As Children’s Day passed last week, it took me back to the first financial lesson I learnt as a teenager, even if I didn’t fully understand it back then.

I was 17 years old, just out of home, and adjusting to a new city. My dad used to send me Rs 5,000 every month. Half of it went straight to my hostel rent, and the rest was supposed to cover my other needs.

But five or six months into this new life, the excitement of freedom got the better of me. I skipped paying rent on time and started overspending, assuming I would somehow “manage ” later.

This happened about fifteen years ago, and I still remember the sinking feeling in my stomach when the hostel warden gave me a final warning to pay up. I remember the guilt of spending the money and the hesitation before calling my mom (who always comes to the rescue) to arrange the funds for me.

That moment, embarrassing as it was, ended up teaching me one of the most important lessons about money: always clear your dues the moment money comes in. Even today, the first thing I do when my salary hits my bank account is to pay off my monthly bills.

That early financial mistake in my teens played a big role in shaping how I think about money today.

Most of us learnt about money management through trial and error, especially when we leave home or earn our first paycheck. Some of us manage to course-correct, while others repeat the same patterns for years. And the truth is, the older we get, the tougher it becomes to change the financial habits we’ve built.

And there’s enough evidence showing that building financial knowledge at a young age improves financial behaviour in later years.

The evidence (in a survey of more than 1.6 lakh individuals) shows that financial education programs have, on average, positive causal treatment effects on financial knowledge and downstream financial behaviors.

Despite that, most schools in India still don’t teach children how to manage money. So the responsibility naturally falls on parents to introduce these lessons using real-life experiences.

In this week’s Second Order edition*,* let’s look at the different financial products you can open in your child’s name. You can always save for them in your own account, but if you want something officially under their name, so that you can teach them or save for them, these are the options available.

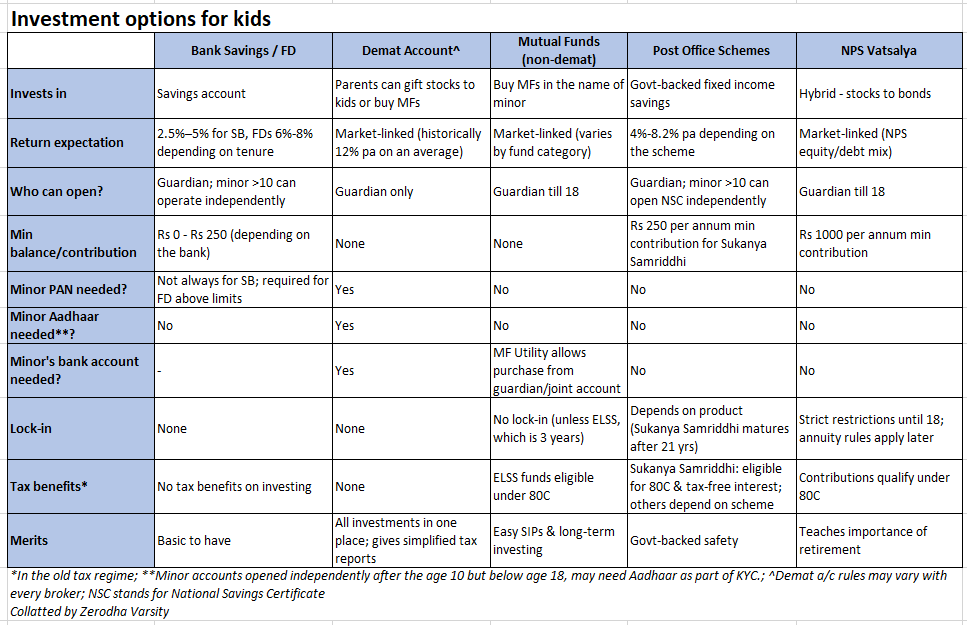

Savings bank accounts for kids

For most parents, the first step in introducing money to their kids is opening a simple savings account in the child’s name. Children above 10 can now operate these accounts independently, while for younger ones, the guardian can open and operate on their behalf. The account operates similarly to a standard savings account, but with certain limitations. Further, a fixed deposit can also be opened in the name of a minor through a guardian.

Banks also issue debit cards to older kids, typically with a small daily limit, such as ₹5,000. Some banks even offer UPI and internet banking for these accounts, which is useful because kids today are growing up using digital payments anyway.

If your child doesn’t have their own bank account yet, there’s also a feature in UPI that you can make use of for payments. ‘UPI Circle’ lets your child make online payments using a UPI platform on their device, but from your bank account. You stay in full control, as you can set visibility and limits.

Demat account for kids

Some brokers also let you open a Demat account for your child. Through this, kids can’t directly buy stocks or trade on their own. But you can gift shares from your Demat account to theirs.

If their bank account supports UPI or online banking, mutual fund purchases (lump sum or SIP) can happen directly from the minor account itself. Any money from selling investments in the minor account is always deposited into the child’s bank account only. These features may vary from broker to broker, so it’s best to check before proceeding.

To open the account, the child needs their own PAN, Aadhaar, and a bank account. But once it’s set up, it becomes easier to keep all their investments in one place, and most platforms give tax-compliant statements that simplify reporting.

All investments stay in the child’s name until they turn 18. After that, the account is converted into a regular Demat account with fresh KYC in the child’s name.

Mutual funds for kids

See, it is always best to start with a bank account in the child’s name. That makes it possible to open a demat account easily.

But if your child doesn’t have a bank account yet, you can still invest in mutual funds in their name using a platform called MF Utility (register eCAN in the name of the minor).

Depending on how it’s set up, the money for investing can come from your own account, a joint account (with minor), or the child’s account. The investments stay in the child’s name while you manage everything as the guardian.

If you ever sell these investments, the sale amount must be routed to a minor bank account or the joint account of the guardian with the minor. Otherwise, the transaction will be rejected.

And once your child turns 18, the folio has to be shifted to their name with the usual KYC. The hassle at that point would be that you’ll need to update the details with each mutual fund company or RTA where the child has investments.

Sukanya Samriddhi & Post Office Schemes for kids

For families with a girl child, the Sukanya Samriddhi Account is a popular option that currently offers an interest rate of 8.2% per annum. You can open it anytime before your daughter turns 10.

You must deposit a minimum of ₹ 250 to ₹1.5 lakh a year for a period of 15 years from the date of opening of the account. The account matures after 21 years.

Other post office products, like Recurring Deposit, Time Deposits, and National Savings Certificate (NSC), can also be opened for minors. A guardian can open these on the child’s behalf, and in some cases, kids above 10 can operate them independently. These are simple, government-backed products.

By the way, we wrote about how much to save for children’s education here.

NPS Vatsalya for kids

National Pension System’s ‘Vatsalya’ is another option that allows parents to open a retirement account in their child’s name. A minimum contribution of ₹1,000 a year is required. At 18, it becomes a normal NPS account once KYC is updated.

When I first heard about NPS Vatsalya, I immediately felt they were taking the idea too far.

But as it lingered in my mind, it struck me that it doesn’t have to be about building their entire retirement fund. It could simply be a tool to start a savings habit early.

But the withdrawal rules for NPS are quite strict: before the child turns 18, only a few partial withdrawals are permitted; and even after 18, 80% of the money withdrawn must be invested in an annuity, with only 20% paid out.

Because of this, it’s best used as a way to teach kids about long-term, retirement-style investing rather than as a main investment option.

The 3-Jar framework

Apart from the above investment products, you will also come across many child ‘money-back’ insurance plans. These usually combine low-return investments with high-cost insurance, making them poor choices. A simple term insurance policy for the parent does a far better job of protecting a child’s future than any bundled child plan.

No matter how many accounts or investments a child has, nothing can replace regular conversations about money between parents and children. Kids learn the most when they see money being used in real life. Some of the most effective and proven ways to build good money habits are letting kids make small decisions at home, involving them in grocery shopping, and even asking them to pick and choose items and pay at the counter.

One popular method that financial planners recommend for parents, especially those with children under 10 years old, is the 3-Jar framework. In this framework, any money the child earns or receives is divided into three jars: a spending jar, a saving jar, and a giving jar.

For example: If a child receives ₹300 as pocket money, they could put ₹150 in the spending jar for immediate wants, ₹120 in the saving jar for something bigger they want later (like a toy or game), and ₹30 in the giving jar for donation or buying gifts for others. This simple structure is likely to teach them the importance of budgeting and delayed gratification.

By the way, at Varsity, we already have a few initiatives running to help kids learn about money in simple and engaging ways. Rupee Tales are illustrated storybooks for young readers, while Varsity Junior offers animated videos for slightly older children. Additionally, we run finance quizzes across schools in India.

In fact, we have a free online boot camp for kids scheduled for November 23, 2025, that teaches children about the evolution of money, the difference between needs and wants, and budgeting. Here is the registration link, in case you think your child might be interested.

This Newsletter was written by @Satya_Sontanam

Do read How does WhatsApp make money? newsletter on our Side Notes by Zerodha Varsity.

For any feedback or topic suggestions, write to us at [email protected].