However it is human nature to have massive aspirations and live life lavishly and BNPL companies are helping in achieving this dream by allowing consumers to purchase products online and pay within a few days or weeks with little to no interest. Users that miss payments are typically charged either interest or late fees… “Buy now, pay later” apps pitch customers on being a safe alternative to credit cards, but are they really?

One out of 3 millennials say their biggest fear is credit card debt, whereas BNPL is still a form of credit and many BNPL providers do not report the use of such services to credit bureaus and this trend could cause consumer debt and credit card default risks given the lack of credit checks.

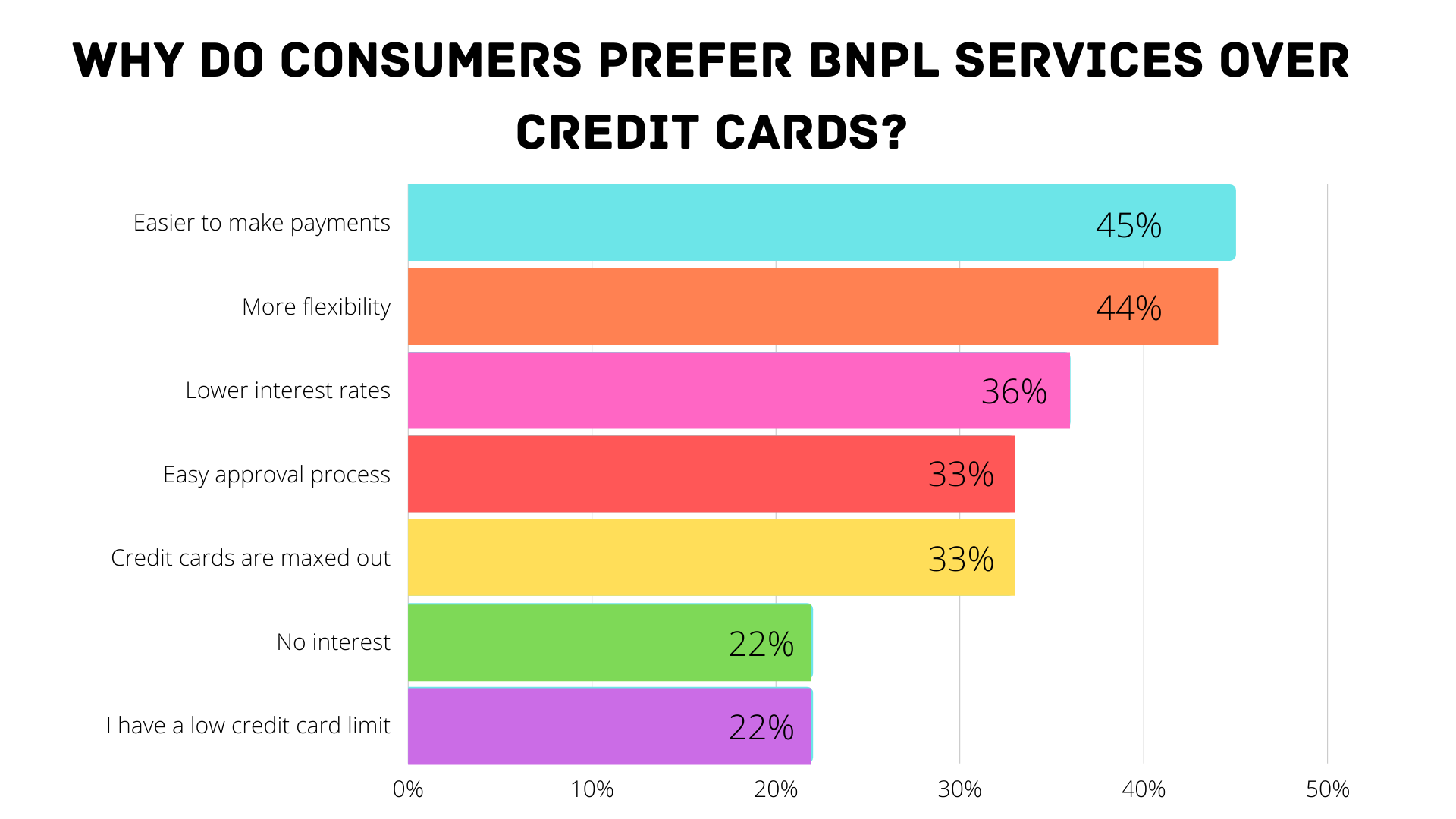

On the consumer side BNPL companies highlight how the fixed payment structure is safer than using credit cards because users:

• Pay a percentage of each purchase up front

• Can’t roll over their balance and continue racking up debt

• Get cut off if they miss multiple payments

But BNPLs offer a conflicting pitch to merchants, their technology causes users to spend more than other shoppers, in fact BNPL saw a 2.3X Increase in Transactions in the fashion and lifestyle category.

At this rate, many users may land up in the same place they feared with credit cards — in debt. Example:

In Australia, 15% of BNPL users had to take out a loan to pay off their purchases.

Do you think BPNL are better than credit cards? Or is it better to stick to what you have in your bank account?

Credit cards or BNPL is ok provided you have a regular income to pay it back in the short term. If you default on dues, the interest rates are relatively high and you will end up paying way more than your initial debt. Also defaulting will reduce your credit score be it a CC or BNPL.

In short, stick to own funds as much as possible. Tap the short term credit line if there is no other way.

For a few years they will have to look to at least appear to be better if they are trying to make Credit Cards obsolete. So a lot of freebies, goodies, and unsecured loans surely be expected in plenty.

I have always found the ease with which I can order stuff on swiggy/zomato in many cases quickly. Using credit cards means I have to type in CVV and then wait for the SMS to arrive( which might not) then pay for the same transaction.

I use LazyPay almost every other day because I order food on swiggy mostly for dinner. I mostly use it for the convenience it provides.

The scary/sad part of these Buy-Now-Pay-Later (BNPL) schemes is the way they are packaged and shown on apps/websites. Most folks opting-in to BNPL schemes have no idea of all the complications they are unknowingly signing-up for.

“They are burning VC-money to gain customers” is the biggest lie!

They are minting money with opaque/predatory lending practices,

currently possible due to the lack of regulation in NBFC-lending (compared to traditional banking).

The individual is ultimately on the line for anything that goes wrong down the line. Behind the scenes, there’s a loan issued in the name of the buyer/individual which immediately affects their credit-score. Also, in case one later claims a return/refund on the purchase, the seller/marketplace is now free to flag this loan as a default and ruin the individual’s credit-history/score.