Ok, a lot of really stupid advice on the thread so far. Really horrible advice. Here’s how you think about it.

Diversification doesn’t mean adding 20 different funds, that would be DIWORSIFICATION.

In all the funds above, the theme is IT broadly, meaning, it’s a sectoral or a thematic bet. I am guessing you want to invest in IT because the returns have been good or you might have heard about AI/ML and all that stuff.

Anyways, the thing about investing in such a narrow sector is that, things can really volatile. Take a look at the NSE IT Index chart

The index can fall quite a bit and do nothing for a really long time. So, you need to be ready for that. Your IT funds will do nothing while a border index like Nifty 50 will be going up quite a bit.

Looking under the hood of the funds

Diversifying doesn’t mean picking 5 different IT funds. Think of it this way, Does it make sense to go to 5 different coffee shops to fill one cup of coffee? I hope you’ll answer yes.

It’s the same logic here. When you’re investing in a theme, it makes ZERO sense to buy 10 funds of the same theme. Now, the next thing you need to do is look at what you are getting. If you look at the underlying holdings of ICICI Tech, Tata, and Fraklin funds, you’ll see that a lot of the holdings are common-Infy, TCS, HCL, TCS, Tech Mahindra, Persistent are the top holdings. How does it make sense to hold 3 different funds to get exposure to the same set of stocks?

SBI is a bit different because it has a mix of Indian and US stocks. But if you choose to invest in Nasdaq 100, you’ll again get exposure to the same US stocks. So, how does it make sense?

Having said that, there’s a another factor at play here. Some people think you should also diversify across AMCs because what if some AMC messes up like Franklin, DHFL, etc? That’s a personal call you have to make.

Thinking about sectoral investments.

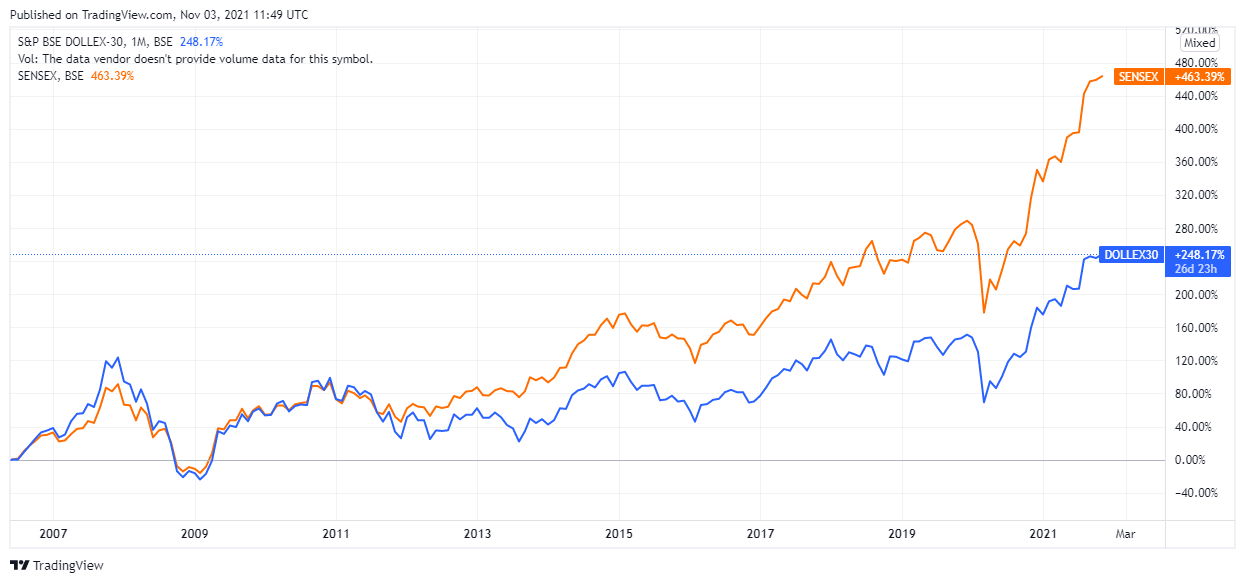

When you look at the Nifty IT chart you’ll be tempted to invest. I mean, who doesn’t want 5X returns compared to Nifty 50

The other interesting thing in the chart is that, unless I’ve got it wrong, the long-term returns of Nasdaq in rupee terms are much lower than the dollar returns. This will seem confusing since you’re a beginner, but in simple terms, since Nasdaq is a US fund, you’ll have to bear the currency risk.

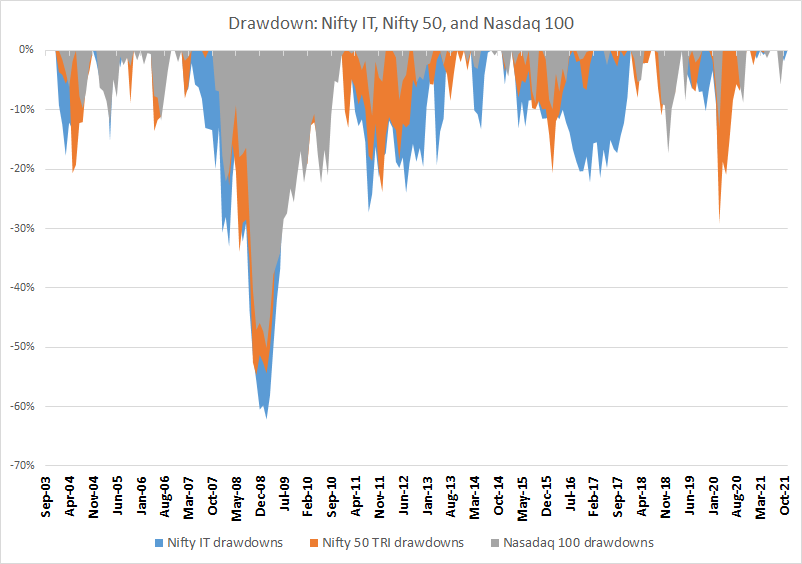

But this line chart shows only one side of the picture. Look at the drawdowns-the % fall from a peak to bottom. Notice the blue area, Nifty IT is much riskier compared to Nifty 50 and even Nasdaq.

Hope this gives you a starting point to think about things.