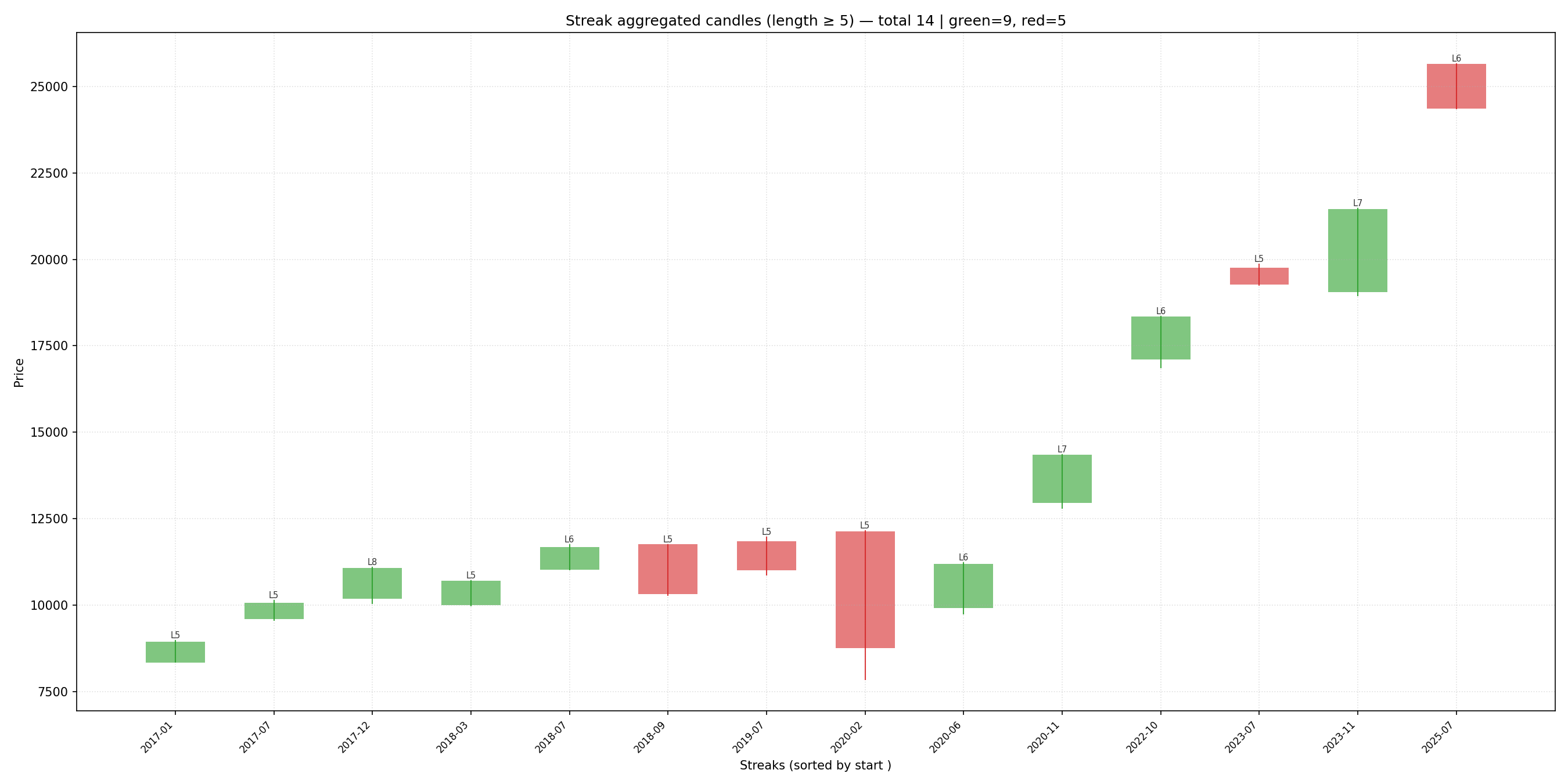

By adding-up the probabilities of all the outcomes that end-up with a streak

in a series of independent n red or green candles,

with the largest red-green streak (of length m).

Note: Very likely it is not intuitive to simply read the above in isolation.

Perhaps re-reading it after going through the n=1, n=2, …, n=3 calculations below, helps?

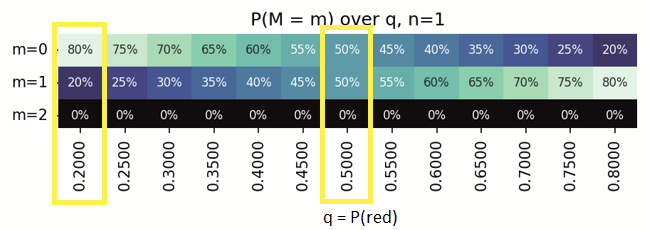

Looking at a simple case - Instead of 12 years, a 'series' of just 1 week, i.e. a single candle (n=1)

With a series of n=1, the possible outcomes are - either 1xGreen or 1xRed.

Looking at the column q=0.5,

- m=0 is streak of zero reds, Green (1/2) = 50%

- m=1 is streak of 1 red, Red (1/2) = 50%

- m=2 is impossible to have a run/streak of 2 reds in a series with 1 trial, 0%.

Similarly, looking at the column q=0.2,

- m=0 is streak of zero reds, Green (1 - 0.2) = 0.8 = 80%

- m=1 is streak of 1 red, Red (0.2) = 20%

- m=2 is impossible to have a run/streak of 2 reds in a series with 1 trial, 0%.

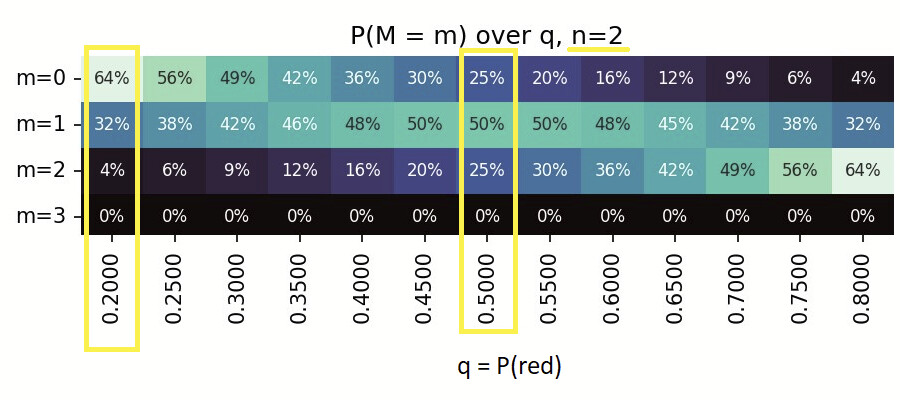

Extending this logic beyond 1 - a 'series' of 2 weeks, i.e. 2 candles (n=2)

With a series of n=2, the possible outcomes are - GreenGreen, GreenRed, RedGreen, RedRed.

Looking at the column q=0.5,

- m=0 is streak of zero reds, GreenGreen (1/4, 25%)

- m=1 is streak of 1 red, GreenRed+RedGreen (2/4, 50%)

- m=2 is streak of 2 reds, RedRed (1/4, 25%)

- m=3 is impossible to have a run/streak of 3 reds in a series with 2 trials, 0%.

Similarly, one can calculate the probabilities for biased (not 50-50%) probabilities as well.

with the same series of n=2,

the possible outcomes are still - GreenGreen, GreenRed, RedGreen, RedRed,

Looking at the column q=0.2,

however, we now have distinct probabilities (Green= 80%, Red = 20%).

- m=0 is streak of zero reds, GreenGreen - (0.8 x 0.8) = 0.64 = 64%

- m=1 is streak of 1 red, GreenRed+RedGreen - (0.8 x 0.2) + (0.2 x 0.8) = 0.32 = 32%

- m=2 is streak of 2 reds, RedRed - (0.2 x 0.2) = 0.04 = 4%

- m=3 is impossible to have a run/streak of 3 reds in a series with 2 trials, 0%.

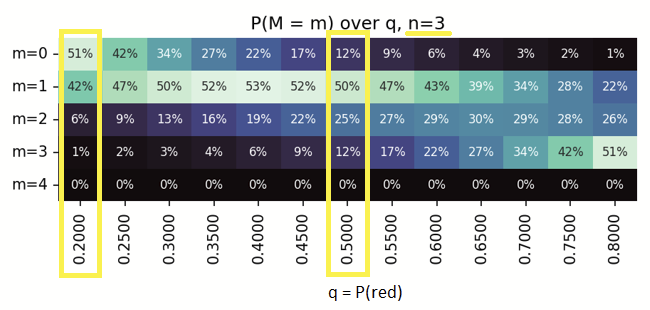

Can still do the mental-math? - Here's a 'series' of 3 weeks, i.e. 3 candles (n=3)

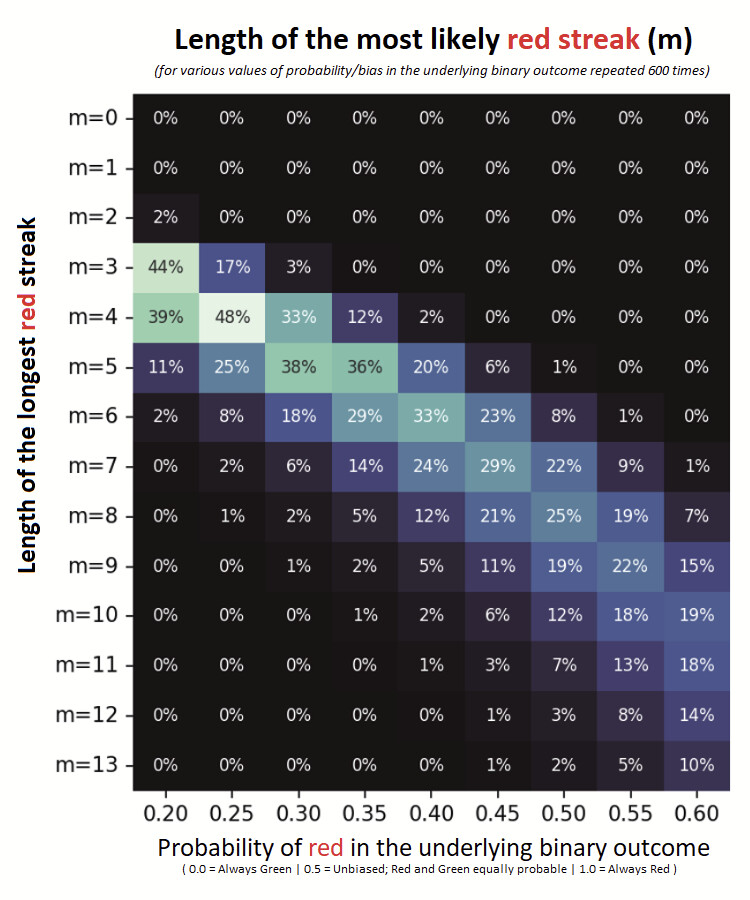

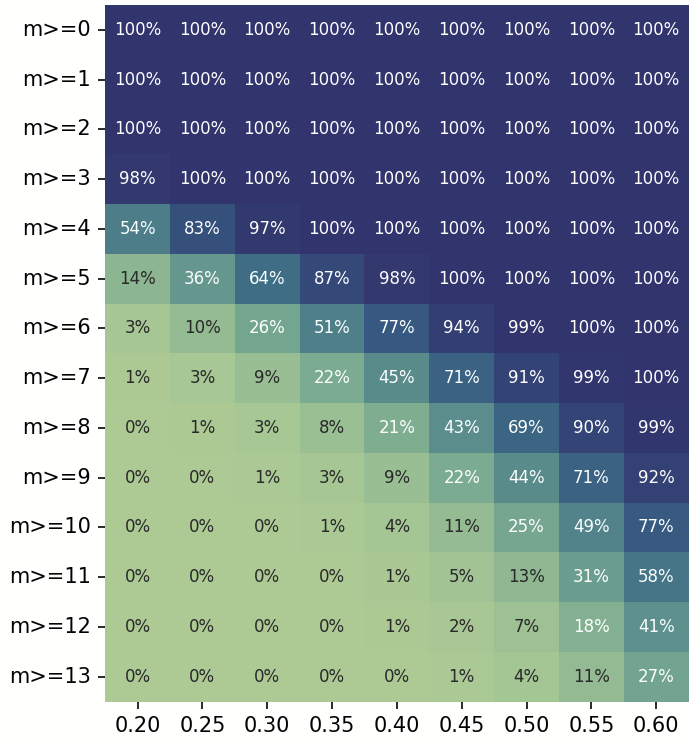

Extending this to a series of ~600 runs

(to arrive at the probabilities in the same ballpark as the number of weeks in 12 years),

we have the heatmap of probabilities of weekly red-streaks over 12 years.

Here’s the sample Python code to generate such a heatmap on the command-line.

heatmap_individual.py

"""Utilities to compute probabilities of runs in sequences of Bernoulli(q) trials.

Exposes:

- prob_no_run(n, r, q): P(no run of r consecutive successes within n trials)

- prob_exact_m_in_a_row(n, m, q): P(at least one run of exactly m and no run ≥ m+1)

"""

def prob_no_run(n: int, r: int, q: float) -> float:

"""Return P(no run of ``r`` consecutive successes in ``n`` Bernoulli(q) trials).

Dynamic-programming model:

- State ``dp[k]`` stores the probability that the current suffix of the

processed prefix ends with exactly ``k`` consecutive successes (``k`` in

``0..r-1``) and that no run of length ``r`` has occurred so far.

- On a success, the run length increases by 1 (shift right), but we cap at

``r-1`` by construction of the state space, which ensures we never count

states that already contain a forbidden run.

- On a failure, the run length resets to 0.

The answer is the total probability mass over all allowable end states.

"""

# Initialize all mass at run-length 0 before any trials

dp = [0.0] * r

dp[0] = 1.0

for _ in range(n):

# Next-step distribution over run-length states 0..r-1

nxt = [0.0] * r

# Success transitions: extend runs of length k to k+1 for k in [0, r-2]

for k in range(r - 1):

nxt[k + 1] += dp[k] * q

# Failure transitions: any state collapses to run-length 0

mass = sum(dp)

nxt[0] += mass * (1 - q)

dp = nxt

# Sum over all non-forbidden end states

return sum(dp)

def prob_exact_m_in_a_row(n: int, m: int, q: float) -> float:

"""Return P(at least one run of exactly ``m`` successes, and none of length ≥ ``m+1``).

Uses the identity:

P(no run ≥ m+1) − P(no run ≥ m) = P(at least one run of exactly m and no run ≥ m+1).

Special case ``m == 0`` corresponds to no successes at all, i.e., ``(1−q)^n``.

"""

if m == 0:

# No run ≥ 1 means no successes at all

return (1 - q) ** n

# Subtract the probabilities of having no run of length ≥ m and ≥ m+1

return prob_no_run(n, m + 1, q) - prob_no_run(n, m, q)

if __name__ == "__main__":

import argparse

# CLI to evaluate a single probability value for provided (n, m, q)

parser = argparse.ArgumentParser(description="Probability of at least one run of exactly length m (and no run ≥ m+1) in n Bernoulli(q) trials. For m=0, this equals (1−q)^n (no successes at all).")

parser.add_argument("-n", "--n", type=int, required=True, help="number of trials (n >= 0)")

parser.add_argument("-m", "--m", type=int, required=True, help="run length m (m >= 0)")

parser.add_argument("-q", "--q", type=float, required=True, help="success probability q in [0,1]")

parser.add_argument("--precision", type=int, default=2, help="decimal places to print (default 2)")

args = parser.parse_args()

if args.n < 0:

raise SystemExit("n must be >= 0")

if args.m < 0:

raise SystemExit("m must be >= 0")

if not (0.0 <= args.q <= 1.0):

raise SystemExit("q must be in [0, 1]")

prob = prob_exact_m_in_a_row(args.n, args.m, args.q)

print(f"{prob:.{args.precision}f}")

heatmap_table.py

"""Print a table of probabilities for runs of exactly length M across q values.

For each M in [0, m] and each q in [q_min, q_max] with step q_step, this CLI

prints P(at least one run of exactly length M and no run ≥ M+1) for n trials.

"""

import argparse

import sys

from typing import List, Optional, Sequence

from heatmap_individual import prob_exact_m_in_a_row

def generate_q_values(q_min: float, q_max: float, q_step: float) -> List[float]:

"""Return an inclusive list of q values from q_min to q_max with step q_step.

- If q_step <= 0, raises ValueError.

- If q_min > q_max, returns an empty list.

- Each value is clamped into [0.0, 1.0].

- Uses a small epsilon to ensure q_max is included despite FP accumulation.

"""

if q_step <= 0:

raise ValueError("q_step must be > 0")

if q_min > q_max:

return []

values: List[float] = []

epsilon = 1e-12 # Tolerance to include the upper bound

current = q_min

# Include q_max within tolerance of floating-point arithmetic

while current <= q_max + epsilon:

q = current if current <= q_max else q_max

# Clamp to [0,1]

q = max(0.0, min(1.0, q))

values.append(q)

current += q_step

return values

def parse_args(argv: Optional[Sequence[str]] = None) -> argparse.Namespace:

"""Parse CLI arguments for the probability table generator."""

parser = argparse.ArgumentParser(

description=(

"Print a table of probabilities of at least one run of exactly length M (no run ≥ M+1)\n"

"Rows: M = 0..m; Columns: q from q_min..q_max in steps of q_step."

)

)

parser.add_argument("-n", "--n", type=int, required=True, help="number of trials (n >= 0)")

parser.add_argument("-m", "--m", type=int, required=True, help="max run length row index (m >= 0)")

parser.add_argument("--q-min", type=float, default=0.1, help="min q (default 0.1)")

parser.add_argument("--q-max", type=float, default=0.8, help="max q (default 0.8)")

parser.add_argument("--q-step", type=float, default=0.05, help="step for q (default 0.05)")

parser.add_argument("--precision", type=int, default=4, help="decimal places to print (default 4)")

parser.add_argument("--sep", type=str, default="\t", help="column separator (default TAB)")

return parser.parse_args(argv)

def validate_args(args: argparse.Namespace) -> None:

"""Validate parsed arguments; raise ValueError with a helpful message if invalid."""

if args.n < 0:

raise ValueError("n must be >= 0")

if args.m < 0:

raise ValueError("m must be >= 0")

if not (0.0 <= args.q_min <= 1.0 and 0.0 <= args.q_max <= 1.0):

raise ValueError("q_min and q_max must be in [0, 1]")

if args.q_step <= 0:

raise ValueError("q_step must be > 0")

def print_probability_table(

n: int,

m: int,

q_values: List[float],

precision: int,

sep: str,

) -> None:

"""Print the probability table.

- The header row lists q values.

- Each subsequent row corresponds to a run length M in [0, m].

"""

row_label_width = max(4, len(str(m)))

header_cells = [" " * row_label_width] + [f"{q:.{precision}f}" for q in q_values]

print(sep.join(header_cells))

separator_row = ["-" * row_label_width] + ["-" * len(h) for h in header_cells[1:]]

print(sep.join(separator_row))

for run_length_m in range(0, m + 1):

row_cells = [str(run_length_m).rjust(row_label_width)]

for q in q_values:

probability = prob_exact_m_in_a_row(n, run_length_m, q)

row_cells.append(f"{probability:.{precision}f}")

print(sep.join(row_cells))

def main(argv: Optional[Sequence[str]] = None) -> int:

"""Program entry point.

Parses arguments, validates them, generates q values, and prints the table.

Returns a process exit code (0 for success).

"""

try:

args = parse_args(argv)

validate_args(args)

q_values = generate_q_values(args.q_min, args.q_max, args.q_step)

if not q_values:

raise ValueError("Empty q range; ensure q_min <= q_max")

print_probability_table(

n=args.n,

m=args.m,

q_values=q_values,

precision=args.precision,

sep=args.sep,

)

return 0

except ValueError as exc:

print(str(exc), file=sys.stderr)

return 2

if __name__ == "__main__":

raise SystemExit(main())

NOTE: The above code snippets were generated using LLM assistance.

Subsequently manually reviewed, and output sanity-checked for small sample-sizes.

(probably the weakest link in this entire chain of thought? )

No simulation. Computing each of them as seen above.

While i originally did it intuitively, apparently the formal keyword for it is an I.I.D. - Bernoulli trial.

(something i found out as part of trying to explain this today. Thanks for the review  )

)