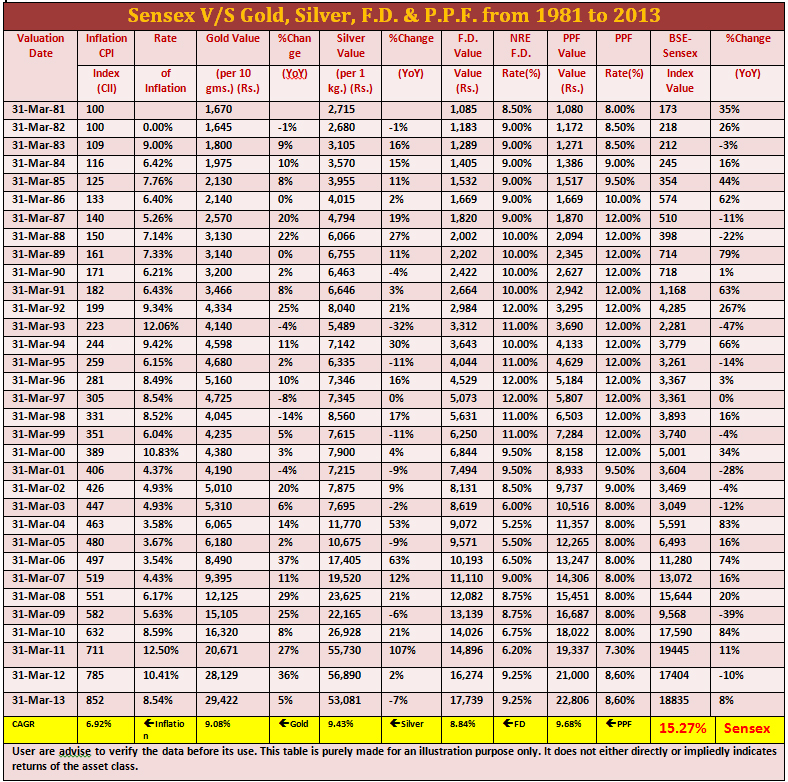

Whenever you think of equity, think of long term, as Ben Gram rightly said “Stock market is voting machine in short term but weighing for long term”. Equity is by far the best investment if you want increase your purchasing power, FD can give you false satisfaction of your capital protection but on the contrary post tax your purchasing power will decrease (ouch). Have a strategy, plan it, write in your notebook about a road map to achieve your goals then apply tactics(for the strategy), then do the action. Last but not the least study as much as possible to become smarter each night before going to bed. Here is a proof that nobody can beat equity returns over longer period.

2 Likes

To made consistent profits from stock market, one need to strictly follows the universal rules, no tips or adivise help in the long run.

First 1-2 years reeding, reading, reading…, gaining good theoretical knowledge on stocks mkts, fundamental & technical analysis, risk management etc. Apply it on practical later on…

As per my opinion FDs are a decent product if someone is not willing to take any sort of risk. some bonds and debentures also give decent and risk free return.

Worst advice ever.

Have you even considered inflation.

FD is a lose making investment in a growing country like india where inflation is consistently high on YoY basis.

FD is suitable only for retired people with no other source of income.

1 Like

Excellent reply, also want to add FDs are may be good vehicle for retirees to protect their capital(but is it?? Hint: Inflation), but life expectancy is improving even some fresh retirees can go for conservative hybrid mutual funds. If anything which is giving less return than 9% is a loss(loss of purchasing power) if we take into account of inflation.

@trader_dude at-least the capital is protected. There will be inflation but atleast the money is guranteed in the end. Say you have 2-3 crore as investment in FD vs MF. In the result of a crash the whole money of MF will be obliterated , in FD atleast you will receive the money. Its people like you who give wrong /inflated opinions to normal people. If a person atall has to take risks invest direct into cash market. There is no point in investing MF , its na ghar ka na ghat ka!

1 Like

I’d advice you to go for Corporate FD which gives better return than bank FD. But if you’re thinking about SIP, don’t give it a second thought at all. Go for it in case of longer period.

I politely disagree with @Jontu , if you can look at past record, there’s not even a single loss for more than 3-5 years in investing.

even you can see in Stock market crash 2008-09, it recover so nicely in just one year plus the benefits of some amounts invested in that crash. Oh, how big there value is now.

Value of FD 6.5%? It will be either zero or negative value of FD when inflation+taxes are considered.

I only agree with you if you’re talking about short terms, but we all know that equity mutual fund is never for short term at all. peace!

[/quote]

@Jontu here’s all about fact and figures, if you want to calculate the real return in FD, the forumla will be “Bank FD - Avg Inflation for that period”, you will realize that FD gives you -1.7 in 5 years, -1.1 in 10 years, -0.8% in 15 years, -0.2% in 20 years. Why you would need to invest for zero return?

Stock market is not a one year game

Retailers see Nifty running to all time highs and Midcaps zooming 5-10 times

They sell their lands and FDs, and put 50 lacs in one shot at highs

Then when index crashes, they lose 20 lacs and feel stock market is a trap

Even SIP if any retailer does they will do from 2017 end to now, and then close the SIPs in panic coz even their SIP is in 30% loss till now

Have you ever invested in your life?

Are you saying that crores of money is obliterated in MF in all these years.

Just look the MFs and people investing in them and look at the returns they have made.

I would suggest you study basic economics first and then look at investment.

When it comes to investing in FD vs MFs. I would say its purely subjective and depends on ones risk appetite and understanding of said investment.

If people dont understand MFs , they should not invest it in. Period. There is no debate here.They dont understand ecnonomics , nor market volatiltiy. This is why they will exit right after a crash and cash out and they you see spectacular returns later.

@trader_dude while I type this post I am sitting in a skyscraper in New York working as a Vice President in a Fortune Top 100 company , so yes I have invested in myself that is why I am here.

Have you ever looked at what happened to the mutual funds especially the Pension Funds in the financial crisis ?

Let me say today the data is not even there because the MF propagandas do-not want to see it. But let me say this …most people who had put money in MF during the 2008 crisis has lost the whole corpus. But people who had invested in the government bonds has been saved . Learn from them .

The point is

if you have risk taking capability invest in Stock Market . You would learn and know al lot and you would become knowledgeable enough to take own decisions.

If you are not risk taking then invest in Bonds and Fixed Interest schemes.

Then comes the third group I do-not want to learn but I want to get the benefits of the learners. The MF walaas… I want to take the risk, neither I understand the risk nor has the capacity to deal with it …all I can do is follow the crowd.

Read my previous post.

you are picking one scenario where people lost while all the other time people made a ton of money.

I m assuming people never put all their eggs in one basket.

Investing and risk taking is purely subjective, there is no right or wrong.

But you are making blanket statement like FD is going to save everyone , which is wrong.

Accept where you are wrong , learn and move on.

if you want to fight and take things personally , lets do in private. Lets not disturb the peace here.

@trader_dude read the question in the context of the ans ‘s FDs better and give u peace of mind?’ and I have said yes and given the facts for these. I am in no way arguing with you. In fact I have to stop people like you who runs the MF propaganda

MF propaganda is very much there, but its main aim is not to eat your money as @Jontu is thinking

Its main aim is to serve the masters called FII , and the side effect is that your SIP money gets trapped in wrong sectors at wrong levels

Though mutual funds will definitely perform over a period of 3+ years, because unless something shocking happens, Nifty is always in uptrend

But an intelligent investor could surmise that mutual funds are waste because that investor can always beat the returns of funds and not get trapped at wrong places at wrong times. But ofcourse an intelligent investor is the rarest of rare commodities in our markets

So mutual funds is the right way to go for most retailers.

@trader_dude i am of the principle i invest in FDs in banks and next small fraction in direct equity . I feel other MF funds need not play with our money. We should choose our companies invest direct and face results rather than a fundhouse messing up with our money.

@trader_dude from radio broadcast in 1995 2000 yo TV advs.

MF is the only instrument that found way to get broadcast in aakasa vani radio station.

Recall US 64 of UTI and the then finance minister lobbying hard in vajpayee govt?

How many useless investments LIC funds make?

MF is a big trap by govt.

Fundhouse is messing up with our money?? Are you sure, please elaborate with some examples. I am seriously want to know which fund managers are actually messing up with our money. Because of mutual fund my corpus increased from 14 lac to almost 60 lac and you are talking about they are messing our money? If it is then it is OK for me.

Well said! it totally depends on the risk appetite of investor. that’s the reason everyone has different prospective regarding different investment methods being its MFs, FDs, stocks or anything.

Investors in india blindly follow what media (print/tv) says…so if they ask you to put in balanced funds dividend option via SIP they all do that. then after seeing losses they all wonder what happened. I agree there is a huge corporate wave which controls the market here & you see how suddenly MF sahi hai ads have stopped after creating hype when markets were high. I’ve always maintained that your major investment should be in FDs+bonds+debt MF (ultrashort for current scenario & later start moving for long term debt when we cross 9% govt bond yield). Invest in good stocks & importantly in ETFs rather than equity MF. You should get little into tech charts & follow accumulate/distribute model if you are in equity. This approach has helped me generate 22-25% IRR in equity whereas if you see MF SIP returns are either negative or very low in past 3 yrs…request haters/trollers to keep away from my post.

1 Like