Hi, I have been investing in direct stocks since 2 years. (Infosys, TCS, ITC, Wipro, ICICI, HUL, Asian Paints, IDFC Bank, Karnataka Bank, KVB Bank etc)

Now I am planning to start SIP for long term using MF’s since i can’t concentrate on looking at markets daily. whats your give suggestion on my portfolio:

Depends on what you are investing for, your return expectation, or if you are not expecting anything, how long will you invest etc.

ELSS is for tax, and as such, it should be looked at differently if your 80C is not maxed out by other ways, and not to be mixed with other funds, because we cannot redeem before the lock in period and we can move to open ended funds once the lock in is over. It can be part a of a equity MF PF if that is the plan.

My return expectation is 10-12%. Investing for 7-10 years

Mirae Emerging bluechip has SIP limit of 2500, since Mirae ELSS has almost same portfolio so thought to add. Yes, i need it for ELSS

All are equity , I would suggest diversify atleast 10% into gold .

Gold and equity are quite opposite , any unwanted situations like corona gold will come into hand.

ex: During situation like corona / recession Gold traditionally trades at much higher , at that point you can sell gold and buy equities which would be trading cheap.

if you are doing a job please go for elss will help you save tax . consider nifty 50 index that is much better in tracking coz all others you need to aware of many things . nifty 50 you just need to see once thats it . there is one elss fund which follows nifty 50 incase if you are interested.

Thanks to @GB26 and @siva0 for their good suggestions.

I am also looking for creating a portfolio of Mutual Funds for my specific needs, but unlike you, who is investing all of it into equities, I am doing investment into debt, for my preference of safety over the returns.

During this process, I came to know about the importance of buying the funds in the DIRECT Plan, rather then buying them in the REGULAR Plan. I would suggest you to do all the buying in Direct Plans only. Please checkout the following article to understand this important point -

Also, please be aware that most of the actively managed Mutual Funds are under performing their respective benchmarks, as explained in the following link -

Government bonds will double your money in 10 years (at current rates). I suggest 50% in gsecs, so at the end of 10 years you are pretty much guarantied by the Indian government to receive your full investment amount (if other investments happen to go to zero).

The rest, you can risk on equity or anything else you wish to bet on.

10-12% is possible and a fair expectation, but as you may have seen with stocks, the return of this 10-12% may not come every year, a lot of things have to work for the stock market for giving such a consistent return year over year, so even if you get such return for 3 years in a row, the 4th year’s returns could be -20%, so the profit will get decreased, hence goal based investing and asset rebalancing, wherein investors shift gains from equity to debt or from debt to equity.

So to have a clarity of the time period one is investing is good, but it is just the 1st step, next step is having a plan to reach the goal.

A goal is not necessary, but if that is the case, you should be ready for swings, market goes up, you get more than your expectation, market goes down, there could be capital loss, and after 10 years what will remain, no one knows.

Any asset class that has volatility behaves like this, goes up and down, while going up is certainly to our advantage, as we get a chance to make inflation beating returns, going down is also a possibility which always exists, so yes it has to be considered while investing.

Nifty 50 value 20 fund? (Personally i like the constituents of this fund, even i hold majority of them in my stocks portfolio)

Nifty largemidcap low Volaitility 30 index fund?

Nifty alpha low volatility 30 index fund?

Nifty 200 momentum 30 index (I dont like this because it has high PE stocks like Adani)

Since I do not have practical experience of investing in such ETF etc. so I will not be able to make specific suggestions on this, but this link has got some useful information - ETF: Complete Guide to ETF Funds | Angel One

Unlike universally accepted standard deviation, factor based funds are not defined precisely. So it will be a tough choice, there is also a arbitrary element in them. So it is advised to for market cap weighted indices, or the lesser preferred choice equal weight index.

Also, the current constituents are in your stocks PF, what if they change?

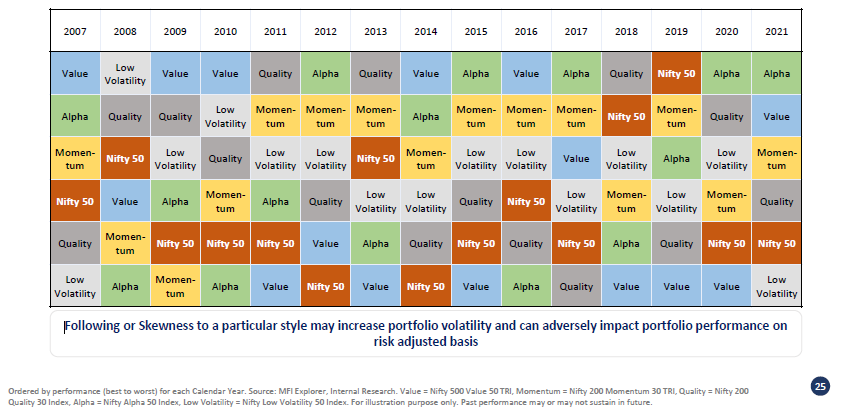

above snippet is from whiteoak presentation. Effectively it means it not possible to predict which factor will perform better next year. It make sense to book profit from factor which has performed better and rebalance all factor funds to the weights which you have originally thought of.