First, i will choose 1 hour time frame 11:15 to 12:15 chart and mark the high-low of candle. now switch to 3 min chart and as the 3 min candle breaks the high and low of the candle, i choose long or short. my SL will be low and high of the same candle

Not good for nifty and bank nifty.

this script, had some other indicators, to make them invalid, set macd limit 0 , cci to 0 ,like that . ci chopiness index to 1000,like that ,use indicator values against to its reference values .

//@version=5

strategy("Candle Intraday", overlay=true ,calc_on_every_tick =true )

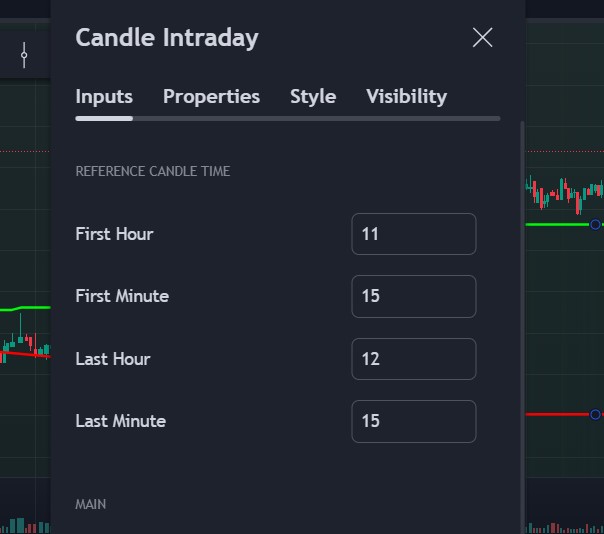

FirstCandleHour = input.int(defval=9, title="First Hour", minval=1,group = "Reference Candle Time")

FirstCandleMinute =input.int(defval=15, title="First Minute", minval=0,group = "Reference Candle Time")

LastCandleHour = input.int(defval=9, title="Last Hour", minval=1,group = "Reference Candle Time")

LastCandleMinute =input.int(defval=30, title="Last Minute", minval=0,group = "Reference Candle Time")

orderLimit = input.int(defval=4, title="Order Limit per Day", minval=1,group = "Main")

MinOrderLifeBars = input.int(defval=2, title="MinOrderLifeBars", minval=1,group = "Main")

nofVolumeCandles = input.int(3, title="Number of Lastc CandleVolume",group = "Volume")

VolumeLimit = input.int(0, title="VolumeLimitToCross",group = "Volume")

// Inputs for the strategy

cciLimit = input.int(defval=0, title="cciLimit", minval=0,group = "Indicators")

rsiUpLimit = input.int(defval=0, title="rsiUpLimit", minval=0,group = "Indicators")

rsiDownLimit = input.int(defval=100, title="rsiDownLimit", minval=0,group = "Indicators")

macdLimit = input.float(defval=0, title="macdLimit", minval=0,step=0.01,group = "Indicators")

ciLimit = input.float(defval=80, title="ciLimit", minval=0,step=0.01,group = "Indicators")

dailyPnLTakeProfit = input.int(defval=2000, title="Daily PnL Limit",group = "Orders")

dailyPnLStopLoss = input.int(defval=-1200, title="dailyPnLStopLoss",group = "Orders")

StopLossPerOrder =input.int(defval=-900, title="StopLossPerOrder",group = "Orders")

TakeProfitPerOrder =input.int(defval=1000, title="TakeProfitPerOrder",group = "Orders")

showHighLowLines = input.bool(defval = true,title = "Draw Lines")

AdditionalPercentage =input.float(defval=0.0001, title="AdditionalPercentageToHighLow", minval=0,step=0.0001)

perOrderValue = input.int(defval=10000, title="perOrderValue", minval=1000)

endHour = input.int(defval=15, title="EOD Hour", minval=1,group = "Intraday ")

endMinute =input.int(defval=15, title="EOD Minute", minval=0,group = "Intraday ")

orderEndHour = input.int(defval=14, title="OrderEod Hour", minval=1,group = "Intraday ")

orderEndMinute =input.int(defval=15, title="OrderEOD Minute", minval=0,group = "Intraday ")

isOrderEOD = (hour(time) <= orderEndHour)

// Initialize a counter to track the number of orders per day

var int orderCount = 0

// Get the current day

var int totalDays = 0

var int Windays=0

var int LostDays=0

var int firstCandleBarIndex = na

var int CandleBarIndex = na

var float CandleHigh4 = 0

var float CandleLow4 = 0

var float DayHigh = 0

var float DayLow = 0

var float DayOpen = 0

var float DayClose = 0

var float dailyPnL = 0.0

var bool dayTakeProfitReached = false

var float runningPnl=0

var int LastOrderType =0

var float MaxPnl=0

var float MinPnl=0

var bool StoptradingForDay = false

var int NopeDays =0

var bool isOrderRunning = false

// Check if it's the end of the day

isEndOfDay = (hour(time) == endHour and minute(time) == endMinute)

if (runningPnl < dailyPnLStopLoss)

StoptradingForDay:=true

// Close all trades at the end of the day

if (isEndOfDay)

LastOrderType:=0

strategy.close_all("EOD","EOD")

orderCount := 0

MaxPnl:=math.max(runningPnl,MaxPnl)

MinPnl:=math.min(runningPnl,MinPnl)

DayHigh := na

DayLow := na

if(runningPnl < 0)

LostDays :=LostDays-1

if(runningPnl > 0)

Windays :=Windays+1

if (runningPnl==0)

NopeDays:=NopeDays+1

// Reset daily stats on new day

if (dayofweek != dayofweek[1])

isOrderRunning:=false

StoptradingForDay:=false

isEndOfDay:=false

LastOrderType:=0

dailyPnL := strategy.netprofit

dayTakeProfitReached := false

totalDays :=totalDays+1

orderCount := 0

DayHigh := 0

DayLow := 0

firstCandleBarIndex:=0

isFirstCandle = (hour(time) == FirstCandleHour) and (minute(time) == FirstCandleMinute)

isLastCandle = (hour(time) == LastCandleHour) and (minute(time) == LastCandleMinute)

isLastCandleCrossed = (hour(time) < LastCandleHour) or ( hour(time) == LastCandleHour and minute(time) < LastCandleMinute)

if (isFirstCandle)

firstCandleBarIndex := bar_index

if (isLastCandle)

CandleBarIndex := bar_index

var float time1 = na

var float time2 = na

if (bar_index ==firstCandleBarIndex)

DayOpen := open

DayClose := close

DayLow := low

DayHigh := high

time1 := time

if ( DayOpen !=0 and isLastCandleCrossed )

DayHigh := math.max(DayHigh, high *(1+AdditionalPercentage))

DayLow := math.min(DayLow, low *(1-AdditionalPercentage))

plotshape(series= bar_index== firstCandleBarIndex and showHighLowLines, location=location.belowbar, color=color.blue, style=shape.diamond, text="First", title="FirstCandle")

plotshape(series= bar_index== CandleBarIndex and showHighLowLines, location=location.belowbar, color=color.blue, style=shape.diamond, text="Last", title="LastCandle")

var float timeDiff=0

if (bar_index == CandleBarIndex+1)

time2 := time

timeDiff := ((time2 - time1)/ 60000)

plot(showHighLowLines ? DayHigh > 0?DayHigh:na : na, color=#00fe08fb, linewidth=2, title="Candle High")

plot(showHighLowLines ? DayLow>0?DayLow:na : na, color=#f70000, linewidth=2, title="Candle Low")

// Track running PnL

runningPnl := (strategy.netprofit - dailyPnL)+ strategy.opentrades.profit(strategy.opentrades - 1)

plot(showHighLowLines ? na : runningPnl, title="Running PnL", color=runningPnl >= 0 ? color.green : color.red, style=plot.style_area)

// Calculate combined volume

combined_volume = 0.0

for i = 0 to nofVolumeCandles - 1

combined_volume := combined_volume + volume[i]

combined_volume :=combined_volume/1000

cciVal = ta.cci(hlc3,20)

fastMA = ta.ema(close, 12)

slowMA = ta.ema(close, 26)

macd = fastMA - slowMA

ci = 100 * math.log10(math.sum(ta.atr(1), 14) / (ta.highest(14) - ta.lowest(14))) / math.log10(14)

rsi = ta.rsi(close,14)

isOpenOkay = not na(DayHigh) and not na(DayLow)

mainCondition1 = isOpenOkay and isOrderEOD and combined_volume > VolumeLimit and ci < ciLimit and bar_index > CandleBarIndex and strategy.opentrades.size(0) == 0 and orderCount < orderLimit and dayTakeProfitReached == false and strategy.opentrades == 0 and StoptradingForDay==false

longCondition = mainCondition1 and close > DayHigh and cciVal > cciLimit and macd > macdLimit and rsi > rsiUpLimit and LastOrderType !=1

shortCondition = mainCondition1 and close < DayLow and cciVal < -cciLimit and macd < -macdLimit and rsi < rsiDownLimit and LastOrderType !=-1

plot(showHighLowLines ? na : cciVal, title="cciVal", color=color.blue, style=plot.style_area)

//longCondition = mainCondition1 and close > DayHigh and cciVal > cciLimit and macd > macdLimit and LastOrderType !=1 and rsi > 70

//shortCondition = mainCondition1 and close < DayLow and cciVal < -cciLimit and macd < -macdLimit and LastOrderType !=-1 and rsi < 30

var float quantity = int(perOrderValue*5/DayHigh)

// Get the current symbol's name

symbolName = syminfo.tickerid

// Define suffixes for different types (this is just an example, adjust as needed)

isFutures = str.contains(symbolName, "1!")

if (isFutures)

quantity:=1

var int orderRunTime = na

// Place orders based on the close price

if (longCondition)

LastOrderType :=1

orderCount += 1

isOrderRunning:=true

orderRunTime := bar_index

strategy.entry("Long", strategy.long,qty=quantity)

alert('{"Symbol": "' + syminfo.ticker + '", "Action": "Buy", "Remarks":"Starting"}', alert.freq_once_per_bar_close)

if ( shortCondition )

LastOrderType :=-1

orderCount += 1

isOrderRunning:=true

orderRunTime := bar_index

strategy.entry("Short", strategy.short,qty=quantity)

alert('{"Symbol": "' + syminfo.ticker + '", "Action": "Sell", "Remarks":"Starting"}', alert.freq_once_per_bar_close)

if (strategy.opentrades != 0)

if (LastOrderType > 0)

if(close < DayLow)

strategy.close_all()

if (LastOrderType < 0)

if(close > DayHigh)

strategy.close_all()

var int StopLossHits =0

var int TakeProfitHits =0

//StopLossPerOrder

if (strategy.opentrades.profit(strategy.opentrades - 1) < StopLossPerOrder and ( bar_index > orderRunTime + MinOrderLifeBars))

strategy.close_all()

StopLossHits := StopLossHits +1

if (strategy.opentrades.profit(strategy.opentrades - 1) > TakeProfitPerOrder and (bar_index > orderRunTime +MinOrderLifeBars))

strategy.close_all()

TakeProfitHits:=TakeProfitHits+1

if(runningPnl > dailyPnLTakeProfit )

dayTakeProfitReached := true

strategy.close_all()

if (isOrderRunning and strategy.opentrades ==0)

if (LastOrderType > 0)

alert('{"Symbol": "' + syminfo.ticker + '", "Action": "Sell", "Remarks":"Closing"}', alert.freq_once_per_bar_close)

if (LastOrderType < 0)

alert('{"Symbol": "' + syminfo.ticker + '", "Action": "Buy", "Remarks":"Closing"}', alert.freq_once_per_bar_close)

isOrderRunning := false

if( open > DayLow and open < DayHigh and strategy.opentrades ==0 and (bar_index > orderRunTime + 30))

LastOrderType:=0

normalizedPnL = (runningPnl + 2000) / 5000 * 20

// Set background colors based on conditions

bgcolor(runningPnl >= 0 ? color.new(color.green, 100- normalizedPnL) : color.new(color.red, 100-normalizedPnL), title="Up Background")

// Create table

var table myTable = table.new(position.top_right, 6, 18,bgcolor = color.white,frame_color = color.blue,frame_width = 1,border_color = color.gray,border_width = 1)

// Populate table

if barstate.isnew or barstate.islast

table.cell(myTable, 0, 0, "TotalDays")

table.cell(myTable, 1, 0, str.tostring( totalDays))

table.cell(myTable, 2, 0, "isFutures")

table.cell(myTable, 3, 0, str.tostring( isFutures) )

table.cell(myTable, 0, 1, "Strategy PNL")

table.cell(myTable, 1, 1, str.tostring(math.round(strategy.netprofit)) , text_color =strategy.netprofit > 0 ? #00ff00 : color.red ,bgcolor = color.gray)

table.cell(myTable, 2, 1, "MaxDayProfit")

table.cell(myTable, 3, 1, "+"+str.tostring(math.round(MaxPnl)))

table.cell(myTable, 0, 2, "WinDays")

table.cell(myTable, 1, 2, str.tostring(Windays))

table.cell(myTable, 2,2, "MaxDayLoss")

table.cell(myTable, 3, 2, str.tostring(math.round(MinPnl)))

table.cell(myTable, 0, 3, "LostDays")

table.cell(myTable, 1, 3, str.tostring(LostDays))

table.cell(myTable, 2, 3, "NopeDays")

table.cell(myTable, 3, 3, str.tostring(NopeDays))

table.cell(myTable, 0, 4, "DayTakeProfit")

table.cell(myTable, 1, 4, str.tostring(dailyPnLTakeProfit))

table.cell(myTable, 2, 4, "DayStopLoss")

table.cell(myTable, 3, 4, str.tostring(dailyPnLStopLoss))

table.cell(myTable, 0, 5, "OrderLimitPerDay")

table.cell(myTable, 1, 5, str.tostring(orderLimit))

table.cell(myTable, 2, 5, "perOrderValue")

table.cell(myTable, 3, 5, str.tostring(perOrderValue))

table.cell(myTable, 0, 6, "cciLimit")

table.cell(myTable, 1, 6, str.tostring(cciLimit))

table.cell(myTable, 2, 6, "macdLimit")

table.cell(myTable, 3, 6, str.tostring(macdLimit))

table.cell(myTable, 0, 7, "RefCandleTime")

table.cell(myTable, 1, 7, str.tostring(timeDiff)+"Min")

table.cell(myTable, 2, 7, "quantity")

table.cell(myTable, 3, 7, str.tostring(quantity))

table.cell(myTable, 0, 8, "StopLossPerOrder")

table.cell(myTable, 1, 8, str.tostring(StopLossPerOrder))

table.cell(myTable, 2, 8, "TakeProfitPerOrder")

table.cell(myTable, 3, 8, str.tostring(TakeProfitPerOrder))

table.cell(myTable, 0, 9, "StopLossHits")

table.cell(myTable, 1, 9, str.tostring(StopLossHits))

table.cell(myTable, 2, 9, "TakeProfitHits")

table.cell(myTable, 3, 9, str.tostring(TakeProfitHits))

table.cell(myTable, 0, 10, "RsiUpLimit")

table.cell(myTable, 1, 10, str.tostring(rsiUpLimit))

table.cell(myTable, 2, 10, "RsiDownLimit")

table.cell(myTable, 3, 10, str.tostring(rsiDownLimit))

table.cell(myTable, 0, 10, "VolumeLimit")

table.cell(myTable, 1, 10, str.tostring(VolumeLimit))

table.cell(myTable, 2, 10, "combined_volume")

table.cell(myTable, 3, 10, str.tostring(combined_volume))

table.cell(myTable, 0, 11, "Today PNL")

table.cell(myTable, 1, 11, str.tostring(runningPnl), text_color =runningPnl > 0 ? #00ff00 : color.white ,bgcolor = color.gray)