AMFI recently celebrated its 25th anniversary and released a factbook in association with CRISL. Here are some interesting numbers about the industry.

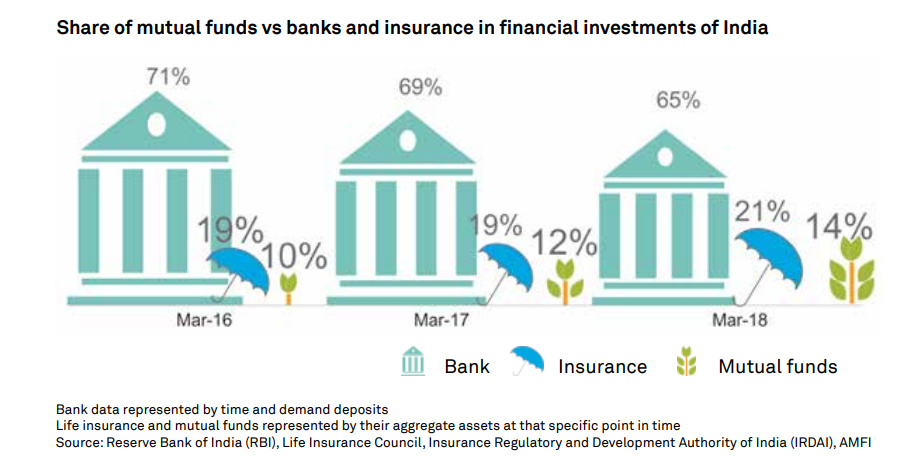

The ratio of the industry’s assets under management (AUM) to bank deposits has grown from

13% as of March 2016 to 22% as of March 2018.Growth has not been just an urban phenomena. Assets under management from cities beyond the top 15 (B15) have grown at 32% annualised since 2014.

Money entering mutual fund schemes through the digital route has multiplied from ~0.5% of gross inflows two years back to ~10% in June 2018. - Ashu Suyash MD & CEO, CRISIL Ltd.

History of the Indian Mutual Fund Industry

1963: Formation of the Unit Trust of India

1964: Launch of the maiden scheme of UTI-Unit Scheme

1987: Entry of public sector funds SBI Mutual Fund was first one followed by Canbank Mutual Fund

1993: Emergence of private sector funds Franklin Templeton (erstwhile Kothari Pioneer) was the first of its kind

1993-2003: Robust growth and revised MF regulation from SEBI in 1996, entry of foreign funds, several mergers and acquisitions.

2009: Removal of the entry load

2012: Single plan structure for mutual fund schemes l Cash investment allowed in mutual funds l Fungibility of total expense ratio (TER) allowed l Portion of TER to be used for investor education l Entire exit load to be credited to the scheme l Launch of Rajiv Gandhi Equity Savings Scheme (RGESS)

2013: Reduction in Securities Transaction Tax (STT) for equity funds l Uniform Dividend Distribution Tax (DDT) of 25% on all debt mutual funds l Product labelling l Introduction of direct plans

2014: Changed the definition of ‘long term’ for debt mutual funds to 36 months from 12 months for LTCG l Tax exemption limit for investment in financial instruments under Section 80C raised to Rs 1.5 lakh from Rs 1 lakh

2015: Launch of MF Utility (MFU) - Digital aggregator platform by the industry, for the industry l SEBI asked fund houses to shift from colour coding to Riskometer which classified schemes based on the risk profile l EPFO started investing in the equity market via Exchange Traded fund (ETF) l SEBI allowed gold ETFs to invest up to 20% of their assets in the government’s Gold Monetisation Scheme

2016: SEBI tightened norms for mutual fund investment in corporate bonds l Allowed investment advisors to use the infrastructure of the stock exchanges for sale and purchase of mutual fund units l Provided easy entry to the foreign fund managers keen to enter India

2017: SEBI allowed mutual funds to invest in REITs and InvITs l Allowed investment up to Rs 50,000 per mutual fund per financial year through digital wallets l Instant access facility to the liquid funds investors (via online mode) of up to Rs 50,000 or 90% of the folio value, whichever is lower l Government discontinued the tax benefits of RGESS

2018: SEBI asked fund houses to benchmark returns of equity schemes against a total return index (TRI) l SEBI introduced categorisation and rationalisation of mutual fund schemes making it simpler for investor to understand l LTCG of 10% without indexation introduced for equity-oriented funds for investment horizon of > 1 year, subject to capital gains of over Rs 1 lakh per assessee per year. Dividend plans of equity-oriented funds subject to a DDT of 10%, deducted at source l Mutual fund houses asked to disclose TER for all schemes under a separate head on their websites on a daily basis l SEBI further redefined the scope for T15/B15 cities to T30/B30 and push for higher penetration

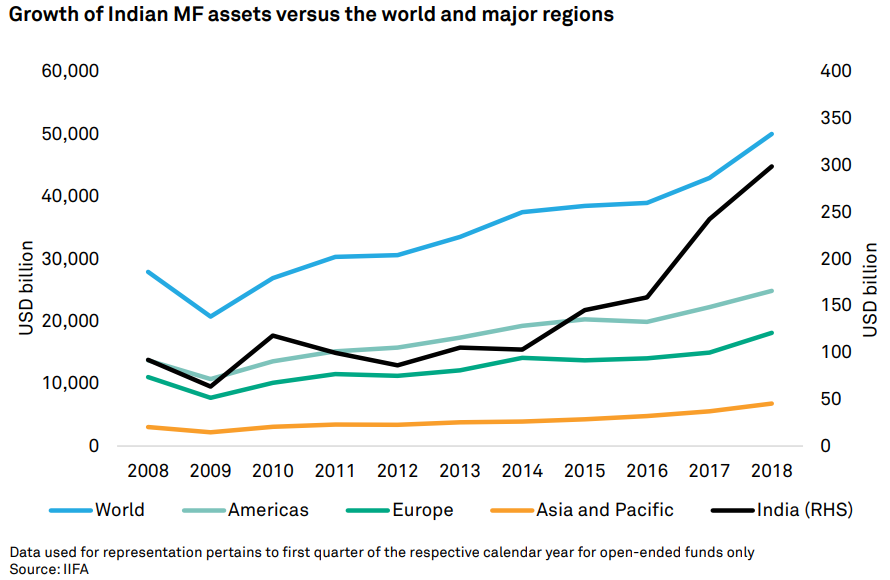

Growth of MF assets in India Vs other major countries

Share of mutual funds vs banks and insurance in financial investments of India

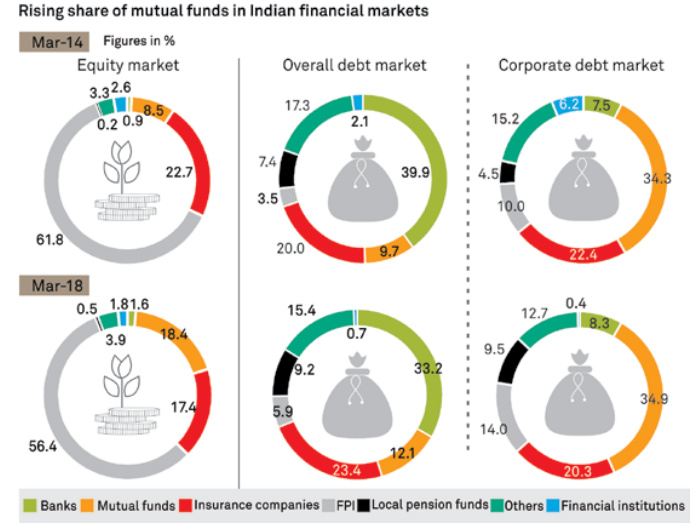

Share of mutual funds in the financial markets

AUM break-up of the industry new structure

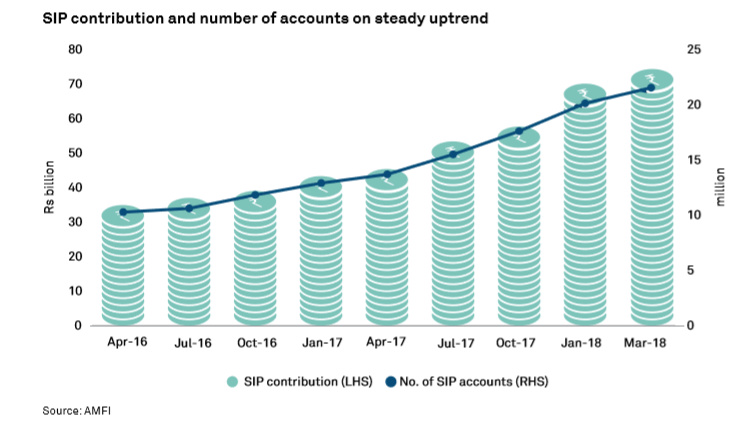

SIP contribution and number of accounts on steady uptrend

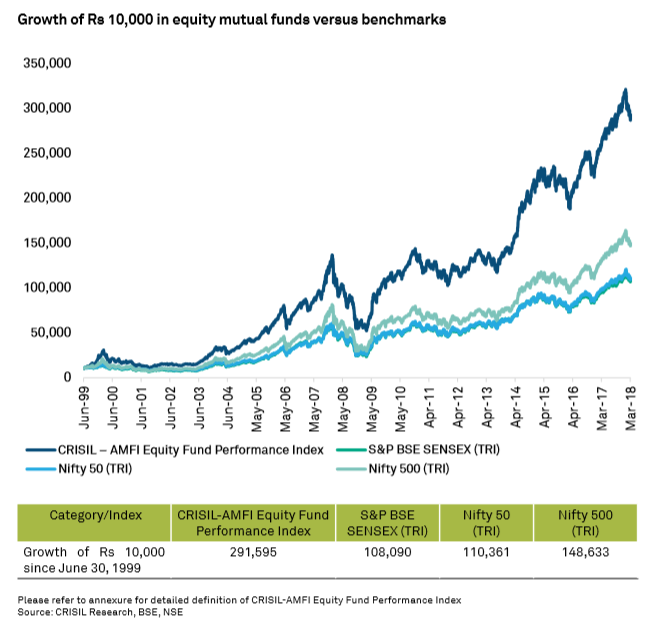

Growth of Rs 10,000 in equity mutual funds versus benchmarks

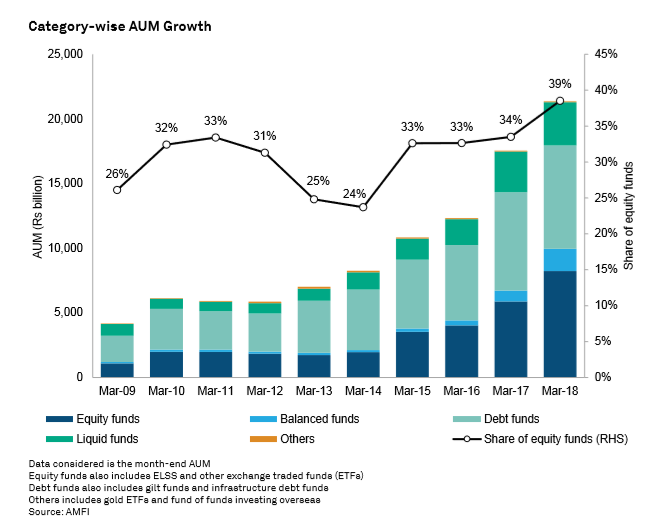

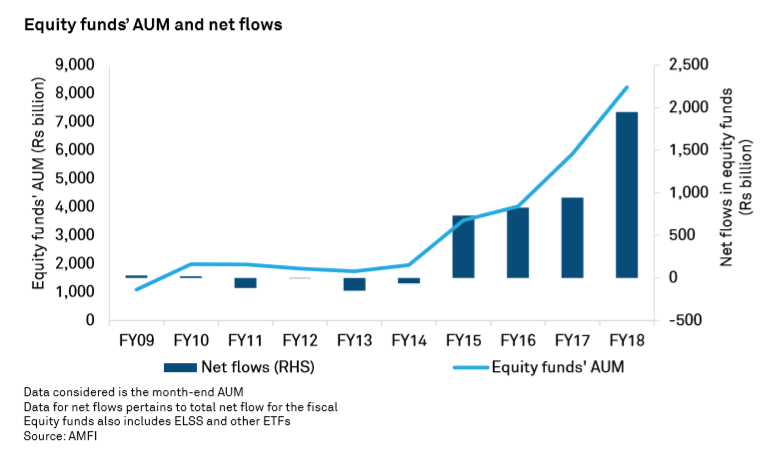

Debt dominates, but equity catching up in assets and inflows

Equity funds’ AUM and net flows

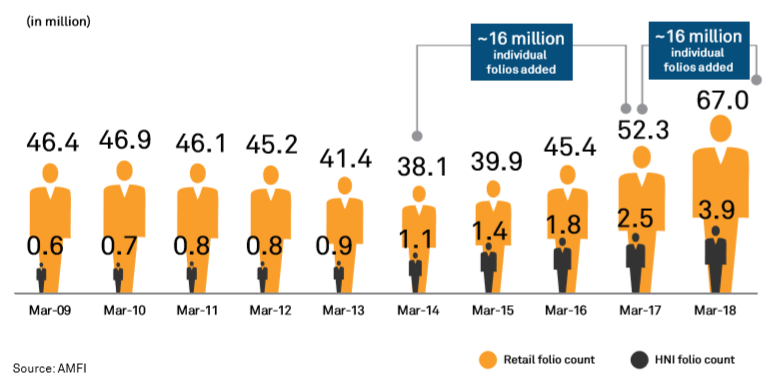

Individual investors gaining momentum

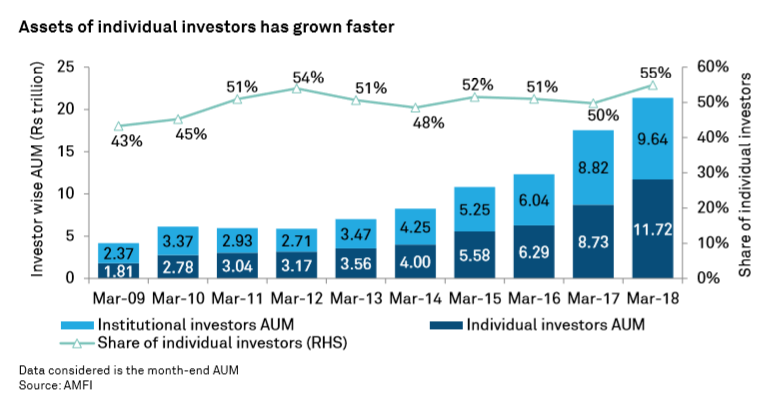

Assets of individual investors has grown faster

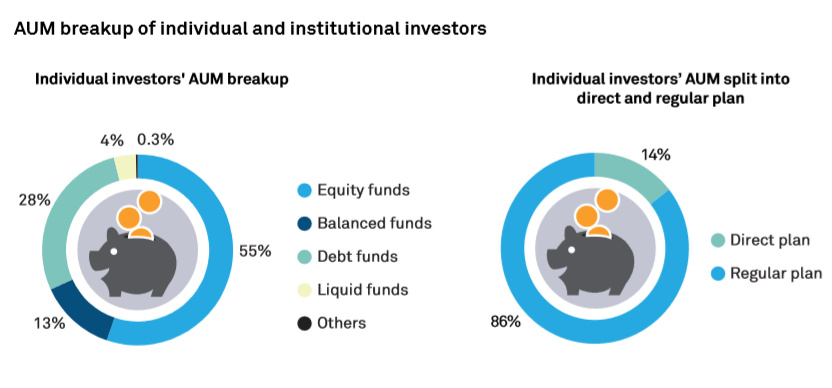

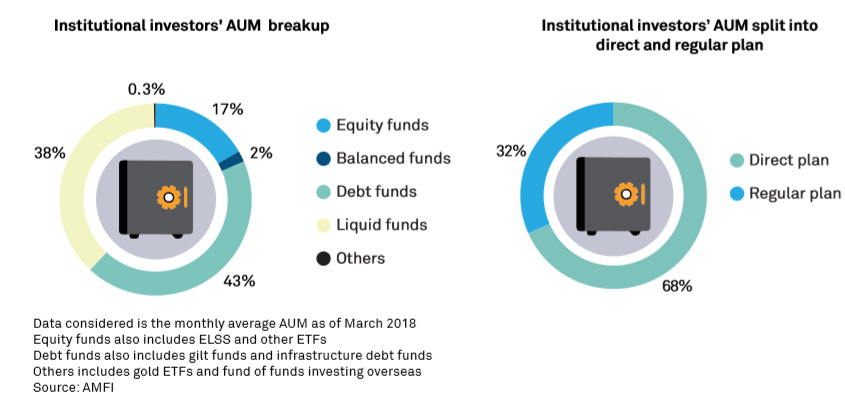

AUM breakup of individual and institutional investors

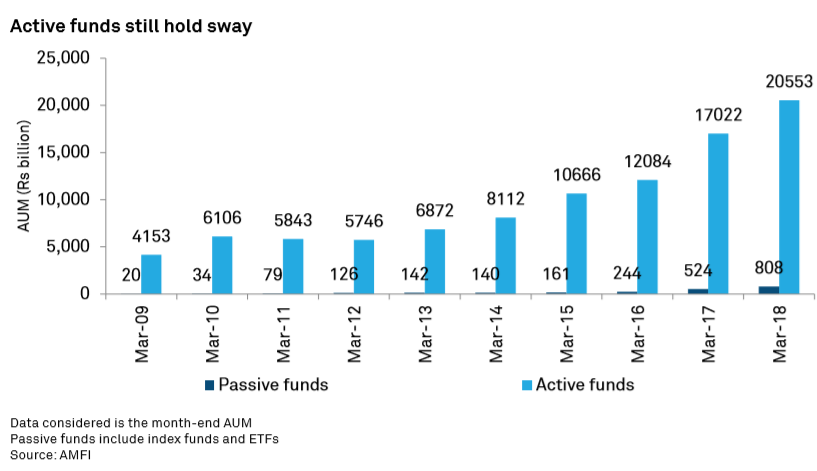

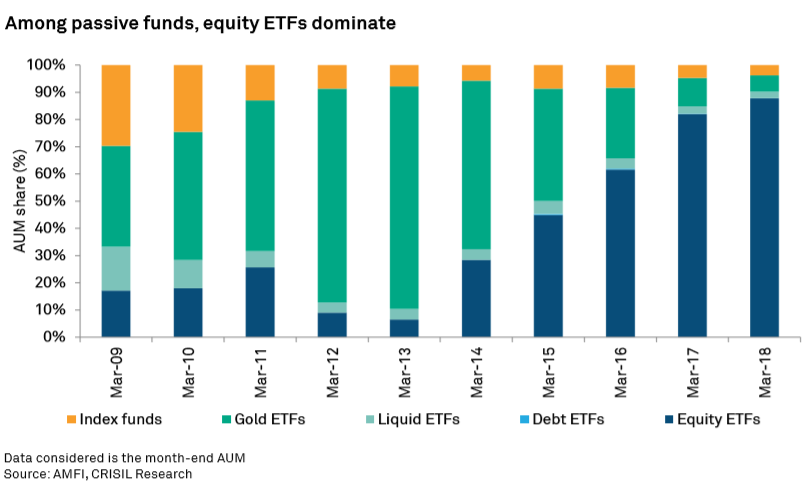

Passive funds gaining popularity