Well thank you , i wanted to know Whether Invts daily prices are depreciating one. on price scale chart Indigrid is moving up, thing is that if any one buys the InvTs without knowing the details , near Invts end life is a disaster

Daily price never have any relation with anything ![]()

Need to look at long term.

For eg. look at this chart of PGINVIT

From May’21 it listed to Oct’22, price was only moving in one direction.

Why? Most likely because all youtube influencer kept on harping about 12% risk free dividend yield. Without ever understanding what an INVIT is.

Then reality hit, and PGINVIT unable to buy new asset compounded the pain.

So in short term prices can go anywhere, only in hindsight you get clearer picture. But again, Indigrid is managing its portfolio really well, so …

1 Like

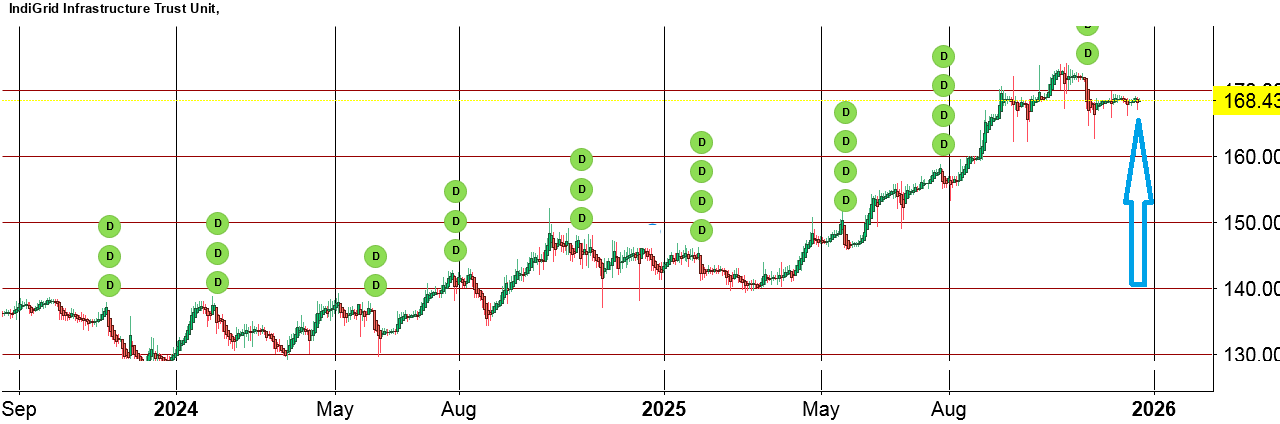

Thank you , i understood the points , what you are trying to say , But still , if you look at the Indigrid chart , dividend payment is very attractive ![]() looks like an ATM machine

looks like an ATM machine

3 Likes

Your analysis is as wrong as it can get. Reason is perhaps you don’t know what a transmission asset, particularly transmission lines, is. To enlighten you, it is to be noted that transmission lines are built for very long period of time. For example 400 kV transmission lines are designed for 50 years and 765 kV transmission lines are designed for 150 years. You can say that they are built for eternity and will certainly outlast us. TSA is executed typically for 35 years. It’s not that after 35 years it will become scrap. It will not. After completion of TSA period the asset will revert to the Invit which it can again lease out to the same entity or to some other entity. This you are hearing from the horse’s mouth. I am a retired engineer from a state transco.

1 Like

Everyone knows what transmission line is. I definitely do ![]()

Can you share some examples where after a transmission line completed its TSA of 35 years, additional contracts were signed with it for continuing transmission.

That data would be more useful than assumption.

I am sure since you have worked with state transco … you will have easy access to data

Invits are in existence for barely 8 odd years. As a corollary TSA is also 8 years old. So no such example can be quoted wherin transmission line has been transferred after completion of TSA. Just to inform that 400 kV transmission lines are designed for 50 years and 765 kV transmission lines are designed for 150 years. Hope this clarifies your query.

Depreciation is notional. Transmission lines will typically increase in value as they are very well maintained and cost of constructing new lines is far higher than older assets simply due to inflation. After 35years their assets will be worth 20 times more than present value.

I do not agree with this logic. A transmission line with an uptime of 99.8percent will continue to be maintained at that level even after its contract life. It is not that the line will simply collapse. Pginvit assets will continue to be owned by company and not transferred to user.After contract terms, there will be a new contract. Transmission asset will have a 100year life.

What you get regularly is profit plus depreciation. But this depreciation is notional. Replacement cost of the asset is actually increasing. Country will always need transmission capacity.

New transmission projects nowadays need to be transferred back to the user at the end of contract and thus have lower value. PGINVIT is in a very sweet spot as they will continue to own assets at the end of 35 year contract.

Your grand children will continue to receive income even after 350years.

1 Like

Whatever be the logic about invit depreciation logic , Indigrid appreciated like a stock , level 144 to level 168 ,it seems it has a lot value in it ![]()

Depreciation is only a book entry. Actually the transmission line has a life of 100years. It’s replacement cost at the end of contract period will be an order of magnitude more than initial value.

It will enter into a new agreement to provide transmission capacity at a higher rate after current agreement expires.

This is if the asset is BOOM and not BOOT.

PGINVIT has BOOM assets. Pginvit will continue to own assets. Boom stands for build own operate and manage. Boot mandates transfer of asset after contract period.

1 Like

True…

Considering even 70 years lifespan for a Transmission Asset and Govt’s shift from BOOM to BOOT strategy will be significant Positive Side for PGInvIT since their current assets are on BOOM basis.

Whereas as per current Govt Strategy, every future asset for any Company of InvIT will be on BOOT basis.

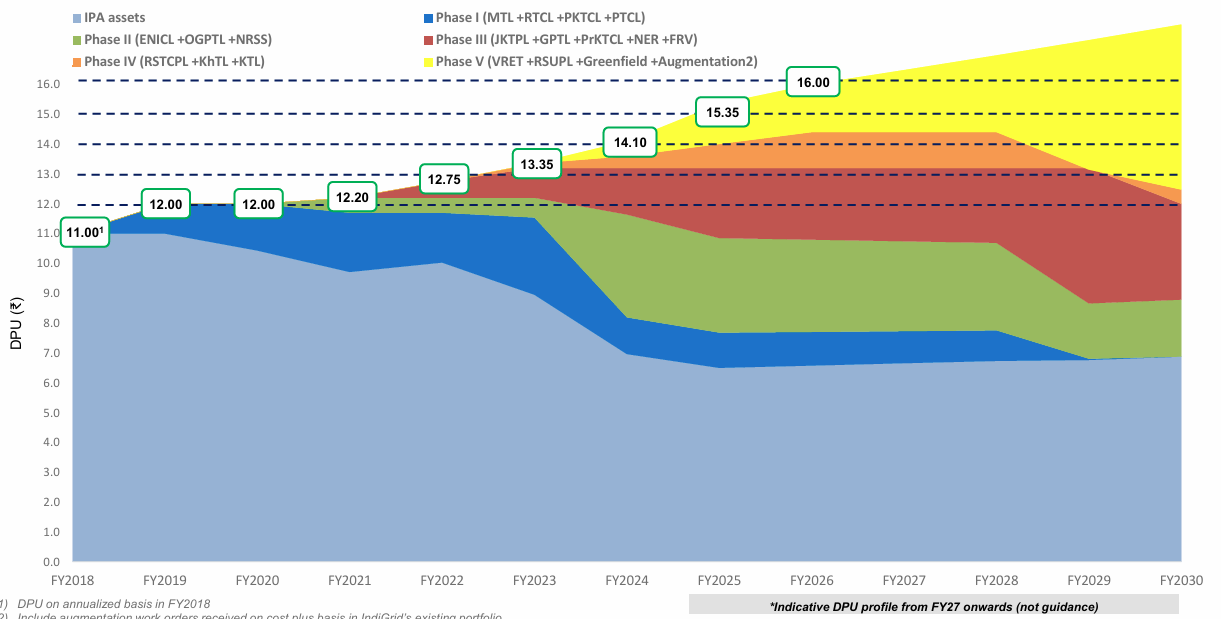

It is true that Rs. 12 DPU can not be maintained without addition of new assets, but it is also not prudent to acquire assets for sake of acquiring assets at excessive price or at price detrimental to existing unitholders.

Also one can simply run a NPV calculation for PGInvIT’s Free Cash Flow per Unit.

Right now, it is actually being treated and valued like a bond by Investors.

Ran a quick calculation…

It is like holding bond with 30 year maturity with varying (decreasing) coupon payout value. The value of equity part is assumed to be near Zero (~Rs. 1 - if valued on par with bond).

Hard disagree. There is logic behind calculating depreciation.

There is a reason, contracts are made for 30-35 years and not 100 years.

Beside you are only thinking about steel, technology also changes.

When India got independence, some of the early transmission lines were of 11kv to 33kv

You think those lines are still in use after 75 years?

No, most got outdated decades back and we are now using 400- 700 KV range. Lot of transmission is also moving from AC to HVDC lines.

So none of those early lines are in use. And new lines are being built and use in its place.

Either ways, there is no point arguing on this. If you feel this asset will be useful for 100 years, go ahead and buy as much PGINVIT as you can. It would be a gold mine if your logic holds.

For all practical purpose, market will only price it for declared useful life (and not assumed) and price of PGINVIT will continue to fall, unless it buys new asset.

Umm, that is precisely the purpose of INVIT, and that is how it should be treated. ![]()

Yes, The assets are still depreciating. But Indigrid is managing its balance sheet really well.

It is using leverage (debt) to buy more assets to increase its DPU, and also used falling interest rates to reduce its cost.

But there is a limit to this (as regulation allows only so much debt) and DPU will fall.

As such DPU has only increased by CAGR of 6% (nothing spectacular), but even a small increase in yield shows up great on NPV calculations, and hence market is rewarding it with increase in stock price.

As such below chart clearly indicates thee depreciating nature of asset. Original assets which were generating around DPU of 11 in 2018 is today around 7-8.

But due to various acquisitions Indigrid has been able to continue raising DPU (but there is aa limit to it) PGINVIT has not been able to do it, and hence getting punished.

1 Like

Here is one point , Transmission lines can be changed from lower KV line to Higher KV line or even HVDC line , but the main thing is the stricture and the land route which cannot be changed , Structure and the land routes are always appreciating one only.