Last week, the US jobs data came in, and it was disappointing. The US unemployment report hit a high last seen in October 2021. This bad jobs report sparked fears that the US is at a high risk of recession if it’s not already in one.

This bad jobs report also triggered something called the “Sahm Rule.”

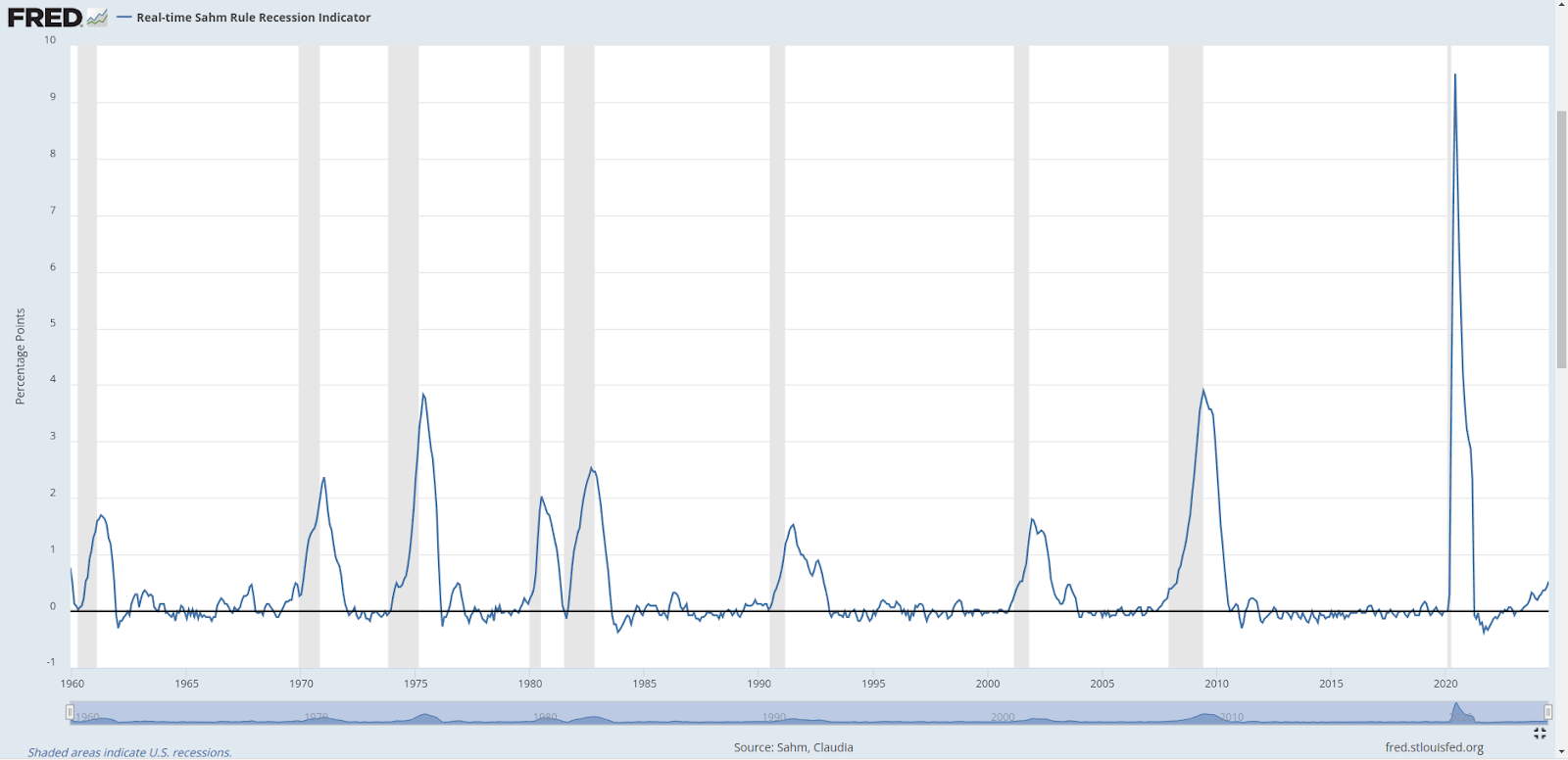

The Sahm rule is a recession indicator that was created by Claudia Sahm (Saam), a former economist at the Federal Reserve. The indicators say that the US economy will be in a recession when the three-month moving average of the national unemployment rate rises by 0.5 percentage points or more above its low during the previous 12 months.

Sahm used the unemployment rate because once it starts rising, it tends to keep rising because bad economic momentum feeds on itself. If the unemployment rate keeps going that means the economy is in bad shape and probably in or entering a recession.

So, is the Sahm rule wrong?

Sahm herself had written that “The Sahm Rule is a historical pattern, not a law of nature”

Furthermore she also recently wrote that:

- A recession is not imminent, even though the Sahm rule is close to triggering.

- The Sahm rule is likely overstating the labor market’s weakening due to unusual shifts in labor supply caused by the pandemic and immigration.

- The risk of a substantial weakening or a recession in the next several months is elevated, adding to the case for the Fed to begin cutting rates.

So yeah, you can’t just take one indicator and predict a recession.

Then the other recession indicator that is getting attention is the US yield curve.

A yield curve is a graph that shows the relationship between interest rates and the time to maturity of debt for a given borrower, usually a government. The curve plots the yields of bonds against their maturities, ranging from short-term to long-term. Changes in the shape of the yield curve give you insights into investor expectations about future interest rates, economic growth, and potential changes in monetary policy.

Typically, a normal yield curve is upward-sloping, meaning that longer-term bonds have higher yields compared to shorter-term ones. This is how you would normally expect things. A 10-year bond pays more than a 1-year bond. A normal upward-sloping yield curve tells you that the economy is healthy.

But sometimes a yield curve can invert. That means the interest rates on short-term government bonds are higher than the interest rates on long-term bonds. Which sounds weird right?

Well, the US govt bond yield curve has been inverted since 2022. That means a 3-month US government treasury bill today is paying a higher interest rate than a 10-year govt bond. Why?

That’s because the US Fed hiked rates massively which pushed short-term bond yields higher. At the same time, investors were expecting inflation to fall and the US to enter a recession which pushed down long-term bond yields.

An “inverted” yield curve is seen as a recession indicator. Historically recessions have occurred anywhere between 6-24 months after the yield curve inverted. Right now, it’s been 23 months since one part of the yield curve was inverted. This probably explains why the indicator is suddenly in the news.

Btw, on a side note the yield curve inversion doesn’t have the same predictive power for recessions everywhere. They are stronger in advanced economies and weaker in emerging markets like India. The Indian government bond yield curve was inverted earlier this year and we aren’t in a recession.

But coming back to the US yield curve. Now some experts are saying that it’s not the inverted curve that predicts a recession but rather the curve uninverting. This means, that when an inverted yield curve becomes normal it predicts a recession. The time between a curve univerting and recession is 66 days, according to one analysis.

Right now, the US 10-year treasury bond minus the 2-year treasury bond is close to univerting. That means that until now, the 2-year bond has given a higher yield than the 10-year bond, which is abnormal, but the situation is normalising.

This is causing worries that this disinversion is predicting a recession. It’s funny that this is happening at the same time that people are screaming that the US is entering or is already in a recession

So, is the US in a recession?

- Yes

- No

This is a snippet from The Daily Brief podcast, you can watch the full episode on YouTube here or listen on Spotify, Apple Podcasts or wherever you listen to your podcasts.