Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

In today’s edition of The Daily Brief:

- Hotels in India Set for Decade-High Earnings

- Mixed Signals in India’s Economic Growth Story

Hotels in India Set for Decade-High Earnings

ICRA recently shared that the Indian hospitality industry is on track to reach its highest Revenue Per Available Room (RevPAR) in a decade by FY2025, with even more growth expected in FY2026.

Now, if you’re wondering what RevPAR actually means, it’s just a way of measuring how much money hotels make per room per day. And the numbers are looking good. Occupancy rates are expected to hit 72-74% by FY2026, and premium hotels’ Average Room Rates (ARR) are set to rise to ₹8,000-8,400. In simple terms, hotels aren’t just filling more rooms—they’re also charging more for them.

But why does this matter? Let’s break it down.

When hotels do well, it often reflects something bigger happening in the economy. People don’t usually spend on hotel stays unless they have extra money to spare—whether it’s for a weekend trip, a wedding, or a business meeting. This suggests that disposable incomes are growing, businesses are thriving enough to send employees on work trips, and large events like meetings, conferences, and exhibitions are back in full swing. When hotels are buzzing, it’s a sign that people are spending on things beyond the basics, which is always a positive sign for economic growth.

There’s another angle to this story: tourism. Domestic travel has bounced back strongly after the pandemic, and international tourist arrivals (FTAs) are recovering too. In 2019, FTAs peaked at 10.9 million, and by 2023, they’ve climbed back to 6.2 million. The government has also stepped in to support the sector by improving travel infrastructure—adding 17 new airports since 2020 has made it easier for both domestic and international tourists to explore India.

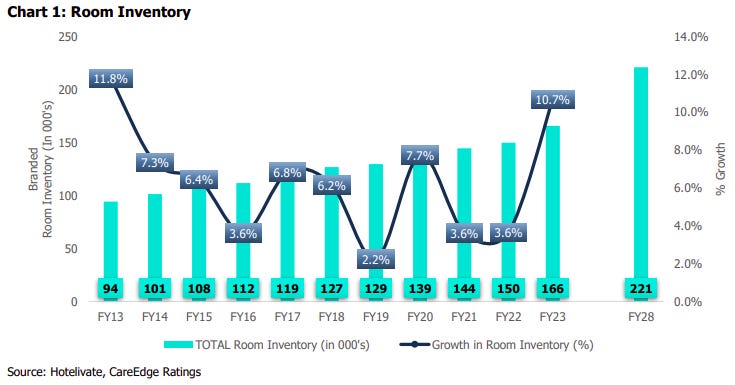

Before we dive in, let’s take a quick look at how the hotel industry works. Broadly, it’s divided into two categories: branded and unbranded players. The branded segment, which includes big names like Marriott, IHCL, and Lemon Tree, currently makes up about 166,000 rooms.

Source: Tijori Finance

This is expected to grow by about 55,000 rooms over the next five years. Sounds like a lot?

Source: Care Ratings

It’s not. Even with this growth, demand is outpacing supply, and that’s one of the main reasons room rates and RevPAR are climbing.

The unbranded segment, on the other hand, is much larger but harder to track. It includes small boutique hotels, family-run guesthouses, and even Airbnbs. While these cater to a big chunk of travelers, they operate in a highly fragmented market, making it tough to get consistent data or metrics for the industry as a whole.

Here’s where it gets interesting.

Many hotel chains are moving away from owning properties outright. Instead, they’re adopting an asset-light approach, using management contracts, franchises, and revenue-sharing models to grow. Why? Because it’s faster, cheaper, and much easier to scale compared to investing heavily in real estate.

Source: Varsity

Lemon Tree and ITC Hotels are also embracing this model. By doing so, they’re able to focus on expanding operations and improving profits, instead of worrying about owning every building they operate.

If demand is so strong, why aren’t we seeing a wave of new hotels? The reason is the long time it takes to build new ones. Developing a hotel isn’t something you can do overnight. Land acquisition, construction, branding—it all takes years. On top of that, challenges like limited land in prime locations and rising development costs slow things down even more.

This delay is why supply growth, estimated at a CAGR of 4.5-5.5%, will continue to lag behind demand in the medium term. By FY2028, India’s branded room inventory is expected to reach 221,000, but it still won’t be enough to close the gap.

Another trend worth paying attention to is where the new supply is coming up. In the past, hotels were mostly focused on Tier 1 cities like Mumbai, Delhi, and Bengaluru. But now, Tier 2 and Tier 3 cities are stepping into the spotlight. With growing urbanization, better infrastructure, and higher incomes in smaller cities, hoteliers are rushing to meet the rising demand in these areas.

In fact, more than 70% of the new supply in the pipeline is planned for these smaller cities. It’s a smart move, as hotel chains look to tap into the potential of domestic tourism and smaller-scale business travel.

If we take a step back, the growth of the hospitality sector says a lot about where the economy is headed. Weddings are in full swing, businesses are hosting conferences again, and families are traveling more—all clear signs of a strong recovery after COVID. Even foreign tourist arrivals, which haven’t fully bounced back yet, are expected to pick up soon, adding even more momentum.

And it’s not just about hotels. When demand for hotels goes up, it sets off a ripple effect. Jobs are created—not just in hotels but also in related industries like travel, food, and construction. Tax revenues increase. Cities have become more appealing for investments. It’s a chain reaction that benefits the entire economy.

So, the next time you book a stay, remember—you’re playing a small but important role in this booming sector.

Mixed Signals in India’s Economic Growth Story

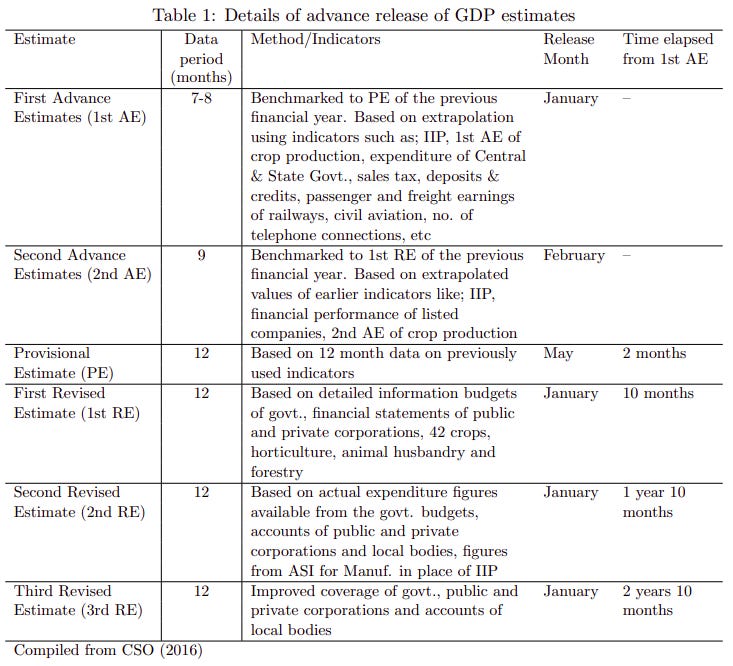

This week, the Ministry of Statistics and Programme Implementation (MoSPI) released its first estimates of how GDP might perform in FY25. These are called “first estimates” because MoSPI updates the annual GDP numbers six times over nearly three years. That’s how detailed and complicated calculating GDP can be.

The initial estimates are known as Advance Estimates (AE) and Provisional Estimates (PE). Over time, they’re updated and released as the First (1st RE), Second (2nd RE), and Third (3rd RE) Revised Estimates.

Source: IGIDR

Because early estimates rely on limited data or high-frequency indicators as proxies, they often have more “noise” or uncertainty. As more data becomes available, the numbers get refined, and the estimates become more accurate. This process explains why there can be small differences between Advance Estimates and Revised Estimates. In fact, research shows that Advance Estimates often underestimate the actual GDP growth rate.

So why use Advance Estimates when they aren’t perfectly accurate? Because the government needs a quick snapshot of the economy to guide policy decisions. Waiting for final numbers would take too long, and by then, it might be too late to act. Even with their limitations, these estimates play a crucial role in shaping timely decisions.

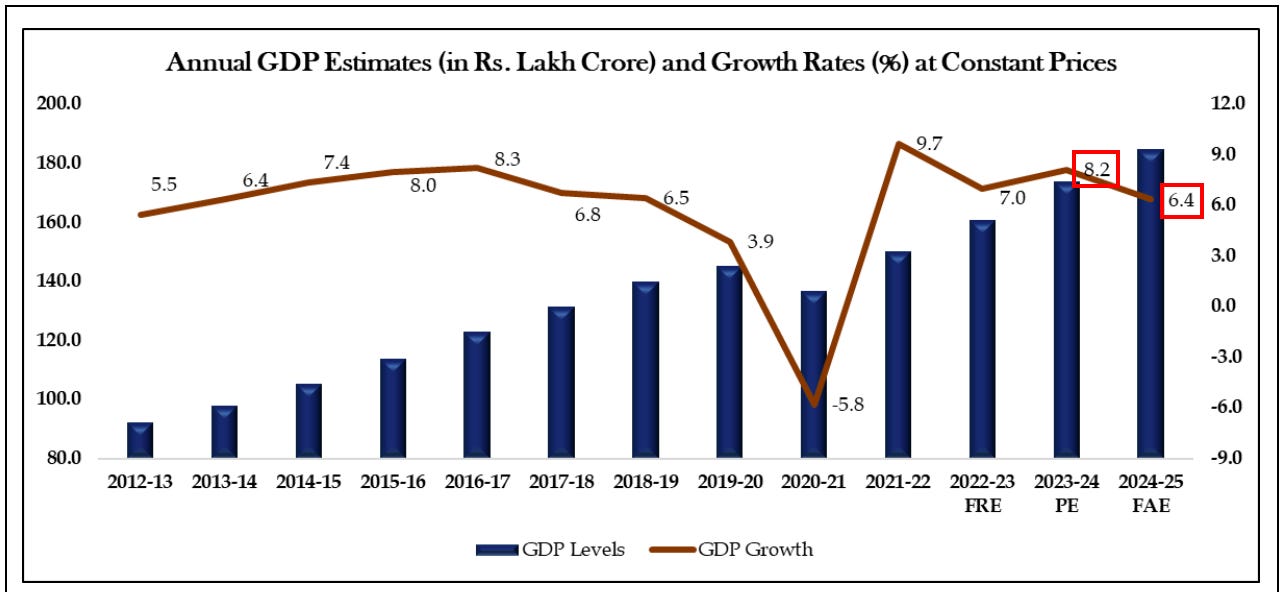

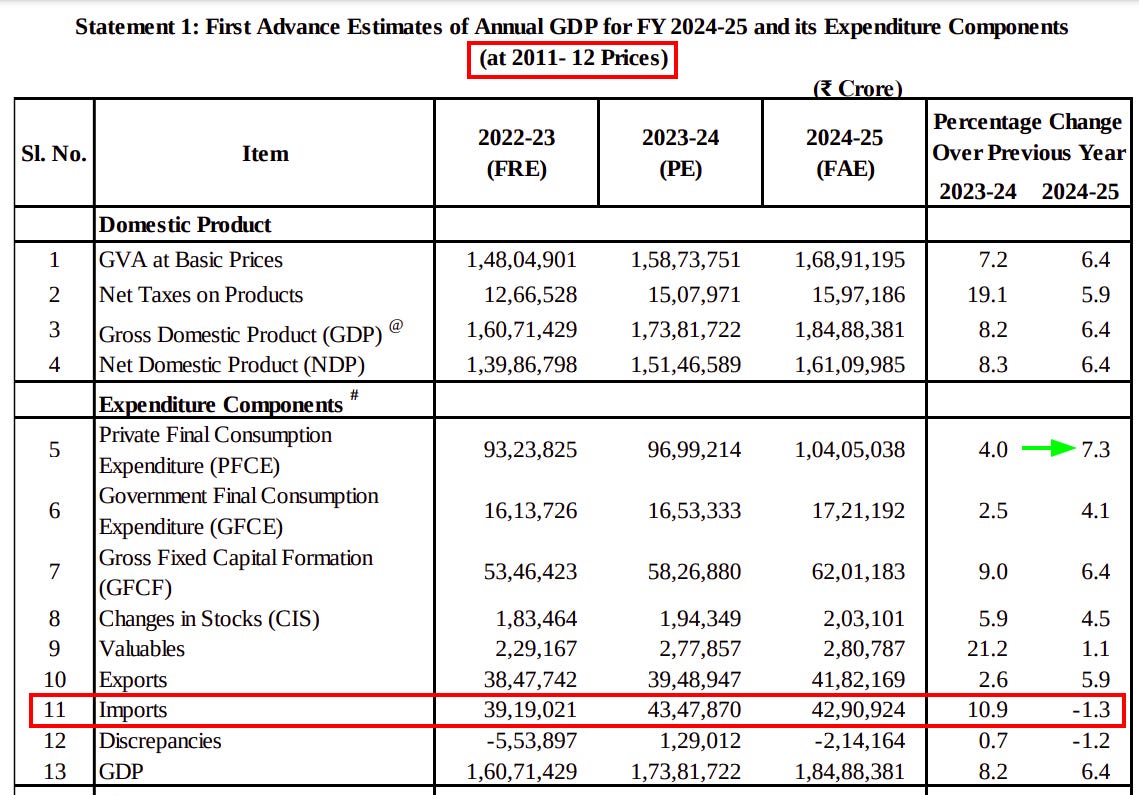

Now, let’s look at what the latest report says, starting with the headline GDP growth numbers. Real GDP is expected to grow by 6.4% in FY25, down from 8.2% in FY24. This is even lower than the Reserve Bank of India’s earlier forecast of 6.6% growth, announced in December.

This slowdown lines up with many high-frequency indicators that have been signaling weaker growth, so it’s not entirely unexpected. We also discussed this in our year-end roundtable conversation. But the real insights often lie beyond the headline numbers. Here are three key takeaways:

Source: MoSPI

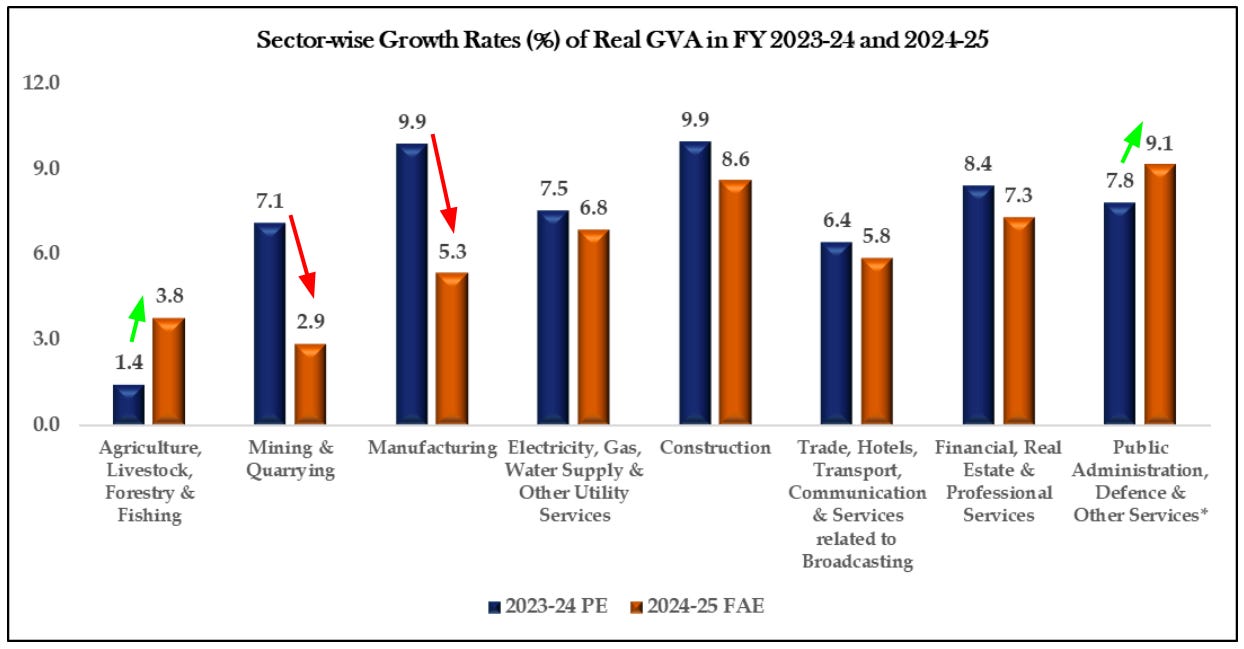

1. Manufacturing and Mining Are Struggling

- Manufacturing : Growth has slowed significantly to 5.3%, down from 9.9% last year.

- Mining : Growth has dropped to 2.9%, compared to 7.1% last year.

Together, these sectors make up about 16% of Gross Value Added (GVA). GVA represents the value added across all sectors, and when you add taxes and subtract subsidies, you get GDP.

This slowdown is concerning because it goes against India’s push to become a global manufacturing hub. Mining, which includes core industries, is also critical for the economy.

Source: MoSPI

On the flip side, agriculture grew by 3.8% this year, up from 1.4% last year. Government spending on public services also accelerated to 9.1%, compared to 7.8% last year. This isn’t surprising—rural demand has been catching up with urban demand, thanks to the recent growth in agriculture.

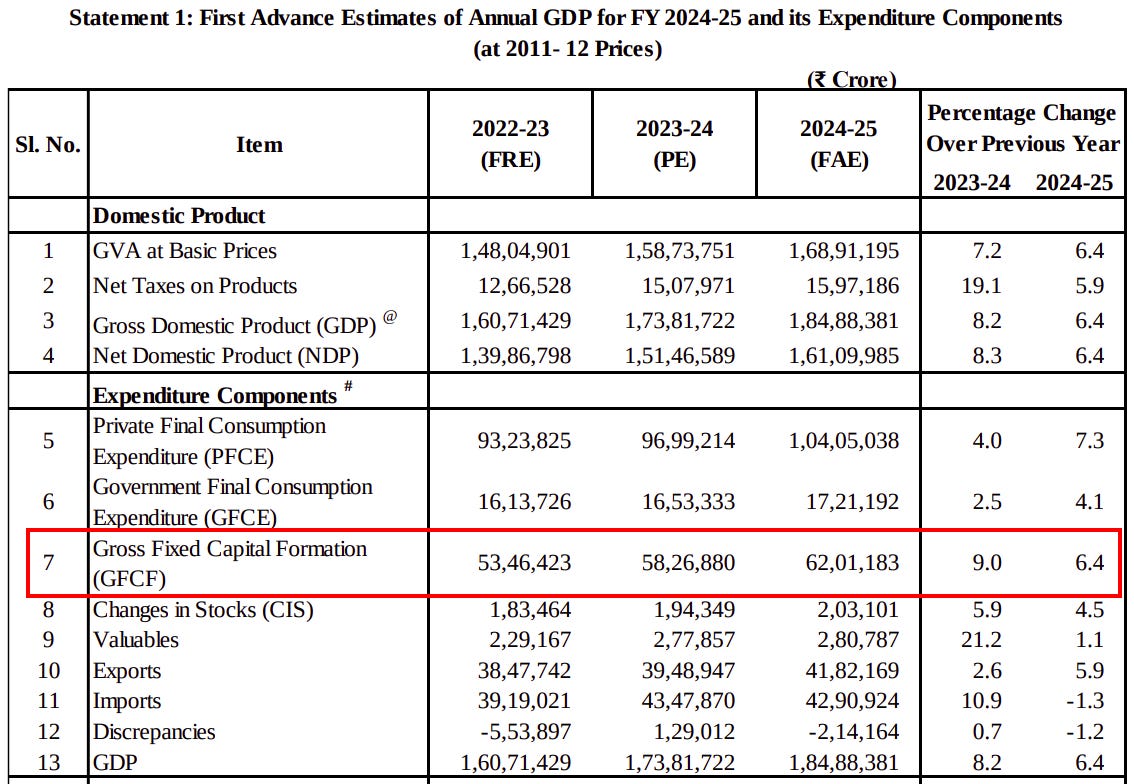

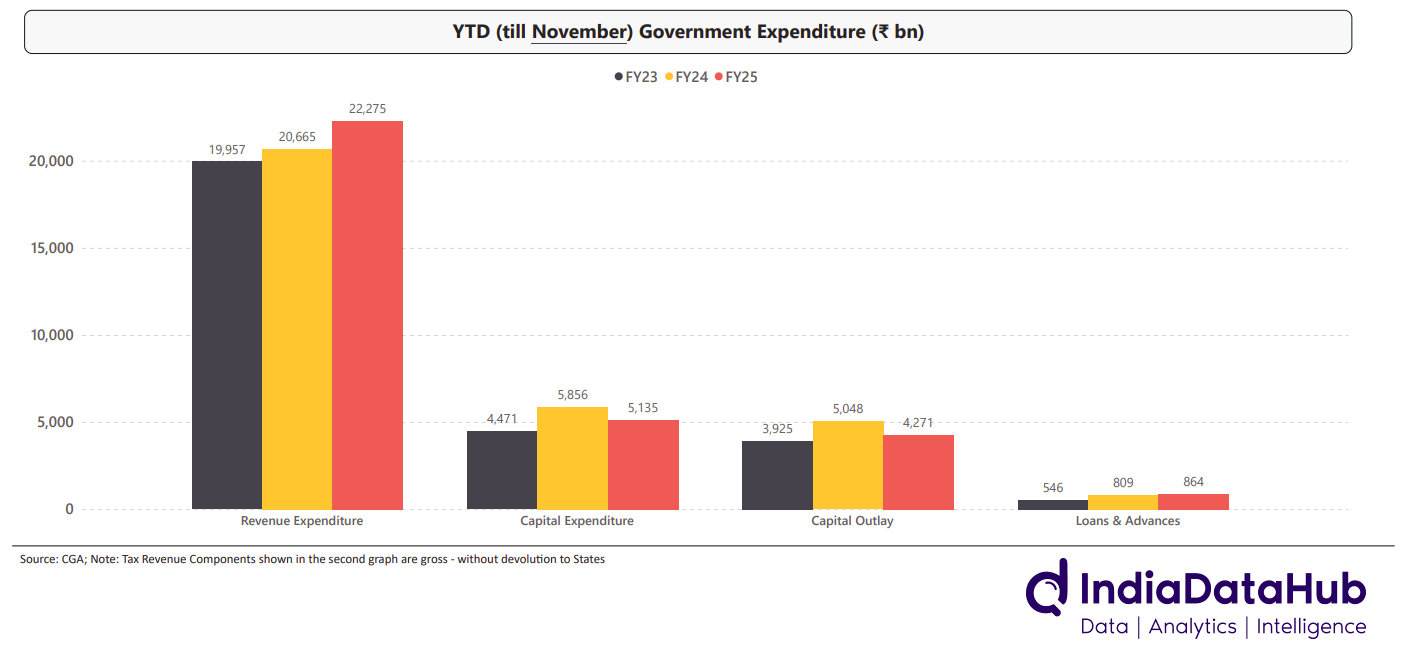

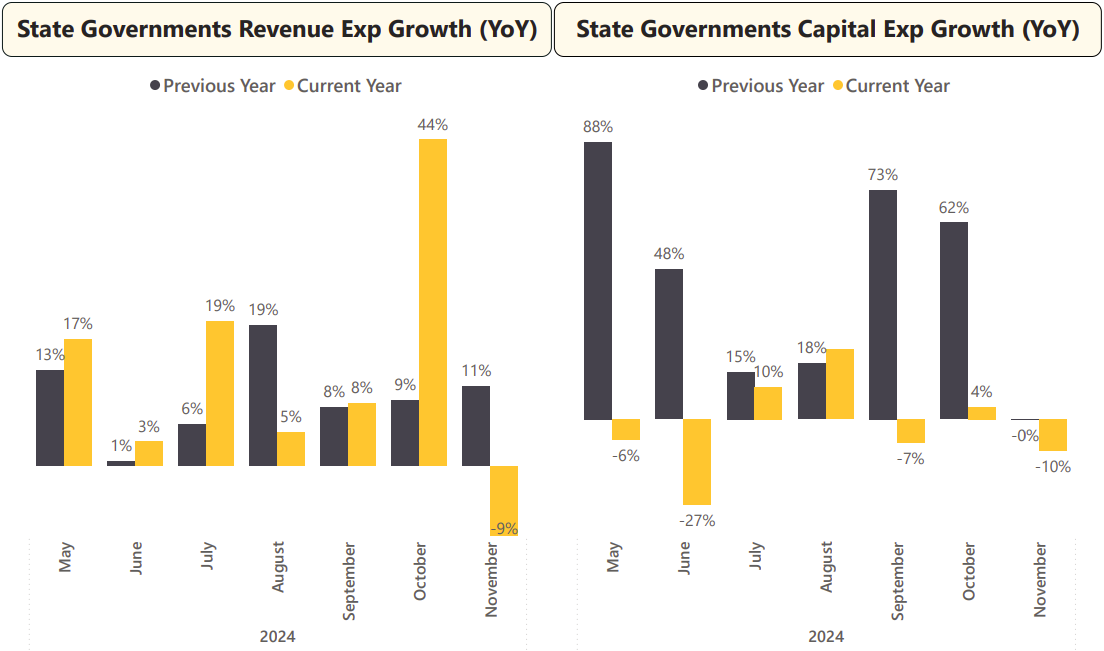

2. Gross Fixed Capital Formation Is a Growing Concern

Gross Fixed Capital Formation (GFCF)—a key indicator of investment—grew by just 6.4%, down from 9.0% last year. This slowdown suggests both the government and private companies aren’t increasing their investments as quickly as needed.

Government spending on capital projects is falling short, with both central and state budgets focusing more on short-term expenses (like administrative costs and salaries) rather than building long-term assets.

Source: MoSPI

Source: IndiaDataHub.com

If the government isn’t stepping up, private companies need to fill the gap. But that doesn’t seem to be happening, and as a result, GFCF growth is slowing. This lack of investment could have serious consequences for long-term growth.

3. Private Final Consumption Expenditure to the Rescue

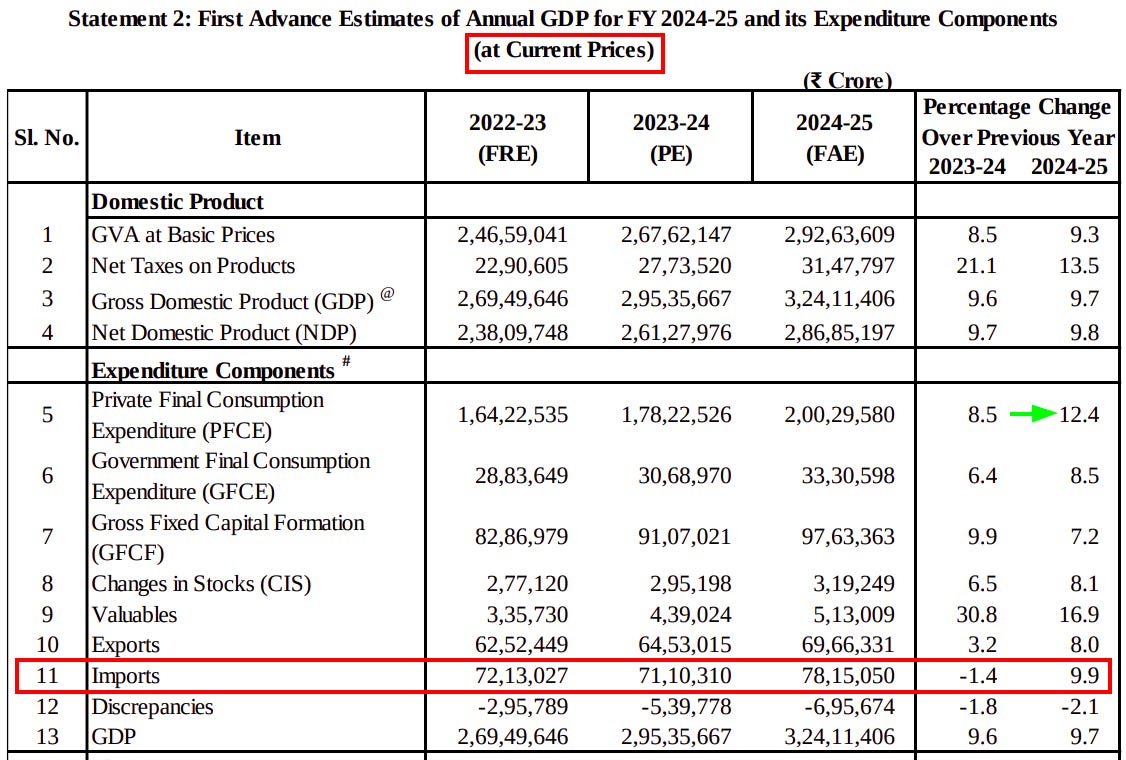

India’s economy leans heavily on consumption, which accounts for about 55% of GDP. The latest data shows that Private Final Consumption Expenditure (PFCE) grew by 7.3% in real terms and 12.4% in nominal terms.

However, this growth isn’t evenly spread. Rural consumption is growing faster than urban consumption, as we mentioned earlier. Still, the overall increase in consumption is good news, and if urban demand catches up, it could push this number even higher.

Source: MoSPI

There’s also an interesting shift in imports. In real terms, imports dropped by 1.3%, but in nominal terms, they rose by 9.9%. What does this mean? We imported fewer goods and services but paid more for them, largely because of currency depreciation. The RBI stepped in to control further depreciation, which helped keep the import bill from climbing even higher.

It’s worth noting that these insights are based on early data, so we can’t draw any firm conclusions just yet. But these numbers do give us a good snapshot of where things stand. We’ll keep watching high-frequency indicators to see how the situation unfolds.

Tidbits

- The Ministry of Heavy Industries in India has put forward a plan to lower the GST on CNG-powered two-wheelers from 28% to 18%, and then eventually to 12%. The main goal is to encourage more people to switch to CNG vehicles, in line with India’s environmental objectives. Although CNG vehicles have strong demand, the government faces possible challenges such as losing tax revenue and being asked to give similar tax breaks to other types of vehicles.

- Microsoft is making a big move by investing $3 billion in expanding its AI and Azure services in India. Part of this plan includes training 10 million Indians in AI by 2030. By committing this much money and effort, Microsoft is showing how important India has become in its worldwide AI strategy.

- Zomato’s shares took a 5% hit after Jefferies downgraded the stock. Jefferies pointed to rising competition and pressure to offer deeper discounts as the main reasons behind its more cautious view of Zomato’s performance.

-This edition of the newsletter was written by Krishna and Kashish

Thank you for reading. Do share this with your friends and make them as smart as you are ![]() Join the discussion on today’s edition here.

Join the discussion on today’s edition here.