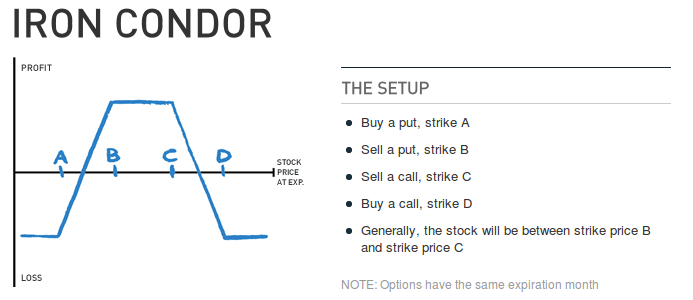

There are many option trading strategies with defined risk, one such option selling strategy with proper hedge is Iron Condor.

What is an Iron Condor strategy?

Iron Condor is a non-directional option strategy, but with risk controlled as we hedge the position by buying options.

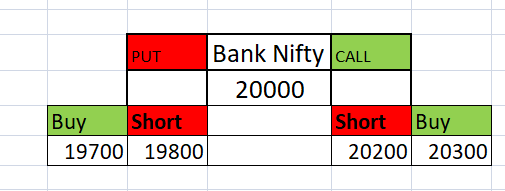

Here’s an example, consider Bank Nifty trading at 20000 levels currently, to create Iron Condor Strategy, the following trades needs to be executed.

- Short 19800 Put option

- Buy 19700 Put option

- Short 20200 Call option

- Buy 20300 Call option

All in same expiry dates, basically we short OTM options and buy the next strike levels of those OTM options to hedge it. We shorted 19800 Put option, so if bank nifty moves down and falls even further to 19700, 19500, 19400, then we end up in high loss , right? So in order to protect ourselves from such losses, we buy 19700 put option, which is next leg of 19800 put to hedge the risk.

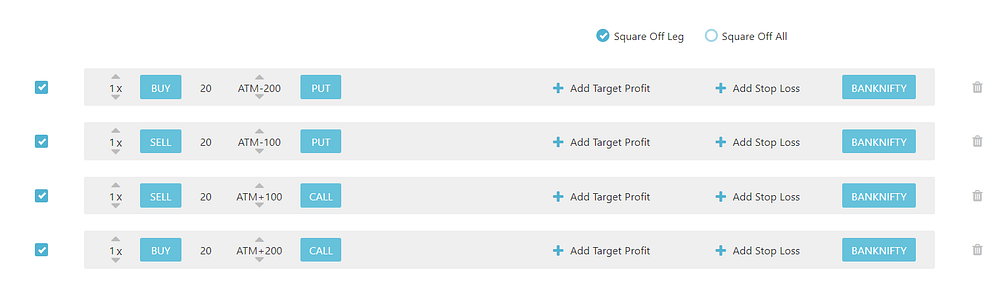

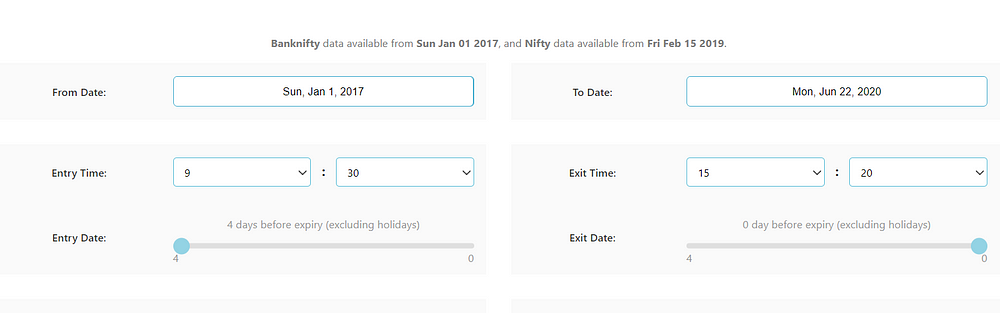

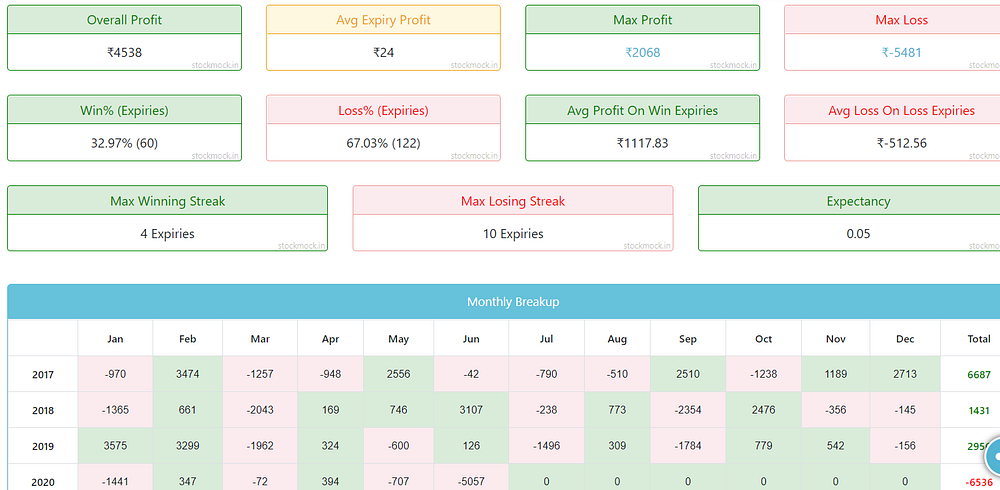

This is how Iron Condor strategy is created, lets backtest with stockmock platform and find it out whether its really a profitable strategy, the below example is for Bank Nifty

We enter at the start of the expiry and close it on the expiry day, tested from 2017 to 2020

Here’s how the results look like, with more than 3 years of data, the over all profit is just Rs.4538 with transaction cost , this will give negative results.

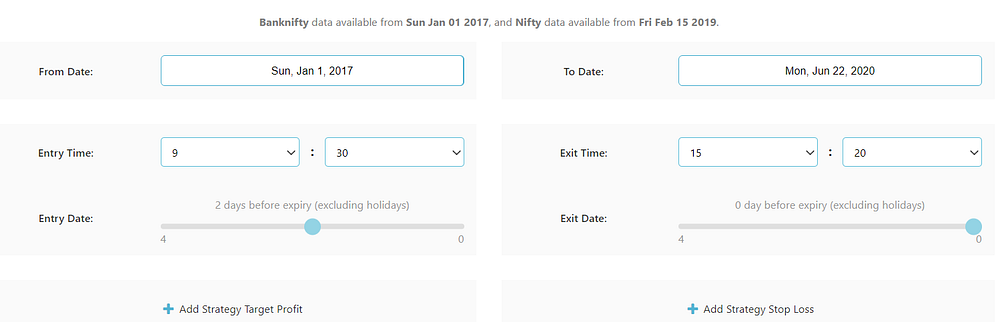

So I tried changing the parameter, by entering just two days before expiry and exiting on the expiry day.

This has given better results than the previous one, however over all profits is still lesser, its 27600 Rs. profits for 3.5 years period, which is very minimal.

Instead of hedging our positions with option buy, what would be the results, if we dont hedge at all? If we simply short OTM options, without hedge/stop loss, does it generate positive returns? We have tested that as well.

Short Strangle:

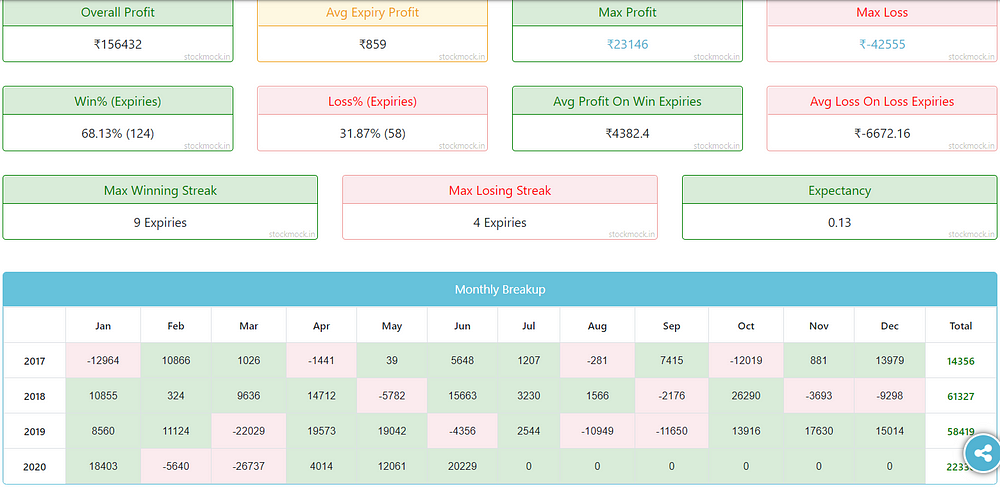

If we remove the buy positions in Iron condor strategy, it becomes Short Strangle. In this example, we shorting OTM options of bank nifty of both put and call.

With same parameters, by entering just two days before expiry and exiting on the expiry day… Tested from 2017 to 2020

The returns are much higher without using any hedge/stop loss, it has given more than 33 times higher profits with more than 68% winning accuracy.

Conclusion:

Even though Iron Condor controls the risk , it drastically reduces the over all profits, in fact it ends up in loss after all cost. Whereas a simple short strangle strategy without any hedge has given outstanding results than the hedged strategy — Iron Condor.

source: Is Iron Condor a Profitable Option Trading Strategy? - Algo Trading in India |