Hi Arnab,

While there are tons of nuances and technicalities to go through. In simple terms, the Fed (or any central bank for that matter) being behind the curve can be in the context of both raising or cutting the policy rate, which can either slow down or add momentum to the economic activity of the US (or any other country).

In the current context, with all that happened,

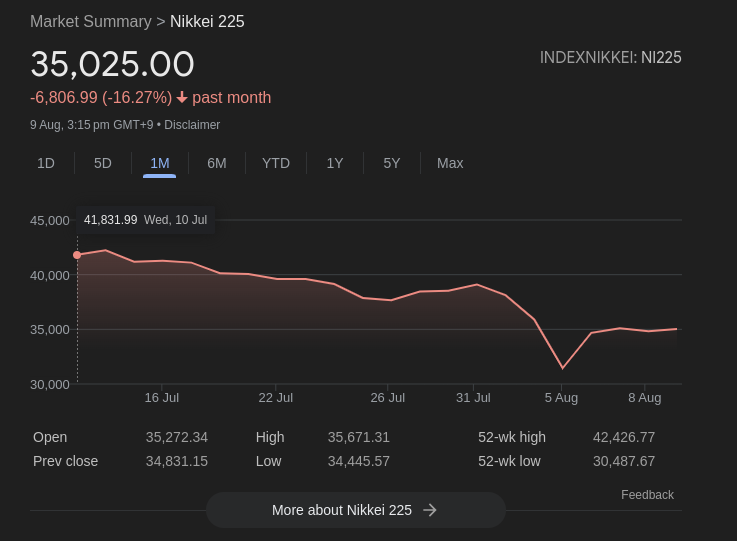

- Japan after Bank of Japan raised interest rates (Nikkei 225 Index dropped a remarkable 12.4% overnight – its sharpest decline since 1987. The Nikkei was also off by a very sharp 24% at one point). Mostly due to leveraged carry trades being wound down - meaning, people borrowing in Japan to invest in foreign assets suddenly realised borrowing isn’t cheap, and would sell off foreign assets to return the borrowed capital.

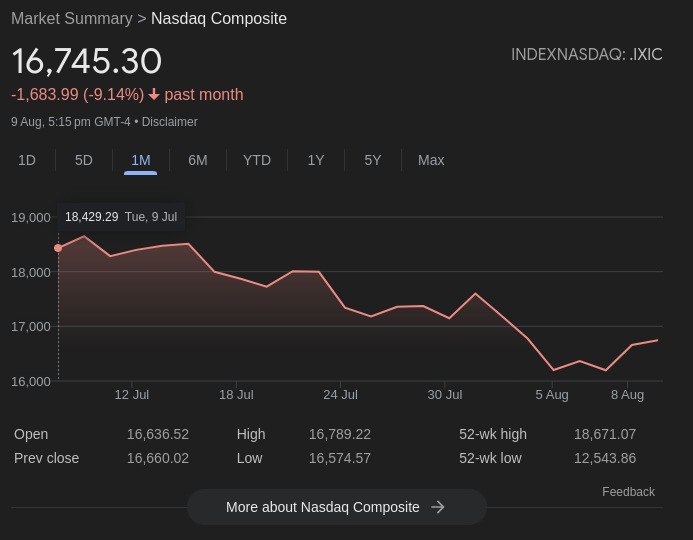

- In point 1, we spoke about foreign assets, the impact was also felt on US stock markets. Sell-off plus the unexpected jobs report in the US (which suggested the economy slowing down more than expected), and the hint from the Fed for rate cuts through the year all added to the frenzy. It is really difficult to put a finger on a few things and say for sure. Am relying mostly on the analyst reports I have seen.

The unemployment data we were speaking about also triggered something called a Sahm rule, which is a recession indicator based on how much job additions are slowing down, here is Shubh from our team explaining how it works,

All of these prompted analysts to start saying the Fed funds rate is too high, too restrictive for businesses to borrow, and too high for economic activity to catch up, and hence rate cuts should have been done already. Hence behind the curve. ![]()