 2025 – 23 July 2025.

3. The Noticees (Accused)

3. The Noticees (Accused)

| Sr. | Name | PAN | Notes |

|---|---|---|---|

| 1 | Bhoovan Singh | BTWPS4875D | Main recipient of UPSI from CERC official |

| 2 | Amar Jit Singh Soran | AAMPS1208C | Traded using UPSI |

| 3 | Amita Soran | AESPS0968P | Traded using UPSI |

| 4 | Anita | BXJPA5277J | Linked account |

| 5 | Narender Kumar | AOPPK9841L | Trader and fund conduit |

| 6 | Virender Singh | FAZPS5201P | Trader and partner in linked firms |

| 7 | Bindu Sharma | EEOPS4198F | Linked to Sanjeev Kumar |

| 8 | Sanjeev Kumar | BJMPS6988P | Placed orders for Bindu Sharma; conduit of information |

4. Source of UPSI and Chain of Communication

4. Source of UPSI and Chain of Communication

-

Official-1 (O1): Ms. Yogieta S. Mehra, Chief of Economics Division, CERC.

-

O2 & O3: Deputy and Assistant Chiefs in the same division — part of the internal committee drafting the order.

-

Evidence:

- WhatsApp and Signal chats between O1 and Bhoovan Singh show she shared confidential CERC documents, meeting minutes, and draft orders.

- Bhoovan shared these details in a WhatsApp group named “OTC”, including screenshots of internal CERC communications.

- Bhoovan deleted WhatsApp chats with O1 after receiving queries from NSE on 31 July 2025, but evidence from Signal remained.

- CERC’s internal draft order, notings, and minutes of 4th & 5th meetings were found in Bhoovan’s phone.

-

Conclusion: Bhoovan obtained UPSI from O1 and disseminated it to others, who traded based on it.

5. Trading Pattern & Profit

5. Trading Pattern & Profit

- The Noticees had no or negligible trading history in IEX before the UPSI period.

- During the UPSI window, they took large positions in IEX Put Options anticipating a fall.

- They booked profits immediately after the CERC order became public.

Profits Made

Profits Made

| Name | Profit (₹) |

|---|---|

| Bhoovan Singh | 72.04 crore |

| Amar Jit Singh Soran | 22.65 crore |

| Amita Soran | 31.60 crore |

| Anita | 3.09 crore |

| Narender Kumar | 34.53 crore |

| Bindu Sharma | 2.19 crore |

| Virender Singh | 7.04 crore |

| Total | ₹173.14 crore |

6. Fund Flow Analysis

6. Fund Flow Analysis

| Noticee | Jai Singh & Co. | GNA Energy Pvt. Ltd. | JSC Infratech Pvt. Ltd. | Total Transferred |

|---|---|---|---|---|

| Bhoovan Singh | 1.00 cr | 3.56 cr | – | 4.56 cr |

| Amita Soran | 0.50 cr | 0.35 cr | – | 0.85 cr |

| Narender Kumar | 6.25 cr | 0.35 cr | 8.60 cr | 15.19 cr |

| Virender Singh | 6.00 cr | 0.04 cr | – | 6.04 cr |

| Total | 13.75 cr | 4.30 cr | 8.60 cr | 26.65 crore |

These transfers were to connected entities controlled or operated by the Noticees — suggesting money layering and potential siphoning of illegal gains.

7. Prima Facie Findings

7. Prima Facie Findings

-

Noticees traded on the basis of UPSI from CERC officials — violating:

- Regulation 3(2) and 4(1) of the PIT Regulations, 2015, and

- Sections 12A(d) & (e) of the SEBI Act, 1992.

-

SEBI observed a coordinated scheme to benefit from insider information.

-

Trading pattern, communications, and fund transfers confirmed pre-planned insider trading activity.

8. SEBI’s Interim Directions (Main Part of the Order)

8. SEBI’s Interim Directions (Main Part of the Order)

Under Sections 11(1), 11(4), and 11B of the SEBI Act, SEBI ordered:

-

Impounding of ₹173.14 crore (equal to alleged unlawful gains).

- Each Noticee must deposit their impounded amount in a fixed deposit (FD) with lien to SEBI.

-

Complete trading ban: All Noticees restrained from buying, selling, or dealing in securities until further orders.

-

Freezing of bank and demat accounts:

- No debit allowed without SEBI’s permission.

- Credits may continue.

-

No disposal of assets: Noticees prohibited from transferring or alienating assets until the FD is created.

-

Full asset disclosure: Noticees to submit detailed inventory of movable and immovable assets, investments, and bank/demat accounts within 15 days.

-

Relaxation: After depositing impounded amounts, trading in other securities may resume, except IEX.

-

Derivative positions: Open contracts to be closed within 3 months.

-

Order effective immediately until further orders.

9. Next Steps

9. Next Steps

- Noticees can file replies within 21 days and request a personal hearing.

- Investigation into O1 (CERC official) and other connected persons is still ongoing.

- SEBI may later levy penalties or issue further directions under the law.

10. Signatory

10. Signatory

Kamlesh C. Varshney

Whole-Time Member (WTM)

SEBI, Mumbai

Order Date: 15 October 2025

In essence:

In essence:

This interim order by SEBI uncovers one of the largest insider trading cases in India (₹173+ crore), where confidential regulatory information from CERC was illegally leaked to market participants who profited through IEX options. SEBI has frozen their funds, restrained them from trading, and is conducting further investigation against both insiders at CERC and the traders who used the UPSI.

Summary by ChatGPT