Japan’s benchmark Index, Nikkei hit a 33-year high, levels last seen in 1990.

What caused the fall?

The Japanese stock market crash is one of the most spectacular crashes in the history of financial markets. 33 years from the peak, it’s still 20%+ down from the peak.

Japan was one of the most advanced economies in the world. What caused the downfall since? Why did it take 33 years to reclaim the levels reached in 1990 and is still 25% down from its all time highs? A note on what happened in the 80s and why the japan bubble popped.

Historical PE multiples

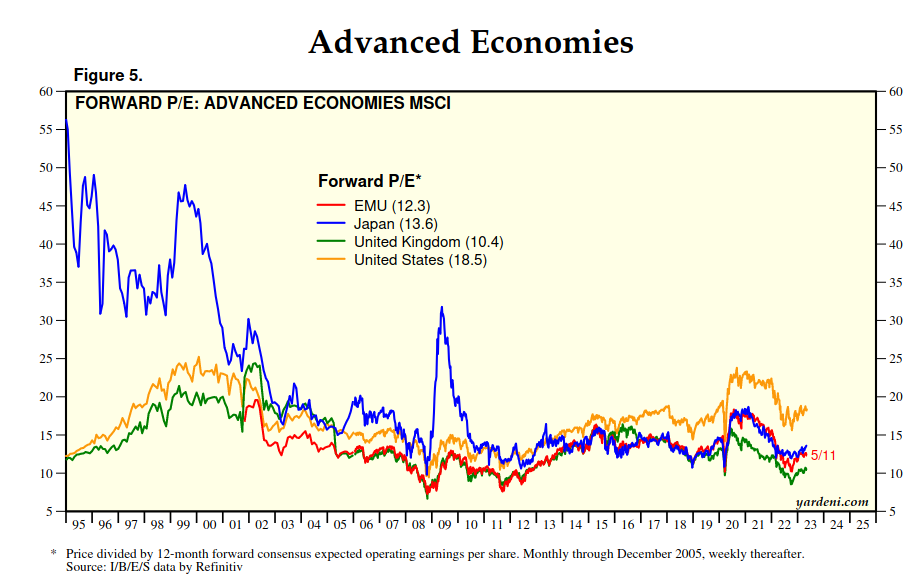

Advanced Economies

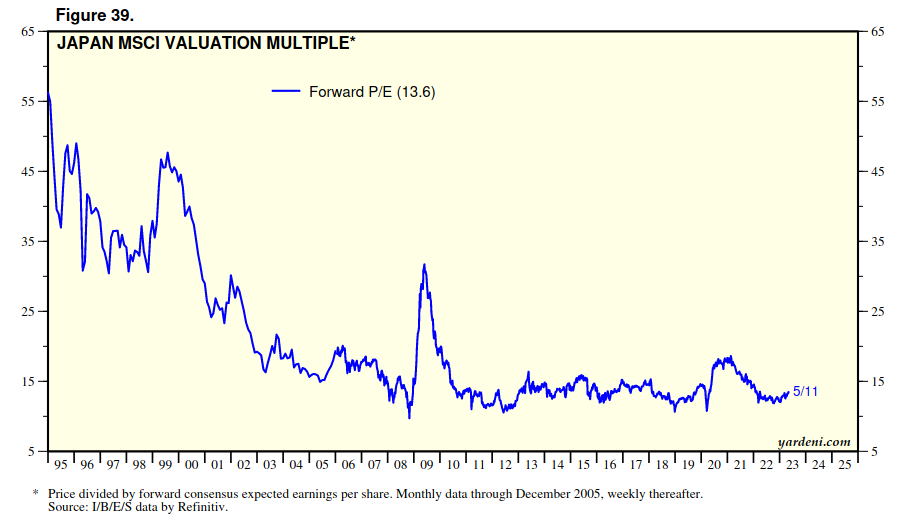

Japan

Only from the last 20 years, the PE multiples of advanced economies are more or less moving in tandem. Before that, the valuations of Japanese markets were skyrocketing like Adani stocks did in the last couple of years.

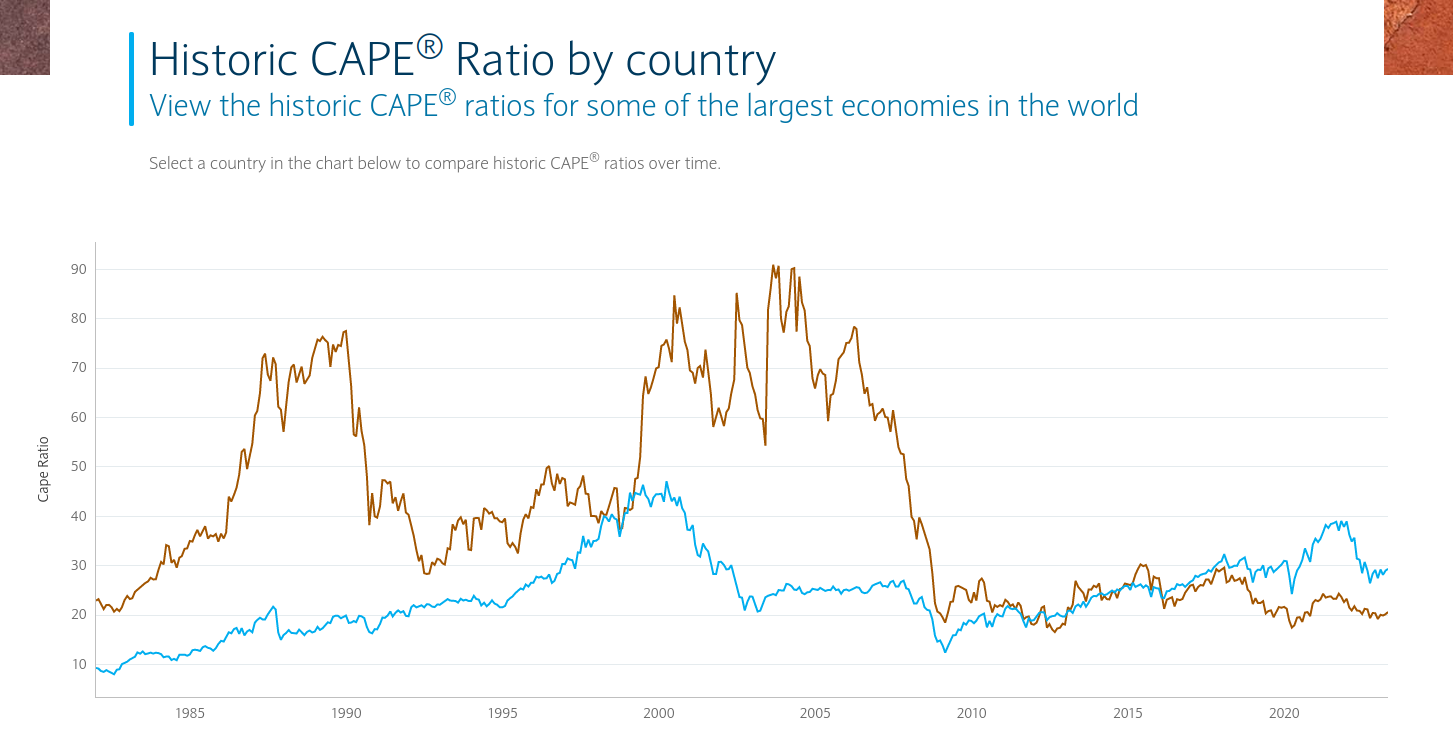

CAPE Ratio:

-

The PE ratio when adjusted to inflation across the last 10 years is called the CAPE Ratio. It stands for “Cyclically-Adjusted Price-to-Earnings Ratio”. It is mainly used to assess long-term financial performance, while isolating the impact of economic cycles.

-

Between 1985 and 2005, the spreads between the CAPE ratio of Japan (in red) and the US (in blue) ranged between 20-70 PE with Japan being costlier by that much variation.

What was the Japanese multi asset bubble?

For starters, Skyrocketing Real Estate and euphoric stock market moves.

Edward Chancellor, in his book Devil Take the Hindmost provided stats on the Japan real estate and stock market bubble from the 1980s:

- Land prices increased 5000% from 1956 to 1986 though consumer prices only doubled in that time.

- In the 1980s, share prices increased 3x faster than corporate profits for Japanese corporations.

- By 1990, the total Japanese property market was valued at over 2,000 trillion yen or roughly 4x the real estate value of the entire United States.

- The grounds on the Imperial Palace were estimated to be worth more than the entire real estate value of California or Canada at the market peak.

- There were over 20 golf clubs that cost more than $1 million to join.

- In 1989, the P/E ratio on the Nikkei was 60x trailing 12 month earnings.

Source: Ben Carlson’s blog

What caused the bubble?

It was pure private greed and government mistakes as Robert J. Samuelson says in this Washington post article.

What did the Japanese Government do?

Between 1985 and 1989, the Bank of Japan kept interest rates very low. The yen was rising on foreign exchange markets, making Japan’s exports more expensive abroad.

The idea was to stimulate domestic spending to offset a feared loss of exports. The key discount rate dropped to 2.5 percent. Easy credit fueled an explosion of corporate investment in new equipment and factories, residential and office construction.

What followed after that was rampant speculation in both real estate and stock markets with residential land values in major cities rising 167% and the stock market doubling within no time.

How did the bubble burst?

- After realizing that this level of growth and speculation isn’t sustainable and hyper inflation is the most likely outcome, in late 1989, Yasushi Mieno–the bank’s new head, began to raise interest rates sharply. Without easy credit, the speculative machine went into reverse. Land prices, the stock market and corporate investments began to slide. The economy slowed dramatically.

Does this sound similar to how various scammy stocks/ SPACs/crypto tokens rallied during the pandemic? And what happened later? Yeah, history often keeps repeating itself. ![]()

What happened in the 90s to Japan?

-

As per the IMF, The 1990s were very difficult for the Japanese economy. Toward the end of the decade, Japan experienced a recession of depth and duration virtually unprecedented for a major industrial country since World War II; a recession from which it has only recently begun to recover.

-

In fact, from 1991 to 1999, output growth averaged only a little over 1%, compared with around 4% achieved in the 1980s.

-

This is proportionate to earning ₹2000 per month right after earning ₹2 lakh a month; that too for the majority of the economy.

-

This experience has led macroeconomic policymaking into uncharted territory and called into question many of the most basic tenets about the behavior of Japan’s economy, including the growth rate of potential output, the effectiveness of fiscal and monetary policies, and the strength of the Japanese system of corporate governance.

What’s buzzing in the last few months?

With valuations coming to historically value buy zones and with levels on par with global indices and looking historically cheap, there is a renewed interest among Investors to buy Japanese stocks.

Warren Buffett recently visited Japan and said that he is keen on adding more Japanese stocks.

Japanese companies are also rewarding their shareholders handsomely off late.

On the hopes of lower inflation, JPY is at a 52 week high against the dollar, lifting shares of exporters and increasing the purchasing power of dollar-based investors looking to buy Japanese stocks.

One wonders if it’s finally a good time to be an Investor in Japanese markets after all these years. ![]()

More reading:

https://www.brookings.edu/wp-content/uploads/2016/07/1998b_bpea_lincoln_friedman.pdf