From the panic lows set in April, Markets are doing pretty well despite many events like Wars, tariff tantrums with Nifty at a touching distance from fresh Highs, while Banks and midcaps are already at highs. But things still seem a bit wobbly with many events around the corner.

Motilal Oswal shared some interesting insights to give us some clarity around where things stand. Here are some of the key highlights:

1. Valuations

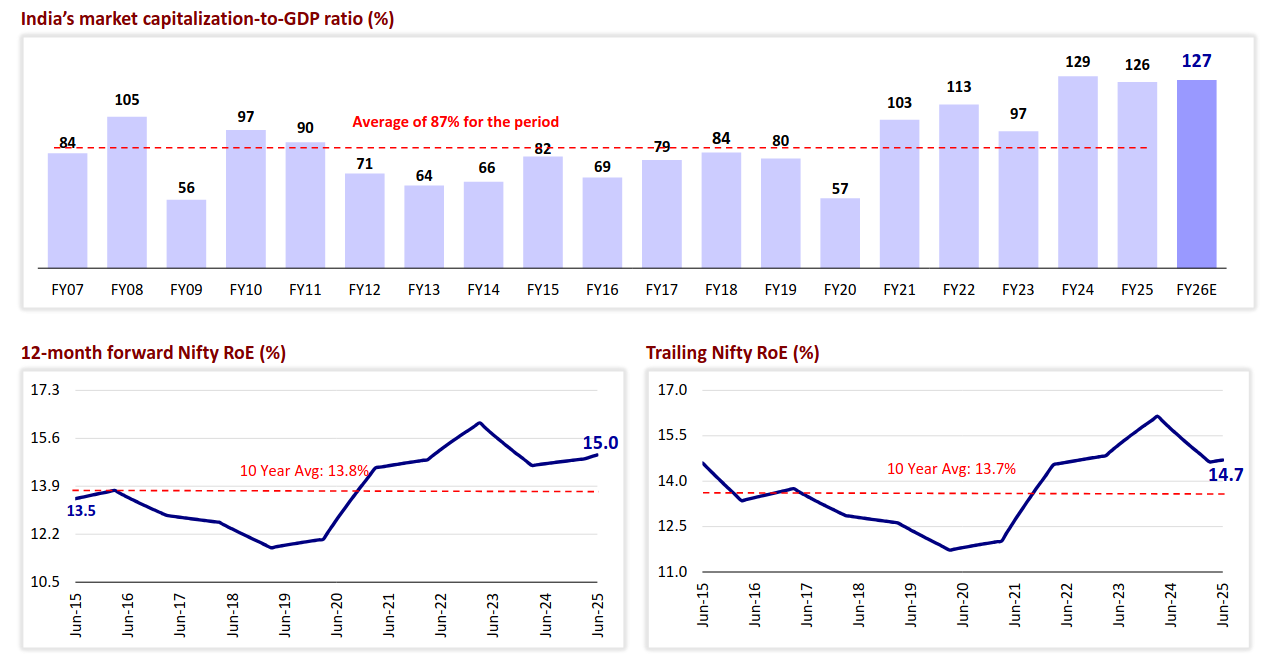

India’s market cap-to-GDP ratio has seen sharp fluctuations in recent years:

-

It fell from 80% in FY19 to 57% of FY20 GDP in March 2020.

-

Since then, it has rebounded strongly to 132% in FY24 and 126% in FY25.

-

Currently, it stands at 127% of FY26E GDP, based on an estimated 10.8% YoY GDP growth,

which is well above the long-term average of 87%.

-

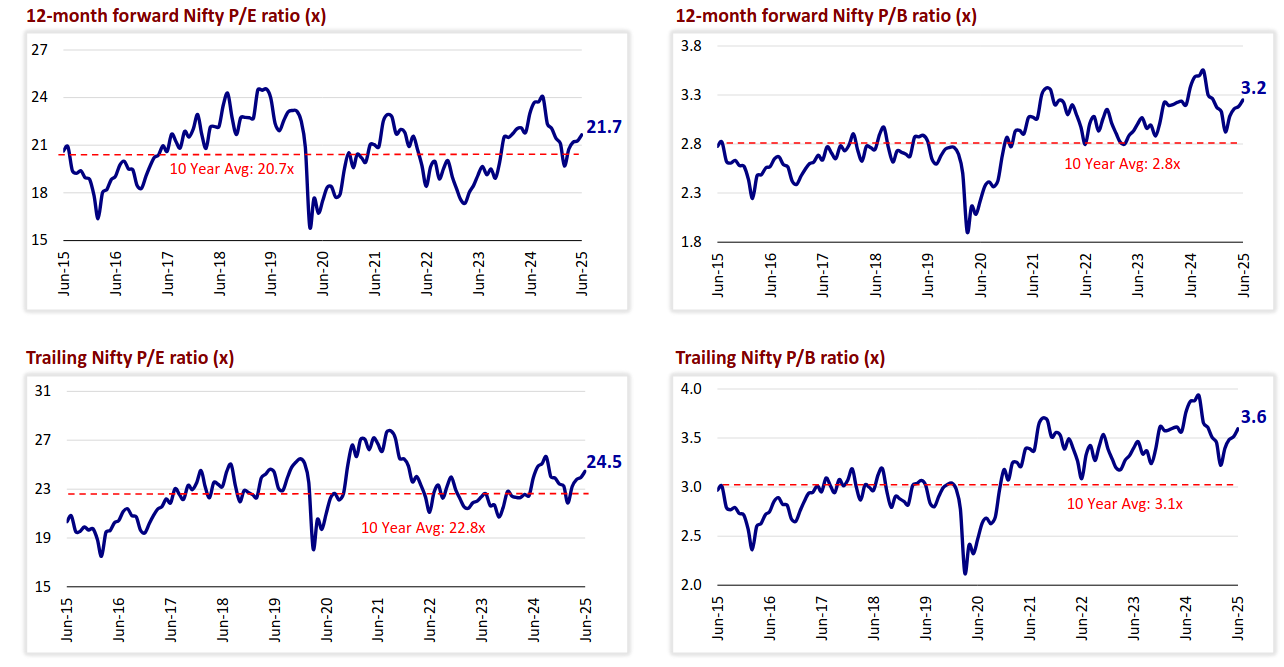

Nifty’s 12-month forward P/E is 21.7x, which is 5% higher than its long-period average (LPA) of 20.7x.

-

Forward P/B ratio stands at 3.2x, reflecting a 14% premium to its historical average of 2.8x.

-

12-month trailing P/E is 24.5x, 7% above the LPA of 22.8x.

-

Trailing P/B ratio is 3.6x, showing a 15% premium over its long-term average of 3.1x.

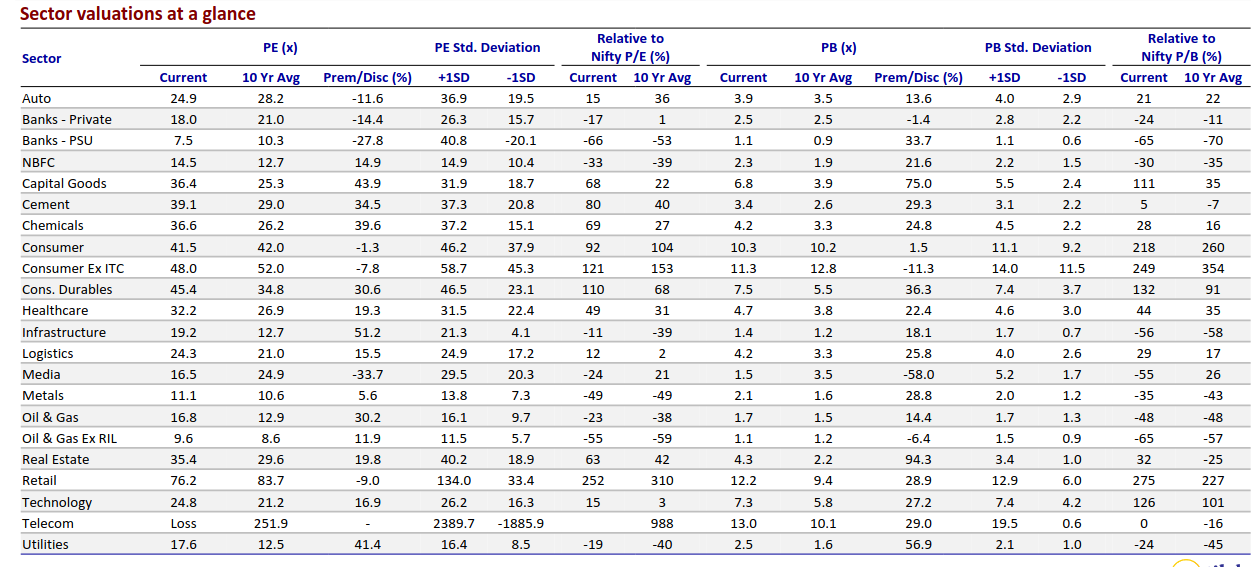

2. Sectoral valuations

Two-thirds of the sectors trade at a premium to their historical averages

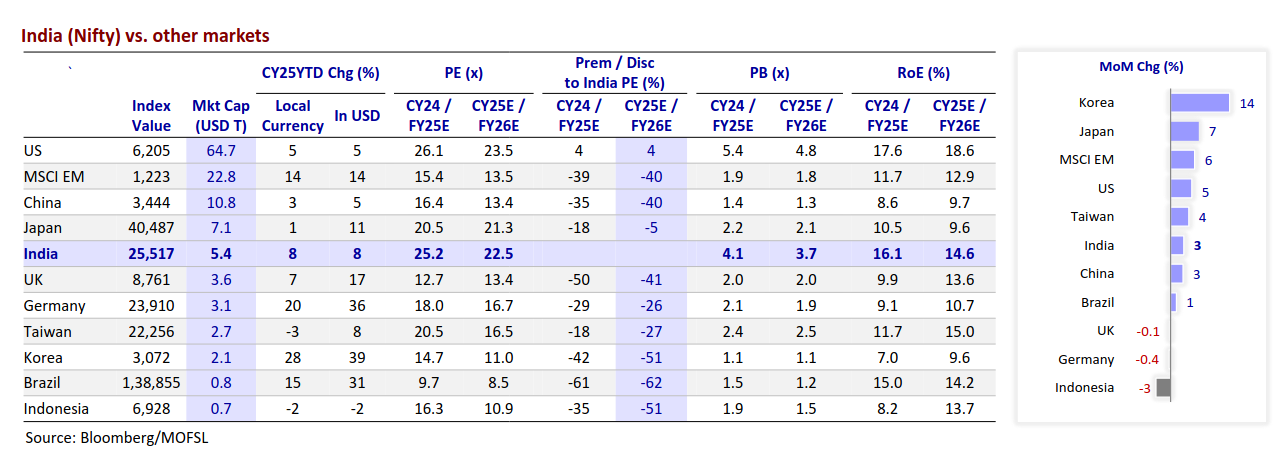

3. India, when compared with Global markets

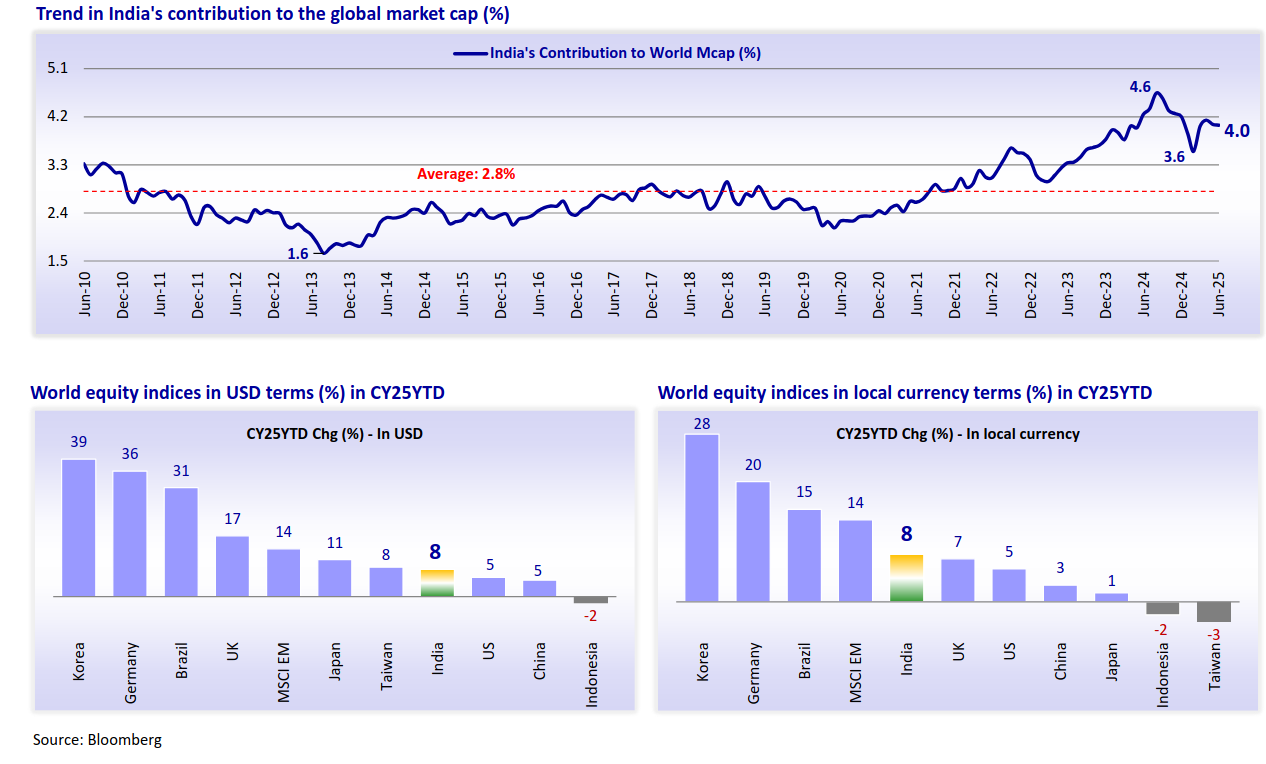

- India’s share of the global market cap rose to 4% in June 2025, recovering from a 16-month low of 3.6% in February 2025.

- India remains one of the top 10 contributors to the global market cap.

- As of June 2025, the top 10 countries together accounted for 82.5% of the global market capitalization.

- Over the last 12 months, global market cap has risen 13.4% (USD15.9t), whereas India’s market cap has increased 8.1%.

- All major key global markets have witnessed a rise in market cap over the last 12 months.

4. Nifty V/s Midcap and Small Cap

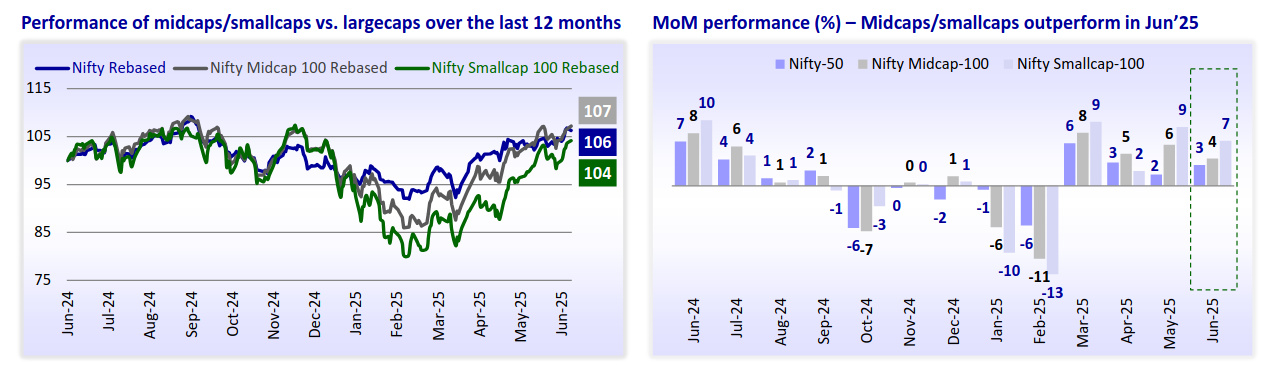

- Over the past 12 months, largecaps and midcaps have delivered gains of 6% and 7%, respectively, outperforming smallcaps, which rose by 4%. However, over a five-year period, midcaps have significantly outpaced largecaps with a return of 158%, while smallcaps have outperformed even more sharply, delivering a 165% gain compared to largecaps.

5. Flows

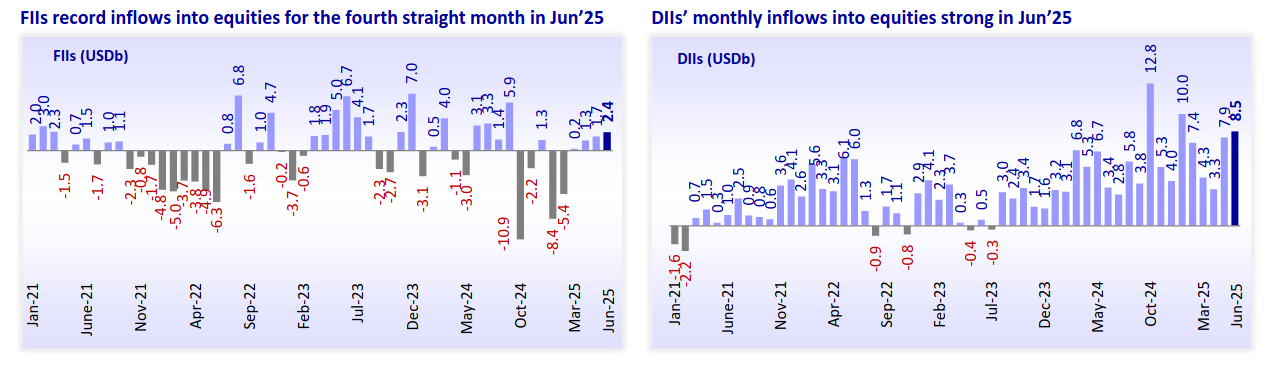

- Foreign Institutional Investors (FIIs) were net buyers for the fourth straight month, investing USD 2.4 billion in June 2025.

- Domestic Institutional Investors (DIIs) also saw strong inflows of USD 8.5 billion during the month.

- Despite recent buying, FII outflows in Indian equities have reached USD 8.2 billion in CY25 YTD, compared to outflows of USD 0.8 billion in CY24.

- DII inflows remain robust, totaling USD 41.5 billion in CY25 YTD, following USD 62.9 billion in inflows during CY24.

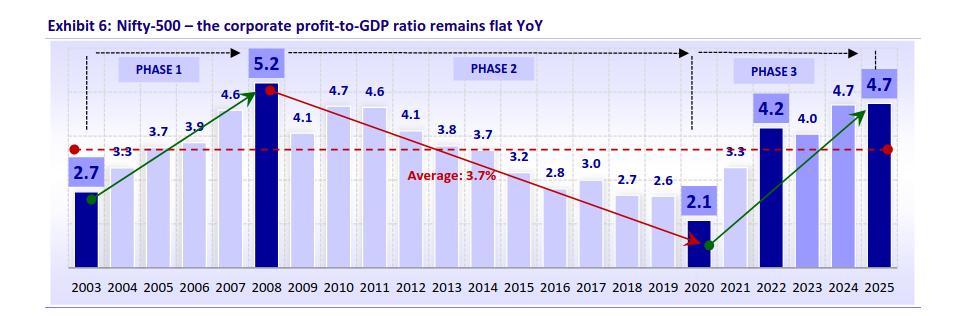

6. Corporate growth to GDP at 17 year highs

-

In 2025, the corporate profit-to-GDP ratio for the Nifty-500 universe stood at 4.7%, marking a 17-year high, while for listed India Inc., it reached 5.1%, a 14-year high. This strong performance was driven by sectors like Telecom (which turned positive after seven years), PSU Banks, Healthcare, Consumer, Metals, and Infrastructure. On the other hand, sectors such as Oil & Gas, Automobiles, Cement, Utilities, Private Banks, and Retail saw a decline in their contribution.

-

Despite a high base of 30.5% growth in FY24, Nifty-500 corporate profits rose by 10.5% in FY25, maintaining a robust 5-year CAGR of 30.3%. This growth came amid weak consumption, reduced government spending during the election period in early FY25, and export volatility caused by global uncertainties.

If I were to summarize in a para:

Our markets continue to show growth despite prevailing headwinds, though valuations remain on the higher side—perhaps reflecting the strength of underlying fundamentals. Global markets have held up so far, but uncertainty remains a persistent theme.

As the saying goes, India never fails to disappoint both optimists and pessimists.