Hi @Anugrah excellent explanation for the people who had any doubt about the product and it’s function. Here is a feature I would like to have (a bit of technical may be) in smallcase is, is there anyway we can have multiple instances of a particular smallcase? Eg. Say I bought a smallcase on 31st March 2017 and till now I haven’t rebalanced but now on 14th December 2018 I want to buy the same smallcase but with the latest composition. Is it possible to implement?

1 Like

@Anugrah I appreciate you standing up to all questions and criticism and patiently answering everyone’s concerns.

But despite all the talk, after 15 months of religiously following your CANSLIM smallcase and rebalancing every advice by smallcase team, I’m standing at 4L loss(20% down). And this is a gradual loss every rebalance.

I understand “Long-term” duration is abstract and market considers atleast 3 years as long term. But if your rebalance continues the way it did for first half, by end of second half I’ll be left with nothing.

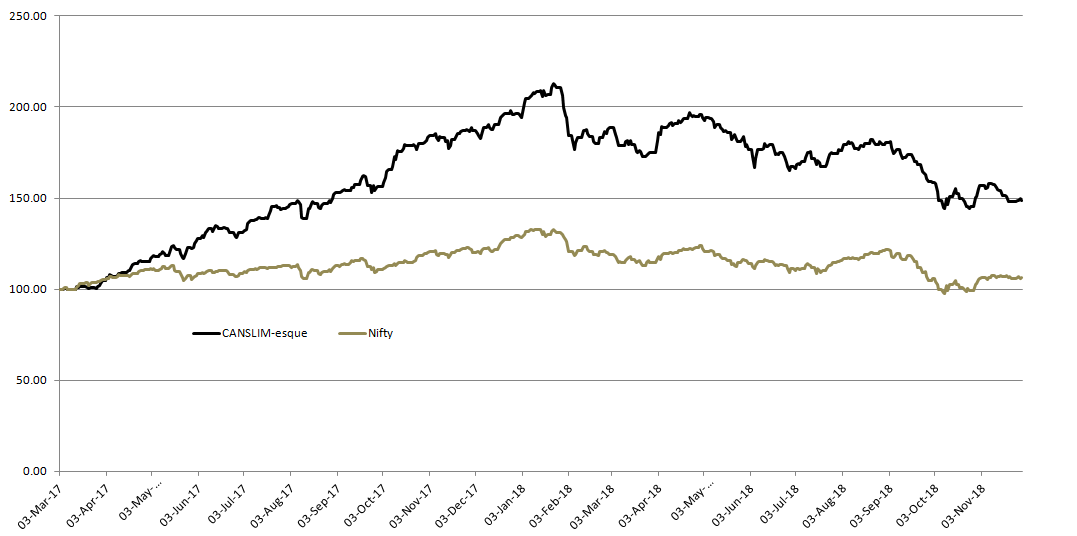

@investor I understand your concern and completely agree that nobody likes to see negative returns. But the nature of the equity market is that we can not avoid it. I would want to show you few numbers, not to prove anything but just to give full information on how the CANSLIM-esque strategy has been performing.

We launched the smallcase on 3rd Mar’17. For this purpose I have only included data since the time smallcase has been in public domain - no backtested data. This is how it has performed

Now coming to what has happening since launch and in last one year in exact numbers

| Event | CANSLIM-esque | Nifty Midcap |

|---|---|---|

| Since Launch | 48.00% | 6.00% |

| Since Nov’17 | -18.00% | -12.00% |

Different strategies work in different scenarios. But I would suggest you that you follow a systematic investment approach through our SIP option. It would ensure that you don’t end up picking a high point and entry risk gets distributed.

1 Like

I would definitely discuss the suggestion internally with the team and let you know what can be done. Thanks

1 Like

Thanks @Anugrah very much for considering this suggestion. It will be my strategic approach to maximize my expected returns through some select smallcases. Also it will boost your revenue as one has to buy the same smallcase more than once  .

.

how would a systematic approach help when you are unsure whether those scripts that you have been buying every month since last 3 months, will have to be sold in next rebalance. And the cycle continues.

Every rebalance incurs in trading charges and hence expense ratio may increase. So if you have bought a low cost smallcase of say Rs 1500. At the time of rebalance let’s assume it asks to sell 4 scripts. Now imagine there is a realised loss of Rs 300.

Trading cost of rebalance = 13*4 = 52+taxes (Zerodha DP charges RS 13 per script). Now say the rebalance also asks to put in Rs 500 more.

So the total investment which was Rs 1500 initially, after the rebalance (after 3 months of buying) has become Rs 2000 (1500 + 500) and in the rebalance you have already lost Rs 300

Total expense = 500 (additional money put in) + 300 (realised loss) + 52 (trading cost).

Also, rebalance has taxation implications.

This is why I am saying that smallcase investors are losing their money because of high expense ratio.

When compared to mutual funds,

a TER is mentioned for the scheme. For e.g. if 1% is the TER, then it is already considered in the return. Whether you are investing 500, or 5 lakh, TER is 1% only of that amount.

Additional money put in (Rs 500) is an investment which average outs the NAV earlier purchased.

Also even if there is a loss (or profit) of 20%, it is not a realised one. So helps in planning taxation.

Please for God’s sake don’t answer that you can choose not to rebalance ![]() (That’s a separate discussion and not an answer to my query).

(That’s a separate discussion and not an answer to my query).

Because I am considering all rebalances are applied religiously because basis that is the CAGR and 1 yr return shown on the smallcase page.

Now, tell me is it worth investing in smallcase knowing the following:-

-

trading charges as expense

-

realised loss as expense

-

additional money put in is an expense because you never know by next rebalance you may have to sell those scripts you just bought in loss.

-

taxation implication in case of STCG profit booking

The biggest difference between mutual fund and smallcase is that you are the fund manager of your portfolio. Smallcase research team through some rebalancing data on the new inputs arrivals but again it’s upto you to decide what to do. Smallcase isn’t an alternative to mutual fund, it’s well crafted tool for an experienced investors who understand the strategy on which the smallcase is constructed. Instead of going to screener.in and screen out some stocks on the basis of some theme or strategy, smallcase is a God send tool for an individual who knows how to use it for their benefit. Smallcase is giving us a starting point how to proceed with the said strategy, duration and whether to rebalance or not is upto you, because you are the fund manager.

I have raised these pointers because @Anugrah has been constantly comparing smallcase with mutual fund saying former is low cost and passive investment. So i demonstrated how expense is more with smallcase.

Maybe you know better than the peers about investing but what percentage is people like you. Comparing with mutual fund is appealing to the passive investors who have given full responsibility to the fund manager.

Moreover, responsibility is black and white. Either take complete responsibility or don’t take. What is the meaning of yes we tell you to rebalance but it is upto you whether to do or not when on the smallcase description page you are showing CAGR and 1 year return basis all rebalances applied in past. Which means an investor will apply rebalance. If you are asking investor to take the responsibility, then add a disclaimer on the homepage while displaying CAGR and 1 year return. Also when rebalance arrives, the copy says - rebalance pending. This means you are expecting us to rebalance.

4 Likes

I very well understand your concern over rebalancing but also believe that it has become a double edged sword for many. To tell the truth I don’t have any clue to explain. Hope @Anugrah can better explain or tune it for better for all smallcase investors.

1 Like

Having Smallcase with other DP like HDFC Securities would be even more expensive to rebalance. Because Zerodha equity delivery is free but not HDFC Securities and the likes. The brokerage charges of other DPs are also more.

I really hope SmallCase team reads this and take it seriously. Most of the numbers what @rupeshmandal has put is exactly how it was working in real world. Gradual loss.

In the Smalltalk blog, they should provide this sort of information. To rebalance or not, what are the implications of these. Like @sabyasachi_sadhu confirmed, it’s suitable for experienced investors.

I thought it was exactly like how SmallCase team described it, like a mutual fund. I invested money and took team’s advice, followed all rebalances passively. Every rebalance it said “Out of 13 stocks, drop 11 - and add 9 new stocks”. If you are dropping 11 stocks, those stocks were not researched for long-term.

3 Likes

Smallcase is cashing on the bull run statistics…

There are so many hidden factors involved in small case investing and many have realized these pitfalls only after burning their fingers (including me)…

They never specify that TIME is the crucial factor in determining the P&L of any smallcase. I can enter a smallcase this week and there may be a rebalance next week and I may have to sell a lot of my securities realizing a loss (as those stocks which I am selling basically does not fit the strategy/theme of the small case). Also, two persons having the same smallcase bought in the same month (one before the small case rebalance and another after the rebalance) will have different P&L.

Even the smallcase team have probably realized it now and they have copied the Core-Satellite strategy from the western world and introduced the ‘‘All Weather Investing (AWI)’’ with the concept of buying ETFs, Gold and debt instruments…

Even if one starts buying these AWI at a monthly SIP for one year, then the total cost incurred would be Rs 50 + taxes per month which would be 600 + Taxes + additional charges such as transaction charges of 0.00325% on turnover(qty * price), 18% GST on transaction charge, SEBI charge of Rs.15/crore and stamp duty as per the state. Also while exiting these ETFs from Demat, a DP charge of Rs.8+GST is charged at Zerodha.

If the AWI is not performing well, then the returns from this smallcase would be worse than the returns from the recurring deposit in any post office scheme…

smallcase is a great idea but poorly implemented. One can proudly say that one has invested in equities through CANSLIM-esque strategy without knowing anything about this strategy.

I strongly believe that the smallcase business model should be tweaked first to educate investors about the theme or strategy and then help the investors to build their portfolio based on that strategy and regularly educate them that they need to periodically revise their strategy and take care of the portfolio all by themselves…

But currently, smallcase simply compares the returns against any benchmark and lures one to buy the smallcase and send reminders to blindly rebalance the portfolio. This strategy has definitely burnt a hole in many people’s pockets…

2 Likes

I have noticed one more flaw of smallcase that may cause price manipulation of the script.

At the time of rebalance, say it asks you to sell script X and buy script Y from a particular smallcase.

Now say there are 1 lakh investors who have that particular smallcase in their portfolio.

Imagine those many unique number of investors clicking on rebalance button within a small time frame and thus what happens is script X that has been recommended to be sold during the rebalance, its price would go down because of mass sell-off happening.

Similarly, the script Y which is recommended to be bought, its price would go up because a synthetic demand has been created in the market.

So a smallcase rebalance which has fixed dates for the act of rebalance may cause price manipulation with such volume of buy and sell.

I don’t know what is SEBI’s take on this.

1 Like

What utter rubbish is this? Do you data to back this up?

Ya, ya, quite clever. Use “SEBI” “Manipulation” “Flaw” and hide behind “May”. When you make an accusation, then you’ll have to back them up with data. If you don’t have data, then ask. Your question should have been:

@Anugrah will the rebalance updates cause unnatural moves in stock prices?

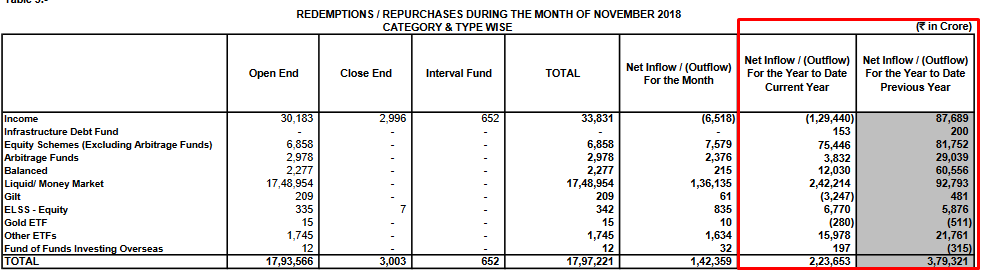

Now let me back this up with data.

Here are the mutual fund flows for the month of November and YTD:

That’s 75,446+6,770 into equity inflows. Did you wonder if these flows are causing “SYNTHETIC DEMAND” and “MANIPULATING” share prices. There are 100’s of funds with turnover of over 100%, 1000% percent even. Which means certain funds have completely churned holdings 12 times in a year. Don’t they “Manipulate” holdings.

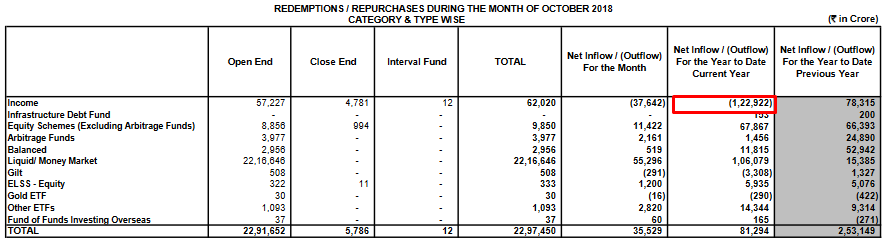

Also, here’s Oct flow. 1,22,000 crore outflow in debt funds. MY GOD, didn’t that cause bond yields to be “MANIPULATED”?

I can go on all day long!

1 Like

What I have mentioned is a hypothetical situation.

If a large number of investors would rebalance, all at the same time, like a flash mob, (in the backend buy script X and sell script Y in the rebalance process) wouldn’t it cause the respective script prices to go up and down by the simple principles of demand and supply?

That’s a worry when smallcase accounts for 90% of all equity volumes on the exchange.

Last month 280 crores of equity assets were purchased by equity MFs every day. Do you think smallcase is bigger than an AMC(s)?

Anyways, your “Flash Mob” theory is a worry when smallcase account 90% of all volumes on the exchange on rebalance day.

Not sure how large Smallcase is, but wouldn’t this be true for any large investor (say when fund manager for the largest mutual fund from ICICI Prudential?)

Hey, is your smallcase portfolio still in loss?