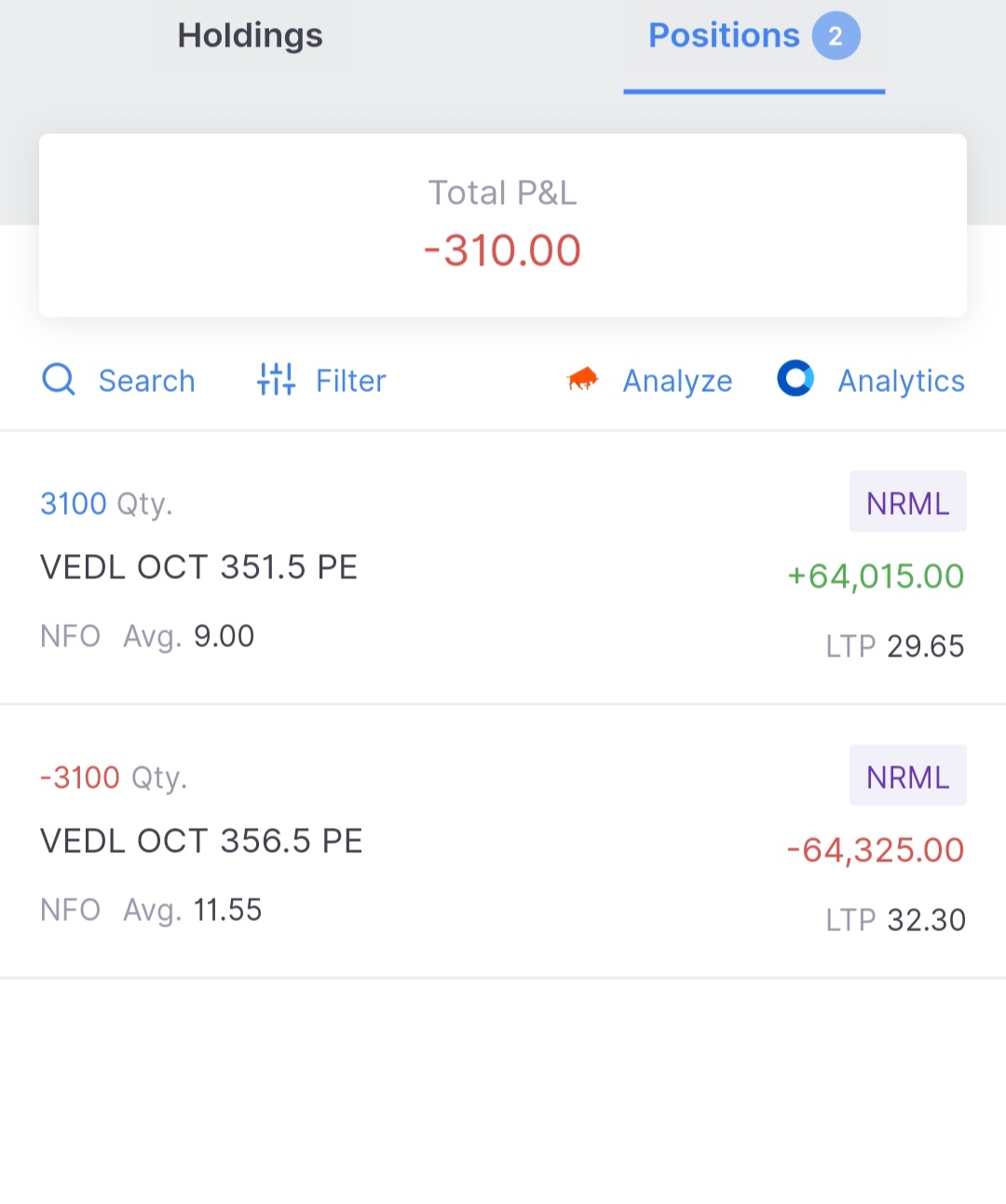

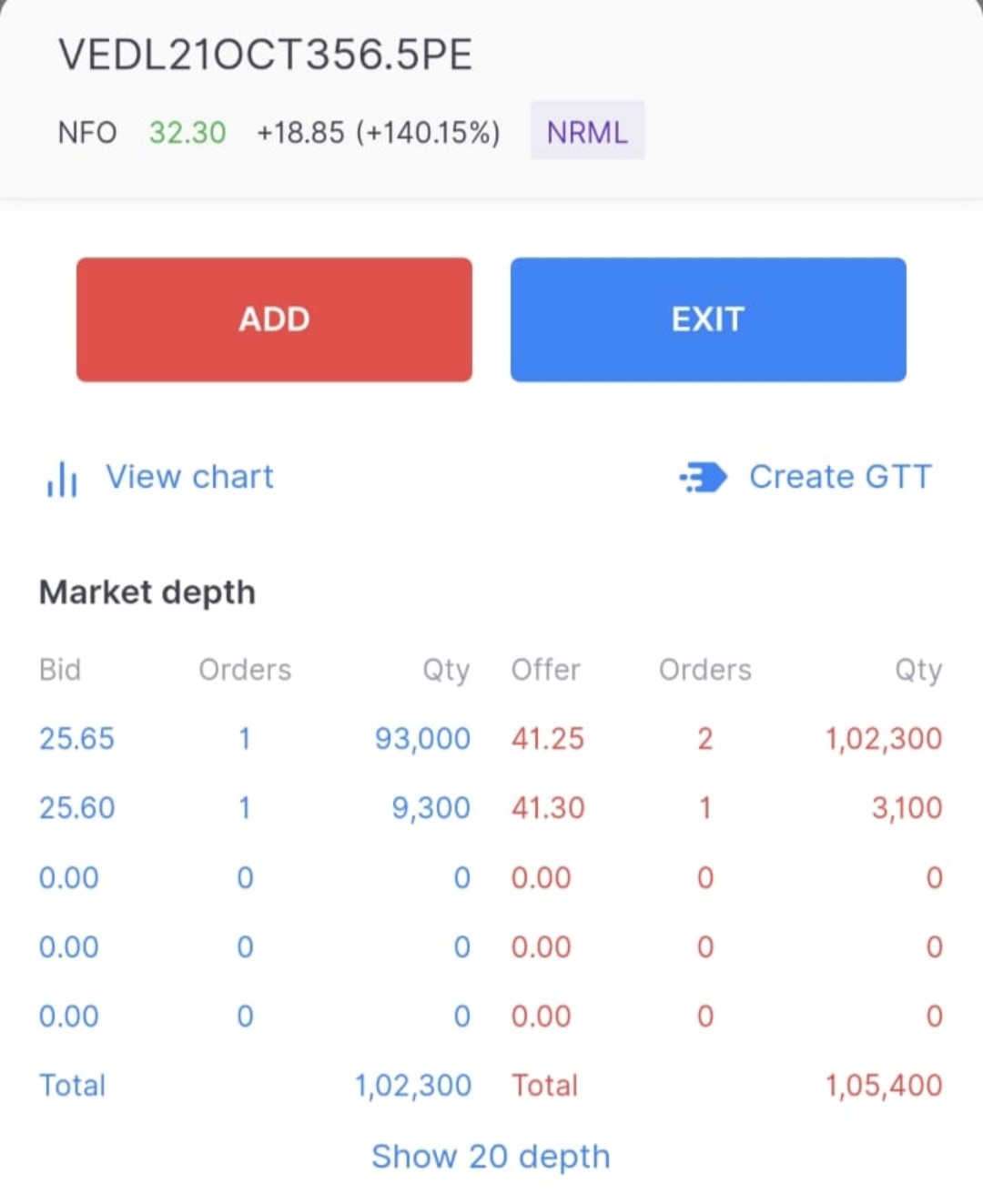

I am holding hedged positions in VEDL(Refer attachment) 351.5 PE long and 356.5 PE Short. Both are ITM.

There is no liquidity and hence I am unable to square off yet.

As both are deep ITM, if it expires in ITM, I dont have delivery obligation and it will be a net off. In that case my losses will be limited to 7.5K + minimal exchange /broker charges.

I am worried if RMS team may square off my positions in the meantime.

I have added funds and can add if needed. However I am not very sure how much I got to keep to ensure there is no square off till expiry.

Can anyone please help me with this detail? and any tips to hqndle the situation with minimal loss.

Note: extra margin won’t be required in case of hedged index positions, as they are cash settled only. While in stock options due to compulsory physical delivery of stocks, extra margin is required in the last week of expiry.

I am reqdy to arrange and have necessary margin. However for these poaitions, I am not sure what is the exact margin I need to keep Thats what I need to know in specific

For ITM Long Stock Option positions, you’ll need additional margins from expiry minus 4 days. The exchange blocks physical delivery margin as a percentage of applicable VAR + ELM + Adhoc margins of the underlying.

For Short Option position, the margin requirement will only increase on expiry day to 40% of the contract value or SPAN + Exposure margin (whichever is higher).

Based on available info the following seems to be the case. Can you please advise?

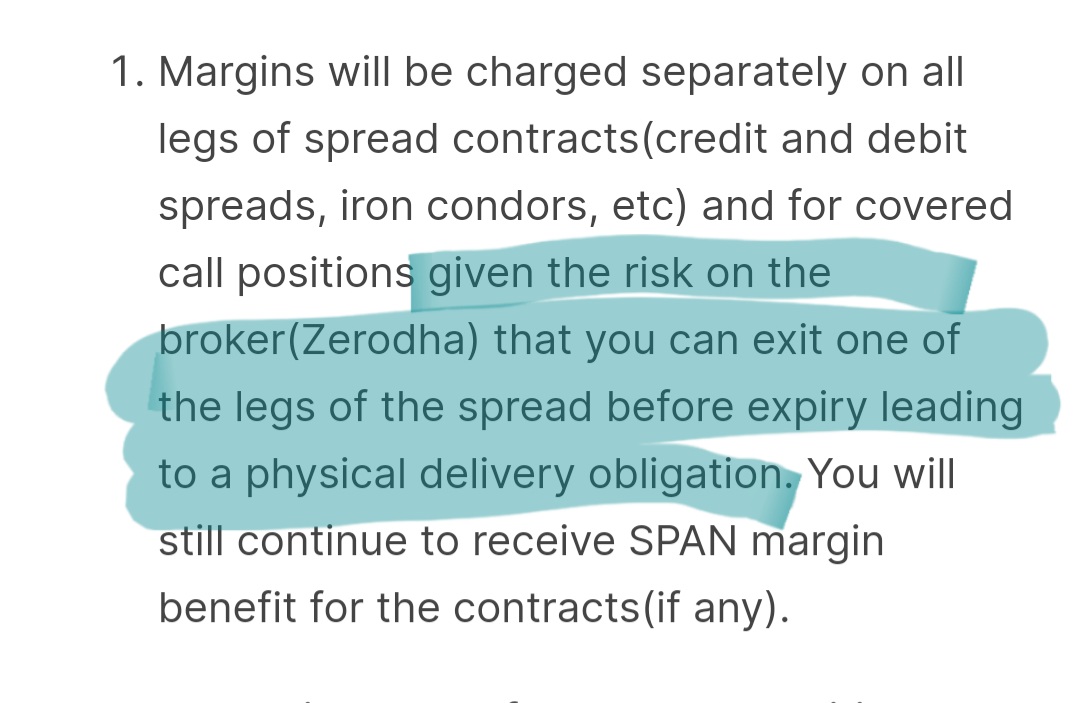

//Margins will be charged separately on all legs of spread contracts//

Hence, I need to calculate maintain margin for both legs ? no hedge benefits on margin at all? [ I understand there wont be any delivery obligation as it will be a net-off if both expire ITM]

To keep position on Thursday till expiry:

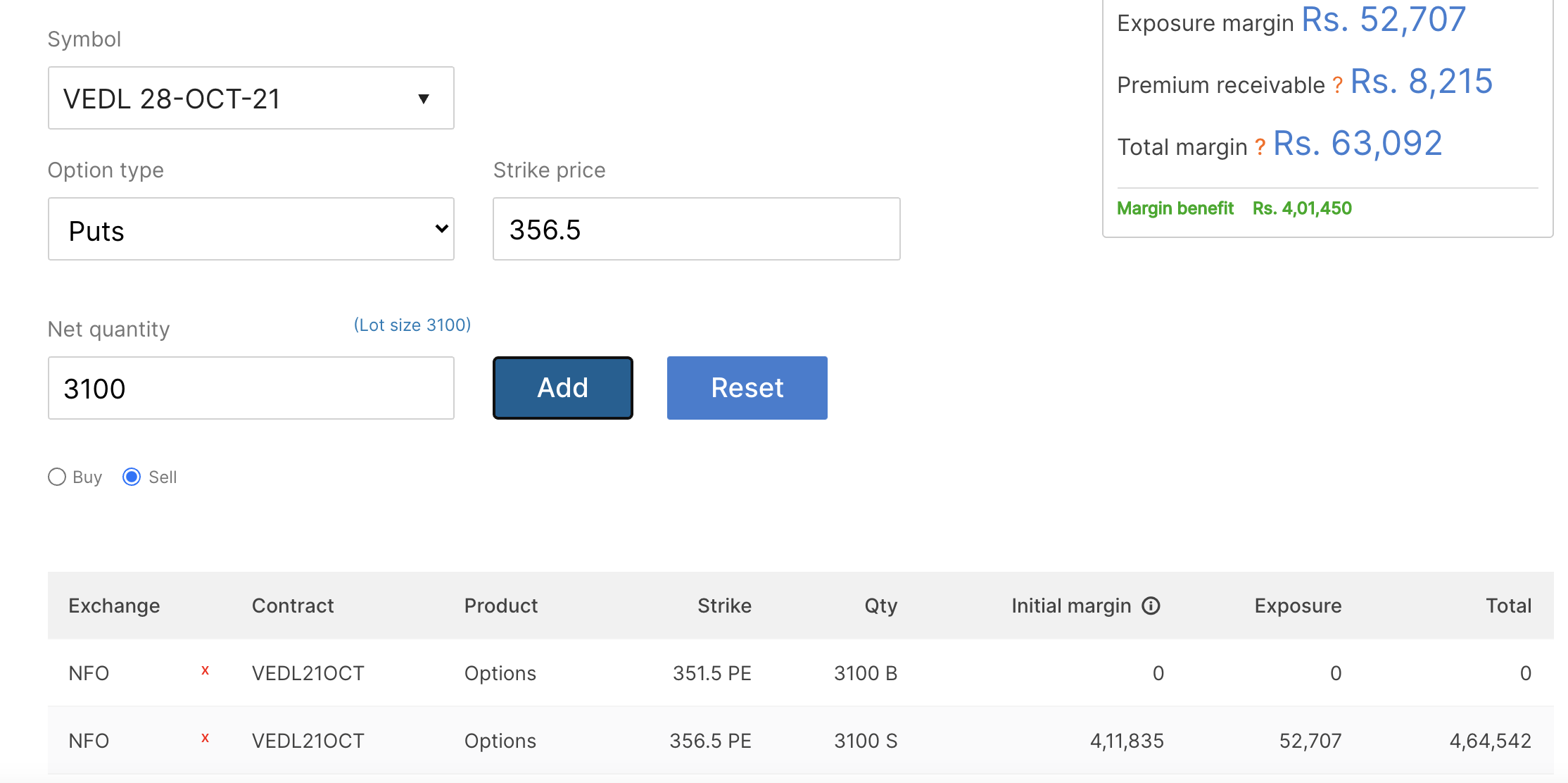

Long option : 50% of contract value : = 50% of 3100 * 351.5 = 4,35,860

Short option : 40% of contract value on Thursday = 40% of 3100 * 356.5 = 4,42,060

Hence I need to have a margin of 8 lakh 75 thousand to keep this spread till expiry ?

In addition the VAR + ELM + Adhoc could change and if that value becomes more the margin for short will further increase?

Are these the right figures? for a spread where I can max incur a loss of 7.5K if left till expiry? ( Refer attached pic)

In this case it is fine to keep the margin for the leg which is higher right? why margin needed for both? if both legs are kept the single leg risk is not there… if exited one leg, only margin for other leg is required.

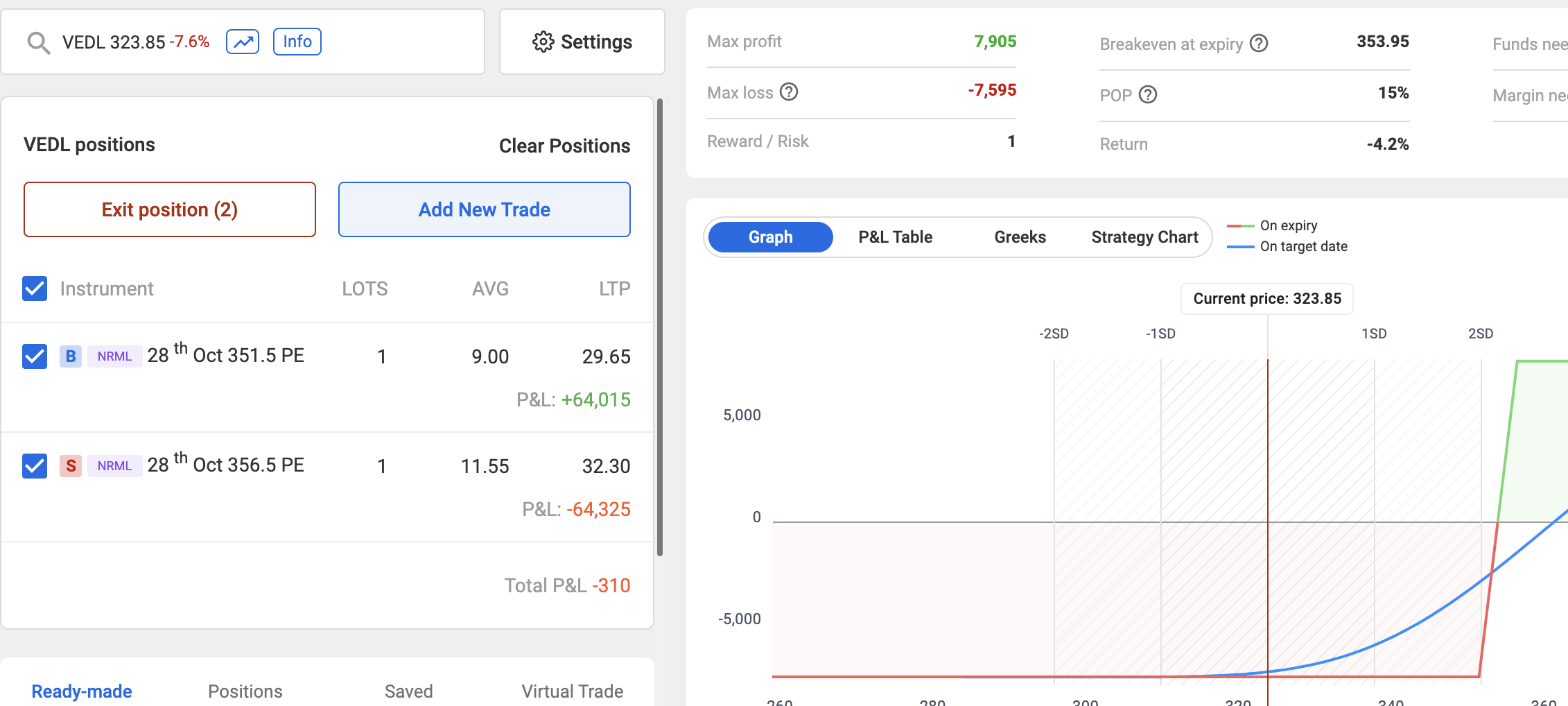

If I maintain necesary margin (5Lakhs) and allow my positions to be expire and net off (Say VEDL final price is below 340) How will my profit / Loss be calculated and posted?

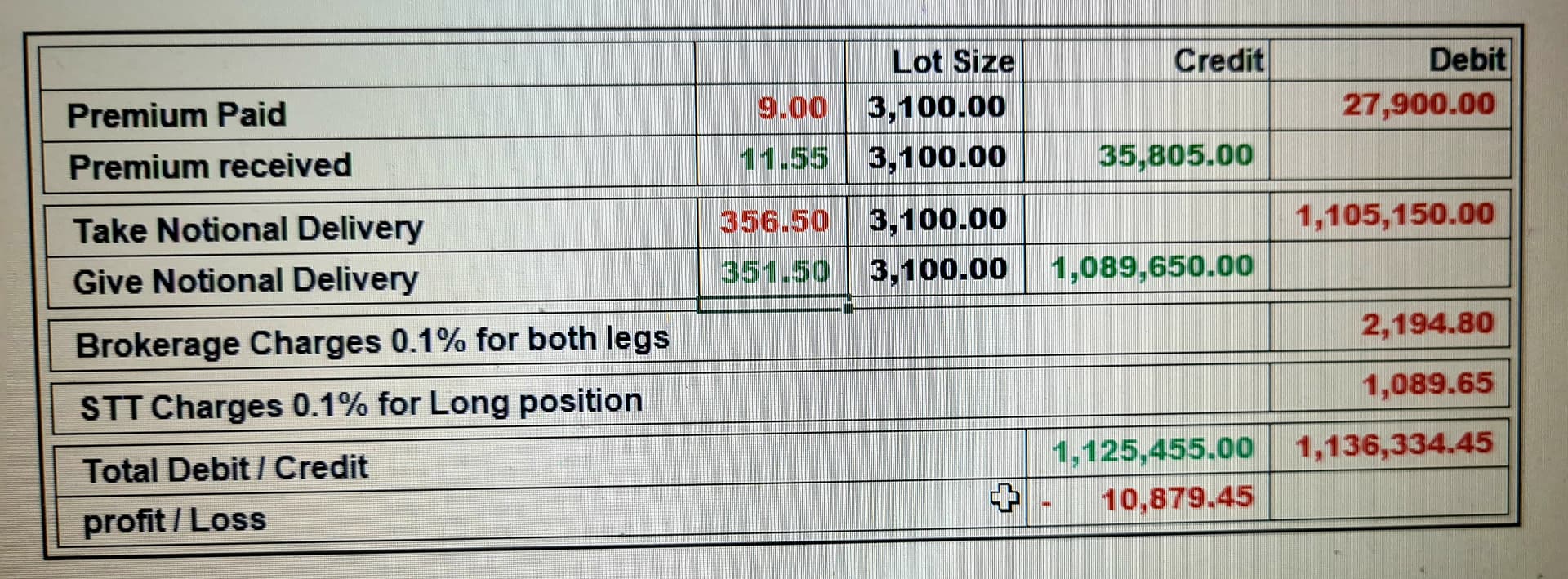

I bought 351.5 PE at 9

I sold 356.5 PE at 11.55

Hence my loss will be (11.55 -9)× 3100 = 7905? Is this correct?

There will be some broker / exchange charges as well

How much that could be?

Appreciate if you can be specific with figures.

Is there any other risk I should be careful about?

Thanks for your continued support.

Bro…I think net off would incur 0.1% brokerage of contract value…and I think stt as well…concept of notional delivery applies that’s why I think…Hope someone more knowledgeable can elaborate…

God bless

I want to understand how the profit or loss be calculated and posted.

I understand it will be 0.1%. Is it on the full contract vamue of both legs or on the difference?

From the NSE FAQ document, the value seems to be the difference of both contract values. Hence asked for experts to advice. Please refer Column L in attached screenshot from Annexure 2 sheet from NSE.

No. As an option seller, you will get to keep the premium received, while you will lose the entire premium paid for buying an option. This is because ITM Stock Options expire at 0 value. The Strike Price of the option will be the settlement price for the physical settlement of shares.

In the above scenario, for the Long Put Option, you will be delivering underlying shares at 351.5 and receive 351.5 * Lot Size, while at the same time you will be taking delivery of shares for Short Put Option at 356.5 and will have to pay 356.5 * Lot Size.

But as your position is hedged, the obligation will be netted-off and the the difference between the amount payable and the amount receivable will be your Net P&L. You can check out the exchange FAQ here, the exel sheet explains the scenarios in detail.

For all netted-off positions the brokerage will be charged at 0.1% of the physically settled value.

For netted-off positions, there will be STT charged at 0.1% on the long position(s) as this is treated as notional delivery. More details here.

Thanks for detailed explanation. This makes it very clear. Hence I dont need to worry about the settlement price at all once both legs expire at ITM.

For illustration purpose and to know the overall profit loss I just put the values based on your response. Pls have a look if you got time.

Based on this I will try to square off before expiry if I believe the overall loss will be less than 11K . Else I will ensure to have margin and leave it to expire.

@ShubhS9 For short deep OTM stock options, are the additional margins required on Wednesday evening or Thursday morning?

If I were to square off the position on Thursday morning as soon as market opens, would I still be required to bring in additional margins?