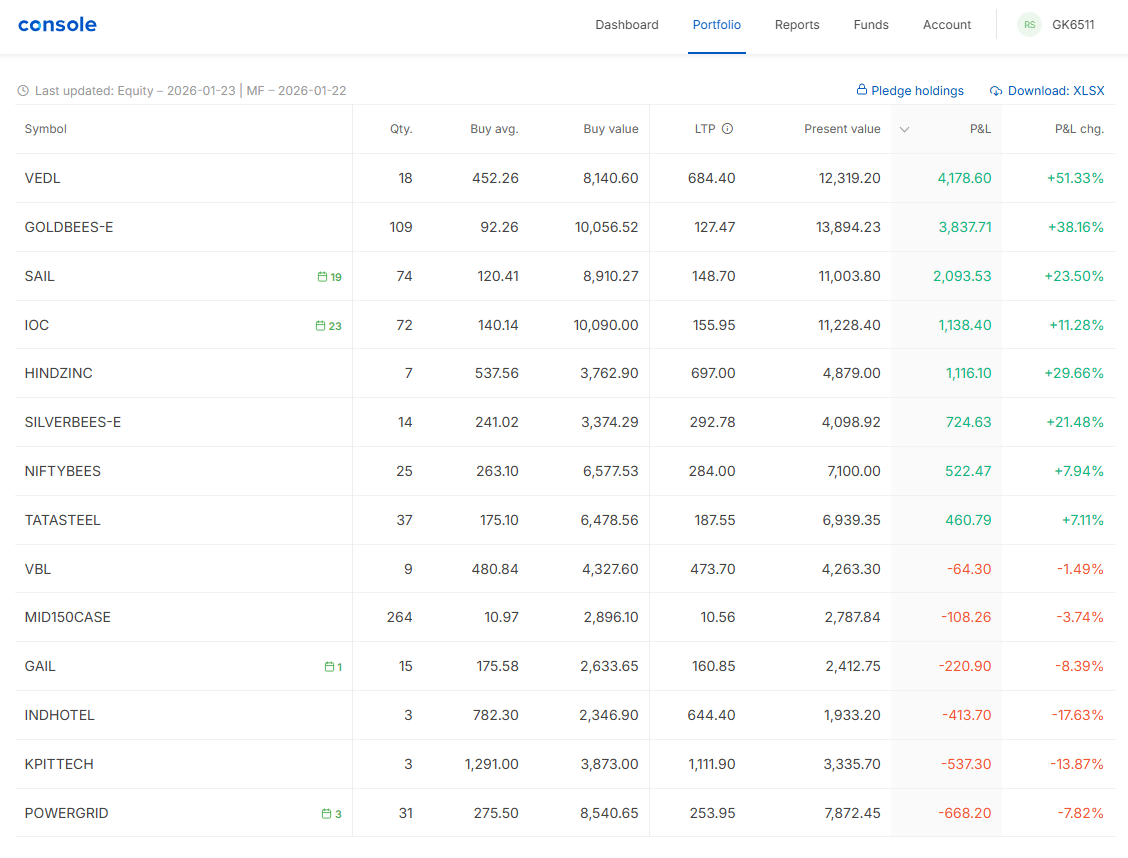

How can I say that I am a good investor if I am currently holding a 15% overall return on my entire long term holdings, I mean that I am nowhere getting any benefits of investing 82K in markets. I will have the profit if I sell those shares (Example: VEDL sold @50% gain).

Can anyone please suggest how can I get my profits withdrawn keeping my capital untouched.

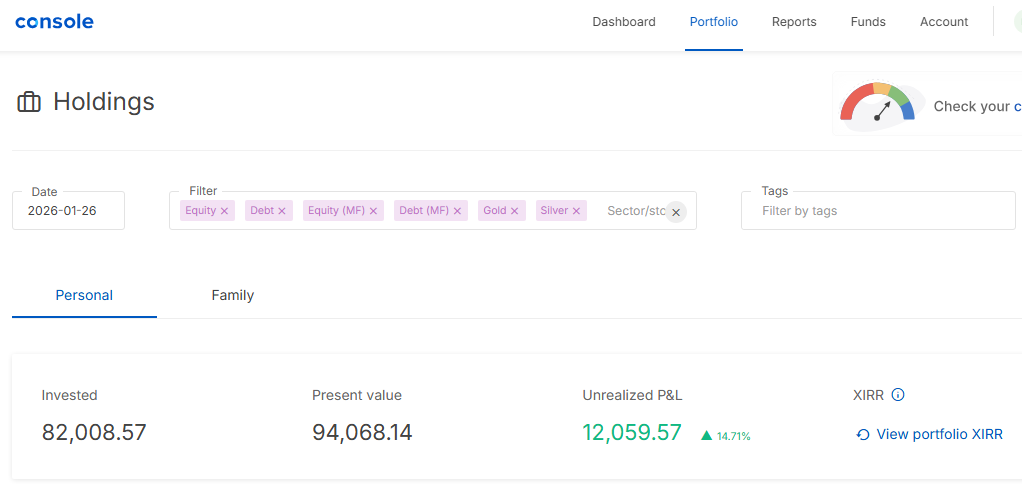

Consider me new to saving and investments. (Invested - 82K / Current value - 95k / Saving acc. balance - Rs. 675  )

)

Your query is very unclear

2 Likes

I need suggestions for getting small amount of regular incomes in the form of dividends or something like that.

There is no benefit of capital appreciation until you are selling your asset, and that is why I am looking for profits/income without selling any of my holdings.

For all direct investment you have made such as VEDL, Powergrid, Sail, IOC etc these companies do declare dividends and you must be getting them. But since the quantity is smaller, the amount will be lower.

From what I can understand, you seem to be comparing equity investments with Fixed deposits or bonds that give out regular interest income. This can be achieved by some of the ways explained by @pavinjoseph

If you want a regular income, you can switch to IDCW plans in mutual funds. They will provide regular cash flow in the form of dividends. (not guaranteed though).

As far as withdrawing profits is concerned, one way is to sell the equivalent amount of shares, as the profits made (in the above example 12k worth of shares). This will bring down your present value to 82k (your original investment). Keep on repeating whenever it rises to your desired profit booking level.

This is highly inadvisable, as your portfolio size is too small, and the demat charges will be relatively high, if you sell proportionate shares in each item. This was just a thought that came to my mind.

Cheers!

2 Likes

Theoretically investing in stocks (and finding out time when you want to sell it) calls for very high amount of study, conviction and knowledge micro/macro environments. Equity mutual funds which generate 10-15% returns in favorable market condition have battery of qualified employees who do this job, I would think that it will be very very difficult although not impossible that newbie can do better job

Fundamentally you should get advice from Independent financial advisor or get in touch with mutual fund advisor who has proven track record, to generate regular income.

Although there are multiple ways and no path is incorrect, a typical advisor will suggest multiple bucket strategy

Simplest is two bucket, in which regular income is generated from stable debt product SWP say from liquid fund. Other bucket high gain, high volatile product say equity mutual fund. He will plan in such a way that from equity to liquid money will go only from position of strength. ie Only when equity is doing good. He will plan in such a way that only partial profit booking happens in equity fund. This way Equity bucket will never dry up.

1 Like

One thing worth noting — that 14.71% shown by Zerodha is simple returns (unrealized P&L / invested), not XIRR. Zerodha’s “View portfolio XIRR” tab is notoriously unreliable and often shows

errors.

Your actual annualised return (XIRR) could be higher or lower depending on when you invested. If you put in ₹82k all at once 3 years ago, XIRR ≈ ~4.7%. If most of it was invested recently,

XIRR could be much higher.

On your actual question — withdrawing profits while keeping capital:

Partial booking: If VEDL is up 50%, sell half. Capital recovered, remaining shares are “free.”

Rebalancing: When any stock crosses 15% of portfolio, trim to 10% and park the rest in liquid funds.

At ₹82k scale, don’t overthink it. The bigger win right now is knowing your actual returns — not the Zerodha P&L number.

Any investing you do should be scalable do not worry if portfolio goes no where a year or two and change methods.

You can check dividend growth investing.

You can read

The Ultimate Dividend Playbook: Income, Insight, and Independence for Todays Investor by Josh Peters

Dividends Still Don’t Lie: The Truth About Investing in Blue Chip Stocks and Winning in the Stock Market by Kelley Wright

spbrunner a blogger I follow does this for decades, her blog inspires me. There are loads of bloggers on internet especially Canadian/European bloggers.

Just to give you an example VST Industries, do not take it as advice. I would normally look below parameters based on sector/industry I would modify the parameters a bit not a lot.

VSTIND

Dividend Yield: Ideally Between 3.5% and 6.5% (4.37%)

Number of Consecutive Years of Dividend Growth: Ideally At Least 10 (25 years)

Average 10y Annual Dividend Growth: Ideally between 5% and 10% (around 8%)

Average 10y Annual Earnings Growth: Ideally in line with or above dividend growth rates. ( around 6.6% slowing recently)

Dividend Payout Ratio: Ideally less than 75%, except for REITs and MLPs ( 74 to 80 % high)

Debt to Equity Ratio: Ideally 1:1 or less (debt free)

Net Margins: Ideally at least 5% (17%- 21%)

Return on Equity: Ideally at least 10% (16% t0 24%)

Fair Value Estimate: 299

Current Price:229

Upside % 30%

I hold VST currently.

Just to tell you it worked for me in past.

Patience is key, the price may not go no where but what you do with dividend counts, reinvesting dividend proceeds is kicker here. Keeps me engaged.

PS: Not an advisor I lost money using these parameters too. Not a serious investor more of hobby.

I usually check screeners, dividend yield funds for ideas. Surprisingly Parag Parikh ELSS Tax Saver Fund has yield of 3% I follow these too.