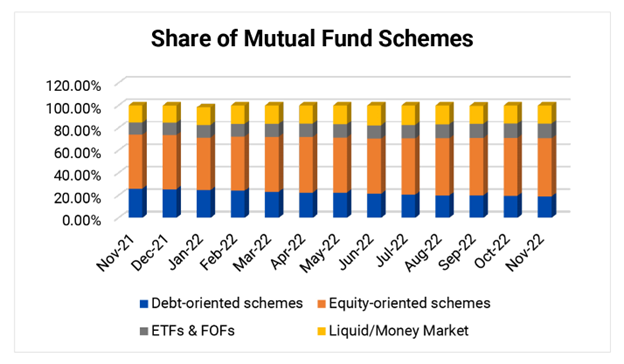

The Mutual Funds Sahi Hai campaign launched by AMFI five years ago has made Systematic Investment Plans (SIPs) a popular mode for retail investors to invest in mutual funds. As of Nov 30, 2022, there are over 6.05 crore SIP folios, and the SIP AUM stands at over 6,80,000 crores. There are over 70,00,000 Debt Fund Folios and over 9 Crore Equity Fund Folios. The proportionate share of equity-oriented schemes is now 51.7% of the industry assets in Nov 2022.

Source: AMFI data as of Nov 30, 2022. Past performance may or may not be sustained in the future.

Investors are wisely recognising the key benefits of SIPs that it helps make regular and systematic investments, instil discipline, is lighter on the wallet, make timing the market irrelevant, facilitate rupee-cost averaging, and effective medium of goal planning while you endeavour to compound hard-earned money.

But does it make sense to take the SIP route to invest in debt funds? Let’s find out…

Typically, SIPs are a suitable mode, particularly for volatile asset classes like equities, which could witness deep corrections in unfavourable market conditions. Debt as an asset class, on the other hand, is far less volatile. A Debt Fund, depending on its sub-category, typically invests in corporate bonds, debentures, government securities (G-sec), Treasury bills (T-bills), Commercial Papers (CPs), Certificates of Deposit (CDs), and other debt and money market securities. The primary objective of debt funds is to benefit from a of interest income and offer moderate capital appreciation to investors.

That said, there are certain debt market undercurrents such as inflation scenario, interest rate cycle (which determine where yields are headed), yields, the credit risk environment, and liquidity, among others that have bearing on debt funds making them risky to an extent.

If a debt fund holds commendable portfolio characteristics and the maturity profile is short and it holds the portfolio till maturity, then usually, the volatility is less. In such a case, it would be sensible to make a lump sum investment, particularly when you are deploying money for the short term.

Conversely when there is the maturity profile of a debt fund is medium-to-long, potentially there is credit risk involved, and interest rates are on an uptrend, whereby the debt fund could be exposed to high volatility, in such a case, SIPs may make sense. Typically, you may enrol for SIPs in sub-categories of debt schemes, such as Medium Duration Funds, Long Duration Funds, Dynamic Bond Funds, Gilt Funds, and Credit Risk Funds that could expose you to high volatility due to their inherent trait and portfolio characteristics. But note, rupee cost averaging in debt funds usually works lesser extent than with equity funds.

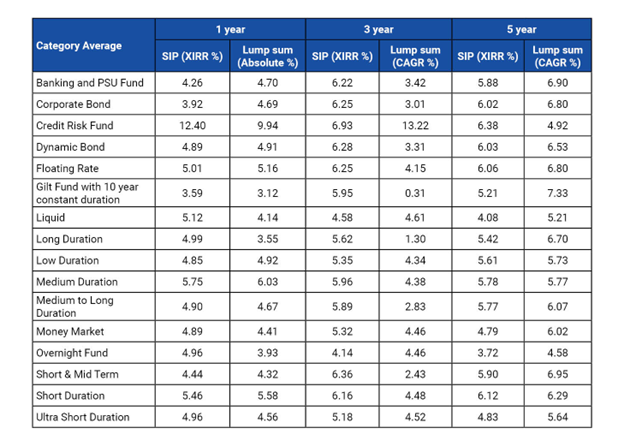

Table 1: SIP v/s Lump Sum Returns of various debt mutual funds

Data as of November 30, 2022. Past performance may or may not be sustained in the future. Investments through SIP is subject to market risk and do not assure a profit or returns or protection against a loss in downturn market.

(Source: ACE MF)

The table above indicates the kind of returns you can expect by SIP-ping into various sub-categories of debt funds compared to making a lump sum investment.

Nonetheless, you ought to be very clear about your investment objective and/or the financial goal you are addressing and accordingly consider suitable debt mutual funds for SIPs or lump sum paying heed to asset allocation best suited for you.

For example, if you wish to systematically keep money worth 12 months of regular expenses (including EMIs on loans) aside or an emergency, staggered lump sum investments or SIPs in a Liquid Fund may make sense. On the other hand, if you wish to invest dynamically across maturity profiles for 3-5 years and want to participate in interest up and downcycle relying on the expertise of the fund manager and take measured credit risk, then perhaps SIPs in a Dynamic Bond Fund may make sense.

Such clarity about when you would need the money (investment horizon), the goal, your risk appetite, and the interest rate cycle will help you make a sensible investment decision.

Bank FD v/s Debt Mutual Funds

For regular monthly ‘savings’ you may consider investing in Recurring Deposits. But for ‘investment’, where one expects at least a moderate inflation-adjusted capital appreciation, debt funds can be a one of the options to invest in.

You see, although interest rates have moved up and bank fixed deposits (FDs) seem to be offering a better nominal return, they may not be earning an attractive real rate. Simply put, they may not beat inflation. For example, the real return (also called inflation-adjusted return) earned on a Bank FD is currently fetching you -0.67% net real returns. Besides, the interest earned on the FD is taxable as per your income-tax slab.

Illustration: Traditional FDs are unable to keep up with inflation

FD interest rate for 3 years tenure.

Data as of December 6, 2022

Comparatively, debt funds are tax efficient if invested for more than 36 months and by taking a calculated risk you can potentially earn real returns if you choose among the debt funds (from the respective sub-category) wisely. Please note that investments in debt mutual funds are subject to market risk in comparison to FD.

Debt Funds Outlook

The return potential of debt funds has improved, and the next three years could be more return generating than what we witnessed in the last three years. The real rates have turned positive in the Indian fixed-income space. Currently, government bonds between 6.0% to 7.5% across all maturities are trading above the expected CPI inflation for the next year. Also, with much of the rate hikes by the RBI already delivered, the probability of the market value of bonds going down has also come down meaningfully.

This makes debt funds as an attractive asset class for investors in the current environment of high macro uncertainty.

How to select the right debt fund?

Here are certain parameters to evaluate if you are considering taking the SIP route or investing a lump sum in debt mutual funds:

- The portfolio characteristics (who are the issuers, the sector they belong to, the type of debt papers held, the ratings of the respective debt papers, etc.)

- The current interest rate cycle

- The maturity profile.

- AUM and the expense ratio of the scheme

- Returns across time periods (3 months, 6 months, 1 year, 2 years, 3 years, and so on)

- The performance across interest rate cycles

- The risk ratios (Standard Deviation, Sharpe Ratio, Sortino Ratio, etc.)

- Track record of the fund house and processes and systems followed by it

Stick to the mutual fund schemes where the fund manager doesn’t chase returns by taking higher credit risk. Keep in mind investing in debt funds is not risk-free or safe. The safety of your principal should be of prime importance when you invest in debt funds, and not clocking extraordinarily high returns.

And last but not the least, assess your risk appetite and investment time horizon. If you adopt a sensible and astute approach, it shall reap financial success.

Happy Investing!

Note: The comparison with Fixed Deposits has been given for the purpose of the general information only and not a recommendation to invest. Investments in Mutual funds should not be construed as a promise, guarantee on or a forecast of any minimum returns. Unlike fixed deposit with Banks there is no capital protection guarantee or assurance of any return in mutual funds investment. Investment in Mutual Funds as compared to Fixed Deposits carry moderately high risk, different tax treatment and subject to market risk.

Disclaimer: The views expressed here in this Article / Video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The Article / Video has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of the Article / Video should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. None of the Quantum Advisors, Quantum AMC, Quantum Trustee or Quantum Mutual Fund, their Affiliates or Representative shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary losses or damages including lost profits arising in any way on account of any action taken basis the data / information / views provided in the Article / video.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.