Any price for cold comfort

Humans will do anything to avoid pain and discomfort—from murder to paying 2 and 20 to avoid mark-to-market prices.

— Swami Bhuvan.

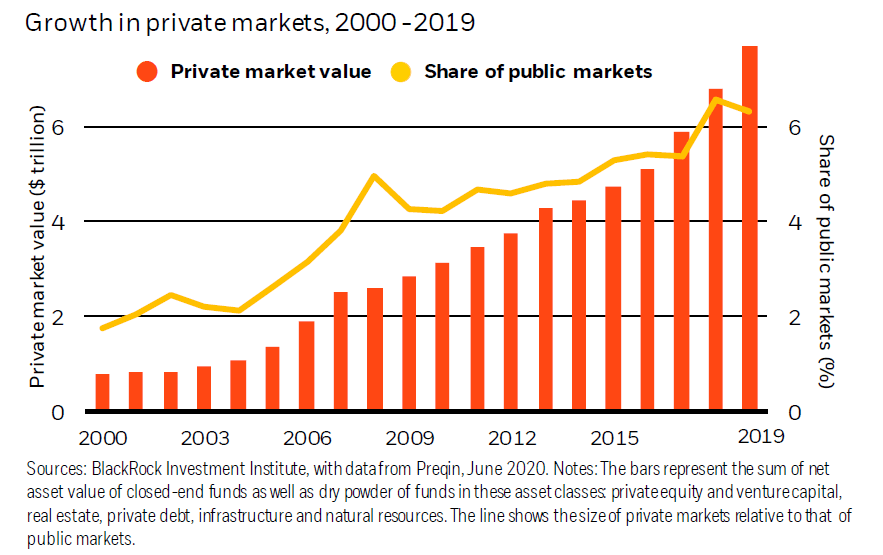

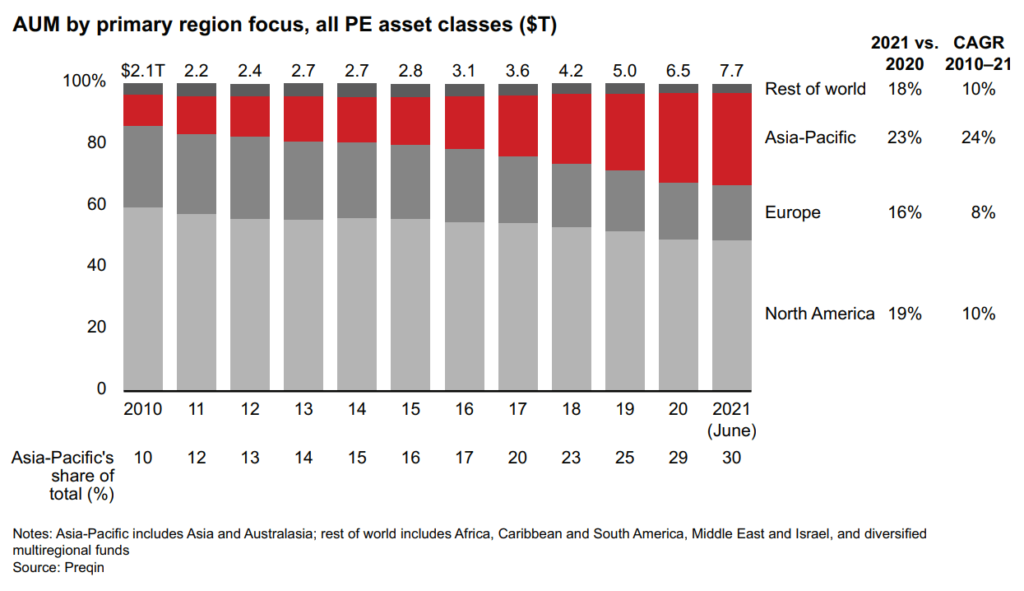

The rise of private markets has been one of the biggest trends in the financial markets over the last two decades. The United States and Europe account for most of the AUM, but Asia has grown faster.

Blackrock

Bain

Notes 1. PE and VC are also called “alternatives.” 2. Private markets is a catch-all term for private equity (PE), real estate (RE), venture capital (VC), private debt, infrastructure, and natural resources. 3. Some refer to all these things as “private equity,” while others define private equity as only “leveraged buyouts.” In this post, I’m using the all-encompassing definition.

People attribute the growth of private markets to the low-interest rate environment, easy liquidity, and the hunt-for-yield phenomenon. These factors played a role, but there were more tailwinds.

What were the factors that led to the rise of the private markets?

- Pensions and insurers have long-term liabilities, and they need to hit specific return targets to meet those liabilities. If interest rates and, by extension, bond yields are low, it becomes harder to meet those liabilities. Declining yields and lower expected returns force them to take more risks.

- Pensions across the world are underfunded. These shortfalls force them to seek additional returns to bridge the return gap.

- Growth of large institutional pools of capital like sovereign wealth funds, endowments, and family offices in the last three-odd decades. These entities have become major players in financial markets.

- Changing market structure and the decline in the number of publicly listed companies and IPOs worldwide.

- Changing regulations and the growing cost of public markets compliance.

- Good old herding. Institutional investors aren’t immune to fads and performance chasing. The monkey see, monkey do phenomenon is prevalent not just among retail investors.

- The regulatory changes post-2008 led to banks retrenching from a lot of areas. Players like private credit and fintechs have stepped in to fill the gap.

So what does this all mean?

One way of looking at this is how these factors change the way institutions invest. Based on certain return assumptions, analysts at Callan looked at what it would take to earn a 7% nominal return (5% real return).

Callan

The graphic below shows that the pattern of increasing complexity over time remains similar over the 30-year period, although the level of additional risk is lower. Today investors need to take on roughly 2½ times the volatility as they did 30 years ago to earn a 5% real expected return, versus over 5 times the risk when matching nominal return expectations.

Things have become even trickier since the piece was published, with inflation at 7-8%.

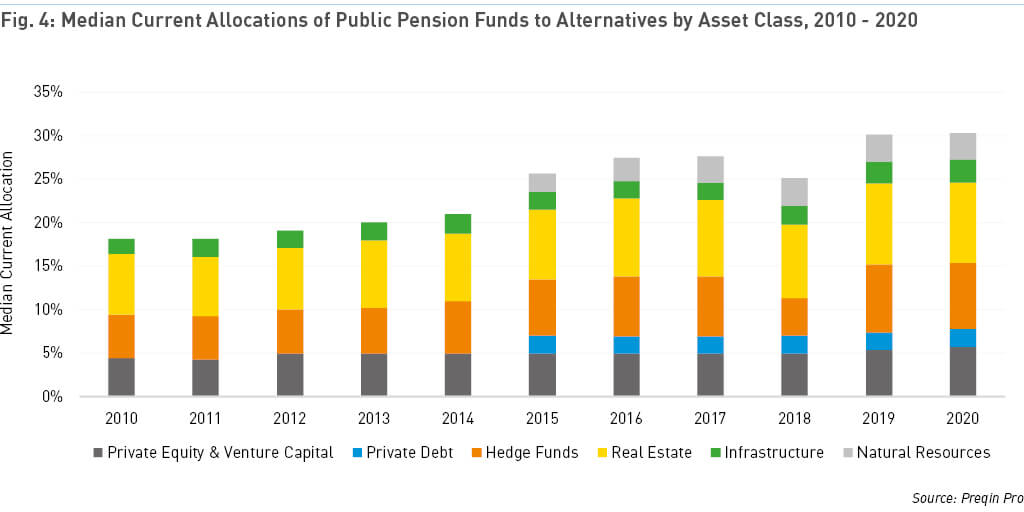

All these factors have led to institutional investors increasing their allocation to private equity, venture capital, real estate, and other alternative investments. On average, the allocation to private markets by institutional investors ranges from 10%-50% across the developed world.

Prequin

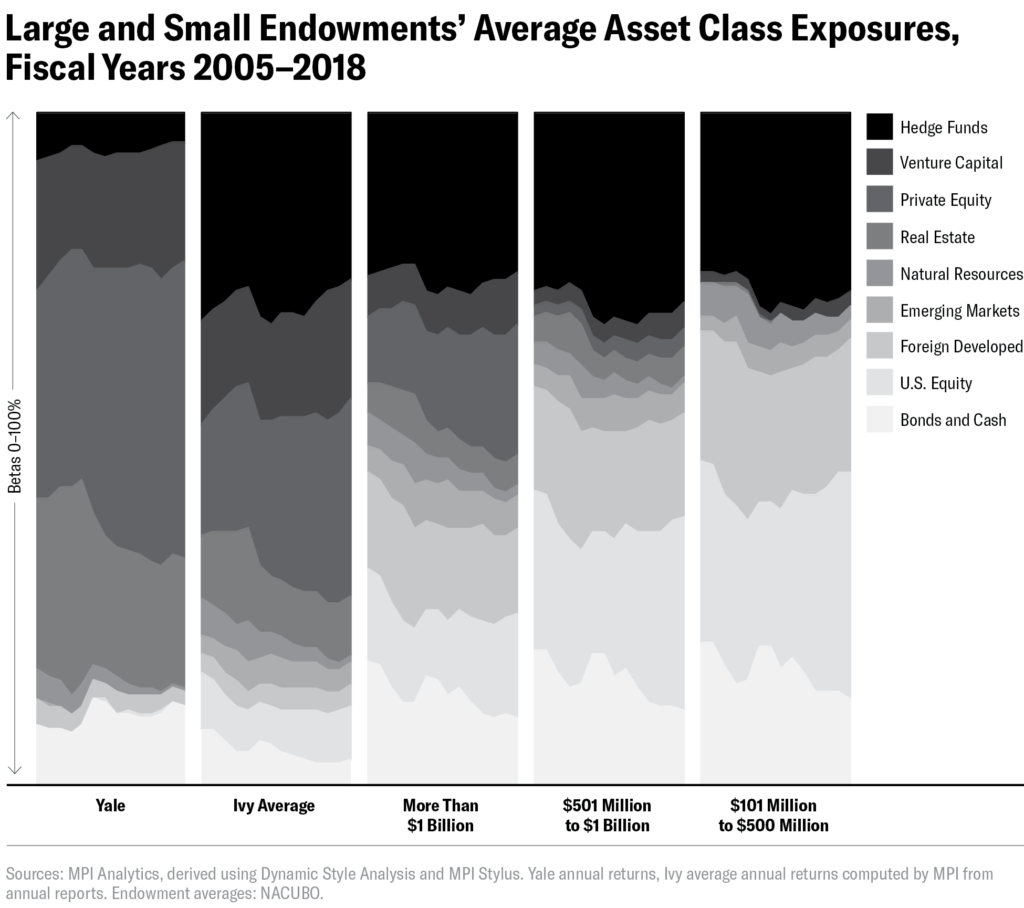

This shift from equities and bonds to a mix of other private assets is called the endowment model. David Swensen pioneered it at Yale and inspired a generation of allocators who’ve tried to emulate him, with mixed results.

Institutional Investor

Falling interest rates and the other structural issues I mentioned above have pushed pensions to increase allocations to private markets. If you still think this is a small allocation, consider that pension funds in the 22 largest countries manage over $56 trillion in assets. When you include other large investors in private markets, such as sovereign wealth funds, endowments, asset managers, and insurance companies, the number goes up to $175 trillion. Even a 1% allocation moves billions.

On average, pension funds in developed markets increased their allocations to alternatives from 7.22% of assets under management (AUM) in 2008 to 11.76% in 2017, a 63% increase. The top ten countries with the largest allocations to Alts as of 2017 were Italy (21.4%), the United States (19.6% of AUM), Canada (17.4%), South Korea (15.9%), Switzerland (14.4%), Brazil (13.8%), Germany (9.1%), Sweden (6.9%), the United Kingdom (4.9%) and Finland (3.5%).

When the Tailwind Stops: The Private Equity Industry in the New Interest Rate Environment – CEPR

Pension fund asset allocation in the 7 largest pension markets—Australia, Canada, Japan, the Netherlands, Switzerland, the UK, and the US.

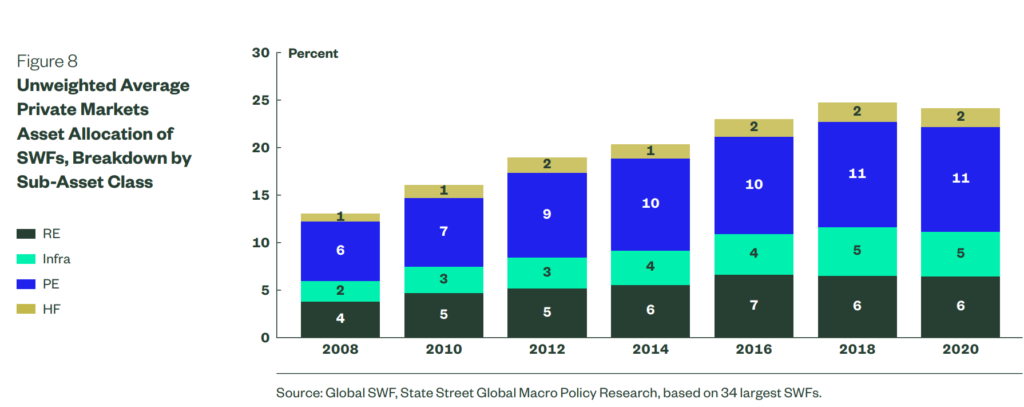

It’s not just pensions and endowments; even sovereign wealth funds have dived head-first into private markets.

State Street

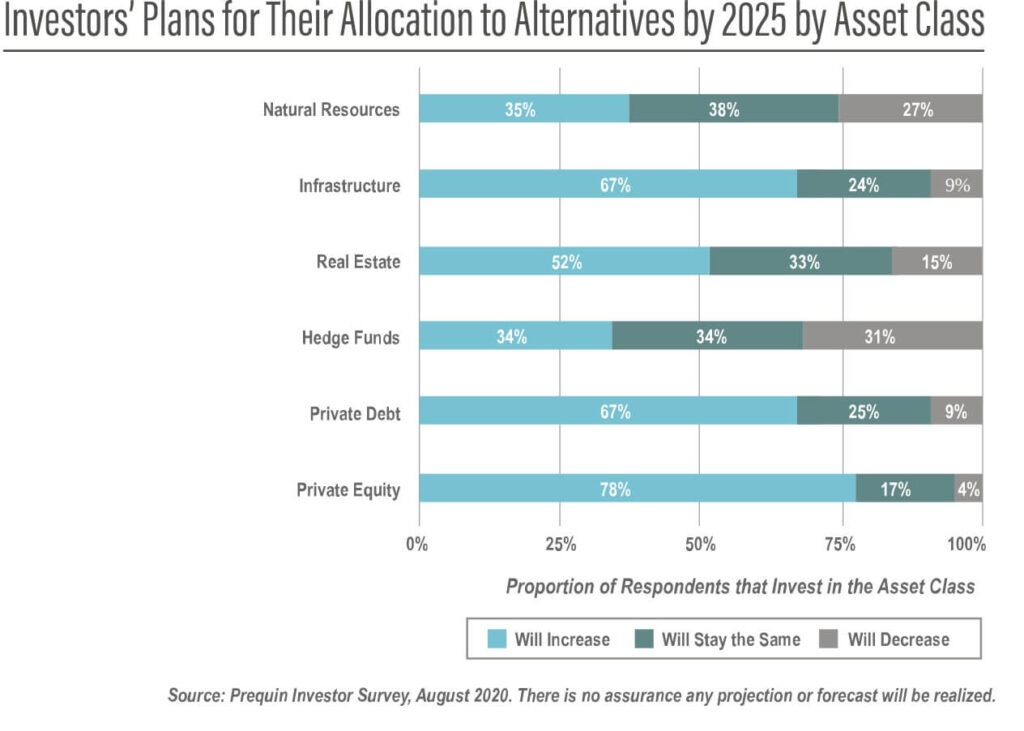

The rush to private markets is only getting started.

Pensions & Investments Alternatives report

What explains the dramatic shift into private markets? The common reasons touted by allocators are:

- Private markets outperform public markets with half the volatility.

- They offer better diversification compared to traditional stocks and bonds.

- They offer access to better opportunities since companies are staying private for longer.

- Private investors can create more value because they have a much longer investment horizon than public market investors.

Is private equity a fairy tale? Before we jump to conclusions, let’s unpack this.

The views about private equity fall on a broad spectrum. On one end of the spectrum, you have Elizabeth Warren, who likened private equity to vampires. Then you have Jeff Hooke, professor of finance at Johns Hopkins and author of The Myth of Private Equity, who says that believing in private equity outperformance is like believing in the tooth fairy. Ludovic Phalippou, the author of Private Equity Laid Bare and professor of financial economics at the University of Oxford, calls private equity a billionaire factory. On the other end, you have people like Steve Kaplan and Steven Davis, both professors at the Chicago Booth School, who think private equity is a force for good.

If you’re a public markets investor, you wouldn’t think much about performance measurement because you have real-time pricing and easy access to historical data. You’d think this shouldn’t be an issue for a $10 trillion asset class like private markets, but you’d be wrong. Something as basic as performance measurement is a nightmare. If you ask five people about the performance of private equity, you will get ten answers.

Why the disconnect?

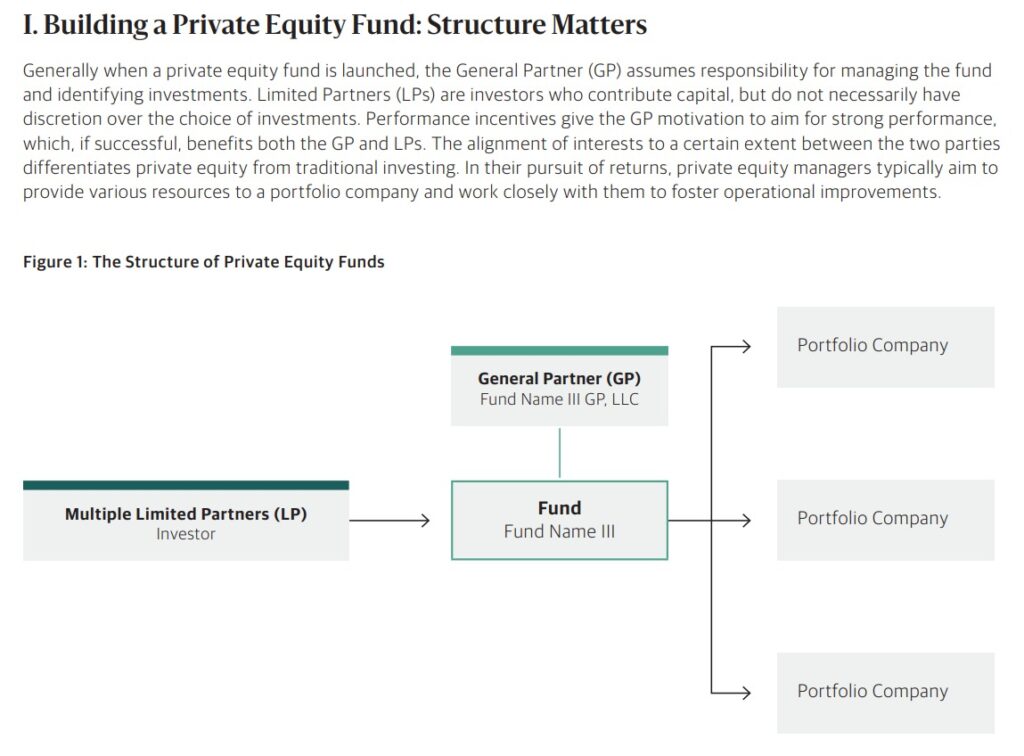

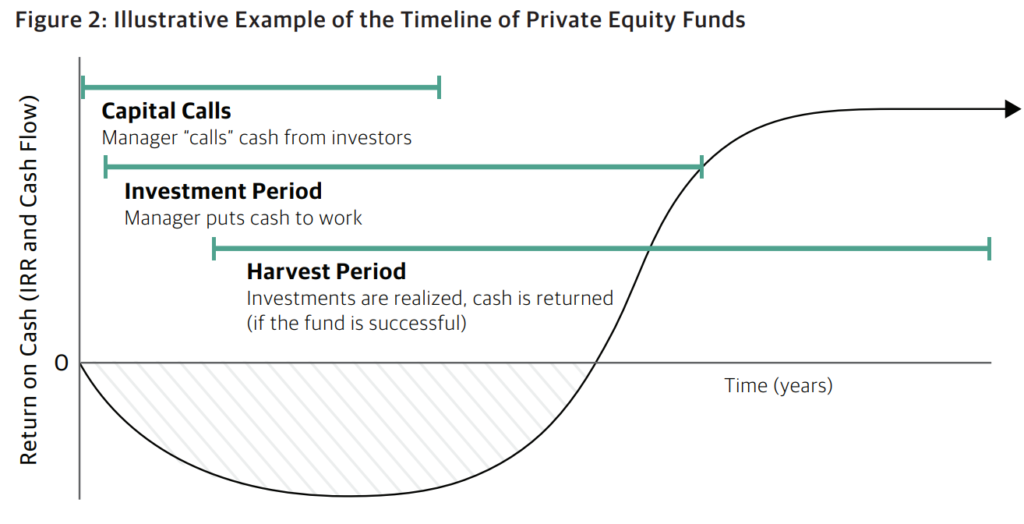

As a refresher, a private equity fund is like a closed-end fund. Private equity firms say they can acquire existing companies and improve their performance.

Structure of a private equity fund.

Blackstone

Fund

Private equity companies like Blackstone or KKR create funds that target a specific sector like healthcare, technology, energy, etc. The common fund structure is a limited liability partnership (LLP). The typical life of a private equity fund is 10 years, but it can be extended for a couple of years.

Investors

The fund then raises money from investors such as pension funds, endowments, and sovereign wealth funds. The investors in a fund are called limited partners (LP).

Management

Much like a mutual fund, a private equity fund will have a manager(s) whose job is to identify companies, acquire them, improve them, and sell them. The fund manager in a PE fund is called a general partner (GP). Unlike a mutual fund, all the money isn’t invested right at the start. LPs commit money to the fund, but the GP calls for the money as and when he identifies opportunities. The GP invests the capital in the first 5 years and then starts selling the companies after, returning the money to the LPs after fees. The sales can be through IPOs, secondary sales to other companies, or private equity firms.

Blackstone

Fees

A private equity fund typically charges a management fee of 1.5%-2% and a performance fee or carry (carried interest) of 20%.

Performance reporting

Most PE funds disclose their NAVs every quarter. Mutual funds invest in publicly traded securities like stocks and bonds that, for the most part, have real-time pricing. So measuring the performance of a mutual fund is easy. But a private equity fund holds private securities that don’t trade. So, private equity firms use fair value or appraisal accounting methods to value the companies they own. It’s a hypothetical price at which you can sell a company. Private equity firms have to adhere to guidelines, such as the fair value guidelines from the Financial Accounting Standards Board (FASB), but despite that, the valuation is based on the opinion of the fund manager (GP).

As you can imagine, this leads to all sorts of issues. Nobody cared about this when the private markets were small. But with over $10 trillion in AUM globally, the private markets are no longer a cottage industry. Private equity manages trillions that belong to public pensions and sovereign wealth funds, which taxpayers and public workers like Govt teachers, firemen, and municipal workers fund. Knowing whether the fiduciaries managing these public pools of money are doing a good job is the least you should expect. After all, private markets are a notoriously costly asset class.

Discussions about private equity lead to questions about performance, fees, whether they create value, systemic risks, and their societal impact. In this post, my objective is to see how smart, professional institutional investors are. So let’s look at the performance of private equity first.

Whether private markets outperform public markets has to be among the loudest debates in modern finance. Nobody agrees on anything because of the opaque nature of the asset class and the lack of accurate data. Publicly traded securities have time series data based on actual trades. This makes it easy to use models like CAPM and the Fama-French factor models to analyze risk and return characteristics.

But private equity funds don’t have market values because the underlying companies are private. Even though private equity funds disclose their net asset values (NAV), the valuations of the underlying companies are based on the opinions of the fund manager. The NAVs are published every quarter, but they tend to be stale. There’s widespread evidence that private equity funds manipulate returns and valuations. Funds are also secretive about the returns. In 2003, Sequoia terminated its relationship with the University of Michigan after the endowment was forced to disclose the returns of its private market investments.

Researchers and academics use databases maintained by firms like Prequin, Burgiss, and Cambridge Associates to analyze private data, but they suffer from obvious self-selection and self-reporting issues. To give you a sense of how difficult it is to get PE data, Prequin collects its data through Freedom of Information Act (FOIA) requests to public pensions in the US and UK. To make matters worse, the fund cash flows are also irregular, and the valuations of company exits can only be determined after the exit. We’re only talking about measuring returns.