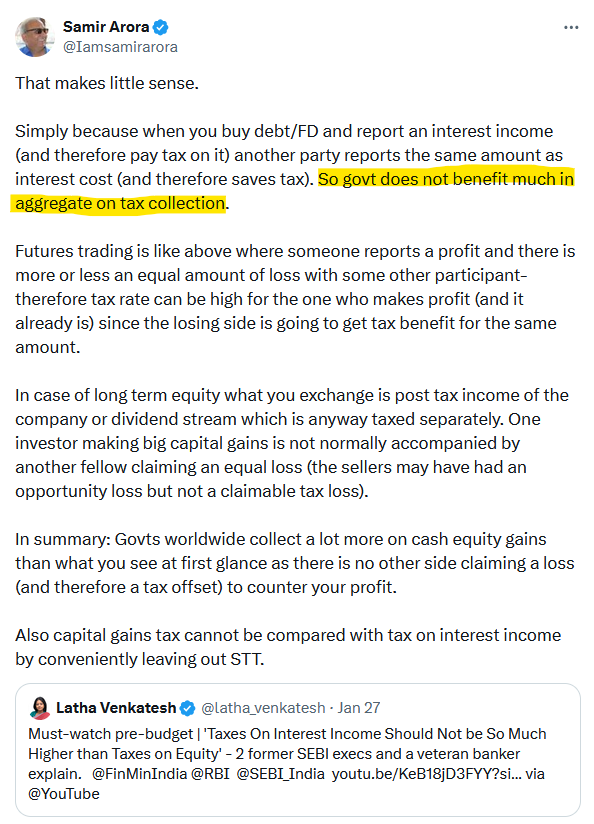

While this might seem true at first glance, there are counter-points to this.

The flawed assumption from the article is that

all borrowers are corporate entities or businesses capable of deducting interest expenses.

Not true.

If an individual takes a personal loan (for a vacation or medical emergency), and they pay interest,

they cannot always deduct that interest from their taxable income.

In this scenario, the government collects tax from the lender’s interest income,

but loses nothing on the borrower’s side.

Similarly, when investors buy GSECs/TBills, the government pays the interest.

The government does not pay tax, nor does it “deduct” interest to save tax.

The tax collected on the bondholder’s interest is pure revenue.

By ignoring such significant segments of the debt market,

the argument from the article ends-up being an example of a hasty generalization logical fallacy.

An LLM-assisted summary of several other logical fallacies present in the rest of the article.

The “Zero-Sum” Fallacy (Futures Trading)

The Argument: In futures, for every winner, there is a loser; therefore, the tax revenue is neutral (or justifies higher rates on winners) because the loser claims a tax benefit.

The Logical Issue: This assumes that tax deductions are always immediately and fully utilizable (perfect liquidity of tax credits).

- Reality: A loss is only useful for tax purposes if the trader has other gains to offset it against. If a trader wipes out their account and has no other income sources or gains in that category, that “tax benefit” is useless in the current year (though it may be carried forward, its present value is lower). The government often collects tax on the winner immediately, while the loser may never fully claim the benefit.

False Equivalence / Category Error (Equity vs. Debt Mechanics)

The Argument: Equity gains result in higher net tax collection because when one person sells for a profit, the buyer doesn’t get to claim a “loss” or deduction.

The Logical Issue: This compares a flow (interest payments) with a valuation change (capital appreciation).

- The Flaw: When Company A pays interest to Lender B, cash changes hands. When Investor A sells a stock to Investor B, the stock changes hands. Investor B now holds the asset at a new “cost basis.” If the stock drops, Investor B will eventually claim a loss. Arora seems to treat the “buyer” in an equity transaction as the counterpart to a “borrower” in a debt transaction, but they are logically distinct roles. The buyer is simply resetting the tax basis.

Special Pleading (Double Taxation)

The Argument: “In case of long term equity what you exchange is post tax income of the company…”

The Logical Issue: While factually true that dividends come from post-tax money, using this to argue against capital gains tax comparisons involves selective application of principles.

- The Flaw: If the argument is about “net government collection,” one must acknowledge that interest is often paid from pre-tax revenue (deductible), whereas dividends are post-tax. This actually supports the idea that the government collects more total tax from the corporate equity lifecycle (Corporate Tax + Dividend Tax + Capital Gains Tax) than from the debt lifecycle. However, Arora frames this as a reason why equity gains are “different,” obscuring the fact that the equity stream is already taxed more heavily at the source (the company level) than debt.

Survivorship Bias (The “No Counterparty Loss” Assumption)

The Argument: “One investor making big capital gains is not normally accompanied by another fellow claiming an equal loss.”

The Logical Issue: This assumes a market that only goes up.

- The Flaw: In a bear market or a crash, millions of investors sell at a loss. In those years, the government’s “net tax collection” on capital gains can drop to near zero or become negative (in terms of carry-forward losses reducing future revenue). Arora’s logic only holds true during a bull market.

Inconsistent Comparison (The STT Point)

The Argument: Comparisons are flawed because they ignore the Securities Transaction Tax (STT).

The Logical Issue: This is a “Red Herring” or an “Apples to Oranges” comparison.

- The Flaw: STT is a turnover/transaction tax, whereas Capital Gains and Interest Tax are income taxes. While relevant to the total cost of trading, STT applies whether you make a profit or a loss. Bringing a transaction fee into a debate about income taxation muddies the logical waters regarding how profits should be treated.