Young investors who start their professional lives. do not generally have savings and investments at the top of their minds. When one receives the salary, the focus is more on spending and enjoying. However, with the rising unemployment due to the pandemic-induced economic deceleration, many youngsters have understood the importance of investing. For those who are serious about investing, the primary question is where to invest.

Risk – Reward Payoff of investment avenues

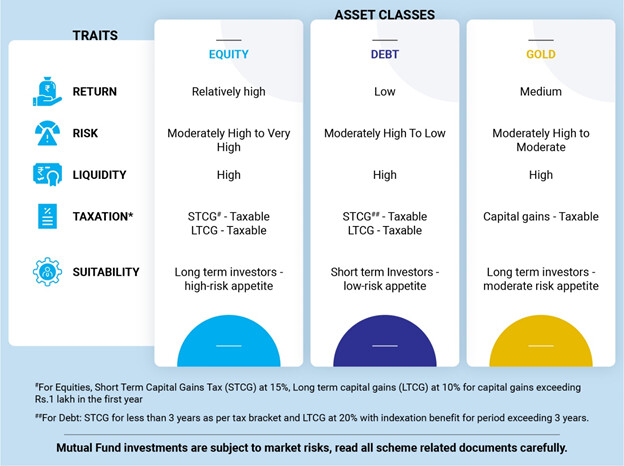

Understanding the Asset Classes

Equity

As a young investor who has a long working life to invest, and the advantage of time to their side, he/she could explore equities. Equities tend to outperform other asset classes in the long run due to:

- Economic recovery

- Earnings upgrade cycle, and

- Strong policy support, if you are looking for a well-researched and diversified pool of stocks that is professionally managed, you may want to consider an equity mutual fund.

Debt

For those with a low appetite for risk, then Debt funds are a good option. Debt funds are less subject to market uncertainty and hence are less risky than equity funds. If you have been saving in traditional fixed income products like Fixed Deposits, and looking to earn relatively higher returns, then debt mutual funds could be a better option.

Gold

Gold is inversely correlated to equities and acts as a good diversifier for investment portfolios allowing investors to reduce risk and optimize returns in the long-term. While traditionally, owning gold means to purchase physical gold bars, coins and jewellery, these can pose challenges: ETFs and mutual funds that invest in gold are increasingly becoming popular options of buying gold among young investors today.

Disadvantages of owning physical gold

- Storage and security

- making charges add to the price markup

- Illiquid

Advantages of Gold ETFs

- Prices on par with market price of Gold

- Can be traded using a demat account

- Offer safety & convenience of buying at the safety of one’s home 24X7 online

Planning your investment portfolio

For new age investors who are just starting their investment journey, it is imperative to understand a few things such as (a) Asset allocation & rebalancing, (b) affordability of investments, (c) multi asset allocation & (d) saving tax.

Asset Allocation and rebalancing

Instead of heavily concentrating on one asset class, it is suggested that investors should have an asset allocation plan for diversifying in different asset classes, such that it allows investors to spread your risk within your portfolio.

After allocating assets in equity, debt and gold in the desired proportion, following the basic principles of asset allocation and regularly rebalancing the portfolio remains essential. It is suggested that investors follow the asset allocation rule of 12-80-20* to build their portfolio. Investor need to set aside 12 months of monthly expenses in a liquid fund. Emergency situations like loss of a job, medical emergencies can arise any moment and drain your savings. The balance 80-20 can be allotted to Equity and Gold.

Staggered investments suitable for any wallet size

Salaried individuals can opt for the convenience of an SIP (Systematic Investment Plan) as it averages out the cost of purchase in the long term and is suited for any wallet size – as low as Rs.500 per month.

Multi Asset Allocation

For those investors who have not yet allocated to equities and are not sure what should be your ideal equity allocation, they could gradually start off with a multi asset fund of fund and give their money the potential to grow while also mitigating downside risks. This Mutual Fund diversifies investor’s money across asset classes such as equity, debt and gold depending on market conditions while aiming to generate long-term risk adjusted returns.

Tax Savings with ELSS

Those looking to invest in equity mutual fund with an added tax advantage can look at investing in Equity Linked Savings Scheme which offers upto Rs. 150,000 tax exemption u/s 80C. It offers twin benefits of tax savings and opportunity to build wealth by investing in equities for the long term vis-a-vis other tax saving instruments.

*Please note that the suggested asset allocation is not to be considered as investment advice/recommended allocation, please seek independent professional advice and arrive at an informed investment decision before making any decision.

Disclaimer: The views expressed here in this Article / Video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The Article / Video has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of the Article / Video should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. None of the Quantum Advisors, Quantum AMC, Quantum Trustee or Quantum Mutual Fund, their Affiliates or Representative shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary losses or damages including lost profits arising in any way on account of any action taken basis the data / information / views provided in the Article / video.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.