Welcome to The Long and the Short—a show where you can expect an honest take on trading, something you won’t hear elsewhere. I am Sandeep Rao.

In our last newsletter, we explored whether one should trade penny options and the pros and cons of it. Today, I want to stick to options, index options particularly, and talk about a fascinating way of using options to limit drawdowns and participate in the upside of an index like Nifty.

Such strategies are packaged as Structured Products or MLDs (Market-Linked Debentures) and sold by wealth management firms to HNIs. Today, I will teach you a DIY way of doing it.

Fair warning: As interesting as this episode is going to be, it would also need a fair bit of your attention to make sense of what I explain. Plus some bit of understanding of how options work. So get your coffee, I have got mine, and let’s get started.

The Concept of Optionality

By now, many of you would know I am a fan of Taleb. If you haven’t yet read the book Antifragile, maybe you should.

The reason I am bringing up Taleb again in this episode is because of the idea of Optionality that is central to the book Antifragile, and equally foundational to the strategy that we will discuss today.

What Exactly is Optionality?

In textbook terms, Optionality as Taleb defines is similar to an option—a right but not an obligation. The defining mathematical property of an option is that it is a nonlinear way to be exposed to a source of variation.

In simple words, you pay a small price (the premium) to participate in the upside, but on the downside, your loss is capped at that small price. It offers what is known as “Non-linear” exposure. Heads I win, tails I don’t lose much.

This idea is at the heart of what we will discuss today in our Limited Downside Nifty Strategy.

But before we go into the strategy, we would need to understand some definitions, context, historical, and product-specific stuff. Let’s start.

What Are Structured Products and MLDs?

First things first—what exactly is a structured product or an MLD (market-linked debenture)?

Market-Linked Debentures (MLDs) are hybrid financial products sold primarily to India’s High-Net-Worth Individuals (HNIs). They are designed to give investors better returns than fixed deposits by adding a chance for stock market returns, while also offering protection against losses.

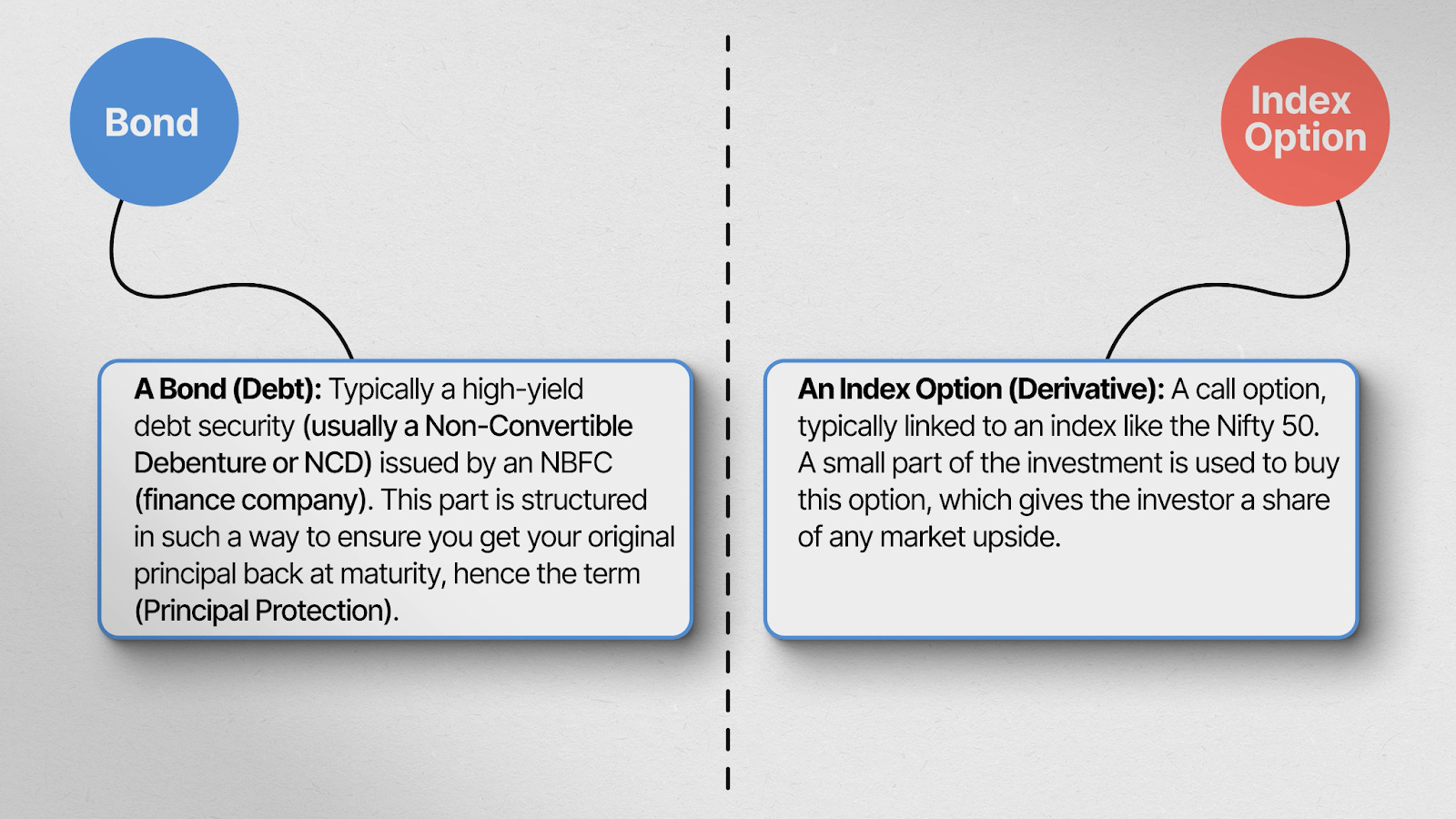

The Two Components

An MLD is simply a combination of two things:

- First, A Bond (Debt): Typically, a high-yield debt security (usually a Non-Convertible Debenture or NCD) issued by an NBFC (finance company). This part is structured in such a way to ensure you get your original principal back at maturity, hence the term “Principal Protection.”

- Second, An Index Option (Derivative): A call option, typically linked to an index like the Nifty 50. A small part of the investment is used to buy this option, which gives the investor a share of any market upside.

In short:

- If the market rises, you get your principal back as the bond’s minimum interest covers it, plus you get the upside from the option

- If the market falls, you still get your principal back, which includes the bond’s minimum interest, and nothing from the call option, as it simply expires worthless

Example Structure

A typical MLD would look like this:

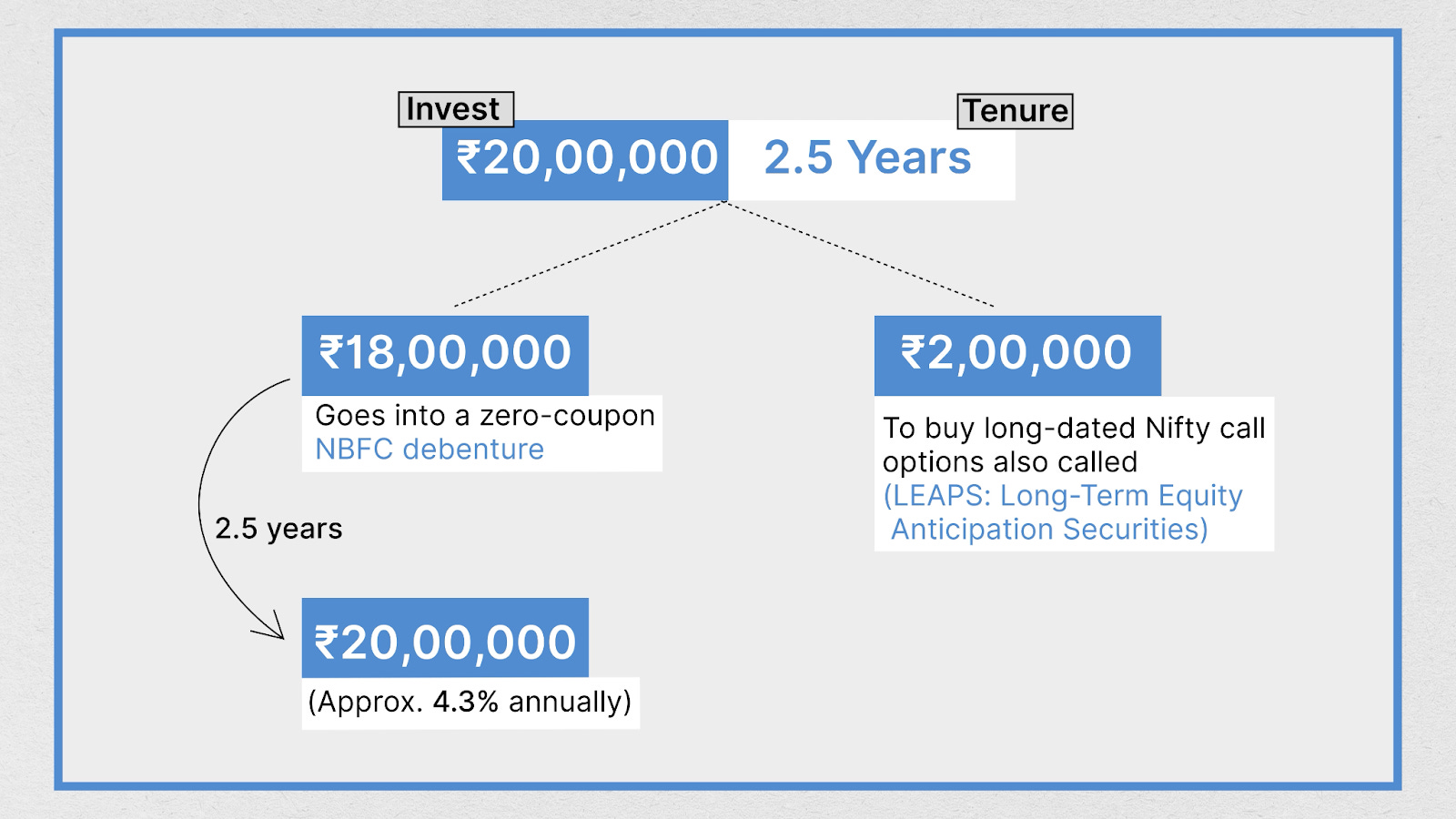

You invest ₹20 lakh for about 2.5 years:

- About 90% of it (₹18 lakh) goes into a zero-coupon NBFC debenture. It pays no periodic interest. ₹18 lakh grows to ₹20 lakh in 2.5 years (approx. 4.3% annually). This ensures full principal protection at maturity.

- The remaining ₹2 lakh is used to buy long-dated Nifty call options, also called LEAPS (Long-Term Equity Anticipation Securities). This portion provides market-linked upside.

Typical Payoff Structure

Typical upside structure that an MLD would promise: about 1.5× Nifty returns, up to a cap.

Scenario outcomes:

- If Nifty rises 20%: You get roughly 30% on the total investment → about ₹26 lakh

- If Nifty rises strongly (e.g., 35%): Return is capped around 33% → about ₹26.6 lakh

- If Nifty falls: Option value becomes zero → you still receive ₹20 lakh

In short: A structured product or an MLD is a bond layered with a derivative. While the bond would have credit risk, it does not have market risk, and the call option offers participation on the upside.

History of Structured Products & MLDs in India

MLDs first appeared around 2006-2007 and grew in popularity, especially after the 2008 global financial crisis, as investors sought safety with some upside.

RBI’s Concerns and Restrictions

But the Reserve Bank of India (RBI), the banking regulator, grew concerned about the complexity and risk associated with structured derivatives. They were particularly worried about:

- Mis-selling: Retail investors might not fully understand these complex products

- Systemic Risk: Widespread offering of complex derivatives could pose a risk to the banking system

In 2008, the RBI restricted domestic banks from offering complex structured derivative products to retail investors. This effectively forced banks out of the business of widely distributing these notes domestically.

The NBFC Route

Since the RBI restricted banks, issuers had to find another legal channel. They found it in Non-Banking Financial Companies (NBFCs). NBFCs (which are regulated by RBI but under a different set of rules than banks) became the primary issuers of the debt portion of these products.

Wealth management firms often set up their own NBFC subsidiaries to issue these Market-Linked Debentures (MLDs), allowing the business to continue outside the banking system’s stricter derivative restrictions.

SEBI Guidelines

With the increasing popularity of these products, SEBI stepped in. In 2011, SEBI announced Guidelines for Issue and Listing of Structured Products/Market-Linked Debentures. It also set a minimum net worth requirement (₹100+ crore) for MLD issuers and mandated strict disclosure norms (e.g., scenario analysis, credit risk warning, etc.).

In Jan 2023, SEBI reduced the minimum face value of privately placed debt securities (including MLDs) from ₹10 Lakh to ₹1 Lakh to allow for wider participation.

Tax Change (2023)

But the biggest impact came in April 2023 when the Government of India changed the taxation status of MLDs. Gains are now taxed as Short-Term Capital Gains (STCG), regardless of holding period. This change significantly reduced the appeal of MLDs for high-net-worth investors, as the favorable Long-Term Capital Gains (LTCG) tax arbitrage was removed.

Today

Today, these products remain niche HNI tools used for capital protection + tactical equity exposure, though volumes have moderated post-tax change. Their future will depend on whether investors still value the asymmetric risk-return profile now that the tax arbitrage is gone.

Creating a DIY Structured Product

With the basics sorted, let’s now look at how to create a Structured Product the DIY way.

Disclaimers

First things first, disclaimers. The mutual funds and index options referred to in the examples are only for illustrative purposes, and this is not a recommendation to invest in any of these products, including the index calls.

Capital Required

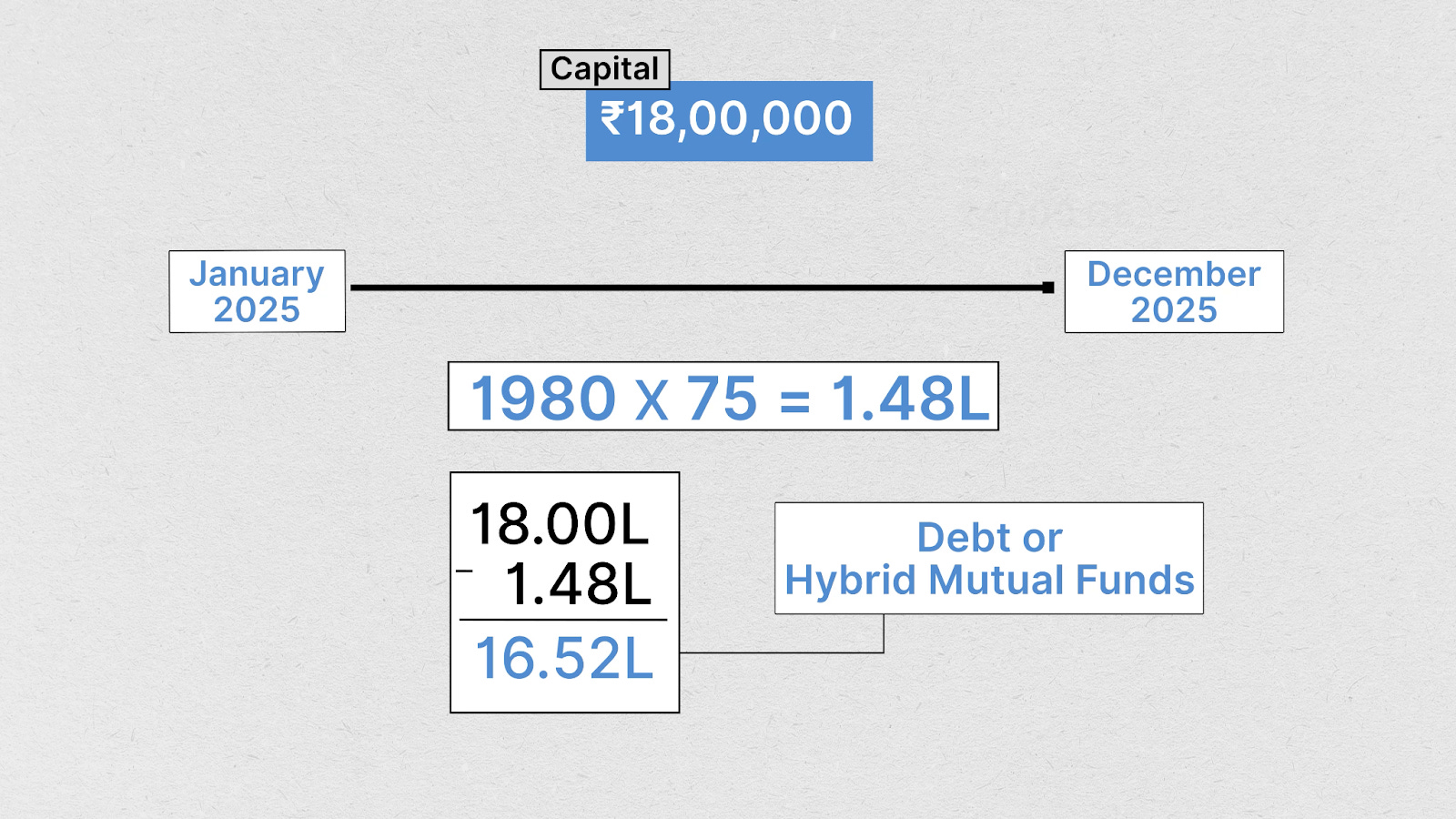

In our illustration, the minimum capital required would be equal to the notional or contract value of Nifty at the time of initiation of the structure.

For example, if you were to start the structure in Jan 2025, you would need a capital of approximately ₹18L (24,000 × 75 lot size).

Debt Component Options

For the debt component of the structure, I would share three options with you:

- A simple Liquid fund

- A Gilt fund

- A more riskier Hybrid fund

Unlike an MLD, where the debt component can be quite opaque, here you have full control over where you would want to invest.

Example Structure

Back to the example of the ₹18L:

The first thing you would need to do is buy a long-dated Nifty Call option. Say in January 2025, the 24000 Nifty Call expiring in December 2025 would have cost you ₹1980 × 75 = ₹1.48L. The balance of ₹16.52 lakhs would need to be invested in any of the Debt or Hybrid Mutual Funds that we choose.

Also, to fully cover the cost of funding the Nifty call through the base investment, you may need approximately 9% yield. In which case, your downside risk at the end of the year becomes zero. However, it’s hard to find a safe and liquid pure debt product that would yield 9+%.

Let’s assume you get a yield of 6%, in which case your max drawdown is 3%. Upside would depend on the index move. If the index closes above 24,000 plus the amount paid for the CE option by the end of December, you would be positive on the Index Call Option.

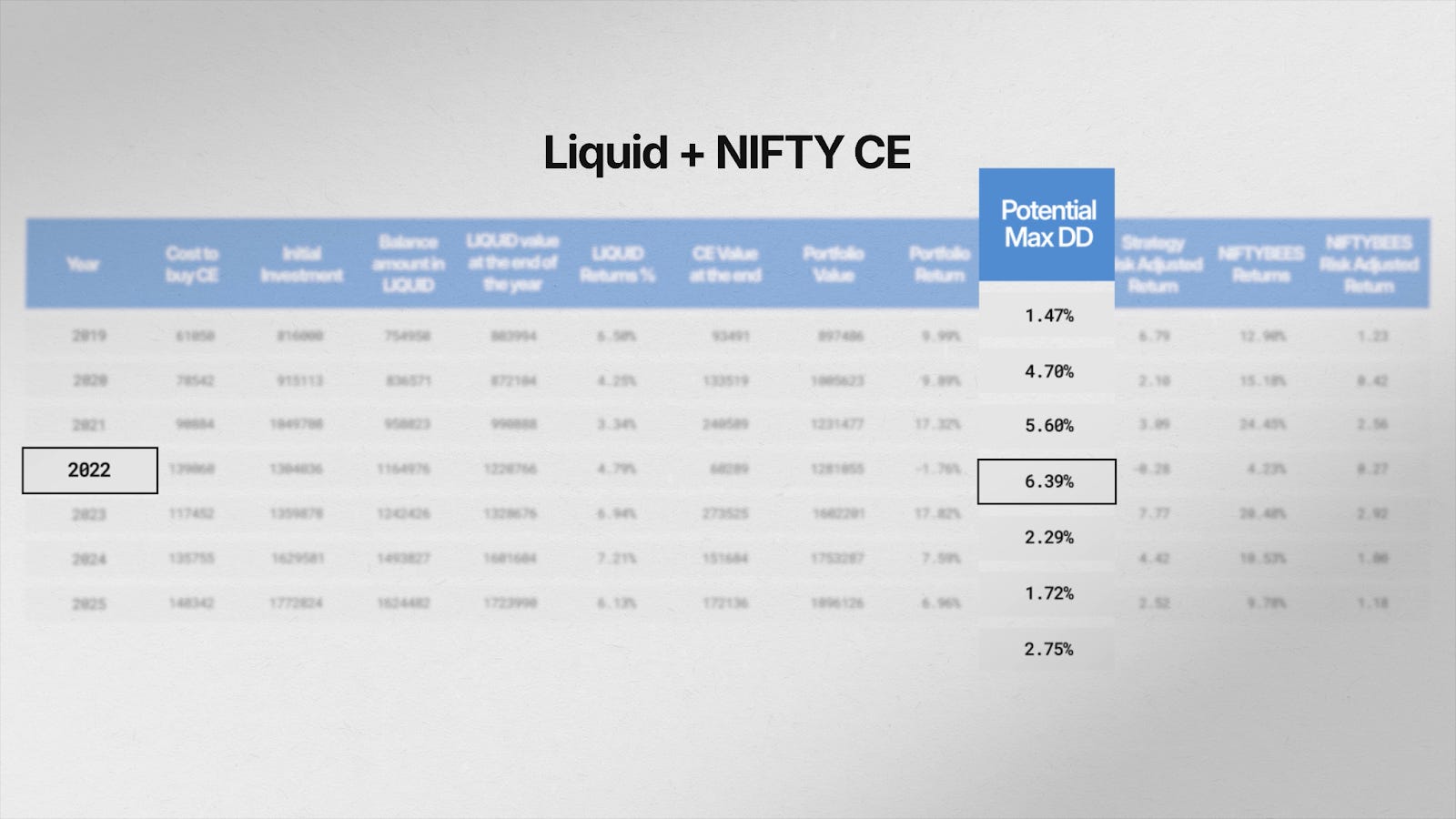

Backtest Results (2019-2025)

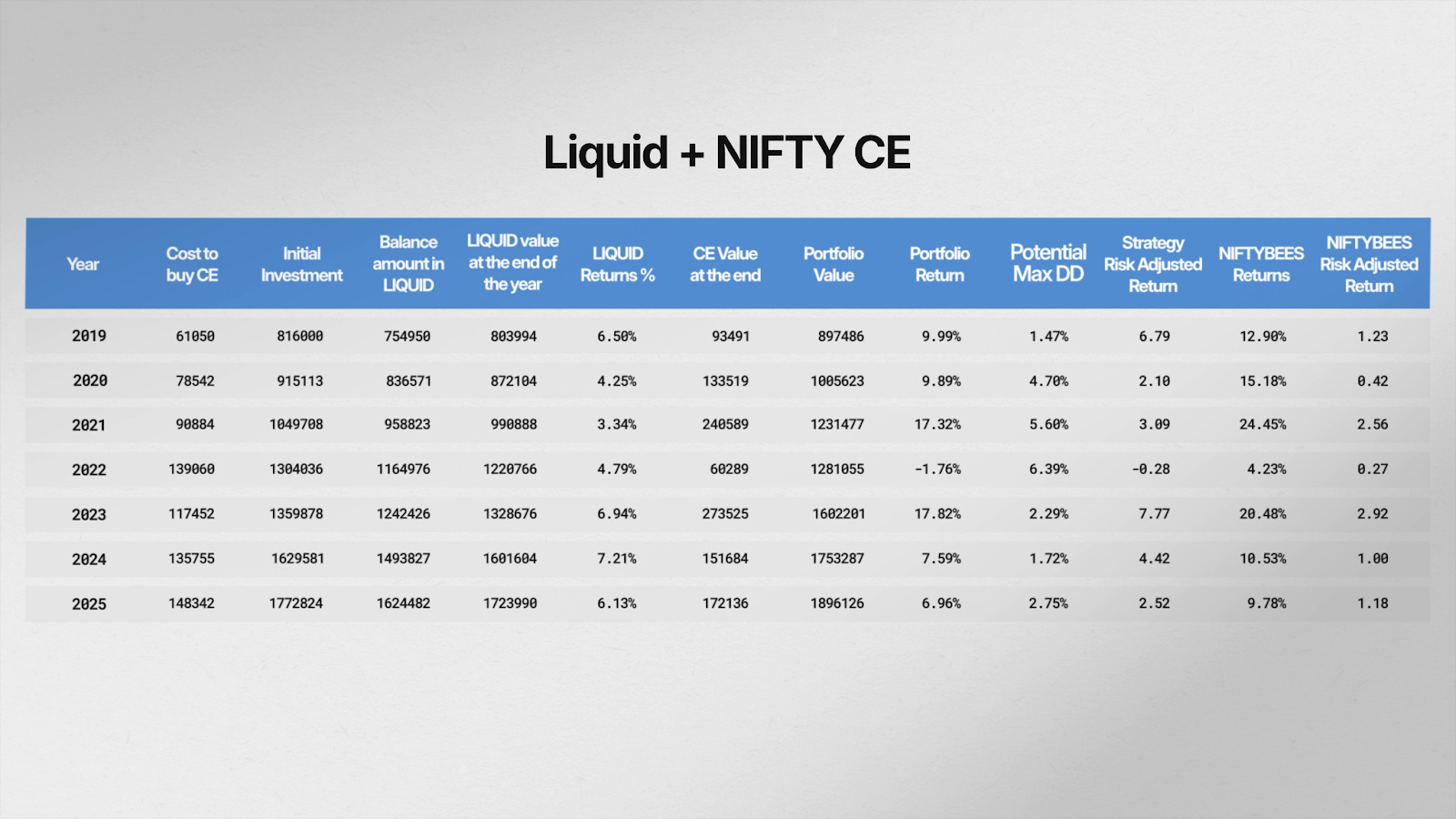

Let’s look at how the strategy would have fared had we used Liquid Fund as the base since 2019.

Backtest Rules

Here are the rules that I used for the backtest:

- We invest on the first trading day of each calendar year; calculate returns up to the December CE expiry (last Thursday/Tuesday)

- Initial investment = NIFTY Spot open on day 1 × lot size (75)

- On day 1, we buy ATM December CE; strike rounded to nearest 1,000 due to liquidity

- Remaining capital (initial value − CE cost) is invested at day-1 closing NAV into: (a) Liquid Fund, (b) Gilt Fund, or (c) Conservative Hybrid Fund

- On December CE expiry, record fund values based on NAV

- Total portfolio value = CE payoff + final fund value for each scenario

- Max Potential DD for all three scenarios = CE premium (CE can expire worthless) - returns from Liquid/Gilt/Hybrid funds; their individual drawdowns are ignored in this working

- For NIFTYBEES comparison, we use the closing price on entry and exit dates

- NIFTYBEES max DD is calculated using daily closing prices

Key Observations

In absolute terms, this strategy will underperform Nifty sometimes, but that’s not the reason you should choose it. Instead, look at the risk-adjusted returns—you take very little risk and yet participate in the upside of the index.

Look at the potential max drawdown value. It went at max to 6.4% in 2022. It fully depends on the cost of the call option and the expected yield from the mutual fund investment. There will be some cases, especially with Gilt funds and hybrid funds, which will fully cover the cost of the call options.

Now look at the Risk Adjusted Returns columns—you can see for yourself the impact of having debt as the base. You are taking very little risk and still participating in the upside.

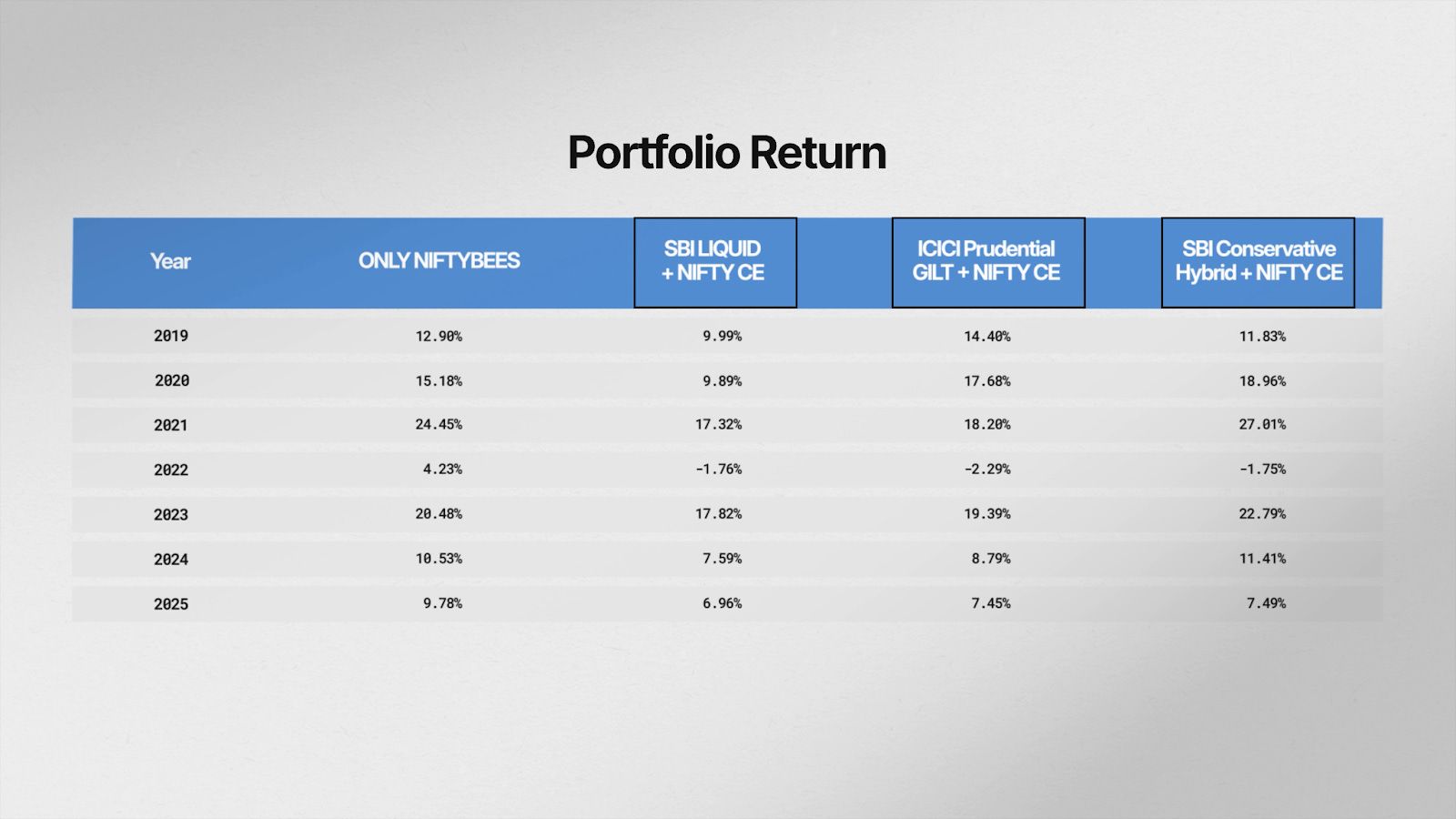

Different Fund Comparisons

Now Liquid fund is just one way to do it. You can always choose a Gilt Fund or a Hybrid Fund as well. While it will alter the return profile, it still gives you a choice to aim for better returns.

In this table, I have taken SBI Liquid Fund, ICICI Prudential Gilt Fund, and SBI Conservative Hybrid Fund as examples. Here’s a comparison across different mutual fund products using the same structure:

- 2019: While NIFTYBEES gave 12.9%, Gilt + Nifty Call combination outperformed at 14.40%, whereas Liquid fund + NIFTY Call Option gave about 9.99%—not bad for the low risk

- 2022: Was bad across all structures

- 2025: While in absolute terms all combinations underperformed, but if you look at it from a risk-adjusted perspective, the portfolio would look super stable

As I have mentioned earlier, the key here is not absolute returns; the key here is how risk-managed the structure is. The loss of returns is the price you pay for peaceful sleep.

Pros and Cons

Now obviously all is not hunky dory, be it with a DIY Structure or with an MLD. There are pros and cons of each, and here is what you need to know.

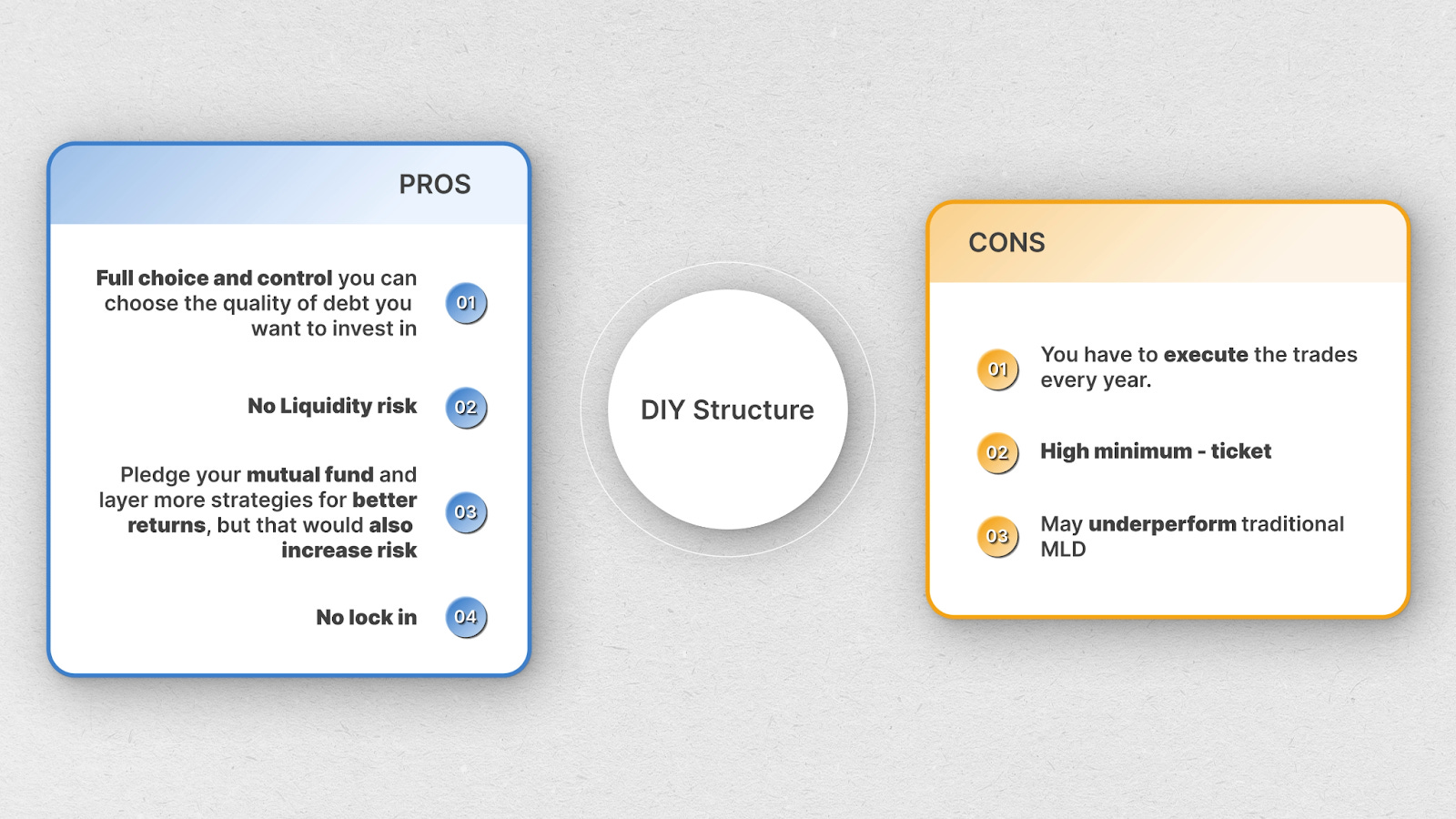

Pros of DIY Structure

- Full choice and control—you can choose the quality of debt you want to invest in

- No liquidity risk

- You can, if you wish, pledge your mutual fund and layer more strategies for better returns (but yes, that would also increase risk)

- No lock-in

Cons of DIY Structure

- You have to execute the trades every year

- High minimum ticket

- May underperform traditional MLD

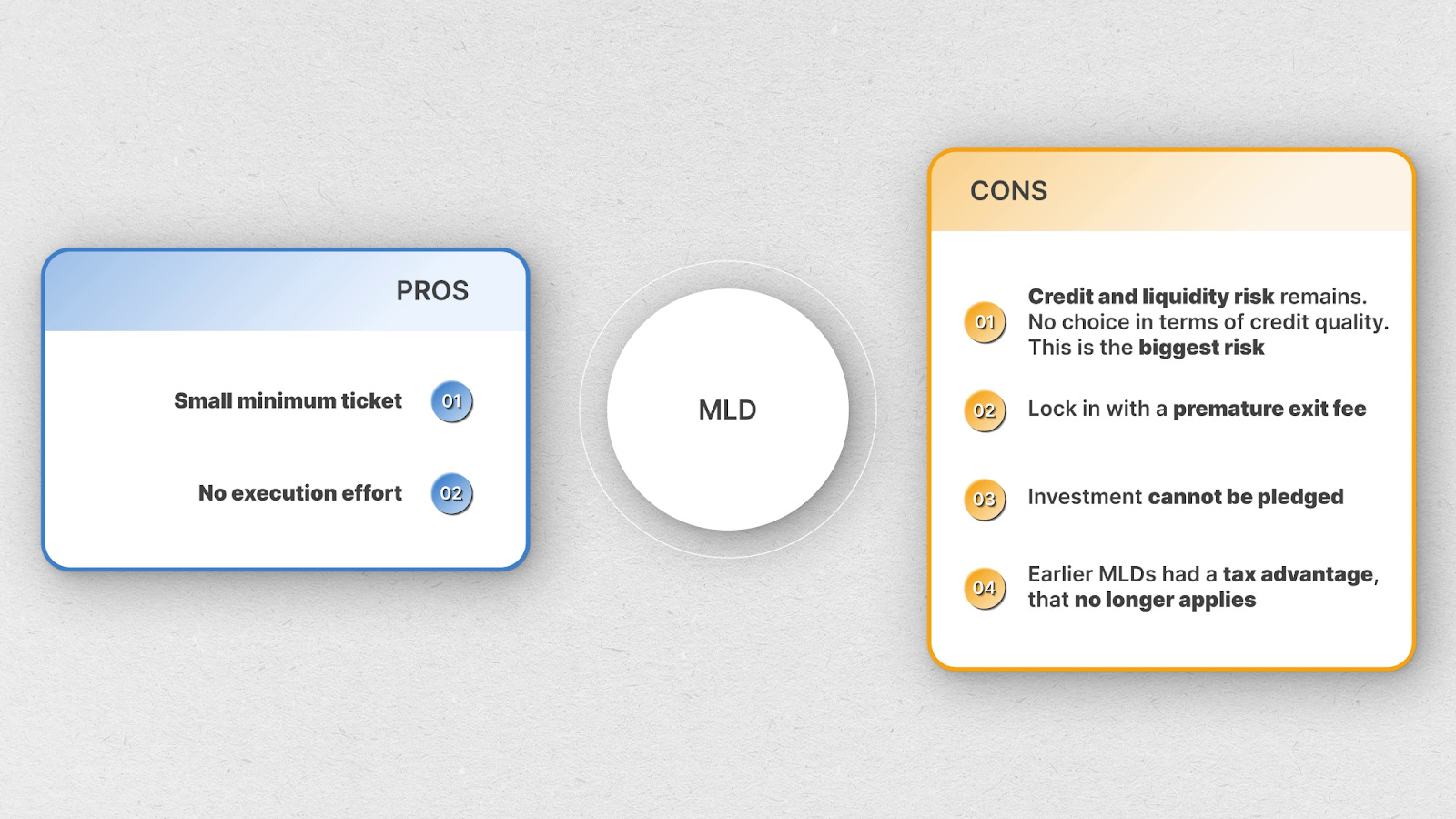

Pros of MLD

- Small minimum ticket

- No execution effort

Cons of MLD

- Credit and liquidity risk remains—no choice in terms of credit quality. This is the biggest risk

- Lock-in with a premature exit fee

- Investment cannot be pledged

- While earlier MLDs had a tax advantage, that no longer applies

Advanced Strategies

In summary, if you are an active investor and would like to geek out on structuring portfolios, the ideas shared in this video are a good starting point.

Once you understand this dual-layered design, you can now play with both the components:

- You can choose to go OTM with Calls to reduce the cost basis

- You can also choose to create other option spreads depending on your reading of the markets

- Sometimes you can choose to time your call buy based on a specific market reference, say you would buy the call only if markets correct 10%

- Likewise, as we had shown, you can also play around with the underlying by investing in different categories of funds. You can fine-tune the risk-return profile of the larger portfolio

The possibilities are many, with your imagination being the only limiting factor. If you have more such ideas, do share them in the comments.

So that brings us to the end of this deep dive on DIY Structured products and MLDs. I hope you found this newsletter valuable.

Do share your questions, thoughts, and feedback in the comments—I’ll do my best to respond.

Thank you for reading, and see you in the next one.