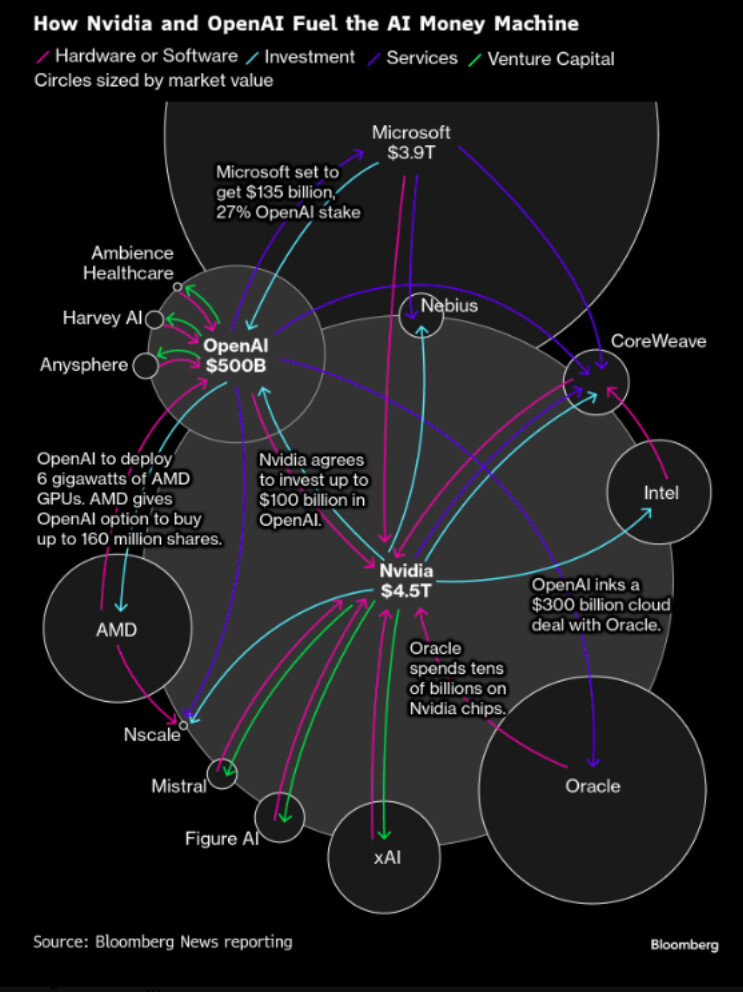

Look at this chart for a second. It shows all the big AI companies buying stuff from each other, investing in each other, and then spending that same money back with each other.

OpenAI gets money from Microsoft, then spends billions on Microsoft cloud.

Startups get money from Nvidia, then use that money to buy Nvidia chips.

Oracle buys Nvidia chips, OpenAI signs a huge cloud deal with Oracle.

And around and around it goes.

When every company’s “customer” is also their “investor,” the revenue starts to look less like real demand… and more like everyone passing the same money in a circle. A normal business sells to real customers. Here, most customers exist only because someone funded them first.

In a few years, people might look at this and say: this wasn’t a flywheel it was financial recycling.

Where do you stand, real growth or money merry-go-round?

So last week, i had asked ChatGPT to go back 50 years and do some digging around bubbles and how their timeline looks like, and how they evolve over years before bursting. This one is for the dot-com bubble

Mid-1990s–2000 – Dot-com Bubble (The First Modern Tech Mania)

1995–1998: Internet goes mainstream. Media headlines celebrate “the new economy.” VC money flows into anything with “.com” in the name.

1995–2000: Nasdaq rises roughly 400–600% and hits a P/E ratio around 200 at the peak — total insanity by historical standards. Wikipedia

1999–early 2000: Super Bowl is full of dot-com ads; “eyeballs” and “page views” replace profits in narratives.

March 2000: Bubble peaks; by 2002 Nasdaq is down ~78% from the high. Wikipedia

Important: it wasn’t that “no one” saw it. Plenty of people were shouting “this is nuts.” The majority just chose to ignore them.

Now the interesting part and similarities between dot-com and AI are very close. Everything “AI” is getting money - valuations are being blatently ignored, OpenAI is botching it’s books to overestimate revenue, if you have a business plan around anything remotely AI, then venture capitalists are ready to give you money regardless of how the returns might look like, revenue made by companies are overrun by the costs.

Despite the difference that NASDAQ PE was 200 at that time (in dot-com), but currently they are still much higher than normal levels of 20-25. In isoliation, NVIDIA PE is pushing 50 already, and it alone is ~15% of NASDAQ100.

And yes, companies are cross investing in the name of AI. This is only adding higher valuations.

Watch this video where Finance Professor Aswath Damodaran talks about how AI is being overhyped, and what levels of revenue do these companies need to generate to make a profit or even breakeven.

When a bubble is forming, hardly people realize that it is forming as everyone is celebrating the changing times and is in euphoria. Most of the markets are held by institutions and crashes are also caused largely by institutions. Euphoria in the markets is very dangerous - it is the biggest time to be scared when the markets are euphoric. People are enjoying the greens in their porfolio seeing large gains and “feeling rich”, without really booking profits.

Buffet is very correct about saying - be fearful when the markets are greedy and be greedy when the markets are fearful.

Personally in my opinion - it is not just an AI bubble, but this time it is coupled with debt bubble as well. Credit card dues are at an all time high, mortgages and loans are being taken with people being at risk of job losses but still taking loans due to feeling rich from green portfolios. US national debt grew fastest in last 10 months than it did in the past. People are defaulting aggresively on loans too and companies are trying to get the dues settled with reduced payments. Inflation is biting into savings of people with most hardly having 3-6 months of expenses worth saved.

India doesn’t have any AI names on its bourses. But still whenever this bubble will burst, markets across the world, including India will crash. Everything wiĺl crash due to bad sentiment

AFAIK, the common term for this is Circular Financing.

IIUC, this is prevalent in other sectors/economies as well.

How about when a company’s supplier is also their investor?

Does it have the same implications?

Here’s a scenario 1 -

Also, let us consider the practice of a company performing share buy-backs using its reserves, with the intent of boosting the share price. It is treated as a good practice. One that helps shareholders to book profits they desire in a tax-efficient manner (instead of a company declaring dividends).

Here’s another scenario 2 -

Now let us consider the circular financing activities being carried out by a supplier using its reserves (inventory, cash-reserves), with the intent of boosting the share price. Is it a similar good practice? If not, why not?

One potentially significant difference in the 2 scenarios is that the investing company now has exposure to one of its customers.

Compared to scenario 1, is scenario 2 concentrating risk or diverisifying risk?

Also does it matter? Are some of these specific companies already too big to fail? (or the collection as a whole, too big to fail now?)

FWIW, there’s a meme that is making the rounds on social media that attempts to look past all the “noise”, and at the “house of cards” this financialised world is perched upon.