Is it a good time to invest in Gilts funds? I wish to invest in Gilt funds for at least 5 years, but I am concerned about the volatility in this category. Is it advisable to do a STP from Liquid fund to Gilt fund to average out the variations, or should I not worry and make lumpsum investment in one go? If doing a STP, what should be the duration of the STP?

Unless you are fully aware of the risks of Gilt funds it’s advisable to stay away from this category because it is incredibly volatile. When it comes to debt funds the two biggest risks or

- Credit risk - risk of company not paying or going bust

- Interest rate risk - change in bond prices due to interest rate movements

Now, with gilt funds, there’s no credit risk because unless the Govt of India goes bankrupt, you’ll get your money back. But that doesn’t mean there’s no risk, you’ll still have to bear the interest rate risk. Before that there are 2 types of Gilt funds

Gilt funds

10-year constant maturity Gilt funds.

A normal gilt fund can vary it’s maturity based on the fund managers view of the interest rates. But a constant maturity Gilt will have the average duration of 10-years at all time, tracking the yield of the bechmark 10-year Gsec.

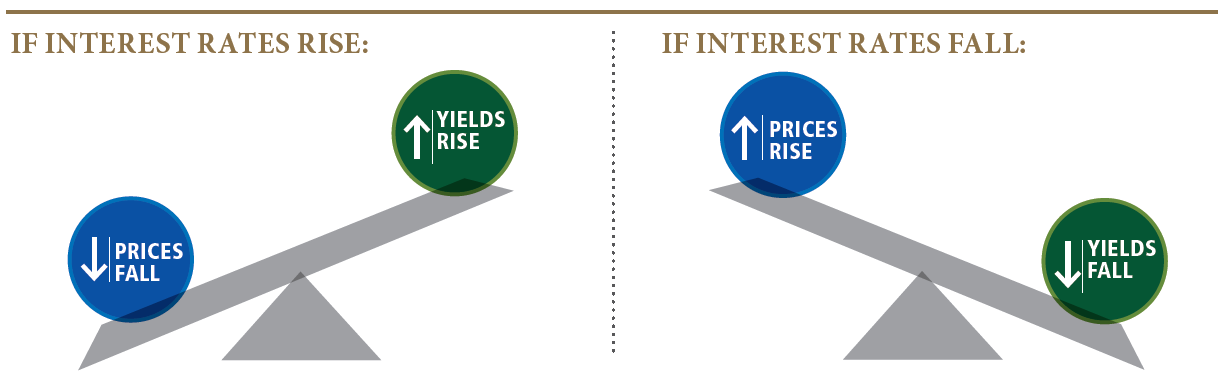

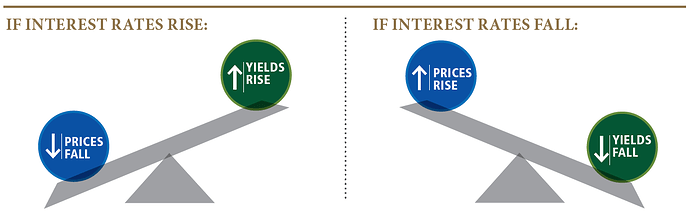

Now, coming back. Interest rates and bond yields have an inverse relations ship.

Source: PIMCO

Meaning as interest rates fall, bond prices rise, because the older bonds now just became more valuable because they have higher coupons (interest payments). Falling rates are always good for bonds and this when these Gilt funds make money for you. On the other hand, they lose money during phases when the interest rates are rising.

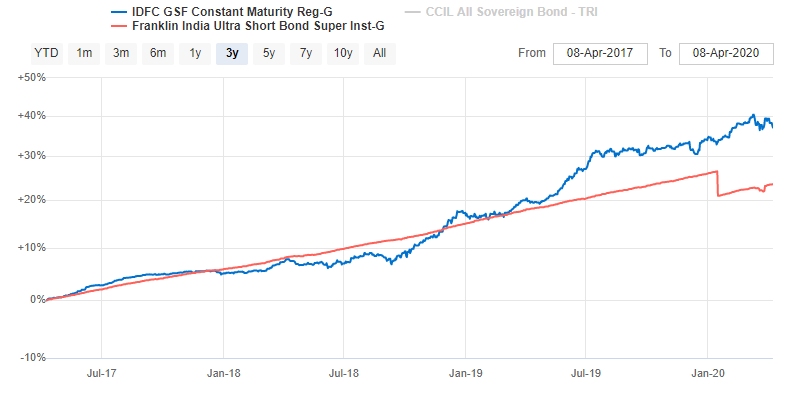

So buying Gilt fund for most people makes sense only if they have a deep understanding of interest rate cycles. In the past couple of years, we have been on a massive rate cut cycle and hence the returns on Gilt funds have been phenomenal

But if the world returns to normal post-Corona and RBI starts raising rates, the returns fall for Gilt funds. Also, look at the volatility in the fund’s movements compared to an ultra-short fund. 2-5% drops in the NAV are quite common.

So unless you have the ability to time the interest rates and use GILT funds tactically, I don’t think these funds make sense. For most parts, a short duration fund or corporate bond fund is all most retail investors need.

Please do consult your advisor. Hope this helps.

Also, check out this series of webinars we had done on bonds

6 Likes

@Bhuvan Thanks for the explanation. I have a few questions though.

Ex. One AMC has a 10-year gilt fund with 2 GOI securities. one at 6% and the other at 7%.

- What is the likely interest rate risk if I hold the bond for 10 years?

- Will I get around 6.5% annual return minus the expense rate?

OR Will the AMC keep trading the bonds to keep bond maturity at 10 years in which case I am more susceptible to the losses incurred due to capital loss on the bond.

Other questions not specific to 10-year gilt funds:

3. Is it possible that the return on the gilt fund can be lower than the lowest coupon gsec they hold for the long term, say 10-15 years?

4. Is it just better to buy GSECs when the interest rates are high and sell them in the secondary market when interest rates fall? (if they are available at the time. ex. 8-9% GSECs were issued during 2018-2019). Now they might be valued at 1.25 times face value which might put return at 10-15% which is comparable to GILT funds without interest rate risk.

5. Is buying 8-10% coupon PSU bank bonds even better considering they have a huge government stake? What are the possible risks to consider before buying A- to AA+ PSU bank bonds?

6. How is it that GILT funds are susceptible to such huge interest rate risk while ones such as short term or corporate bond funds are not?

7. Is there any resource I can use to understand GILT funds better. Even though I understand bond pricing, it’s extremely hard to understand and quantify interest rate risk.

Please add any other points you may see fit and correct me if I am wrong in my assumptions anywhere.

Thanks!

"

“Now, coming back. Interest rates and bond yields have an inverse relationship.”

I think the above statement must be corrected. Bond price and yield is inversely proprtional.

But interest rate and yield are in same direction

1 Like

You can read that as bong prices and interest rates have an inverse relationship.

Nobody knows

Can’t predict returns. Depends on interest rate movements. Plus, the portfolio of gilt funds isn’t static, the manager changes the duration based on his views on the interest rate cycle. The duration stays constant only on 10-year constant duration gilt funds - regardless of the interest rate cycle, the maturity of the portfolio remains the same at 10 years. Gilt funds and constant 10-year maturity gilt funds are 2 separate categories.

The returns in some years have been negative as well. Read this post:

Sounds good in theory but hard to do it. Timing interest is next to impossible for average investors. Better not try it.

They have an implied sovereign guarantee, not an explicit sovereign guarantee and there’s a first time for everything. What if some PSU is in trouble and the govt lets it fail for the first time? Highly unlikely but you never know. Plus the govt is reducing stake in all PSUs, it’s a thing to keep an eye on.

Shorter the duration of a fund, lower the sensitivity to interest changes and vice versa. Gilt funds always hold Gsecs which have higher durations (maturities). This is a tricky concept to understand and explain in a post. Better if you watch these webinars

Watch those webinars. There Investopedia, Khan Academy, Coursera and a 100 other resources which you can find by Googling a bit ![]()

2 Likes

I am looking to get into some gilt funds to fund the cash collateral. The money market funds are okay-ish but I’d like to give the cash collateral returns some “teeth” per se and allocate 40% of cash collateral to gilt funds. This may not be the ideal time for Gilt, but over the years good gilt funds have proven to be rather consistent, across high interest and low interest environments.

Nippon India Gilt Securities (year by year)

2014 - 20.06

2015 - 7.52

2016 - 18.31

2017 - 4.58

2018 - 9.03

2019 - 13.39

2020 - 12.29

Edit:

It appears the very long term performance has been subdued.

Below are all Regular Funds (to compare very long term performance)

Nippon India Gilt Securities since 2003 has offered only 6.42% CAGR

ICICI Prudential Gilt Fund since 1999 9.94%

SBI Magnum Gilt Fund since 2000 8.3%

Views invited.

2 Likes

Even I have similar doubts , so have you found any answers ?

i Purchased SGBs so that 50% of cash collateral is done and remaining 50% I am planning either gilt funds or liquid funds . you have any suggestions for me?

Also one basic doubt can we exit gilt fund whenever i feel like ? or is there any lock in period?

1 Like

hi @Bhuvan

I know you are a busy man , but genuine request , is there any lock in period in gilt funds , say axis / idfc gilt funds ? or i can exit them whenever i feel like.

Sorry missed this. No lock-ins but there’s an interest rate risk component here

Thanks Bhuvan , all this confusion because in COIN it doesnt show any info of fund except the ‘buy’ button .

if you can mention few details like Riskometer , lock in period , manager name , past 10 year performance it would be helpful all of us naive investors

You can se the fund presentation (pdf). You’ll get all these details

1 Like

Where can you fund presentation?

@TradeXMaster even worse coin doesn’t give proper link of the PDF it gives some random page .

I don’t want to be harsh here but @Bhuvan the Head of coin is definitely sleeping . its not personal attack but when you compare kite and coin … its so contrasting it looks sooo discouraging to open coin except for my collateral otherwise I wont even bothered here commenting about it.

P.S: Big fan zerodha

1 Like

Best place to find that would be fund AMC’s website.

1 Like

so finally, what did you choose for cash component? and what’s your allocation for each category.

currently i am having 60% money market, 40% gilt. Looking for more diversification