If you go through circular what NSE has put, it says SPAN files will be updated only from Sep 21st. So all the calculators will get updated only by then. Until then, the math to remember is - around 6% more margin than current for index and 10% for Stocks.

1 Like

@nithin

As per my understanding, physical delivery is not compulsory up to 3 CTM long options; will this additional margin is also required for these 3 CTM options from t-4 days ??

Struggling to understand (and am not interested) in the theory/math and just want to know how this is going to affect me when I trade intraday. Currently I assume the margin requirement for bnf is 8%. Read @nithin saying assume 6% extra margin for index so that means a total of 14%? So at current rate the margin (SPAN+Exposure) would be 1.5 lakhs and for intraday at 40% would be almost 61k…ie double of what we are paying now?

1 Like

Ah my bad if I wasn’t clear, 6% additional to the current margin. So if margin now is 70k, it will be 6% more or around Rs 4200 extra. But by november it will be overall around 25% more than current margin. So around 17.5k more.

1 Like

Where can I see the physical deliver of options stocks

Check this doc, has updated list of all stocks whose F&O contracts which are physically delivered on expiry.

@nithin

Why is the retail trader taking all the crap from SEBI and NSE? why dont all the brokers goto court and put a stay order on this useless increase of margin from SEBI? A better way to protect innocent and new traders is through education and make it mandatory to pass some minimum test in order to qualify to trade derivatives not by increasing the margin which kills the market.

Here both the brokers and the traders are at a huge loss due to loss of liquidity and many would leave trading due to less ROI. markets are known for high ROI because they have high risk.

@nithin

You guys at brokers have the ability to go against this and take SEBI to court otherwise SEBI has no resistance. Simply killing the free market due to excessive regulation.

4 Likes

hmm… for a market like ours where - currency can do the jig the way it did, and where corporate governance or default issues keep coming up - is 8% on index and 12.5% on stock derivatives enough to cover for a one day risk (intraday or overnight). I don’t know. 8% going to 10% or 12.5% going to 17.5% may not necessarily be that bad in the long run. Yes of course it affects in the short run, more for us as a retail brokerage firm than anyone else.

Below is an email that I had sent to the broker associations to maybe push for one big change - which they are already working on.

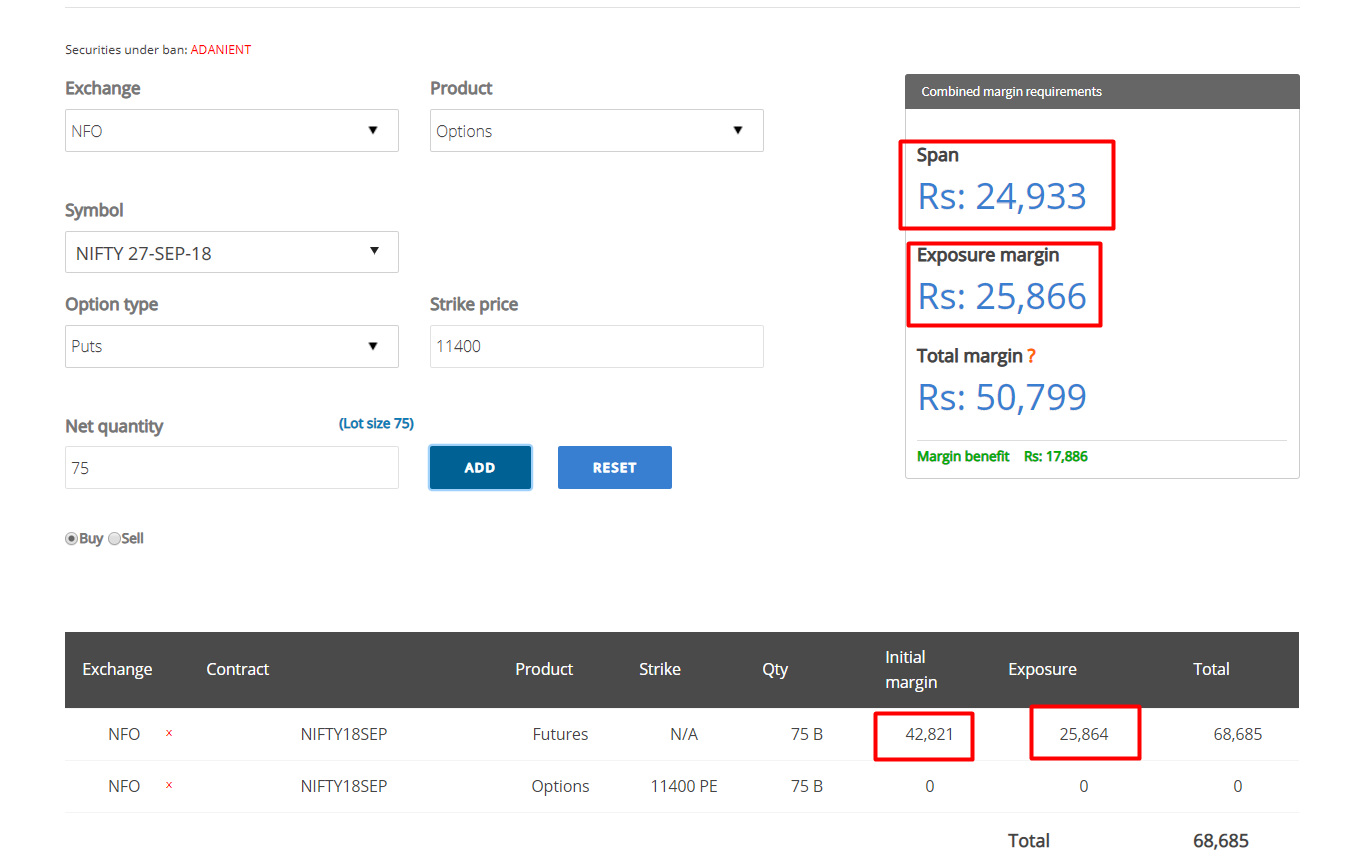

On the group it was indicated that there is a possibility to push for incorporating all margins within SPAN, instead of having SPAN and Exposure separately.

Considering that the recent circular to increase exposure margin (ASM adding to Exposure) was amended to incorporate that same change within SPAN, I am guessing it will be the right time to request for that change as they would have analysed the impact of increase in Exposure vs increase in SPAN.Today, the way SPAN and Exposure is blocked, the incentive isn’t as much for a person who trades strategies, hedges, arbitrage’s etc. If the exposure was to be included as SPAN itself, the benefit of taking any of the above strategies will actually show up in the margins a lot more.

Take this below strategy for example, Long futures + Long puts. Even though SPAN dropped from 42k to 24k because the position is hedged, the Exposure margin remained the same at 25k. If this wasn’t a separate exposure margin, but was included within SPAN, this Exposure would have also dropped to around 13k. So this entire strategy at 38k vs 50k.

One of the reason why regulator is so focused on derivatives segment is because of huge amount of trades (trading turnover) vs open interest and high derivatives turnover vs cash market turnover. If margins encouraged people to trade more strategies vs just trading naked, automatically people will hold positions for longer and hence reduce trading turnover and also increase the open interest. The bonus is that trading strategies is generally lot more safer than trading naked.

Hopefully this makes sense.

4 Likes

Man, I feel you. That’s why I created ARTI which stands for ASSOCIATION OF RETAIL TRADERS OF INDIA. Come, join. Let’s share our sorrows and possibly go to court against this. I will PM you the link to join. Peace.

2 Likes

@nithin;

India is matured economy; currency has depreciated due to widening CAD and price of crude which has risen. Any market can break 10%. Even the US market dropped 40% in a matter of days in the huge crash 1987.

You cant start wearing an armoured suit just becuase you know one day you will die. We are know we will die dont we, but we dont stop living.

That doesnt mean you start increasing margin for this one isolated event that comes once in a decade or even a generation. And if doesnt cause huge losses so be it. I think SEBI lacks maturity and they are becoming protectionist.

The reason of excessive derivative turnover is SEBI dosent allow short selling in cash/equity market. So there is no choice but to look at derivatives if you wanna go short. The whole idea of free market is let the market decide and not SEBI try to control it.

The idea of merging SPAN and exposure is good but it is still not good enough.

Worldwide most markets only SPAN is levied on derivatives thats the whole idea of having derivatives in the first place. Here SEBI has not only increased SPAN to crazy values but also continues with exposure margin. Exposure Margin shouldn’t be mandatory; it should be left upto the discretion of broker and clients. Only Span should be collected by exchange.

@nithin

You have an excellent platform in Zerodha. Highly commendable job! As a vanilla retailer my voices cant be heard in SEBI or the exchanges. But it is our earnest request to take this matter in court if SEBI is not yielding and we all will contribute valid points which our case stronger. SEBI is relying on committee reports in which we have no representation. Like for FPI there is strong lobby to take up their case. But for us; we rely on brokers to make our pitch.

4 Likes

…As the number of brokers increased, they had to shift from place to place, but they always overflowed to the streets. At last, in 1874, the brokers found a permanent place, and one that they could, quite literally, call their own.

Source: https://www.bseindia.com/static/about/heritage.aspx?expandable=0

Small retailers become tenant in her/his own house…

Source: Fearless Girl - Wikipedia

1 Like

This guy actually has brains. Kudos, fam.

1 Like

@nithin Yes, having only SPAN is a nice idea suggested by you. Also margin can be reduced by calculating the actual risk of a position which is not being done now.

For eg. currently there is no margin difference between having say 10 lots short puts vs 5 lots put and 5 lots call short. (short strangle) In the second case the risk is half on a big one sided move but still the margin is the same. A portfolio risk based margin system is needed.

1 Like

Well explained @nithin. However, I feel strong urge to put my viewpoint which may or may not supplement the notion in your post.

Presently there are three main issues going on :-

(a) The high ratio of Derivatives trades vs EQ trades, which in SEBI visdom is too high.

(b) The risk management in terms of upfront margin to avoid any systematic breakdown.

© To save small retail trader from inherent risk in f&o segment.

On the first point, what difference does this high ratio makes? EQ trading or even EQ investing are also speculation only. You never know the exact facts of business. Some say by EQ investing you are buying part of business. True, but there is a difference between owning the business and running the business, specially when you are a minority shareholder. So, even investing through mutual fund has the same effect. Can you name a stock which will guarantee a positive return, however small may be, in eternity, let it be yearly, 5 yearly or even 20 yearly basis. So, stock market is speculation in different forms. And ratio between fno and EQ trades are of no use other than evaluating current trends.

On the second point, apprehension of all stakeholders including sebi, exchanges and brokerage firms are well appreciated. However, as you yourself has articulated that present form of margin is not efficient. Present form hardly makes any difference between naked speculation and hedged speculation. I will give you one more example atleast. If one already has fno shares in no equal to lot size and sell ITM, ATM , ITM , far away otm, i.e. Covered call option writing, he is hardly making any threat to system. But in present system, he is treated as same as naked speculator. Person like you can keep insisting exchanges and SEBI to do some intelligent work rather than implementing dumb ideas.

On the last point, I am strongly convinced that this is an example of crony capitalism at its best rather worst. I recollect that somewhere you had mentioned that retail fno traders moves to scrips which has smaller lot sizes (lot values). Retail traders doesn’t have any specific affinity towards poor quality stocks. In fact they have equal affinity towards good stocks as any other celebrated market player, but the present high lot value of some of the good stocks now a days which drives them away. I believe that lot sizes equal to around one lakh or even more lower will be good to retailers also as they can manage the risk better or even can diversify. High no of transaction in this process is no problem in today age of technology. I don’t recollect at this moment, what is the idea behind increasing the lot value , but I m sure that must be a dumb idea.

I would appreciate if @nithin or any other person from @zeodha counter my opinion expressed above. If not, they may like to bring a research paper on present and proposed ambiguities in SEBI and exchanges working for mass awareness.

Regards.

3 Likes

I think in India we need to urgently relook at our margining requirements to better reflect the particular risks emanating from any given structure. The purpose of posting margin is to cover the risk of traders being unable to settle potential losses. These risks can be of two types: 1. Where the maximum theoretical loss is definable (such as in sold call spread / sold put spread structures), here there is no justification for the margin to be more than this maximum definable loss… and 2. Where the extent of the loss is undefined and must therefore be estimated assuming a large adverse market / underlying move, such as the 10% move now being implemented for Index linked derivatives. The problem in India is that we do not give adequate margining benefit for trading structures with a defined maximum loss even though this is commonly followed by most developed markets e.g. CBOE (sorry, but SPAN doesn’t come even close to giving fair margining benefit for the bought options). Such an approach would significantly incentivise trading of spreads, rather than structures with undefined maximum losses, thereby reducing systemic risk. I believe most brokers and the exchanges already have adequate IT systems to measure risk at the individual structure level, so there is really no reason for not offering structure based margining to traders now.

Please check file row # 13. Code says Godrej CP and name says Godfrey Philip.

There is no debate here, I am by your side. I don’t think increasing lot size is the right way to even attempt keeping retail away. Pushes people from futures/shorting options to buying options, which is a lot more riskier. Also like I have said, if we are able to push all margin to be included in SPAN, automatically benefit of being in hedged positions will be so much more.

But increasing margin as a % of contract value is not necessarily bad. As a broker, if client loses more money than what he has in the account, recovering is the toughest job we have. So if the margin in place covered more risk, it is good for the system overall. If not, it can create systemic risk when markets go volatile.

NSE has licensed SPAN from CBOE for margin calculations. Exposure is what is added additionally. Check this post of mine above.

Hi Nithin

Is that change applies to all script options?

Initially there was only 41 scripts. Now i am not able to figure out the exact details from the mail I received.

I mean long options…

Thanks in advance

@nithin Bit confused here. This 4% additional ASM is on contract or 4% of span margin?. You are saying, 25% additional over current margin by Nov. If they add 4% to total contract, won’t it be around 40%-50% increase to the current margin?.