Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

Zohra Khan on the business of Indian EV infra

India’s EV adoption is now less dependent on the vehicles, and more everything it plugs into — the charger, the connector, the software, the protocols that charging networks use to talk to one another, and, most importantly, the ageing Indian electricity grid beneath all of it.

To make sense of all this, we spoke to Zohra Khan, founder & CEO of IPEC, which designs and manufactures EV chargers for India’s leading two- and three-wheeler OEMs, to understand what it actually takes to build charging infrastructure at scale in India.

You can also listen to the full conversation on Spotify and Apple Podcasts. The full transcript of the podcast is below if you prefer to read.

In today’s edition of The Daily Brief:

- The country without interest

- The tower of sovereign debt gets more twisted

The country without interest

At the end of March 2025, Japanese households held more than half their financial assets in cash and bank deposits.

Globally, this is an unusual way to hold one’s wealth, at least in advanced economies. In the United States, for instance, cash makes up just 11.5% of household financial assets. Meanwhile, over 40% of American wealth is held in equities. Japanese households, meanwhile, had invested just over 12% of their financial assets in equities. In fact, even Indian households hold less cash and more equity — even though ours is a far less developed economy.

There’s a reason for this. In most of the world, cash keeps bleeding its value, gnawed down by inflation. Idle money loses its purchasing power. You can only protect the value of your wealth if you invest it in something productive.

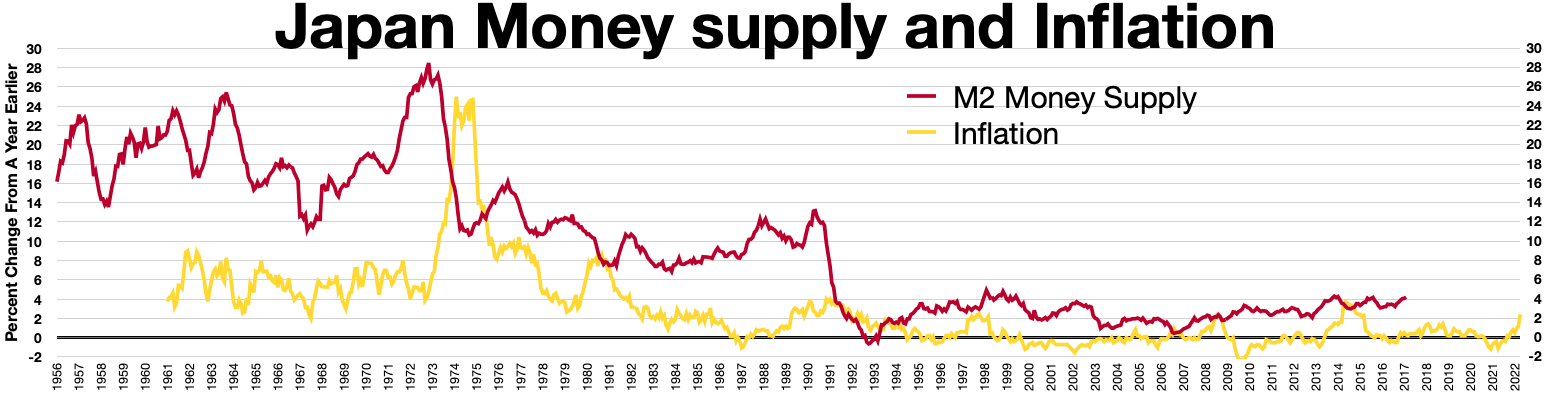

Japan, however, learnt a different lesson from history. Its financial life was frozen in time. For decades, prices barely moved. Wages barely moved. Your bank would barely pay any interest for the money you deposited with them, but that was alright. At least it kept its value. Nothing else could promise that.

Most Japanese had lived through an apocalyptic collapse in their stock and property markets back in the 1980s. The economy never recovered. If you invested in the Japanese stock markets in 1989, you wouldn’t see a single yen in returns until twenty-five years later, in 2024.

In an economy like this, rationally, cash was the only safe option. And as it remained stuck year-after-year, that rational choice became culture .

That era lasted for three decades. Holding cash, for all those years, came with no cost. That fact shaped Japanese financial life — how households saved, what firms charged, how the government borrowed, and what the Yen meant for outsiders.

And then, with the chaos of recent years, inflation returned. With that, interest rates finally returned as well. What does the return of a price of money do to a country that had forgotten all about it? Nobody can tell you for sure.

The missing price of money

Japan’s economic stupor was born out of a period of irrational excitement. In the late 1980s, Japanese stock and land prices had become a national mania. When that bubble was eventually punctured, the floor fell off. Assets collapsed in price. Banks were held with mountains of bad debt. Firms stopped investing. An economy that once threatened the United States’ dominance lost all its buoyancy.

The country suddenly found itself in a waking nightmare. The economy’s momentum had stalled to a point where people refused to invest even when money was practically free. Prices were falling, to a point where opening a business no longer made sense. Whenever there was a flutter of optimism, disasters like the Global Financial Crisis or the 2011 Tōhuku earthquake broke its back again. Ordinary monetary policy lost its power.

Japan tried everything it could to get out of this bind. By 1999, interest rates were zero. In the 2000s, it began quantitative easing — flooding banks with money by buying banks’ assets. In 2016, it even tried negative interest rates, effectively punishing people for keeping money idle. Then, it began to control the rate on long-term government borrowing as well, buying 10-year bonds indiscriminately from the market. Nothing worked.

A new normal had taken hold.

How an interest-free economy works

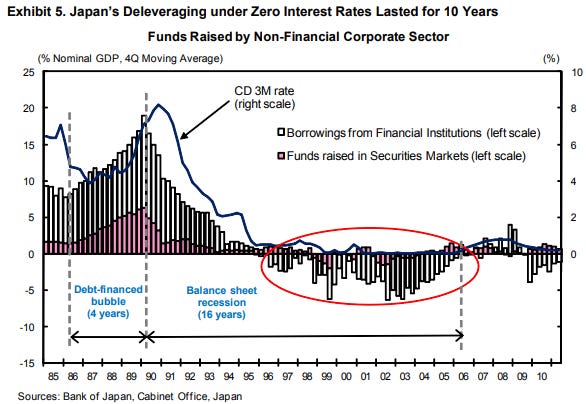

So brutal was Japan’s bubble bust that companies fundamentally changed their character. Japan went into something the economist Richard Koo calls “balance sheet recession”. Businesses no longer behaved like profit-making machines. For ten straight years, all their cash went into paying off debts and cleaning up their balance sheets.

Debt, meanwhile, became taboo. Companies would not borrow to expand their operations, even if you offered them that money for free . This is why even when interest rates hit zero, no investment followed.

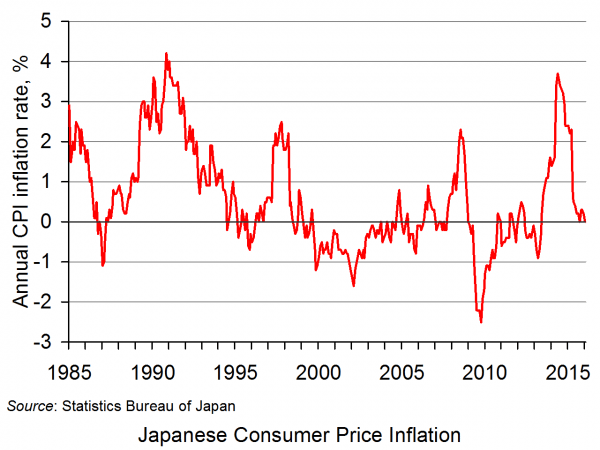

This fuelled a doom loop. As the economy teetered and investments stopped, jobs disappeared. The country went into an “employment ice age.” Those that kept their jobs had to take wage cuts. With things so desperate, people stopped spending, delaying purchases as much as they could. Companies had to slash prices to keep selling. For long periods, Japan went into deflation.

Like a snake devouring its own tail, the cycle fed itself. With chronically low demand, firms had no reason to invest in expansions. People’s wages, as a result, stayed still — pushing them out of the market. That, in turn, kept prices low. Over time, this logjam hardened into expectation — people learnt that wages and prices would both stay the same.

In such an environment, a Japanese bank had little chance of finding yields at home. The only way to get any return was to lend for very long — thirty-forty years into the future — or go abroad. Similarly, insurers saw their business model stall. They needed to grow their money to pay for future claims, but Japan lacked opportunities to do so.

The only serious demand for money came from the Japanese government: which could borrow staggering sums, for very long periods, at miniscule rates. By the end of fiscal 2024, outstanding Japanese government bonds totalled to ¥1,171.1 trillion: two-and-a-half times the size of the country’s GDP. The average bond matured in nearly ten years, at an interest of just 0.83%. After years of quantitative easing, by 2024, nearly half those bonds were held by the Japanese central bank itself.

Outside Japan, however, Japan’s frozen economy opened space for a new trade.

A global investor could borrow yen from Japan, sell them in exchange for something else — dollars, rupees, pesos, whatever — and then invest it in something that promised returns. Those returns were yours to keep. The only real risk was if the yen appreciated too much before you repaid that yen loan. That happened every once in a while, sparking a panic through global markets. But as long as forex rates remained reasonably stable, this was free money.

According to an August 2024 assessment, the scale of these “carry trades” was more than ¥40 trillion — or over ₹23 lakh crore. A lot of this money reached us as well, often hitting our markets as FPI inflows. It’s hard to estimate how much — these trades are fundamentally opaque. But by some estimates, nearly a quarter of that money flowed into India.

Regime change

Japan imports nearly all its food and fuel.

For decades, we lived in a stable, globalised economy, where such arrangements were routine. In 2022, however, as Russian forces marched into Ukraine, both suddenly became expensive. At long last, Japan had seen a real bout of inflation.

In the short term, this was a bad thing for Japanese households, who suddenly found themselves poorer. But it created momentum in a cycle that had long been stalled.

In the following years, Japanese workers succeeded in meaningfully increasing their wages — especially since workers were scarce in its aging population. In 2024, for instance, Japanese workers negotiated an average wage increase of 5.1%. This was the highest increase they had seen in 33 years . In turn, this allowed the prices of goods and services to both appreciate. More importantly, at long last, people expected prices to rise — and began ordering their affairs accordingly.

With prices finally moving, the Bank of Japan started unwinding the many deflation-fighting measures it had put in place over the years. In March 2024, it finally did away with negative interest rates, setting them at 0-0.1%. It also culled some of its market interventions.

Then, it actually let interest rates rise . In July 2024, rates were hiked to 0.25%. They hit 0.5% in January 2025, and 0.75% in December 2025. And then, on July 16 this year, they breached the single-digit mark. For the first time since 1995, interest rates went up to 1%.

Sitting here, in India, that number probably looks like nothing. To a country that had learnt to expect free money, though, it was a sea change. Finally, after decades, money had a real price. The old regime had finally ended.

What this change means

This new moment will transform all of the Japanese economy, just as the zero inflation regime did thirty years ago.

Consider banks. On one hand, their lending margins might finally recover. At the same time, though, the value of their older bonds has fallen. If the government is now issuing bonds that pay real interest — say, at 1.5% — bonds they held from before, with rates somewhere near 0.5%, look unattractive. Those dropping values have sparked a meaningful decline in the capital base of many smaller banks. In time, their future incomes will improve, but the past has been marked down.

Life insurers saw the same dynamic: their assets have fallen in value. They’ve also turned cautious about buying super-long dated government bonds, as volatility has risen.

For the last many decades, these were the borrowers the government had banked on to fuel its heavy borrowing. Slowly, that is becoming more expensive. The government’s interest bills are growing rapidly. Its interest on general bonds has gone from ~¥8 trillion in fiscal 2024, to over ~¥10 trillion in fiscal 2025, to over ¥13 trillion in fiscal 2026. In Fiscal 2026, across instruments, it’s paying ¥31.3 trillion for debt servicing — a quarter of its budget. As old, cheap bonds fade away over the next decade, this burden will keep increasing year-on-year.

Of course, most of the government’s bonds are currently held by the Bank of Japan. That has its costs. According to the BOJ’s own surveys, the median market participant considers the market terribly impaired. Now, with inflation finally back, the BOJ is stepping back, with plans of unloading ¥350–370 trillion of bonds by March 2030.

As the Japanese economy recovers to a semblance of normalcy, something unusual has happened. Ordinarily, stock markets hate a rate hike. In Japan, however, this was seen as a signal: that the country would see higher nominal growth, while cash, like in the rest of the world, would start losing value. This resulted in a surge of money hitting the Japanese stock markets — with the Tokyo Stock Price Index practically doubling in three years.

And while there’s no recent data on the carry trade — the data is hard to collect — there are chances that it has shrunk meaningfully. This might even be a tiny piece of our own FPI outflows.

Together, this points to a momentous transition. Japan is shedding the vestiges of an old regime, and learning to live within a new one. This adjustment will come with friction. Japan has made many choices over three decades — embedded in portfolios, pricing habits, balance sheets and debt structures. This will all take years to unwind.

The old world is dead. Who knows what the new one will look like.

The tower of sovereign debt gets more twisted

For most of modern financial history, a government’s balance sheet used to be very simple. They had fewer types of creditors, fewer financial instruments, and clearer legal arrangements. That’s how sovereign debt used to work.

The hierarchy of paying off sovereign debt was also legible: the IMF was at the top, and below it were developed-nation creditors (known as the Paris Club) and commercial banks below, both at broadly the same rank. When a country couldn’t pay, everyone knew the rules. Creditors coordinated through the Paris and London Clubs, and debt sustainability analyses worked because the stock of debt was transparent enough to analyse. To be sure, the process was painful for the debtor country, but rules were clearer.

That simplicity is now eroding.

Over the past decade, the liability structures of emerging markets have become incredibly more complicated with new financial instruments. And this matters enormously, because it changes what happens when things go wrong, especially for poor and developing countries.

For instance, when Zambia defaulted in 2020, it took over four years to reach even a partial resolution. It wasn’t because of someone gaming the system, but because nobody could agree on who was owed what, who ranked where in the repayment queue, and who should absorb the losses. Ethiopia, meanwhile, has been stuck in restructuring mode for a few years. The old machinery of sovereign debt workouts, which were built for a simpler world, is struggling to process what sovereign debt has become.

Much of this story is based on two recent reports by financial advisory firm Lazard and the World Bank. Let’s dive in.

The invisible pecking order

The first layer of this new complexity is an unofficial hierarchy of claims that has crystallised across emerging-market sovereign debt.

In theory, besides institutions like the IMF, most government creditors lend on somewhat equal terms. In the event of a repayment, there should not be highly-preferential arrangements amongst creditors. But in practice, a steep pecking order has emerged that determines who gets paid first. And much of it is invisible to the people at the bottom.

At the top sits the IMF, protected by convention as the lender of last resort. Below it are the major multilateral development banks like the World Bank and the African Development Bank. Their “preferred creditor status “ means they typically avoid taking losses, so long as they keep lending through a crisis.

Then come commercial creditors who happen to be guaranteed by one of these multilaterals: if anything goes wrong, the guarantee kicks in, and they’re repaid the guarantee amount. Now, below all of them sit collateralised creditors — lenders who’ve secured their loans against specific government assets or future revenue streams. Then come regional development banks with weaker protections. And at the very bottom are unsecured creditors who absorb the consequences of everyone else’s protection.

The existence of this hierarchy is just part of the problem, though. Additionally, it is largely implicit, hardly codified on paper, and it’s getting more rigid.

See, for instance, multilateral banks increasingly offer guarantees to commercial lenders to attract private money into financing developing countries. That’s a powerful multiplier for development finance, but it also creates a structural trap. When a lender activates that guarantee during a debt restructuring exercise, their commercial claim effectively transforms into a preferred multilateral claim . And everyone below sees their recovery shrink.

This hierarchy isn’t stable, either. Creditors are actively competing to climb it.

For instance, China’s government-owned policy banks are now the largest bilateral creditors to low- and middle-income countries. But they frequently resist being classified as either “official “ or “commercial “ creditors. Additionally, they often require that their loan terms remain confidential. We covered this in a recent story on China’s debt diplomacy.

This ambiguity directly influences who’s involved in the debt restructure and in what sequence In Zambia, where China was the dominant bilateral lender, this contested ranking was a primary cause of years of delay.

The race to collateralise

Within this hierarchy, the collateral attached to this debt deserves its own scrutiny.

Angola is the clearest case study. After its civil war ended in 2002, Angola rebuilt largely on credit from Chinese policy banks, repaid not in cash but in future oil shipments. By 2011, the country had borrowed more than $20 billion against its oil revenues. And much of it was barely visible to the outside world.

This goes deeper than one country. A landmark study by the Natural Resource Governance Institute examined 52 resource-backed loans signed between 2004 and 2018, worth a combined $164 billion. Thirty of these, worth $66 billion, went to sub-Saharan Africa, with 53% of that amount supplied by China’s two main policy banks. Somehow, only one of the 52 contracts was made public.

When World Bank researchers later tried to cross-check the sub-Saharan loans against their own Debtor Reporting System, they could identify only half. Some had been booked not as debt at all, but as advance payments to suppliers instead.

Then, collateral becomes a way for each creditor to demand their piece if they’re not paid. If pledging a revenue stream reliably moves a lender up the repayment queue, then every new creditor will demand that protection. Whoever lends without collateral, and earliest, is only pushed further down the repayment schedule.

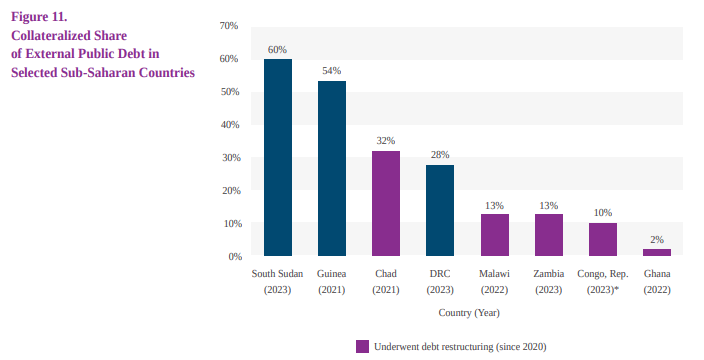

The numbers across many African countries bear this out: collateralised debt makes up 60% of external public debt in South Sudan, 54% in Guinea, 32% in Chad, and 28% in the Democratic Republic of Congo. Three of the four countries that sought debt restructuring featured resource-backed loans.

Angola is now trying to exit this model. It stopped contracting oil-backed loans in 2017, and has been reducing its Chinese debts. But the exit itself — replacing Chinese lending with Western private capital — is expensive, since it means paying higher interest rates. But moreover, this exit causes new problems in the repayment schedule.

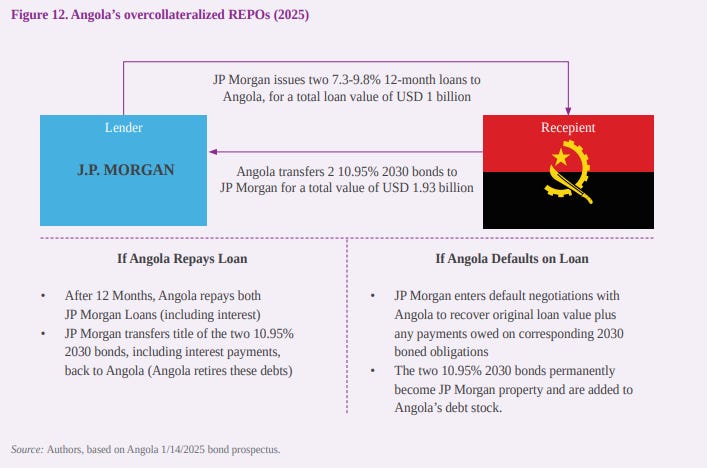

See, in 2025, Angola borrowed $1 billion from JP Morgan, and handed over $1.93 billion worth of newly-issued bonds as collateral. If it pays JP Morgan, the collateral gets returned, and Angola can service it at its own pace.

If Angola actually fails to pay the new loans, JP Morgan will assume full ownership of the collateral. That, in turn, dilutes the claims of any past creditors in Angola’s capital structure, pushing JP Morgan up the ladder, and Angola loses freedom in servicing the bonds it first issued. In other words, the hierarchy ends up being a different shade of complicated, not less.

When the music stops

All of this cascades on top of each other precisely when a country defaults and needs to restructure its debt.

The G20 Common Framework was supposed to handle exactly this. Launched in 2020, it was designed to bring China and other non-Paris Club bilateral lenders into a structured, predictable restructuring process alongside traditional creditors. Four countries have applied: Chad, Ethiopia, Ghana, and Zambia.

But, as you probably guessed already, the results have been sobering.

The first domino to fall was Zambia, which defaulted in November 2020 — the first African sovereign to do so during the pandemic. It applied for the Common Framework almost immediately. The official creditor committee, co-chaired by China and France, reached a memorandum of understanding in 2023. But the first bilateral implementation agreement, which was with France, wasn’t signed until December 2024. That’s over four years from default to even partial resolution.

Ethiopia’s experience has been worse — it applied in early 2021 and, five years later, is still negotiating piecemeal, with bilateral agreements only being signed this year, and bondholders threatening litigation. The Common Framework has been very slow in helping with debt restructuring.

Why so? Well, before anyone can negotiate haircuts, the parties first need to figure out who’s owed what and where they sit in the queue. In Zambia, the core dispute was comparability of treatment. China insisted that the bondholders restructuring Zambia’s $3 billion in Eurobonds were getting a better deal than bilateral creditors had been offered, but the bondholders disagreed.

Zambia was caught in the middle, unable to resolve a fight between its own creditors over whose losses were truly comparable, partly because the full scope of secured and unsecured claims was never transparent to begin with.

Even the instruments designed to fix restructurings can make things worse.

For instance, take value-recovery instruments. They compensate creditors if a country’s economy outperforms certain projections, and emerged partly because creditors and debtors disagreed about future growth prospects of the country, and partly because creditors stopped trusting the IMF’s forecasts of other countries. That’s understandable, but they make the debt burden swing in ways that are hard to model and harder to negotiate around.

The textbook example where those dynamics came into play was Greece, which, as we covered earlier, underwent the largest sovereign debt restructuring in history in 2012. As part of the deal, creditors received GDP-linked warrants that would pay out more if Greece’s economy performed better than expected over the following decades. The idea was simple: creditors would accept losses immediately but retain some upside if Greece eventually recovered.

The problem was that these instruments were extraordinarily difficult to value. For years, Greece’s economy remained weak, making the warrants appear nearly worthless. But as the country’s recovery gathered pace in the 2020s, investors began to expect larger future payouts. Greece then exercised a contractual option to buy back the warrants, triggering a dispute over their fair value. Creditors argued the instruments were worth far more than the buyback price, leading to years of litigation in London courts until recently when Greece won the case.

India, incidentally, is no longer a bystander in this system. It co-chaired Sri Lanka’s Official Creditor Committee alongside Japan and France, and signed the Zambia memorandum of understanding as a bilateral creditor. As India’s bilateral lending grows, it will increasingly face the same classification and coordination questions that have tangled up these restructurings.

Conclusion

Not all new complexity is harmful. Climate-resilient debt clauses and genuine state-contingent instruments can build automatic relief into a contract, sparing a country the need to default and renegotiate every time a hurricane hits. The distinction isn’t between old and new instruments per se, but rather between instruments that are contingent and transparent, and those that are opaque and subordinating.

A few things would help, like clarity on who actually enjoys preferred creditor status, debtor-creditor data reconciliation, legal reforms to close the loopholes that allow off-balance-sheet borrowing, and the ability of countries to write buyback options into complex instruments from day one, so they can simplify their structures once they can afford to.

In the 1980s, the hard part of a sovereign debt crisis was usually distributing losses across banks. In the 2000s, it was neutralising holdouts, who were creditors that refused to participate in a restructuring process that everyone else accepted. In the 2020s, the hard part is figuring out which debts are official, private, guaranteed, collateralised, domestic, external, preferred, or contingent, all before the restructuring can even begin.

Tidbits:

- The Ministry of Railways approved a ₹755 crore, 42-km third railway line between Champa and Korba under Mission 3000 MT, expected to add 5.95 MTPA freight capacity and generate ₹85 crore in additional annual earnings.

2.Source:* ET - Tamil Nadu announced ₹15,032 crore to build 231 new substations alongside 121 already underway at ₹10,109 crore, with a separate ₹2,275 crore earmarked for Chennai’s urban distribution upgrade and plans to recruit 15,058 electricity personnel.

4.Source:* The Hindu BusinessLine - India’s textile and apparel exports fell 2% to $35.80 billion in FY26 from $36.61 billion, with the rupee’s slide from 86.60 to 94.83 providing currency support even as US tariff uncertainty and West Asia slowdown weighed on volumes.

6.Source:* The Hindu

- This edition of the newsletter was written by Pranav and Manie.

Over 2 crore Indians invest with Zerodha. Open a free demat account in minutes and invest in stocks, mutual funds, ETFs, and bonds at 0 brokerage. No hidden charges, no gimmicks. Plus, get free access to research tools like Tijori, Sensibull and more.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Subtext by Zerodha

Subtext by ZerodhaThank you for reading. Do share this with your friends and make them as smart as you are ![]()