According to me, these stocks are going to produce huge return in 2018.

High Confidence

Sanwaria -> The stock has already given a 800% growth last year. Sanwaria has added multi operational businesses and new products recently. Tie up with Patanjali for supplying raw materials, robust and growing quarter results, soon to be pan-india presence all these are triggers for the stock to continue posting good numbers. CMP-26. One year target 95+

Future Retail -> This company is providing cloths in wide range of pricing (low to high). Many offline stores across all the big cities and few stores in tier II cities as well. Plus the Management of the company is very sound . Good promoters share holding and continuously increasing profit every quarter. This company is doing well in their peer group too.

Sanghi Industries -> One of the largest producers of low cost cement. Key beneficiary of housing for all project. usually posts solid growth in the third and fourth quarters every year. Its peers are as expensive as three times its stock price so a strong re-rating can be seen very soon since Motilal Oswal have started coverage with a buy call. CMP-139. One year target 265+

Less confidence

L&T Finance -> The company is in the consolidating phase after reaching 210 levels one month back. Its unique business model, wide presence and a large market cap can drive it to it`s actual valuated price in the coming year. CMP-174. One year target 260+

Jamna Auto -> Auto ancillary company with a 72% market share in auto suspension products with a huge order book, surplus cash flow, huge dividend yield and a long list of clients. Also ranked in world top 3 companies in the segment. Since suspension products are going to be used by both non electric and futuristic electric vehicles, the business of Jamna auto will be unaffected by the entry of electric vehicles. CMP-81. One year target 210+

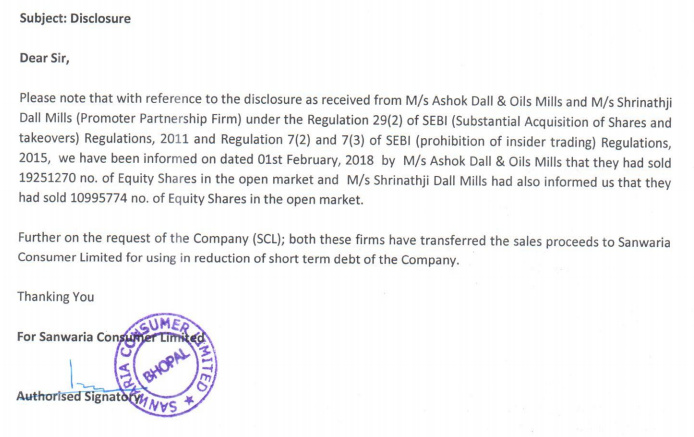

Promoters sold total Shares of 30247044 in the open market to reduce short term debt as per the update submitted to BSE and resulting in reduction of promoter shareholding to 67.56% from 71.68%. The transaction happened in December and they have reported very lately after announcing the results. The reason given by promoters for selling is stake is to reduce short term debt. BSE link

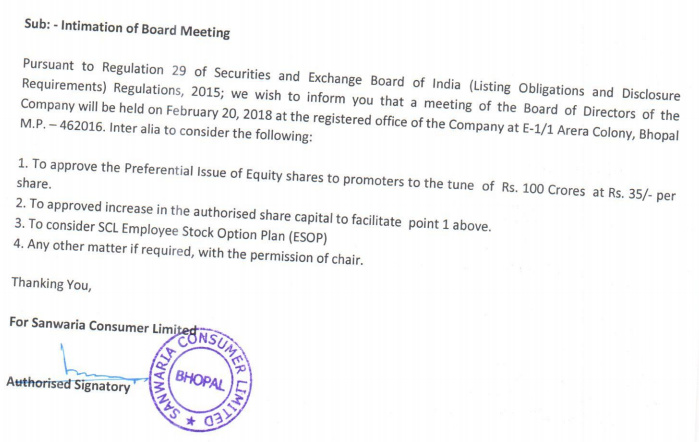

Now they updated bse saying that, Issue of preferential shares of 100cr at a price of 35/- per share adding these shares again promoters shareholding percentage will come back close to 70%.

Why promoters sold the shares in open market and they are issuing preferential at price 35, why can’t they use the same amount to pay back the debt ? Doesn’t it looks like big negativity on the promoter integrity ?

Is there something I’m missing ?

and the target 95+ is something impossible for sanwaria to become 95+, with of P/E of 25 and EPS 3.8 is achievable, considering equity dilution through preferential shares and ESOP, acheving 95+ is impossible as EPS 3.8 is very difficult to achieve , you cannot expect sanwaria to be at high P/E rated company, as they a lot debt and considering promoters integrity.