I have read your post but still believe there is no justification for the kind of margins being charged on even very simple option structures that have very limited risks.

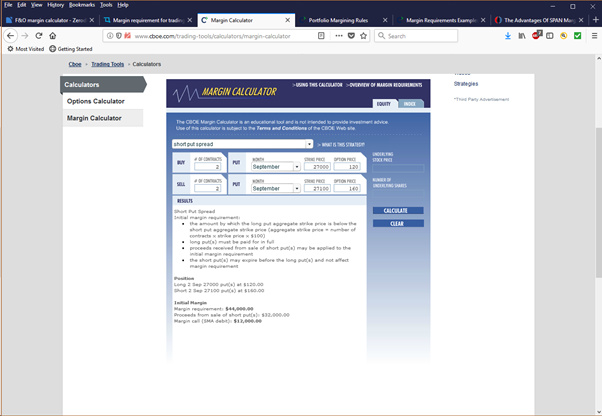

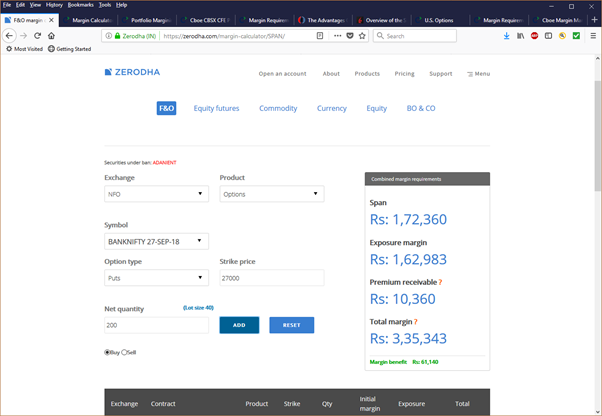

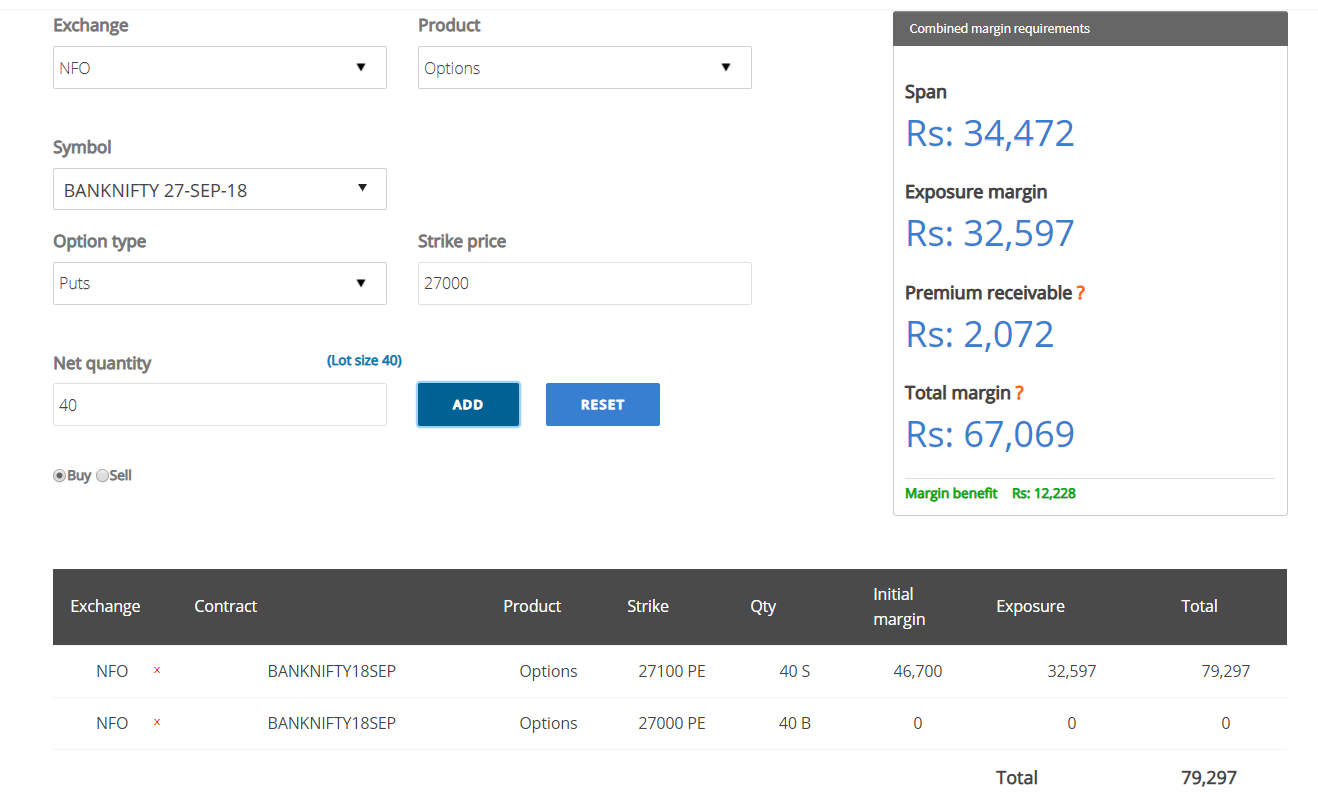

I have modeled the Margin requirement for selling the following put spread on Nifty Bank on both the CBOE and the Zerodha calculators:

Sold 200 Sep Put @ 27100 for Inr 160

Bought 200 Sep Put @ 27000 for Inr 120

You will notice that the total margin required on NSE for the same structure is 335,343/- while for the CBOE is 12,000/- !!! Even if we exclude the Exposure Margin of NSE, the SPAM Margin alone is 172,360/-. You will also notice that the CBOE margin gives credit for the premium received when the structure is sold (which NSE does not). How can this be justified? Isn’t there something inherently wrong in the way margins are being calculated for these structures?

There is no doubt that there is serious excess margin already being charged for these structures, even before the latest increases. In my view if SEBI / Exchanges want to keep retail investors away from f&o risks, better to institute a rigorous exam as a per-requisite for trading f&o rather than charging humongous margins that are way in excess of the risks involved, a suggestion someone already made on this forum earlier. Also, SEBI can regulate the market wide position limits on any underlying if it feels there is too much f&o being traded on it.

Current margin is 8% of contract value for index futures. So This will go upto 10% of the contract value . The increase is 2% over 3 months. 2% is 25% of 8%.

For shorting index options, the margin required will be higher - especially for in the money options the % margin required will go much higher - by almost 40%. It is currently around 6% of the contract - will go upto 10% of the contract value.

The reason for this is, today instead of buying futures - you can short deep in the money calls with lesser margin - but with similar unlimited risk position.

Instead of 67k, assume only around 2.5k was charged (12k for 3.3, so around 2.5 for 67k).

What will happen if a client decides to exit the bought put option first? Should the platform allow a client to hold naked short option with just 2.5k in the account? - for whatever little time it takes to exit?

or, what if the client exits long put and then there is no liquidity on the short put position and he isn’t able to exit?

There are so many scenario’s where this can go horribly wrong and bring huge systemic risk to the industry. What you are asking for is possible only if the Short put spread was trading as a single product on the exchange. So a contract - Banknifty27100S27000B trading at Rs 40. Based on if you are bullish or bearish on the spread, you trade it directly.

Can the exchange introduce such contracts today and expect liquidity on it? I don’t think so, India is still atleast 20 years behind in terms of professionalism of the trading community compared to countries like US. The reason for this is we were introduced to derivatives only in 2000’s, whereas US has been using derivatives forever. Interest rate futures, VIX futures both fared miserably as a product when introduced here. VIX failing with so much option trading happening here was shocking.

So yeah, hopefully we will have option strategies listed as a product on the exchange over the coming years. But the first step towards that would be to make it more attractive for people trading strategies than trading naked positions by hopefully including Exposure as part of the SPAN margins itself.

Hi, Nithin

you are explain this Risk Scenario to we trader, which is great.

But as a Derivative trader we all should know all this common things before going to trade derivatives product and this is not hard simply have to qurious mind about the work we do.

AND this is the type of lack in knowledge indicate by SEBI & NSE.

Plz don’t take it wrong I am not in favour of SEBI & NSE for all steps they are taking.

@nithin Well abroad one can do spreads with low margin without any separate product being listed. Basically if one tries to cover the long option side first, that can only be done if there is sufficient margin for naked short leg… otherwise that order would be rejected and short leg would have to be covered first to close the position.

Yep, that is what I meant by a product. Ability to tie in two separate contracts. Currently in India calendar spreads for futures work in a similar fashion.

I’d like to put my input on the three points you mentioned -

There was recent report that stated that the actual equity to derivatives ratio is under global normal. It’s not 15 times lol. One thing is that derivatives is a leveraged product so naturally you are paying less to buy more, so when you look at turnover in terms of the contract value it’s gonna be higher than equity but even then if you look at futures for examples it is only roughly 2 times more. And if you look at margin turnover, then of course it’s way less than equity. But of course SEBI is our daddy, they must know better. Hmmm hmmm hmmm.

Well, it’s gonna reduce profits just as well or I should say Return on investment. Trading is a business without a doubt and clearly we need less profits because we’ll that’s what our regulator thinks. And for the systemic breakdown I keep hearing. Well, what is that? People gonna run into debts? Well, that will never happen. The system is designed like that and it has never happened as stated in a report that everyone has been margin compliant.

Greatest risk is ignorance. Try saving that SEBI. You should get into trading only when you know the risk behind it. That applies to not only derivatives but equity as well. Someone in moneycontrol forums wrote that he bought Bel at 150 on ashwani gujral’s recommendation and now bel is at around 88. That’s burning roughly half of your investment. So, you can see how ignorance is biggest risk factor. That’s just one of the several examples of ignorance I can give but that’s for another day. And they want higher margin to reduce losses. But well it’s reducing profits as well. So it’s not a particularly good logic. And not to mention how the ecosystem of the market will be affected as a result especially for retailers. And like I said, everyone is margin compliant so you are not gonna loss more than you put in. And even under higher margin requirements you can still lose your entire capital if you are not careful. And what else do I say. Intraday is a thing know. People put their entire captial in intraday and lose it real quick. So I don’t know the whole logic of “We must protect retailers against losses” is flawed really.

Nithin,

I agree with your logic.

There may be hundreds good logic or argument in favour or against the decision of SEBI / NSE.

But, you MUST agree that with with these thousands of logical conclusion and argument, best practices comes up.

Now, Europe and US has much a bigger market than ours. And they already have come across with these problem which is experienced by SEBI or NSE.

So, my suggestion is that we should follow the best practices already evolved or settled in Europe and US.

Further, all the present instruments of NSE or BSE are simply a replica with little modifications of the instruments prevailed at Europe and US.