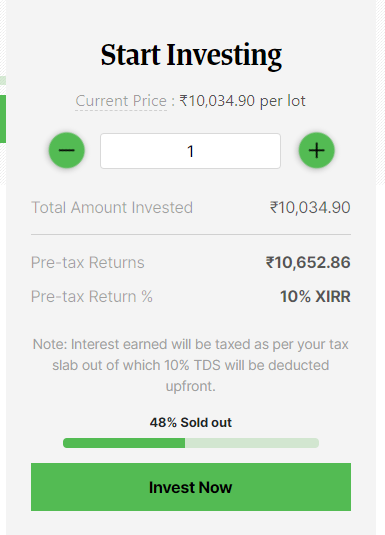

Wint wealth provides senior secured bonds of 1-3 years tenure and yield around ~10% returns.

With STCG, for people in 30% tax slab, it will yield 7% returns.

whats your opinion on this?

Wint wealth provides senior secured bonds of 1-3 years tenure and yield around ~10% returns.

With STCG, for people in 30% tax slab, it will yield 7% returns.

whats your opinion on this?

One suggestion I can give is, how much will you be going to invest, and how much more you are going to get here than other similar products, and if such a difference in returns is meaningful to you?

I have invested in multiple bonds on Wintwealth. While it is good option for diversification, I am struggling with whether it actually makes sense to continue investing or not. Two main problem I have are actual returns and Taxation.

As you rightly pointed out if you are in 30% or higher slab, taxation is very unfriendly and returns are not as high as the risk being taken. I would think that post tax a credit risk fund might give similar returns if held for more than 3 years.

Second is the way returns are calculated. Most of the bonds coming up these days have very short duration and also intermittent principal repayment. So XIRR looks high, but actual return are not very great. For eg. their latest offering provides an interest of around RS. 650 for 10K invested for year. Nothing spectacular.

XIRR still works out as 10% because it repays 1/3rd principal every 4 months. So nothing wrong with math, but if you don’t really have a need of repayment at every 4 month, then it is useless for you, because you overall earn only 6.5% interest, unless you reinvest what you get back every 4 months (which is tedious and uncertain)

So I am holding back investing for now.

This pattern reminds me of predatory lending practices of NBFCs,

which i studied in some detail earlier this year.

NBFCs have been running these “too good to be true” so-called “zero-EMI” loan schemes,

that prey on the borrower’s naivety to miss out on these details.

I wouldn’t be surprised if the some NBFC was trying to raise money to fund their “zero-EMI” loan schemes by floating the above bond on Wint.

Personally, I have found GoldenPi offering more diverse and trustworthy. Most of the funds are from well known institutes and they provide credit rating info etc too. If you are concerned about the large ticket size of secondary market bonds, just register and hang in, they open Bond IPOs regularly with minimum investment of 10K and various duration and interest frequency.

Bonds or other debt products are not hedging, they are an asset class, a stable asset class which while does not beat inflation, but acts as a regular income source and can be used to put the gains of equity into. We cannot at all ages of life be in equity alone, we need debt too as we grow old, unless needs are taken care of by other means, which again will be a permanent cash flow source like rent from property.

@GB26 Thanks for putting it in right context. I edited my post.

While I personally use bonds in that fashion (diversify to potentially offset the loss of a high risk investment), I realised that statement might create a wrong impression to the broader community, without a background.