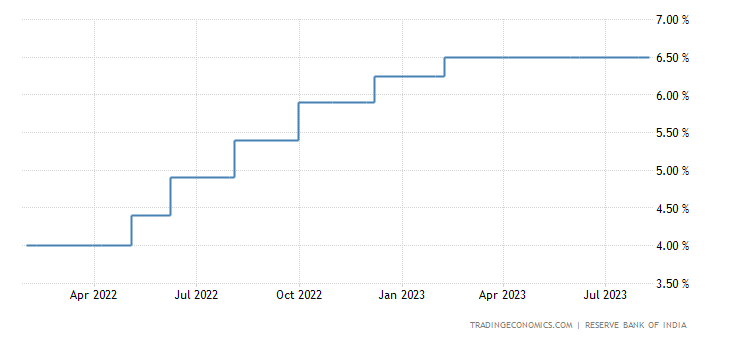

What’s happening on the Interest rates front?

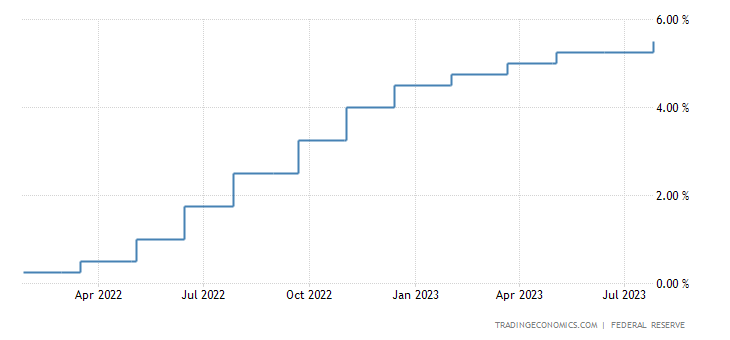

US 10 year yields are at 15 year highs

Japanese 10 year yields at 9 year highs

German 10 year Bund yields are 5 bps away from 12 year highs

And we’ve already started seeing gloomy articles across the board saying how bad this is for the markets.

But at the same time, Equity markets are stubborn and unwilling to go down. So, what’s happening?

What’s the generally perceived correlation between higher interest rates and equity?

-

Most of us would logically think, there’s higher inflation, so central banks raise interest rates and when interest rates go up, the cost of borrowing for governments, companies and individuals go up. Bottomline goes for a toss and this leads to lower profits or higher deficits.

-

So, naturally, we may think stocks should do badly on lower earnings and therefore Price to earnings gets corrected, plus as the interest rates are higher, investors would prefer to buy bonds as they offer comparatively higher returns when compared to the risk one is taking.

So yeah, If we were to take a overtly simplistic way, Markets should go lower and we should short the markets and make money - Sounds simple right? But, markets aren’t really that simple.

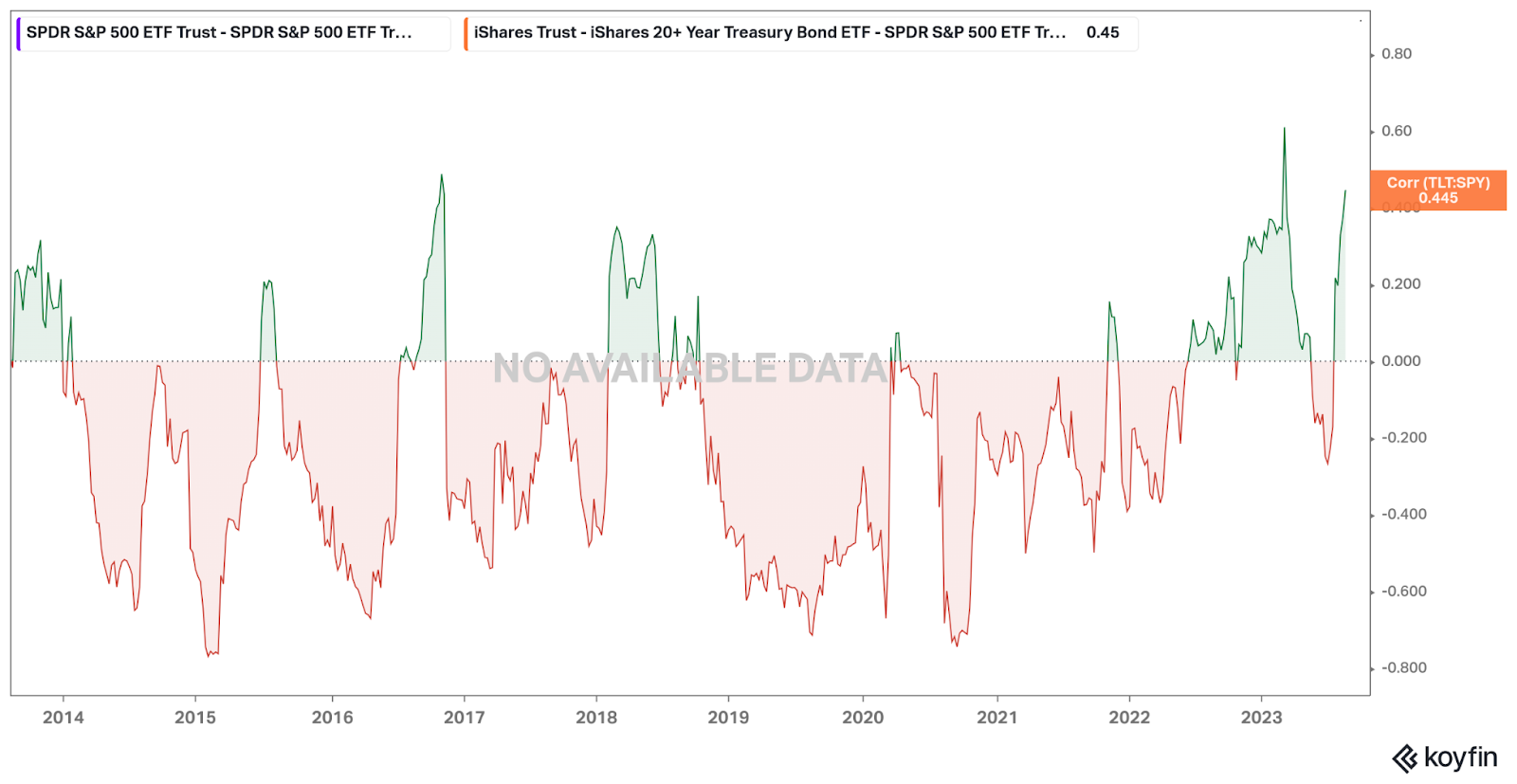

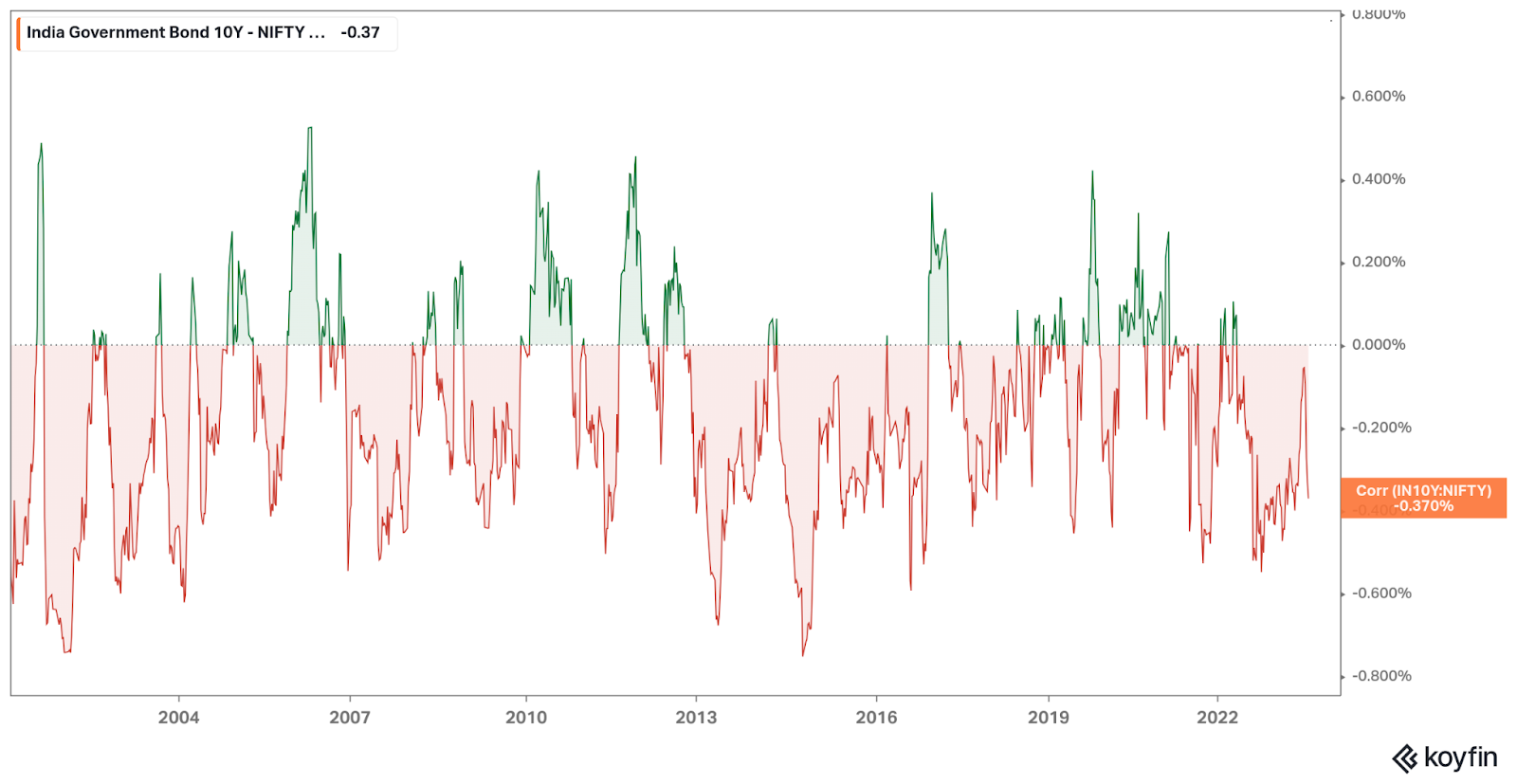

When I asked my colleague @Bhuvan about this , He said “These correlations are never static. They keep changing.”

And shared couple of charts on this point:

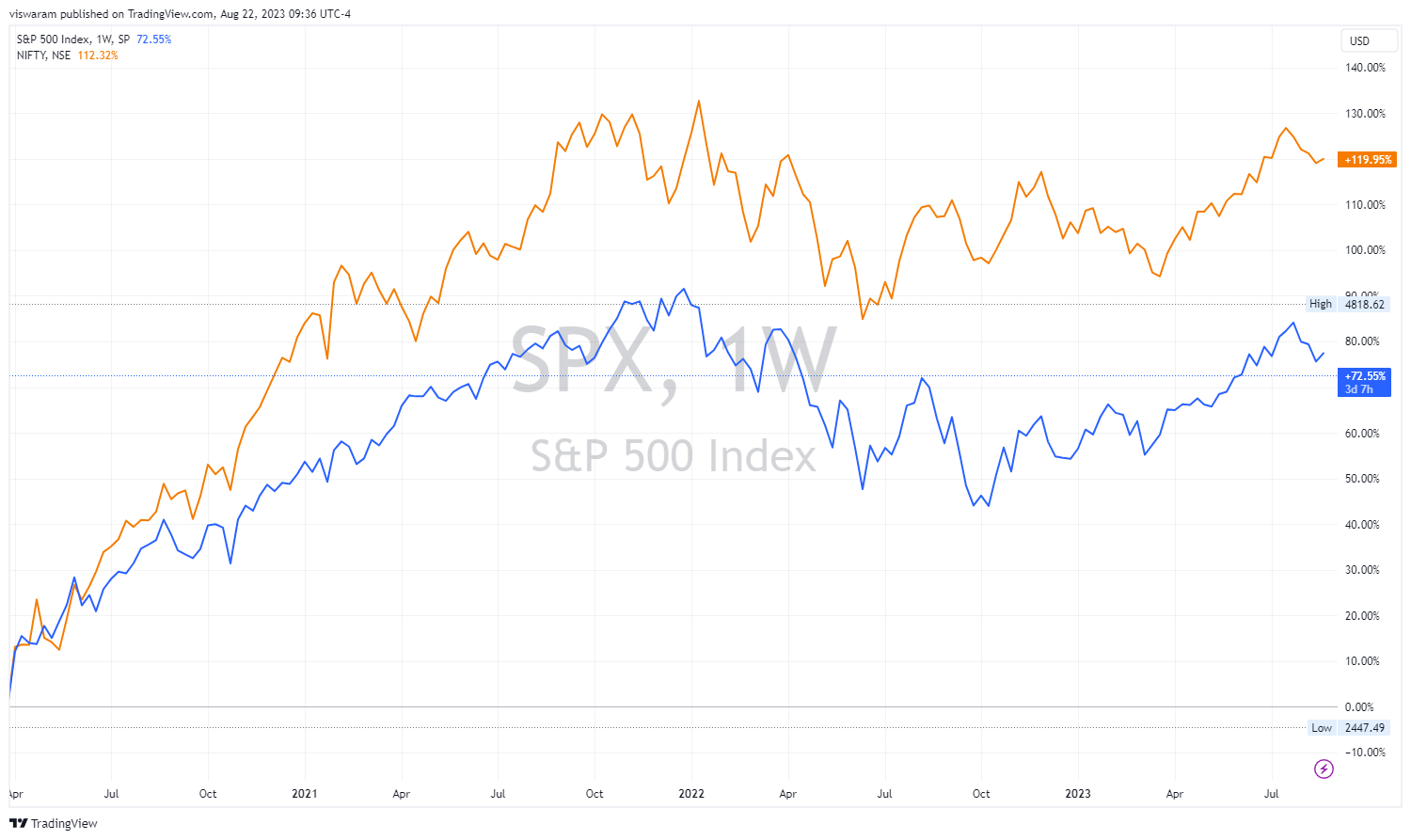

Correlation between S&P 500 and US 20+ year bonds:

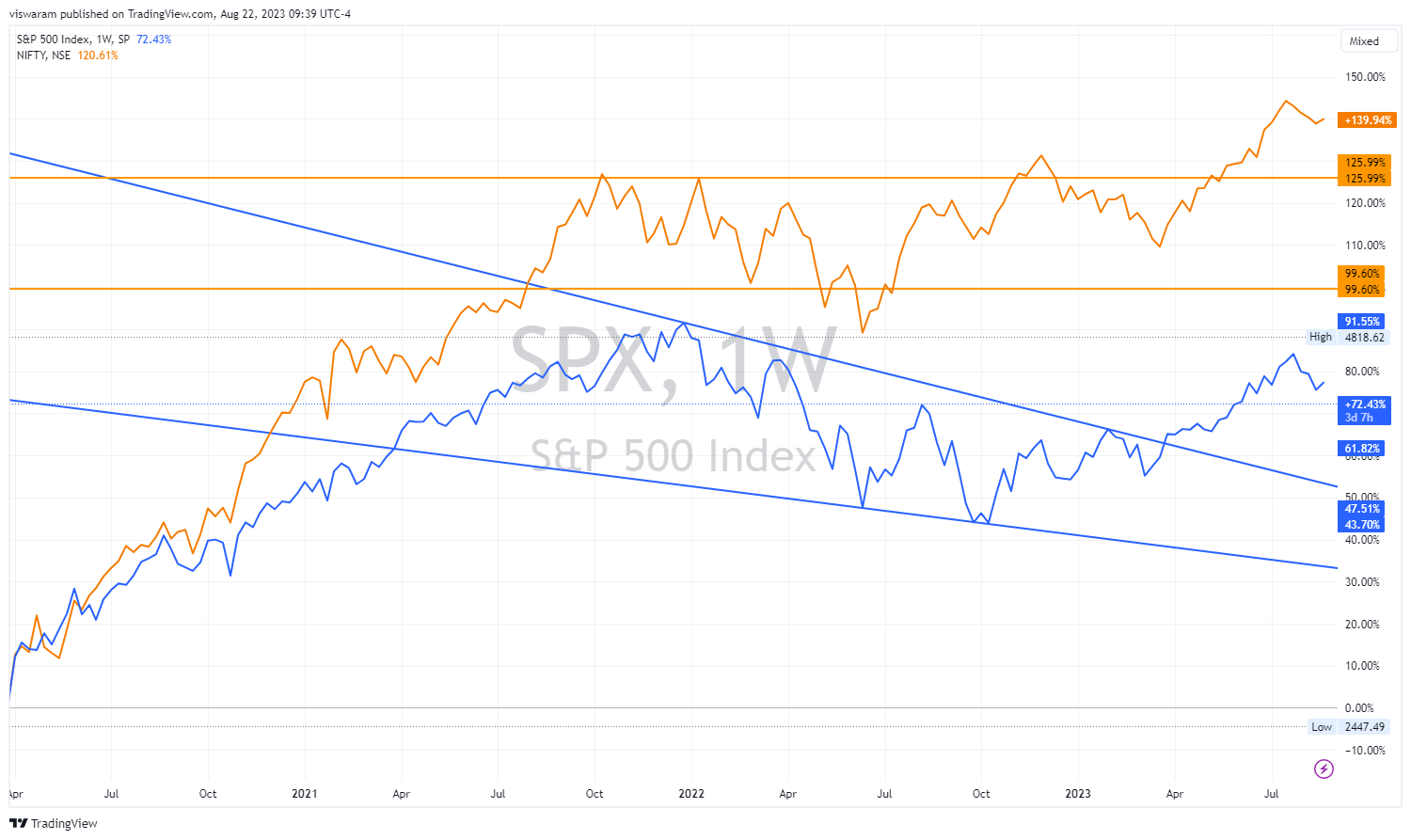

Correlation between Nifty and Indian Government 10 year bonds:

As we can see in the above charts, we can hardly see a -0.37% negative correlation between Nifty and 10 year bonds and the correlation is surprisingly +0.44% when it comes to the US markets.

So, if you short the markets purely looking at the interest rates, you will either be making meager returns or even losses - One thing is for sure you will be disappointed. ![]()

So, what’s holding up markets?

The thing about markets is one can never be able to pinpoint at some things and say - this is happening because of that. But let’s try anyway.

Here are some of the reasons I can think of:

US:

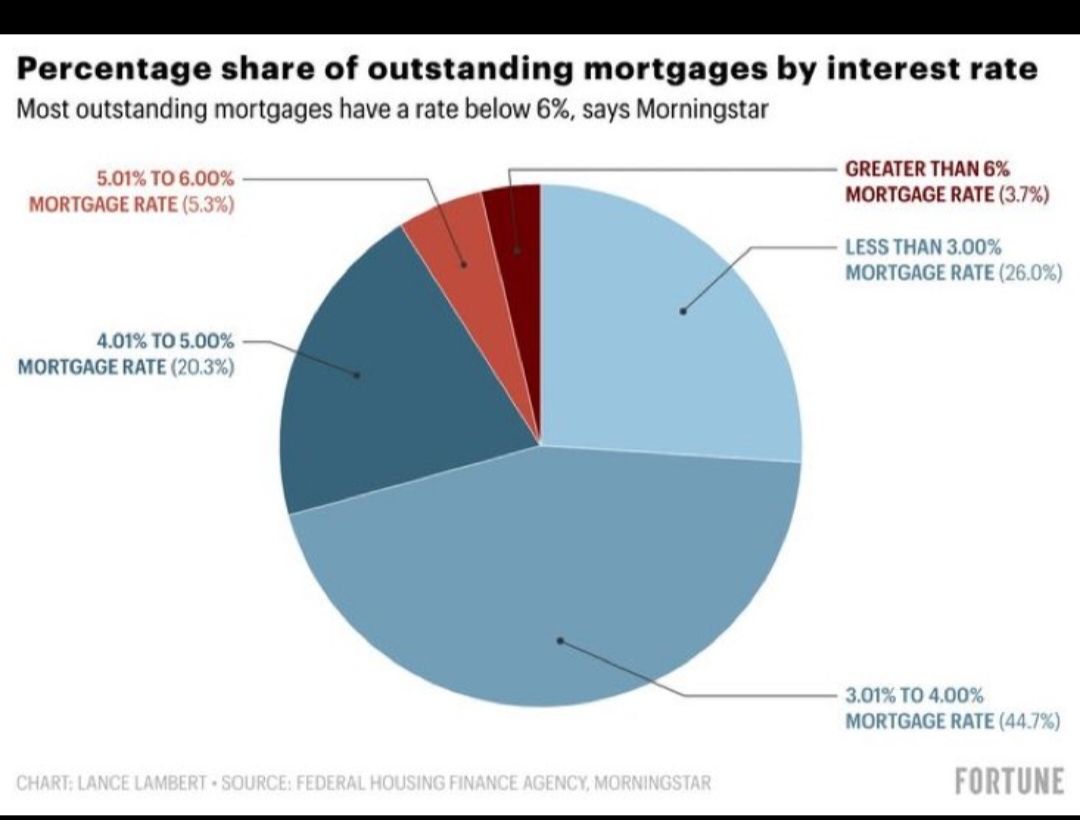

91% of the outstanding mortgage loans are under 5.01% in the US. Consumers are definitely facing pressure on higher interest rates when compared to the last 2 years but, below 5% seems still manageable for most of them at least till now.

Consumers who want to buy a new house using mortgage are the ones who are seeing the most pain now as the affordability is now at 40 year lows as fresh mortgage rated topped 7.15%

https://finance.yahoo.com/news/us-mortgage-rate-climbs-7-125042869.html

So, who will most likely face the biggest brunt in this? The banks - When we have 90% people locking their interest rates at 5% and below and rates closing 5% . What will the banks be left with? Extremely compressed margins and potential bad loans and therefore, are already facing downgrades from multiple credit agencies.

So, yeah, things are holding up for now. But, this time it feels like the US economy needs a helping hand from the global economy to get themselves out of this trouble.

Europe:

Things are comparatively better in Europe. Despite higher rates, The inflation is heading lower and there are hopes that we may eventually see a decent cool down in Inflation and eventually the rates going forward.

https://www.reuters.com/markets/europe/german-producer-prices-fall-60-yy-july-2023-08-21/

China:

This is where things are getting more and more interesting and murkier for the second largest economy and World’s manufacturing hub.

Here’s how things started getting messier in China in the past few years:

-

When the world was shut down due to the pandemic, there was obviously slow down in the exports due to demand destruction and also, supply chain troubles.

-

And when the world started recovering slowly in 2021, Their strict covid policies previously meant, the pandemic pain was only delayed. Added to this, things started cracking up in the real estate space starting with It’s second largest real estate developer Evergrande defaulting. It’s been 2 years since that event but the trouble is only getting worse day by day as the Chinese real estate index is down 82% from May 21 peaks.

China is also facing a geopolitical challenge where countries are moving out their manufacturing base and want to depend less on China.

Parting thoughts:

With China facing a serious threat being posed on its exports and massive construction and real estate growth based economic model, and US and co. facing issues related to higher interest rates. We are stuck between one side trying to bring down inflation with higher rates while the other side is slowing down the global economy.

And maybe that’s why markets are just confused and are just staying in the range for now.