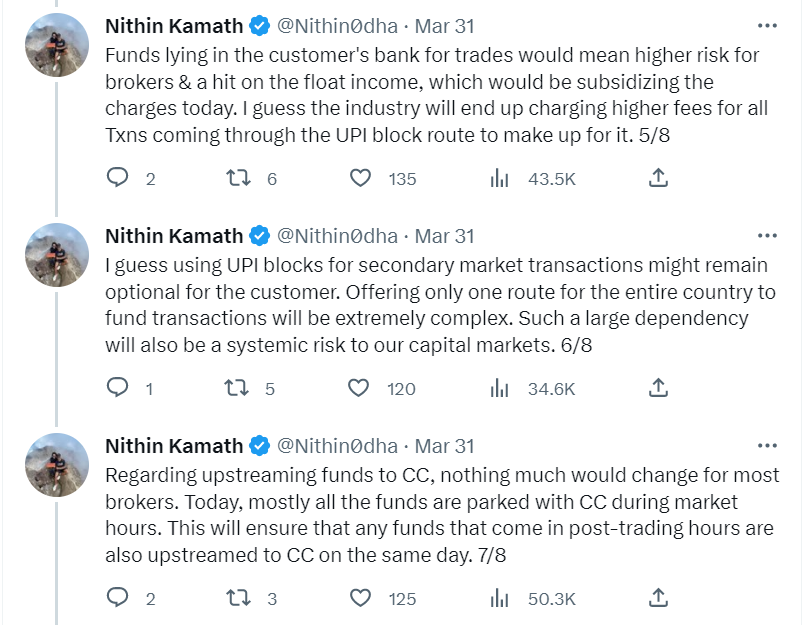

More than ASBA, I think what is being considered is how mandates work IPO using UPI. Tough to see how something like this can be implemented where there is risk involved (intraday trading, F&O, etc.). In all likelihood, I think this will be mostly for equity investing, where time is not of the essence. So allocate funds, get a mandate request through UPI, and place a buy order to invest once blocked. Similarly, first, block the security and then place a sell order.

I don’t think this move would affect the broking industry much; in any case, most equity investors withdraw funds themselves, or brokers send them out once a month. There might be some loss in income, but this will also mean a much lesser compliance burden and costs. Most people around us invest passively, and brokers might welcome the move if using this mechanism to invest reduces the compliance burden. I think the mandate route will be optional; otherwise, customers will not be able to place orders when the banking or UPI system is facing issues.

Today customers use brokers not just for execution; it is for everything from offering a trading platform to reporting to handling customer queries and reducing system risk. If exchanges can do all of these well, then brokers become redundant. I had written something earlier.

@nithin

Sir thankyou very much for your reply. I have understood that is is going to be tough for exchange to replace a broker.

But sir do you see that in future a sustainable 0 brokerage company can come into this industry. Like just to give an example. There is a broker FINVASIA which provides 0 brokerage but because of this the did not have large profits to invest in their platform. What I did is I used to trade with them but use your platform. At the end of the day I was saving lot of money. So what give zerodha an advantage was being used by me free of cost but I was giving business to somebody else.

There are still few was for a 0 brokerage company to earn only if they scale up. The get incentive from exchanges on certain volume of trade. If you have a lot of clients you can do more of cross selling. I think you can probably even sell your client data base. A zero brokerage company can take NBFC license, mutual fund license. They can get clients with 0 brokerage and earn money via cross selling.

This company FINVASIA has not even started marketing only because today they don’t have the technology to support heavy client base. They are slowly building it.

There are two types of trades - leveraged (intraday stock, F&O, etc) and non-leveraged (equity delivery paying 100% money upfront). In non-leveraged trades, the broker doesn’t take risks and can afford to offer a zero brokerage platform, provided there is some earning to sustain and grow the business. At Zerodha, we earn through our equity-only active customers by charging an AMC charge on demat.

Leveraged business is a business of risk, almost like an insurance business. You keep earning a small premium/brokerage, but every once in a while, there is an incident when the customer is out of money, and the broker will have to fund it from their own pockets. For example, in April 2020, when Crude oil went negative, no risk management system could have helped us ensure customers don’t lose more than the margins they have. We lost over Rs 30 crores that day; essentially, the client debts were over and above the margin. We could make good of Rs 30 crores and survive because we were earning as a business. As more leveraged customers increase, the higher the risk for the business. The issue with not earning enough as the business grows is that one incident is enough to bring you down, and if a broker goes down, he takes all other customers down along with them as well.

So I don’t think a flat fee per month or zero brokerage is a viable business model. Eventually, one incident is all it takes to be out of money as a business. Imagine an insurance business insuring everyone at really or no premium; what do you think will happen the day there are a lot of claims?

But all said, I might be conflicted as the CEO of Zerodha with a different pricing model. Do take everything I said with a pinch of salt.

Sir than you very much for taking time and replying.

I am extremely sorry to disturbed you. I will just ask 1 last question.

How much did zerodha lose in EQUITY and F&O segment during 2020. MCX works in a different way when compared to NSE and BSE. What if a zero brokerage company is giving leverage only in equity and F&O and not in MCX?

Does it effect zerodha in any way if a better broker offers brokerage of 10rs. I mean are the clients rational enough to leave zerodha for 10rs.

Last is ok zerodha survives for another 10yrs or 20yrs. What is the growth prospects? will discount brokerage industry grow ? If the total profit of discount brokerage today is around X where do you see this in next 5yrs assuming there is no market crash and capital markets are growing in high single digit

Thankyou very much. Have a nice day.

I would also like to ask a question out of curiosity you may not answer this. Is it really NITHIN Kamath replying me?

Losses typically happen when the margins available aren’t sufficient to cover losses. Since in equity, there hasn’t been a large move, and there haven’t been any losses recently. Every time there is a stock in F&O that suddenly moves up or down more than 25%, can cause losses as well. But back in 2008, there were two days when markets moved more than 20% and caused many brokers who weren’t capitalized enough for the size of their business to disappear.

There have been many competitors who have offered at lesser and continue to do so. I guess we have to stick by our guns and not get swayed into matching every competitor in pricing. In any case, Rs 10 or Rs 20 isn’t going to make a big difference. The business today is of product and not pricing.

If you track me on social media, I have generally been pessimistic about how much can the business grow from here.

But sir being a CEO of India’s largest broking firm, how do you manage to get time for this? I’ve never seen any CEO of a big firm talking directly to his customers

I think everyone has time; different people prioritize different things with their time. I give myself 2 hours of personal time daily (health, fitness, music, sports, podcasts, reading, etc.), another 1 hour for family, and am disconnected from all electronic stuff for 8 to 9 hours (including sleep time). We stop all work-related chats mandatorily by 6 pm and no work chats on weekends, so everyone in the office also has personal time. We have done quite okay as a business, and I don’t think anyone feels burnt out as well.

I think life is a marathon and not a 100m dash, so conserving energy and having a balanced life is the key to doing well. Hence, I also think working hard all the time is overrated.

But generally, some things that have helped us significantly to stay efficient at Zerodha are having a flat hierarchy and not having meetings unless required. We are also in no hurry to grow fast and are not trying to build too many new businesses. We have also kept an extremely complex business simple by offering one deal to our customers and then transparently talking about all aspects, which helps our team and the customers better understand all aspects of the business.

@nithin

I went a little bit deep and observed that equity is less volatile and is being managed in less riskier way than MCX. Referring from your previous post you have till date not experienced any loss from equity segment and last time was back in 2008. You also said that if brokers who are not enough capitalized will have to leave this business.

Since the risk management in equity is way better comparatively to MCX and exchanges being very much capitalized cant SEBI start direct trading only for the equity segment assuming that they figure out the technology for transfer and all the operational problems. Exchanges an implement even better risk management strategy and they are ready to take a hit once in 15yrs because the possibility to loose money in equity is extremely low.

F&O is only for specific stock and they can do better risk management with upper and lower circuit. They can little bit increase the margin requirement.

Plz share your view that direct trading only in equity segment where probability of loss is low and exchanges are well capitalized to take a shock one in 10 or 15yrs assuming they crack the technology for transfer. How do you see your business in this case

Yesterday GBPINR fell 4.5% at market opening, the margin required was 3.5%, we had bad customer accounts going into debit of almost Rs 1 crore. There was nothing our risk management software could do as the move happened overnight. Similarly, in equities also there have been many individual stocks that have fallen or gone up more than the SPAN margin requirements overnight or suddenly and created debits to the brokerage firms.

Yes, equity indices have probably been the safest in terms of volatility as compared to margin charged, but again you never know what is around the corner. Global war and we might see markets opening down 20% the next day.

As a broker, I think the most important aspect is to be well prepared for a day like that when shit hits the fan. Being well prepared is being sufficiently capitalized, which means the business has to generate enough profits and hence increase the networth, as the business scales in terms of customers and increasing risk.

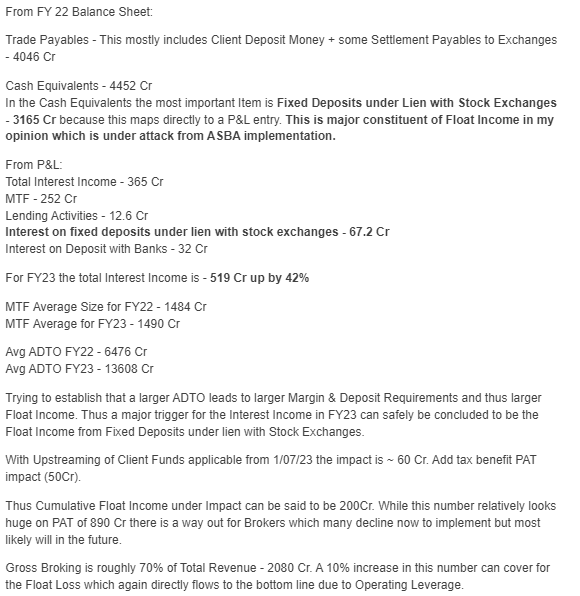

Hi @nithin SIr just wanted to ask a follow up on ASBA. You said it would not have a big impact but recently I came across a wonderful analysis on how angel one will loose a FLOAT INCOME of 200cr and their PAT is 900cr. He also makes a point that the gross brokerage is 2000cr from them which is 70% of revenue and if they increase that by 10% they can make it for the loss.

Not just float income, but not being in control of the funds also means more risk. The business of broking is like running an insurance business, you make small amounts of premium, but every once in a while, there can be a black swan when you give back. So logically, pricing will have to go up, especially given that the funding bull market in the startup world has ended.

We already have an NBFC where we do loans against securities.

We don’t promote it because an investment app shouldn’t encourage customers to borrow. Philosophically it doesn’t align. But we had to offer this because our customers would use other NBFCs to borrow against securities. So we built it without any of those crazy penalties or processing charges.

We’d love to build a bank which doesn’t lend, puts all customer funds in Gsecs (no risk), and offer a simple and spam-free user experience. Unfortunately getting a banking license is really really really hard.

Unfortunately, nothing is available, and new licenses RBI has stopped giving to payments bank as it has generally been an initiative that hasn’t worked very well. Very few people want to do banking without lending. Everyone who got the license got it thinking they could become a universal bank at some point. Today everyone with those ambitions takes a Small finance bank license and not Payments bank. But SFB isn’t something that we’d want to be as we have no lending ambitions.

@nithin, I have been using Zerodha for the last 5 years. I must have paid almost 15-20 Lac as brokerage to Zerodha. One issue I consistently faced with Zerodha is “Getting a copy-paste reply or an unrelated reply,” even when I escalate any issue, the issue gets marked duplicate.

I do not know how else to reach you to make sure you know about this issue. I already tried reaching you on X, email, but never got an acknowledgement.

I hope I get a reply this time.