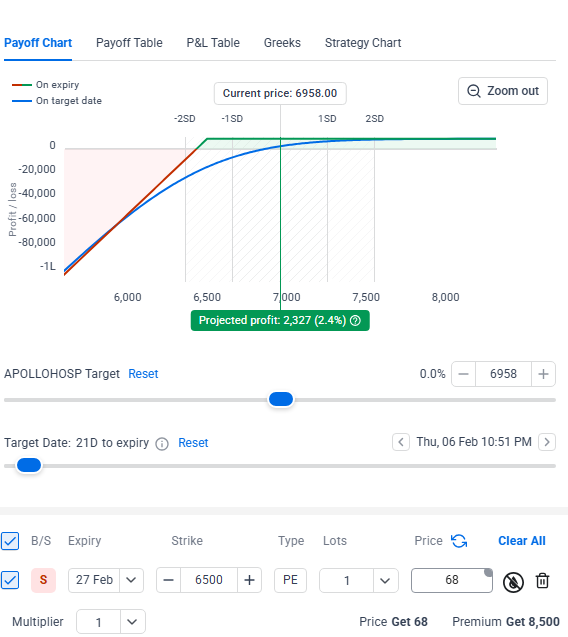

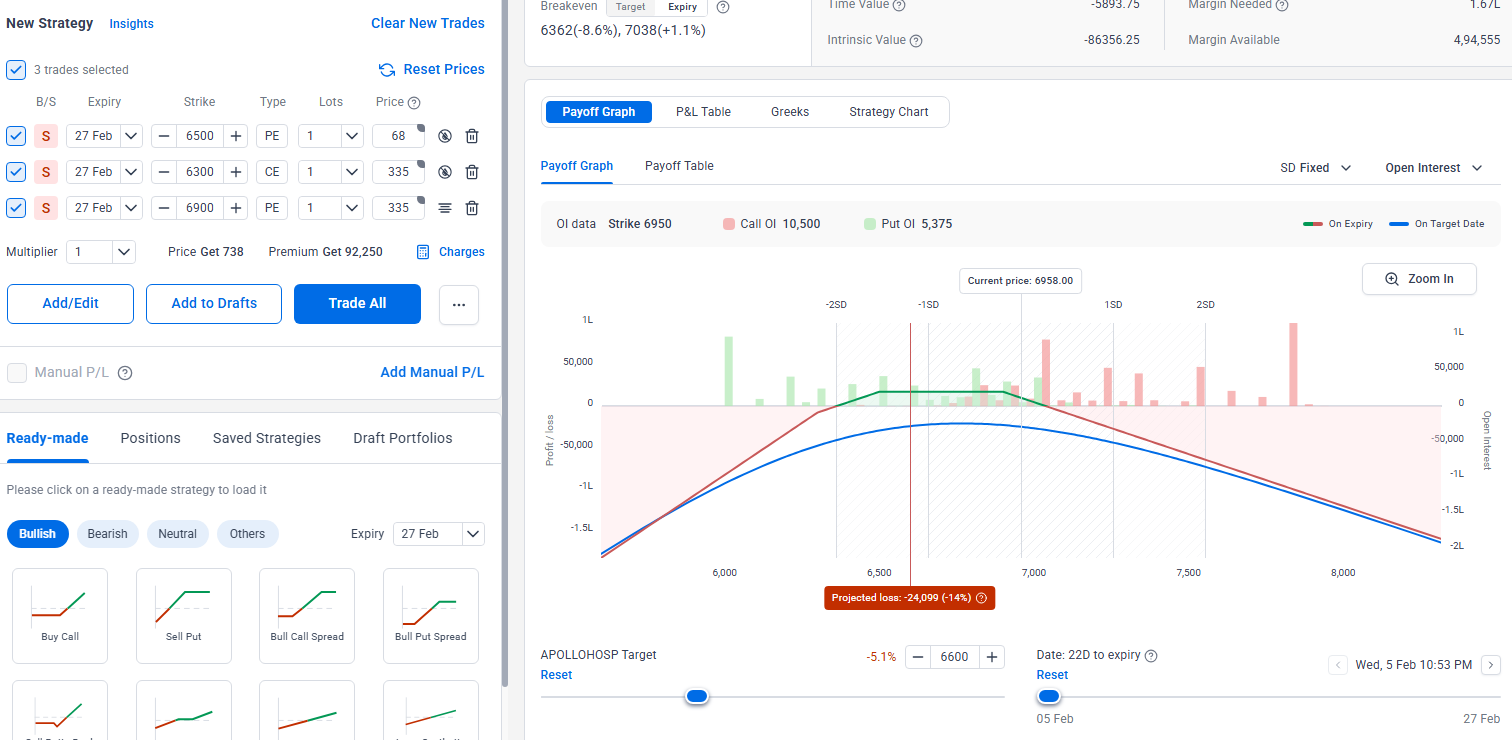

Let’s say I sold a put on Apollo Hospitals with strike 6,500 when the spot price was 6,800. The premium received was 68.

The spot price has now moved to 6,600 and I think it MIGHT move further down. I want to cover my risk for a range around the 6,600 spot price, instead of rolling the strike or in time.

In that case, would doing the following make sense:

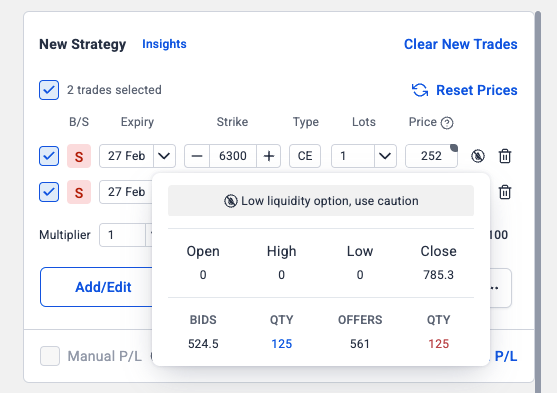

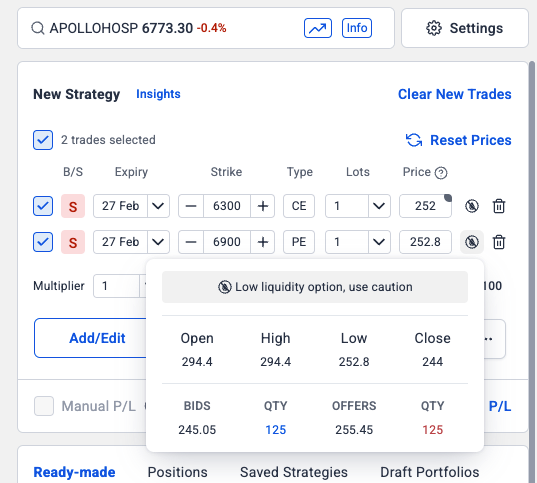

I sell an in the money call with a strike price of 6,300 for a premium of 335.

I sell an in the money put with a strike price of 6,900 for a premium of 335.

It makes theoretical sense because if Apollo expires between above 6,300 and below 6,900, I should come out with a profit. Am I thinking in the right direction? What are the pitfalls of this apart from larger downside beyond the selected ITM strikes and higher margins?

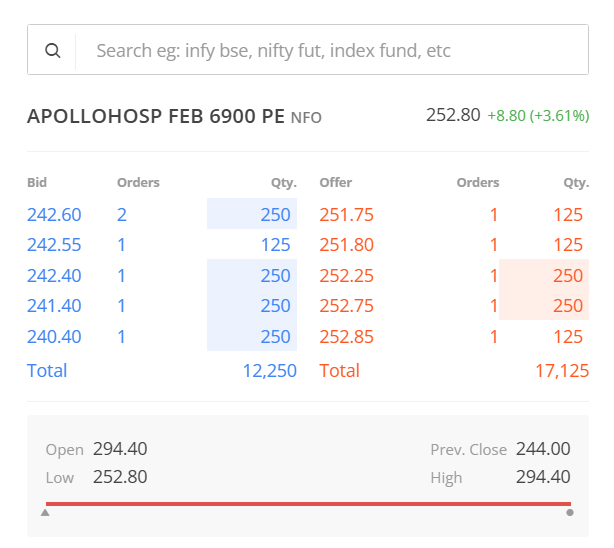

You’re correct. But I’d be entering those ITM positions 300 points away (when price moves to 6,600) so I think liquidity should emerge. Even currently I’m getting over 100 in time value for this ITM option:

Nevertheless, I used Apollo as an example, but I think this should work on more liquid underlyings like Nifty or even Reliance at times.

The part I need help understanding is what should I keep in mind when executing this (except for liquidity in case of stock options like you mentioned).

You are selling ITM call and ITM put. Instead just sell OTM call and OTM put. Your payoff is exactly the same. Unlimited loss outside 6300 and 6900. You are only paying higher charges because of higher premium. Makes no sense to me.

But doesn’t make sense. Simple thing is complicated by going for ITM strikes. More charges. Less liquidity.

I’d always OTM strikes of course. I was just re-evaluating my firefighting methods should things go south and this just randomly popped into my head. I know it’s not the most optimal way, and that’s why I created this post.

Liquidity is a real problem, yes. For now, I’ll continue rolling over because I don’t feel too confident about this. But this looked OK on the payoff chart (provided there’s enough directional conviction).

It will give the exact same pay off as selling OTMs. If there was some difference, it was because of liquidity. You can check with nifty contracts. Take the ITM strikes that you want and change them to OTM by changing call to put. You will get same pay off to last rupee.

Let’s say 10 days later, the spot price is 6,600. There’s usually enough liquidity ITM roughly 4-5% in APOLLOHOSP (and most underlyings I believe). So I sell ITM 6,300 CE and 6,900 PE. I’ve assumed the price of these options to be the intrinsic value (300) plus Rs. 35 (time value - this is assumed and ofcourse can differ based on DTE).

Assuming everything goes well (the price remains between my breakeven points), I can buy back ITM strikes for its then intrinsic value and profit from the theta earned so far.

It’s definitely an overcomplication, and rolling is definitely simpler. I’m just exploring the viability of something like this in a very specific scenario such as the stock going below my sold strike closer to expiry and me needing some range bound protection on both sides. The margin requirement would also be colossal on this, but I’m focused on preserving that cash flow and generally have that capital available closer to expiry.

Instead of this just sell 6300pe and 6900ce. It will give you same 35 points without any intrinsic value.

Pay off will be same. Risk will be same. Charges will be less. Liquidity will be better.